ID : MRU_ 428598 | Date : Oct, 2025 | Pages : 241 | Region : Global | Publisher : MRU

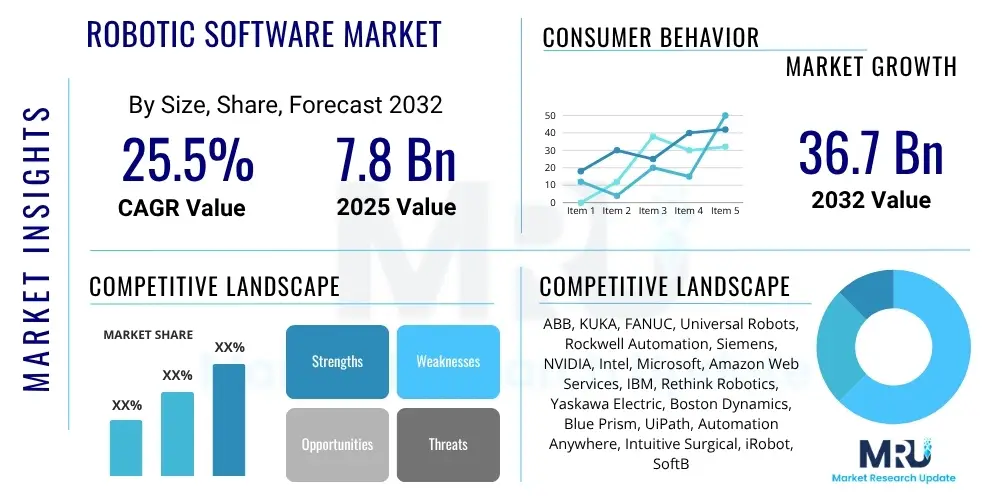

The Robotic Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2025 and 2032. The market is estimated at USD 7.8 Billion in 2025 and is projected to reach USD 36.7 Billion by the end of the forecast period in 2032.

The Robotic Software Market encompasses the development, deployment, and maintenance of programs that control, manage, and facilitate the operation of robotic systems across diverse applications. This software forms the intelligent core of robots, enabling them to perceive, process information, make decisions, and execute tasks autonomously or semi-autonomously. Its essential function is to bridge the gap between hardware capabilities and desired operational outcomes, transforming mere mechanical systems into sophisticated, adaptable tools capable of performing complex functions in dynamic environments.

Product descriptions within this market range from low-level operating systems and middleware that provide foundational communication and control, to high-level application software that dictates specific tasks, integrates artificial intelligence algorithms, and manages human-robot interaction. Key benefits derived from robust robotic software include enhanced operational efficiency, superior precision in task execution, improved safety in hazardous environments, and significant cost reductions through automation. These advantages are crucial across industries, driving widespread adoption.

Major applications span industrial automation in manufacturing, precise surgical assistance in healthcare, complex logistics and warehousing operations, advanced defense and security systems, and an expanding array of service robotics in commercial and domestic settings. The primary driving factors for market expansion include the surging global demand for automation to optimize productivity, rapid advancements in artificial intelligence and machine learning technologies, the decreasing cost of robotic hardware, and the transformative impact of Industry 4.0 initiatives that prioritize smart, connected systems.

The Robotic Software Market is undergoing a significant transformation driven by converging business trends, evolving regional dynamics, and specialized segment growth. Key business trends indicate a strong shift towards cloud-based robotics solutions, enabling greater scalability, remote management, and collaborative robot (cobot) functionalities. There is an increasing focus on human-robot interaction (HRI) software, aiming to make robotic systems more intuitive and safer for co-working environments. Additionally, AI-driven adaptive learning capabilities are becoming paramount, allowing robots to refine their performance over time and handle unstructured tasks more effectively, moving beyond pre-programmed instructions.

From a regional perspective, the Asia Pacific region continues to dominate the market, primarily fueled by extensive manufacturing automation in countries like China, Japan, and South Korea, coupled with significant government investments in robotics research and deployment. North America stands as a hub for innovation and R&D, particularly in advanced AI and specialized service robotics software, demonstrating high adoption rates in logistics and healthcare. Europe maintains a strong position in industrial automation, with robust demand from the automotive and electronics sectors, alongside a growing emphasis on ethical AI and regulatory frameworks for robotic deployment.

Segment trends reveal accelerated growth in application-specific software tailored for critical industries such as automotive assembly, precise surgical operations, and intelligent warehouse management systems. Middleware and operating systems segments are also experiencing innovation, with open-source platforms like ROS (Robot Operating System) gaining broader industry acceptance for their flexibility and community support. The increasing sophistication of these software solutions is enabling robots to perform more complex, nuanced, and value-added tasks, thereby expanding their market penetration and utility across a wider spectrum of industries.

