ID : MRU_ 430325 | Date : Nov, 2025 | Pages : 243 | Region : Global | Publisher : MRU

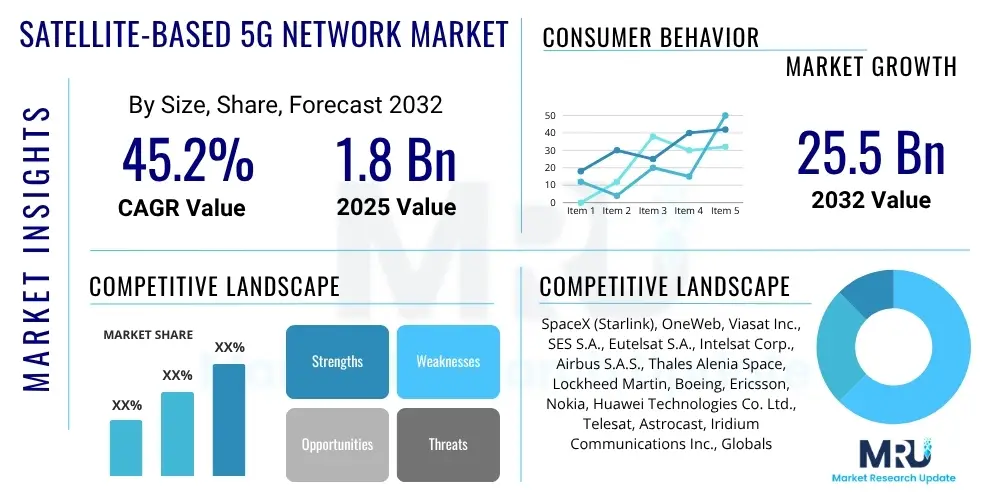

The Satellite-based 5G Network Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 45.2% between 2025 and 2032. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 25.5 Billion by the end of the forecast period in 2032.

The Satellite-based 5G Network market represents a critical evolution in global telecommunications, aiming to extend the capabilities and reach of 5G infrastructure beyond traditional terrestrial limitations. This market encompasses the development, deployment, and operation of satellite constellations and associated ground infrastructure designed to integrate seamlessly with 5G networks, providing ubiquitous connectivity. The primary product is the provision of 5G services—including enhanced mobile broadband (eMBB), massive machine-type communications (mMTC), and ultra-reliable low-latency communications (URLLC)—leveraging satellites for backhaul, direct-to-device connectivity, and extending coverage to unserved or underserved areas, particularly remote, rural, maritime, and aerial regions. This integration overcomes geographical constraints, offering unparalleled network resilience and accessibility.

Major applications of satellite-based 5G networks include bridging the digital divide by providing internet access in remote locations, enabling global IoT and M2M communications for diverse industries such as agriculture, logistics, and smart infrastructure, and supporting critical communications for disaster recovery and defense operations. Furthermore, it facilitates enhanced mobile broadband for maritime and aviation sectors, ensuring high-speed, low-latency connectivity even in the most isolated environments. The benefits derived from this market are substantial, including truly global coverage, increased network resilience through diversified infrastructure, reduced infrastructure costs in difficult terrains, and the enablement of new services and applications that require pervasive connectivity, such as autonomous vehicles and smart cities.

Driving factors for the growth of this market are multifold. A significant driver is the escalating global demand for ubiquitous, high-speed connectivity, particularly for emerging applications like IoT, AI-powered services, and augmented reality. The limitations of terrestrial infrastructure in reaching remote areas naturally push for satellite solutions. Moreover, the rapid advancement in satellite technology, specifically the proliferation of Low Earth Orbit (LEO) constellations, which promise lower latency and higher throughput, is making satellite-based 5G a technically and economically viable option. Government initiatives to promote digital inclusion and investment from both public and private sectors in next-generation communication infrastructure further accelerate market expansion.

The Satellite-based 5G Network market is experiencing dynamic growth, propelled by the relentless demand for global connectivity and the strategic integration of space-based assets into terrestrial 5G ecosystems. Key business trends indicate a strong focus on strategic partnerships between satellite operators, mobile network operators (MNOs), and technology providers to develop hybrid network architectures. There is an increasing emphasis on standardizing satellite-5G integration through 3GPP Release 17 and beyond, fostering interoperability and accelerating commercial deployments. Furthermore, significant investments are pouring into the launch of large LEO satellite constellations, fundamentally transforming the economics and technical capabilities of satellite communications by offering lower latency and higher bandwidth compared to traditional GEO satellites.

