ID : MRU_ 429475 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

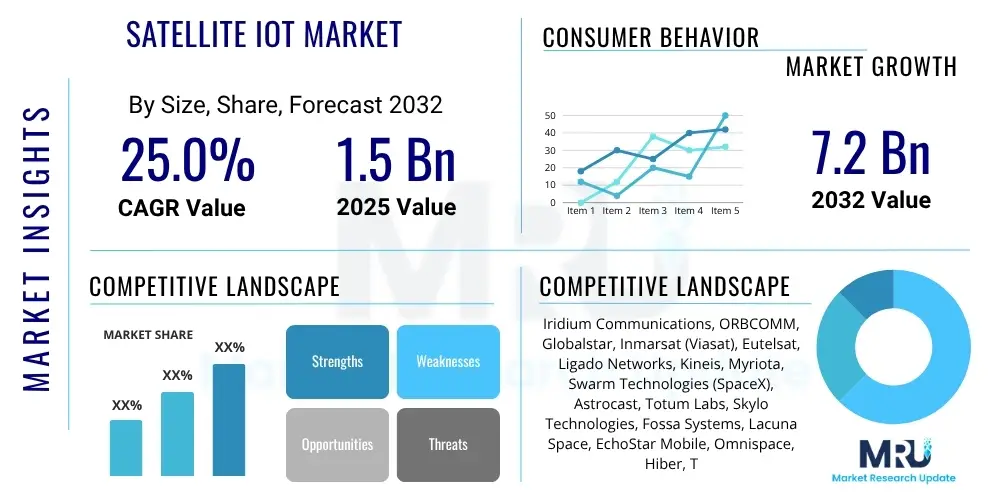

The Satellite IoT Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.0% between 2025 and 2032. The market is estimated at USD 1.5 billion in 2025 and is projected to reach USD 7.2 billion by the end of the forecast period in 2032.

The Satellite IoT market represents a crucial technological convergence, integrating satellite communication capabilities with the burgeoning ecosystem of Internet of Things (IoT) devices. This synergistic combination facilitates seamless data exchange in remote, underserved, and often hazardous environments where traditional terrestrial networks are either non-existent or unreliable. The primary objective is to provide ubiquitous, global connectivity for IoT sensors and devices, enabling real-time monitoring and control across vast geographical expanses, from deserts and oceans to polar regions.

The core product offerings within this market encompass a range of hardware and services. Hardware solutions include compact, energy-efficient satellite modems, transceivers, antennas, and specialized IoT sensors designed for low-power operation and robust data transmission. These devices leverage various satellite constellations, including geostationary (GEO), medium Earth orbit (MEO), and increasingly, low Earth orbit (LEO) satellites, each offering distinct advantages in terms of latency, bandwidth, and coverage cost. Major applications are diverse and critical, spanning asset tracking for logistics and supply chains, smart agriculture for optimizing crop yields, maritime monitoring for vessel and cargo safety, environmental sensing for climate data collection, and remote infrastructure management for utilities and oil and gas.

The benefits derived from Satellite IoT are substantial, offering unparalleled global coverage, inherent reliability in extreme operating conditions, enhanced data collection capabilities from previously inaccessible assets, and significant improvements in operational efficiency through automated monitoring and data-driven insights. These advantages are pivotal for industries seeking to extend their digital footprint beyond urban centers. The market's growth is predominantly driven by the pervasive expansion of IoT applications across numerous sectors, the escalating demand for truly pervasive connectivity, the continuous decline in satellite launch and operational costs, and the ongoing development of more compact, power-efficient, and affordable satellite communication terminals, making Satellite IoT solutions increasingly accessible and economically viable for a broader range of enterprises.

The Satellite IoT market is undergoing rapid transformation, characterized by dynamic business trends, evolving regional adoption patterns, and significant segmentation shifts. Key business trends include an increasing emphasis on strategic partnerships and collaborations between satellite operators, IoT platform providers, and vertical-specific solution integrators to deliver comprehensive, end-to-end services. There is a discernible shift towards hybrid connectivity models, seamlessly integrating satellite communication with terrestrial networks to optimize cost, latency, and reliability based on specific application requirements. Furthermore, the market is witnessing the emergence of innovative business models, such as "IoT-as-a-Service," which aim to simplify deployment and reduce capital expenditure for end-users, fostering broader adoption across industries.