User inquiries regarding AI's influence on the Robotic Software Market frequently center on how artificial intelligence enhances robot capabilities, the implications for human labor, the ethical considerations of autonomous systems, and the future trajectory of human-robot collaboration. Users are keen to understand how AI-powered robotic software moves beyond simple automation to enable adaptive learning, real-time decision-making, and more natural interaction. There is considerable interest in predictive maintenance, advanced vision systems, and natural language processing capabilities that AI brings to robotics, while simultaneously expressing concerns about job displacement, data privacy, and the responsible development of increasingly intelligent machines. Expectations are high for AI to unlock new levels of efficiency, flexibility, and autonomy in robotic operations, transforming various industries.

The Robotic Software Market is profoundly influenced by a complex interplay of drivers, restraints, opportunities, and broader impact forces that shape its growth trajectory and adoption. Key drivers include the escalating global demand for industrial and service automation across sectors like manufacturing, logistics, and healthcare, propelled by the pursuit of higher productivity, reduced operational costs, and enhanced quality control. The rapid evolution and integration of artificial intelligence and machine learning capabilities into robotic systems are also significant growth catalysts, enabling robots to perform more complex, adaptive, and intelligent tasks. Furthermore, the persistent challenge of labor shortages in developed economies and the imperative for improved workplace safety drive organizations to invest in advanced robotic solutions controlled by sophisticated software.

However, the market faces notable restraints such as the substantial initial investment required for deploying advanced robotic systems, which can be a barrier for small and medium-sized enterprises. The inherent complexity of integrating robotic software with existing operational technology (OT) and information technology (IT) infrastructures often necessitates specialized expertise and can lead to implementation challenges. Concerns surrounding data security, privacy, and potential cyber vulnerabilities in networked robotic systems also act as deterrents. Moreover, the shortage of a skilled workforce capable of developing, deploying, and maintaining sophisticated robotic software, coupled with ethical and societal concerns regarding automation-induced job displacement, presents ongoing challenges.

Opportunities for market expansion are abundant, particularly in the burgeoning fields of cloud robotics, which offers scalable and flexible solutions, and in the continued development of human-robot collaboration (HRC) technologies that foster safer and more efficient human-machine partnerships. The expanding scope of service robotics in sectors like retail, hospitality, and agriculture, alongside the increasing customization of software solutions for niche applications, presents significant growth avenues. Furthermore, emerging markets with burgeoning industrialization and digitalization initiatives represent untapped potential for robotic software adoption. Impact forces such as rapid technological advancements in AI, sensors, and connectivity, alongside evolving regulatory landscapes concerning autonomous systems and data governance, play a pivotal role in shaping market dynamics. Economic conditions, geopolitical stability, and the varying levels of societal acceptance of robotics also exert considerable influence on market penetration and investment trends.

The Robotic Software Market is broadly segmented based on various attributes including component, robot type, application, deployment, and industry vertical, allowing for a detailed understanding of market dynamics and growth pockets. This comprehensive segmentation highlights the diverse ecosystem of robotic software, from foundational operating systems to highly specialized application modules, and its tailored adoption across a multitude of industries and operational needs. Each segment contributes uniquely to the market's overall expansion, reflecting the increasing sophistication and versatility of robotic solutions.

The value chain for the Robotic Software Market is characterized by a series of integrated activities that transform raw intellectual property into deployable robotic intelligence, delivering value to end-users. The upstream segment of the value chain primarily involves research and development activities, where software developers, algorithm designers, AI specialists, and operating system architects create the foundational frameworks and advanced functionalities. This stage also includes the development of core middleware components and specialized libraries that interface with diverse robotic hardware and sensors, often relying on input from component providers for processors, memory, and communication modules. Intellectual property generation and patenting are critical aspects at this initial stage, forming the bedrock for competitive differentiation.

Moving downstream, the value chain encompasses the integration, customization, and deployment of robotic software solutions. System integrators play a pivotal role here, tailoring generic software platforms to specific application needs and seamlessly merging them with robotic hardware and existing operational infrastructures. This segment also includes training and support services, ensuring optimal performance and user proficiency. The distribution channels for robotic software are varied, including direct sales from software vendors to large enterprise clients, partnerships with robot manufacturers who bundle software with their hardware, and indirect sales through a network of certified system integrators and value-added resellers. Online marketplaces and cloud-based platforms are also emerging as significant indirect channels, especially for specialized modules and updates.

Direct distribution often involves dedicated sales teams engaging directly with end-users in key industry verticals, offering bespoke solutions and ongoing technical support. Indirect distribution channels, on the other hand, leverage the reach and expertise of partners to penetrate diverse markets and cater to a wider array of customers, particularly smaller enterprises or those requiring localized support. Both direct and indirect models are crucial for market penetration, with the choice often depending on the complexity of the solution, the target customer segment, and the geographic scope. This interconnected value chain ensures that sophisticated robotic software is effectively developed, delivered, and integrated to meet the evolving demands of various industries.