Regional trends reveal that North America and Europe are at the forefront of innovation and commercial adoption, driven by robust R&D, early trials, and the presence of major aerospace and telecommunications companies. The Asia Pacific region is rapidly emerging as a critical growth hub, spurred by substantial government investments in digital infrastructure, the vast geographical expanse requiring connectivity solutions, and a rapidly expanding mobile subscriber base. Latin America, the Middle East, and Africa present immense potential, primarily due to large unserved populations and a pressing need to bridge the digital divide, making satellite-based 5G a crucial enabler for socio-economic development in these regions.

Segment trends highlight that the Low Earth Orbit (LEO) segment by orbit type is projected to witness the most substantial growth, attributed to its inherent advantages in latency and capacity suitable for 5G applications. In terms of components, the services segment, particularly managed and professional services, is expected to expand significantly as operators seek expertise in deploying and maintaining complex satellite-terrestrial integrated networks. Among end-users, Mobile Network Operators (MNOs) will remain the largest segment, leveraging satellite solutions for backhaul and extending rural coverage, while government and defense applications, alongside maritime and aviation, are also rapidly adopting these solutions for critical and remote communications. Enhanced Mobile Broadband (eMBB) and IoT backhaul are poised to be the leading application segments driving market demand.

User inquiries concerning AI's influence on the Satellite-based 5G Network Market primarily revolve around how artificial intelligence can optimize network performance, enable predictive maintenance, enhance security, and facilitate intelligent resource management within these complex hybrid infrastructures. Common questions explore AI's role in dynamic spectrum allocation, beamforming optimization for satellite communications, managing vast amounts of data generated by LEO constellations, and ensuring seamless handovers between satellite and terrestrial networks. There is significant interest in AI's capacity to automate network operations, predict potential outages, and provide personalized service delivery, ultimately addressing concerns about operational complexity, efficiency, and the scalability of integrated 5G environments. Users anticipate AI will be instrumental in making satellite-based 5G networks more autonomous, reliable, and cost-effective, while also raising questions about the ethical implications and data privacy aspects of extensive AI deployment in critical communication infrastructure.

The Satellite-based 5G Network market is influenced by a powerful combination of drivers, restraints, opportunities, and external impact forces. A primary driver is the accelerating global demand for ubiquitous connectivity, particularly in remote and underserved areas where terrestrial infrastructure is economically unfeasible or geographically challenging. The exponential growth of IoT and M2M communications further fuels this demand, requiring pervasive network coverage for diverse applications across industries like smart agriculture, logistics, and environmental monitoring. The imperative to bridge the global digital divide, coupled with the increasing need for enhanced mobile broadband (eMBB) for high-speed data access in critical sectors such as maritime and aviation, are also significant driving forces. Furthermore, the strategic importance of resilient and tactical communications for government and defense applications underscores the value of satellite-based solutions, ensuring continuity of operations in challenging environments.

However, the market faces notable restraints that could temper its growth trajectory. The initial capital expenditure required for deploying extensive satellite constellations, particularly LEO systems, and associated ground infrastructure remains extremely high, posing a significant barrier to entry for new players and demanding substantial investment from existing ones. Regulatory complexities, including international spectrum allocation and licensing procedures, create bureaucratic hurdles and can delay market entry or expansion. Latency concerns, although significantly reduced by LEO satellites compared to GEOs, still present a challenge for ultra-low latency applications crucial for certain 5G use cases. Additionally, potential cybersecurity risks associated with a vast, distributed satellite network and the challenges of managing interference with terrestrial networks pose ongoing technical and operational challenges.

Despite these restraints, numerous opportunities abound for market participants. The ongoing development and deployment of mega LEO satellite constellations by companies like Starlink and OneWeb offer unprecedented capacity and global coverage, creating new avenues for direct-to-device connectivity and seamless integration with terrestrial 5G. The continuous advancements in Non-Terrestrial Network (NTN) integration within 3GPP standards are facilitating greater interoperability and standardization, simplifying deployment. The synergy with edge computing allows for processing data closer to the source, reducing latency and enabling new AI-driven applications. Furthermore, the market presents opportunities in enabling private 5G networks for enterprises in remote industrial settings and providing critical disaster recovery services, ensuring communication resilience when terrestrial networks fail. External impact forces, such as rapid technological advancements in satellite propulsion, antenna design, and ground station capabilities, continue to lower costs and improve performance. The evolving geopolitical landscape influences national investments in space infrastructure, while environmental sustainability goals drive demand for greener satellite technologies. Economic volatility can impact investment cycles, and evolving consumer demands for seamless, high-performance connectivity constantly push the boundaries of network innovation.