Regionally, North America and Europe currently lead the market in terms of adoption, primarily driven by their advanced industrial infrastructures, significant investments in research and development, and strong demand from established sectors like oil and gas, agriculture, and transportation for enhanced asset visibility and operational efficiency. These regions benefit from a mature regulatory environment and a high concentration of key market players. Concurrently, the Asia Pacific (APAC) and Latin America regions are projected to exhibit the most rapid growth rates. In APAC, this surge is fueled by vast agricultural sectors, expanding maritime trade, and burgeoning logistics needs, particularly in countries like China, India, and Australia, where significant geographical areas lack terrestrial network coverage. Latin America's growth is spurred by the modernization of its agriculture and mining industries and the pressing need for connectivity in remote areas to monitor critical infrastructure and natural resources. The Middle East and Africa (MEA) region, while still nascent, presents substantial opportunities, especially in remote asset monitoring for oil and gas, utilities, and nascent smart agriculture initiatives, supported by government-led digital transformation agendas.

From a segmentation perspective, the market is experiencing notable trends. The Low Earth Orbit (LEO) satellite services segment is gaining significant traction, propelled by the deployment of mega-constellations that offer lower latency, higher bandwidth, and potentially more cost-effective solutions compared to traditional Geostationary (GEO) satellites. This shift is making Satellite IoT more appealing for latency-sensitive applications. The hardware segment is continuously innovating, with a focus on miniaturization, enhanced power efficiency, and reduced cost of satellite terminals, making them more accessible for a wider range of IoT devices. Simultaneously, the services segment, encompassing connectivity, data analytics, and managed services, is expanding rapidly. This growth is driven by the increasing demand for sophisticated data processing, advanced analytics, and seamless integration with existing enterprise systems, allowing businesses to extract actionable insights from the vast amounts of data collected by Satellite IoT networks, thereby driving efficiency and facilitating informed decision-making across various vertical applications.

Users frequently inquire about how Artificial Intelligence (AI) can fundamentally transform and enhance the capabilities of Satellite IoT systems. Common questions center on AI's ability to manage the massive influx of data generated by thousands, if not millions, of remote sensors, and how it can extract meaningful, actionable insights from this complex information. Concerns often arise regarding network optimization, particularly in dynamic satellite environments, and the potential for AI to automate critical functions like predictive maintenance for assets located in inaccessible areas. Users also express interest in AI's role in bolstering cybersecurity for satellite communications and its capacity to enable more autonomous, intelligent operations where human intervention is impractical or impossible. The overarching theme is the expectation that AI will unlock new efficiencies, improve decision-making, and expand the scope of what Satellite IoT can achieve.

The Satellite IoT market is significantly influenced by a confluence of driving forces, restraining factors, emerging opportunities, and broader impact forces that collectively shape its trajectory and potential. A primary driver is the accelerating demand for pervasive remote monitoring and control capabilities across diverse industries, spanning from agriculture to oil and gas, where terrestrial networks are either absent or unreliable. The exponential growth in the adoption of IoT devices across nearly every sector further fuels this demand, creating a critical need for global connectivity solutions. Moreover, the continuous decline in the cost of satellite communication technologies, particularly with the advent of LEO constellations and miniaturized terminals, makes Satellite IoT increasingly economically viable. The inherent need for ubiquitous connectivity, essential for global supply chain visibility, environmental conservation, and disaster response, acts as a fundamental impetus for market expansion.

Conversely, several restraints impede the market's full potential. The high initial investment required for deploying and maintaining satellite infrastructure, including ground stations and extensive satellite constellations, remains a significant barrier for new entrants and can increase service costs. Regulatory complexities, including spectrum allocation and licensing across different jurisdictions, pose challenges for global operators. The potential for signal interference, especially in congested orbital environments, can affect service reliability. Furthermore, in some legacy satellite systems, bandwidth limitations can constrain the volume and speed of data transmission, while persistent concerns regarding data privacy and the robust security of satellite-transmitted information continue to be critical considerations for enterprise adoption.

Despite these challenges, substantial opportunities are emerging, promising to unlock new avenues for growth. The vast untapped markets in developing regions, particularly in parts of Asia Pacific, Latin America, and Africa, present significant potential for Satellite IoT adoption in agriculture, resource management, and infrastructure development. The ongoing development of hybrid connectivity solutions, seamlessly integrating satellite with 5G and other terrestrial networks, offers enhanced flexibility and resilience. Advancements in Artificial Intelligence and Machine Learning (AI/ML) are creating opportunities for sophisticated data analytics and predictive capabilities, transforming raw data into actionable intelligence. Furthermore, the relentless miniaturization of satellite terminals and sensors, coupled with a growing global focus on environmental monitoring and efficient disaster response, positions Satellite IoT as a critical tool for addressing pressing global challenges, driving innovation and expanding its application scope. The interplay of technological advancements like LEO and 5G integration, economic shifts influencing data costs, evolving regulatory environments, and increasing environmental concerns collectively act as broad impact forces that dynamically reshape the competitive landscape and strategic imperatives within the Satellite IoT market.