Potential customers for Robotic Software span a wide array of industries and organizational sizes, reflecting the increasing versatility and essential nature of robotic automation. Manufacturing companies, particularly in the automotive, electronics, and general machinery sectors, represent a significant segment, leveraging robotic software for assembly, welding, material handling, and quality inspection to enhance production efficiency and precision. Logistics and warehousing firms are also primary buyers, utilizing software-driven autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) for inventory management, sorting, and fulfillment, driven by the demands of e-commerce and supply chain optimization.

The healthcare sector is rapidly adopting robotic software for applications ranging from surgical assistance and rehabilitation robots to pharmacy automation and patient monitoring systems, aiming to improve patient outcomes, reduce operational costs, and support medical professionals. Defense and security organizations are investing in robotic software for surveillance, reconnaissance, hazardous environment operations, and autonomous vehicle control, emphasizing reliability and mission-critical performance. Furthermore, the burgeoning agricultural sector is increasingly deploying robotic software in precision farming, harvesting, and crop monitoring, driven by the need for increased yields and reduced labor dependency.

Beyond these industrial heavyweights, other key end-users include commercial service providers in retail and hospitality for tasks like cleaning and customer service, educational and research institutions for advanced robotics development, and even individual consumers for personal service robots like robotic vacuum cleaners or lawnmowers. The continuous development of more user-friendly interfaces and specialized applications is expanding the market to an even broader customer base, making robotic software an indispensable tool across nearly every facet of modern industry and daily life. The diverse needs of these customers drive innovation in software functionality, user experience, and integration capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 7.8 Billion |

| Market Forecast in 2032 | USD 36.7 Billion |

| Growth Rate | 25.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB, KUKA, FANUC, Universal Robots, Rockwell Automation, Siemens, NVIDIA, Intel, Microsoft, Amazon Web Services, IBM, Rethink Robotics, Yaskawa Electric, Boston Dynamics, Blue Prism, UiPath, Automation Anywhere, Intuitive Surgical, iRobot, SoftBank Robotics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Robotic Software Market is underpinned by a dynamic and continuously evolving technology landscape, where innovation in various domains converges to enhance robot capabilities and expand their application scope. Central to this landscape are advancements in Artificial Intelligence (AI) and Machine Learning (ML), which empower robots with cognitive functions such as perception, decision-making, natural language processing, and adaptive learning. These AI capabilities enable robots to move beyond repetitive, pre-programmed tasks to handle complex, unstructured environments and interact more intelligently with their surroundings and human counterparts. The integration of deep learning algorithms for computer vision, for instance, allows robots to accurately recognize objects, navigate, and perform intricate visual inspections, significantly improving their operational efficacy.

Cloud computing and edge computing are also pivotal technologies shaping the market, offering complementary solutions for robotic deployments. Cloud robotics leverages the immense computational power and storage capabilities of cloud platforms, enabling robots to access vast amounts of data, complex AI models, and shared knowledge bases, which is particularly beneficial for tasks requiring extensive data analysis or collaborative learning. Edge computing, conversely, brings processing power closer to the robot, minimizing latency for real-time decision-making in critical applications where immediate responses are paramount, such as in autonomous vehicles or manufacturing assembly lines. The combination of cloud and edge architectures provides a flexible and powerful framework for optimizing robotic intelligence and performance.

Furthermore, the Robot Operating System (ROS) continues to be a foundational technology, providing a flexible framework for robot software development, comprising a collection of tools, libraries, and conventions. Digital twin technology is gaining traction, allowing for the virtual modeling and simulation of robotic systems and their environments, which aids in design, testing, and predictive maintenance. Advancements in human-robot interaction (HRI) technologies, including natural language processing (NLP) and gesture recognition, are making cobots safer and more intuitive to operate alongside human workers, fostering a collaborative work environment. The synergy of these technologies creates intelligent, adaptable, and highly efficient robotic systems that are increasingly integral to modern industrial and service sectors.

Robotic software refers to the programming and operating systems that enable robots to perform tasks. It processes sensor data, plans actions, controls movement, and facilitates human interaction, allowing robots to operate autonomously or semi-autonomously across various applications.

AI significantly enhances robotic software by enabling advanced capabilities such as adaptive learning, real-time decision-making, sophisticated computer vision, natural language processing, and predictive maintenance. This allows robots to perform complex tasks, understand human intent, and adapt to dynamic environments more effectively.

Key applications driving market growth include industrial automation in manufacturing (assembly, welding, material handling), logistics and warehousing (autonomous mobile robots), healthcare (surgical assistance, pharmacy automation), defense and security, and various professional and personal service robotics.

The main challenges include high initial investment costs for deployment, integration complexities with existing systems, cybersecurity risks, a persistent shortage of skilled professionals for development and maintenance, and ethical concerns regarding job displacement and autonomous decision-making.

The Asia Pacific region, particularly China, Japan, and South Korea, leads in adoption due to extensive manufacturing automation. North America excels in R&D and specialized service robotics, while Europe is strong in industrial automation and developing ethical AI frameworks for robotics.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.