The Satellite-based 5G Network market is comprehensively segmented across various dimensions to provide a granular understanding of its structure, dynamics, and potential growth areas. These segmentations allow for detailed analysis of market behavior, competitive landscapes, and strategic opportunities, catering to diverse needs ranging from technical components to end-user applications. Understanding these segments is crucial for stakeholders to tailor their product offerings, penetrate specific markets, and formulate effective business strategies, reflecting the hybrid and complex nature of integrating space and terrestrial communication technologies.

The market is primarily segmented by Orbit Type, Component, End-User, and Application. Each of these categories further breaks down into sub-segments, representing distinct technological approaches, product offerings, customer groups, and use cases within the evolving satellite-based 5G ecosystem. The rapid technological advancements and increasing investments in the space sector are continually redefining these segments, necessitating a flexible and forward-looking analytical framework to capture emerging trends and innovations.

The value chain for the Satellite-based 5G Network market is intricate, involving a diverse set of stakeholders across various stages, from initial research and development to final service delivery. Upstream analysis focuses on the foundational elements, including satellite manufacturing, which involves the design, construction, and launch of satellites (LEO, MEO, GEO). Key players in this stage are aerospace companies, specialized satellite manufacturers, and launch service providers. This segment also includes the providers of critical components for satellites, such as payloads, transponders, antennas, and power systems, as well as the developers of core satellite communication technologies and software defined radios.

Midstream activities primarily involve the operation and management of the satellite constellations and the associated ground segment. This encompasses satellite operators who own and manage the constellations, providing wholesale capacity. It also includes ground segment providers responsible for developing and deploying earth stations, gateways, network control centers, and user terminals that interface with both satellites and terrestrial 5G networks. Furthermore, network integrators play a crucial role in ensuring seamless interoperability between the space-based and terrestrial components of the 5G network, often involving complex software and hardware integration, network slicing, and virtualization technologies.

Downstream analysis centers on the distribution channels and end-user engagement. Connectivity services are delivered through various channels, including direct and indirect models. Direct distribution involves satellite operators or specialized service providers offering satellite-based 5G services directly to end-users, such as enterprises in remote locations, government agencies, or maritime and aviation customers. Indirect distribution heavily relies on partnerships with Mobile Network Operators (MNOs) and Internet Service Providers (ISPs), who integrate satellite capabilities into their existing terrestrial 5G offerings to extend coverage, provide backhaul, or enhance network resilience. This hybrid model allows MNOs to leverage satellite infrastructure to bridge connectivity gaps, particularly in rural and remote areas, thereby expanding their customer base and offering comprehensive global coverage solutions to their subscribers.

The Satellite-based 5G Network market caters to a broad spectrum of potential customers and end-users, driven by the inherent advantages of satellite communication in providing ubiquitous and resilient connectivity. These customers are primarily entities that operate in geographically challenging areas, require highly reliable communication, or demand global reach beyond the scope of traditional terrestrial networks. Mobile Network Operators (MNOs) represent a significant customer segment, seeking to augment their terrestrial 5G networks by leveraging satellites for backhaul in underserved regions, extending rural coverage, and ensuring network resilience during outages. Their objective is to achieve true national or even global coverage without incurring exorbitant costs for deploying physical fiber or cell towers in difficult terrains.

Enterprises across various industries form another substantial customer base. This includes sectors such as mining, oil and gas, agriculture, logistics, and utilities, which often operate in remote locations and require reliable connectivity for IoT sensors, asset tracking, remote operations, and private 5G networks. For these businesses, satellite-based 5G enables efficient data collection, real-time monitoring, and automation, leading to improved operational efficiency and safety in environments where terrestrial communication is unreliable or non-existent. Furthermore, government and defense organizations are crucial end-users, demanding secure, robust, and highly available communication for critical missions, disaster response, border control, and military operations, where terrestrial infrastructure may be compromised or unavailable.

Additional potential customers include maritime and aviation sectors, where ships, oil rigs, and aircraft require continuous high-speed internet and communication services for operational efficiency, crew welfare, and passenger connectivity. The growing demand for in-flight and at-sea broadband, coupled with real-time data transmission for navigation and logistics, makes satellite-based 5G an indispensable solution for these industries. Finally, individuals and communities in rural and remote areas, often part of the global digital divide, represent a vast untapped market. Satellite-based 5G offers these populations the opportunity to access high-speed internet, enabling education, healthcare, e-commerce, and social connectivity, thereby fostering socio-economic development in regions historically excluded from the digital revolution.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2032 | USD 25.5 Billion |