The Satellite IoT market is intricately segmented to address the diverse needs of various industries and applications, providing a granular view of its structure and growth dynamics. This comprehensive segmentation allows for a precise analysis of technological adoption, service offerings, and end-user demand across different verticals. The market can be broadly categorized by components, which include the physical hardware necessary for communication and the extensive range of services that enable data transmission and analysis. Further divisions are made based on the type of satellite connectivity utilized, reflecting the technological advancements and strategic choices made by operators and users. The end-use industry and application segments illustrate the practical implementation and value proposition of Satellite IoT across a myriad of sectors, highlighting the specific pain points addressed and efficiencies gained.

Understanding these segments is crucial for stakeholders, as it informs product development, market entry strategies, and investment decisions. For instance, the demand for hardware might be driven by the deployment of new constellations, while the growth in services is often linked to the increasing sophistication of data analytics and managed solutions tailored for specific industrial requirements. The evolving landscape of connectivity types, particularly the shift towards LEO satellites, indicates a preference for lower latency and potentially higher data rates in certain applications. Analyzing the end-use industries reveals the sectors that are most receptive to Satellite IoT due to their inherent need for remote monitoring, global asset tracking, or critical communication in off-grid locations. This detailed segmentation therefore provides a roadmap for market participants to identify growth areas, competitive advantages, and unmet customer needs, ensuring that solutions are effectively aligned with market demands and technological capabilities.

The value chain of the Satellite IoT market is a complex ecosystem, encompassing various stages from component manufacturing to end-user deployment and service delivery. At the upstream end, the chain begins with foundational technology providers, including manufacturers of critical satellite components such as transponders, antennas, and ground station equipment, alongside IoT sensor providers, chipset manufacturers, and satellite launch service providers. These entities are responsible for developing and supplying the core technological infrastructure and hardware that forms the backbone of any Satellite IoT solution. Their innovation in areas like miniaturization, power efficiency, and signal processing directly impacts the capabilities and cost-effectiveness of the entire system.

Midstream activities involve satellite operators who own and manage the constellations, providing the actual connectivity services, and platform providers who offer the software and cloud infrastructure for data ingestion, processing, and management. This stage also includes system integrators who assemble disparate hardware and software components into a cohesive, functional solution tailored to specific client needs. The downstream segment of the value chain focuses squarely on the end-users, which comprise a broad spectrum of industries such as agriculture, maritime, oil and gas, logistics, and environmental monitoring, who ultimately deploy and utilize these Satellite IoT solutions to achieve their operational objectives. These end-users are the ultimate beneficiaries, leveraging the technology for enhanced tracking, monitoring, and control of their remote assets.

Distribution channels within the Satellite IoT market are multifaceted, accommodating the varied requirements of clients and the complexity of the solutions. Direct sales are common for large enterprises or government contracts, where satellite operators or dedicated solution providers engage directly with clients to offer highly customized services. Indirect channels involve partnerships with system integrators, value-added resellers (VARs), and telecommunication companies, who bundle Satellite IoT services with their existing offerings, extending market reach and providing localized support. Strategic alliances and collaborations are also prevalent, enabling companies to offer integrated solutions that might combine satellite connectivity with terrestrial IoT networks, cloud analytics, and specialized application development, thereby creating comprehensive, hybrid service models. These diverse channels ensure that Satellite IoT solutions can effectively reach a wide range of potential customers, from large multinational corporations to smaller, specialized operations.

The potential customers and end-users for Satellite IoT solutions are organizations and enterprises that operate in environments where traditional terrestrial connectivity is either unreliable, unavailable, or cost-prohibitive. These include industries that inherently require global reach for asset visibility, constant communication with remote infrastructure, or monitoring in geographically dispersed locations. Such customers are typically seeking enhanced operational efficiency, improved safety, regulatory compliance, and the ability to gather critical data from their assets regardless of their location on the planet. Their demand is driven by the necessity to overcome connectivity gaps and leverage real-time data for informed decision-making, ultimately leading to significant cost savings, optimized resource utilization, and increased productivity in challenging operational contexts.

Specifically, the primary buyers of Satellite IoT products and services span a wide array of sectors. This includes large-scale agricultural enterprises managing vast farms, maritime shipping companies needing to track vessels and cargo across oceans, and oil and gas exploration firms monitoring pipelines, wells, and offshore platforms in remote areas. Mining operations, transportation and logistics providers managing fleets across international borders, and utilities overseeing critical infrastructure like power grids and water pipelines in rural regions also represent significant customer segments. Furthermore, government agencies for defense, disaster management, environmental monitoring, and scientific research are key adopters, relying on Satellite IoT for robust, secure communication and data collection in critical missions. Essentially, any organization with remote assets or operations that require constant, dependable connectivity stands to benefit immensely from the unique capabilities offered by the Satellite IoT market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.5 billion |

| Market Forecast in 2032 | USD 7.2 billion |

| Growth Rate | 25.0% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Iridium Communications, ORBCOMM, Globalstar, Inmarsat (Viasat), Eutelsat, Ligado Networks, Kineis, Myriota, Swarm Technologies (SpaceX), Astrocast, Totum Labs, Skylo Technologies, Fossa Systems, Lacuna Space, EchoStar Mobile, Omnispace, Hiber, Thales Alenia Space, ST Engineering iDirect, Intelsat |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Satellite IoT market is characterized by a rapid evolution of diverse innovations, each contributing to the market's expansion and capabilities. Central to this landscape are the Low Earth Orbit (LEO) satellite constellations, which are increasingly favored over traditional Geostationary (GEO) satellites due to their significantly lower latency, faster data transmission speeds, and reduced power consumption for ground terminals. This shift enables more responsive and efficient communication for IoT devices, unlocking new applications that require near real-time data. Complementing satellite infrastructure are the various Low-Power Wide-Area Network (LPWAN) technologies, such as LoRaWAN and NB-IoT, which are being adapted for satellite communication. These technologies are crucial for enabling highly energy-efficient data transmission from battery-powered IoT sensors, ensuring long operational lifetimes in remote deployments.

Beyond the core connectivity, advancements in satellite modems, transceivers, and antennas are vital, leading to smaller, more robust, and more affordable ground terminals that can be easily integrated into a wide range of IoT devices. The market also heavily relies on sophisticated cloud-based IoT platforms for seamless data ingestion, processing, and management. These platforms provide the necessary infrastructure to handle the vast amounts of data collected from thousands of remote sensors, offering scalability and robust data storage solutions. Furthermore, the integration of edge computing capabilities is becoming increasingly important, allowing preliminary data processing and analytics to occur closer to the source, thereby reducing the volume of data transmitted over satellite links and minimizing latency for critical applications.

The strategic incorporation of Artificial Intelligence and Machine Learning (AI/ML) is profoundly transforming the technological landscape, moving beyond mere connectivity to intelligent data interpretation and operational optimization. AI algorithms are deployed for advanced data analytics, extracting actionable insights from complex datasets and enabling predictive maintenance for remote assets. AI also plays a crucial role in optimizing satellite resource allocation, dynamically managing network traffic, and enhancing cybersecurity protocols for robust and secure communication. The convergence of these advanced satellite technologies, LPWAN standards, cloud-based platforms, edge computing, and AI/ML is collectively driving the Satellite IoT market forward, enabling efficient, scalable, and cost-effective data transmission from millions of geographically dispersed IoT devices and fostering the development of previously impossible monitoring and control applications across various global industries.

Satellite IoT utilizes satellite networks to connect Internet of Things devices, providing ubiquitous global coverage, especially in remote or underserved areas where terrestrial networks (like cellular or Wi-Fi) are unavailable. It is ideal for applications requiring connectivity for mobile assets or static sensors in off-grid locations, ensuring data transmission from anywhere on Earth, unlike terrestrial IoT which relies on ground-based infrastructure with limited reach.

Key applications of Satellite IoT are diverse and critical, including global asset tracking and monitoring for logistics, fleet management across vast distances, smart agriculture for optimizing crop yields and livestock, maritime monitoring for vessel and cargo safety, environmental sensing for climate and ecological data, and remote infrastructure management for utilities, oil and gas, and mining operations.

LEO (Low Earth Orbit) satellites are profoundly impacting the Satellite IoT market by offering significantly lower latency, higher data transmission speeds, and potentially more cost-effective solutions compared to traditional Geostationary (GEO) satellites. Their proximity to Earth reduces signal delay and power consumption for ground terminals, making them ideal for a broader range of latency-sensitive and power-constrained IoT applications and accelerating overall market growth.

The Satellite IoT market faces several challenges, including the high initial investment required for deploying and maintaining satellite infrastructure, complex regulatory environments for spectrum allocation across international borders, the potential for signal interference, bandwidth limitations in some legacy systems, and ongoing concerns regarding data privacy and the robust security of satellite-transmitted information.

Artificial Intelligence (AI) significantly enhances Satellite IoT capabilities by enabling advanced data processing and analytics from vast datasets, facilitating predictive maintenance for remote assets, optimizing satellite network management and resource allocation, improving cybersecurity through real-time threat detection, and allowing for automated decision-making in autonomous remote operations, ultimately transforming raw data into actionable intelligence and driving operational efficiencies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.