| Growth Rate | 45.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SpaceX (Starlink), OneWeb, Viasat Inc., SES S.A., Eutelsat S.A., Intelsat Corp., Airbus S.A.S., Thales Alenia Space, Lockheed Martin, Boeing, Ericsson, Nokia, Huawei Technologies Co. Ltd., Telesat, Astrocast, Iridium Communications Inc., Globalstar, Kymeta Corporation, Gilat Satellite Networks, Qualcomm Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Satellite-based 5G Network market is underpinned by a dynamic and evolving technology landscape, driven by continuous innovation in both space and terrestrial communication domains. At its core are advanced satellite technologies, particularly the development and deployment of mega-constellations of Low Earth Orbit (LEO) satellites. These LEO systems, such as Starlink and OneWeb, fundamentally alter the economics and performance of satellite communication by offering significantly lower latency and higher data throughput compared to traditional Geostationary Earth Orbit (GEO) satellites. Key innovations in satellite design include smaller, more agile satellites, mass production capabilities to reduce costs, and sophisticated on-board processing for enhanced flexibility and capacity. Phased array antennas, both on satellites and user terminals, are critical for efficient beam steering and managing multiple simultaneous connections.

Another crucial technological pillar is the seamless integration with terrestrial 5G networks, primarily through the standardization efforts of 3GPP for Non-Terrestrial Networks (NTN). This involves the development of specific interfaces and protocols that allow 5G devices to connect directly to satellites or use satellites for backhaul, ensuring interoperability and global roaming. Technologies like network slicing, derived from 5G core networks, are being adapted to create virtualized, isolated network segments over satellite links, tailored for specific applications such as IoT, eMBB, or URLLC. Software Defined Networking (SDN) and Network Functions Virtualization (NFV) are also pivotal, enabling greater flexibility, automation, and efficient management of the complex hybrid satellite-terrestrial infrastructure, allowing operators to dynamically reconfigure network resources as demand dictates.

Furthermore, advanced modulation and coding schemes (AMCS) are employed to maximize spectral efficiency over satellite links, enhancing data rates and link robustness. Artificial Intelligence (AI) and Machine Learning (ML) play an increasingly vital role in optimizing network operations, from dynamic spectrum allocation and predictive maintenance of satellite components to intelligent traffic management across hybrid networks. Edge computing, potentially deployed in ground stations or even on larger LEO satellites, brings computational power closer to the data source, reducing latency and enabling real-time processing for critical 5G applications. The synergy of these technologies—advanced satellite platforms, NTN integration, SDN/NFV, AI/ML, and edge computing—creates a robust and scalable architecture for the future of ubiquitous 5G connectivity.

A Satellite-based 5G Network integrates satellite communication systems with terrestrial 5G infrastructure to extend network coverage, enhance capacity, and provide reliable connectivity, particularly in remote, rural, maritime, and aerial regions where traditional ground-based networks are challenging to deploy. It leverages satellites for backhaul, direct-to-device communication, and bridging geographical gaps in 5G services, encompassing technologies like LEO, MEO, and GEO satellites seamlessly interfaced with 5G core networks.

The primary benefits include truly ubiquitous global coverage, ensuring connectivity even in the most isolated areas, enhanced network resilience and redundancy through diversified communication paths, and significant cost savings in deploying infrastructure in difficult terrains. It also enables new applications requiring pervasive connectivity, such as global IoT, maritime and aviation broadband, and critical communications for disaster recovery, ultimately bridging the digital divide and fostering economic development in underserved regions.

Low Earth Orbit (LEO) satellites are becoming highly relevant due to their significantly lower latency and higher bandwidth capabilities, making them ideal for performance-sensitive 5G applications. While Geostationary Earth Orbit (GEO) satellites offer wide coverage for backhaul, their higher latency is less suitable for real-time 5G services. Medium Earth Orbit (MEO) satellites offer a balance but LEO constellations are driving the most transformative changes in direct-to-device and low-latency 5G connectivity due to their proximity to Earth.

The market faces several challenges, including the extremely high initial capital investment required for satellite constellation deployment and associated ground infrastructure. Regulatory complexities surrounding spectrum allocation and international licensing also pose significant hurdles. Technical challenges like managing latency for ultra-reliable low-latency communications (URLLC), ensuring cybersecurity across a distributed network, and mitigating interference with terrestrial networks are also persistent concerns that require ongoing innovation and standardization efforts to overcome.

AI significantly impacts satellite-based 5G by enabling advanced network optimization, including dynamic spectrum allocation, efficient beamforming, and intelligent traffic management across hybrid networks. It also powers predictive maintenance for satellites and ground stations, automates complex network orchestration, and enhances cybersecurity through real-time threat detection. AI is crucial for processing the vast amounts of data generated by LEO constellations and ensuring seamless handovers, leading to more autonomous, reliable, and cost-effective network operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.