ID : MRU_ 430674 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

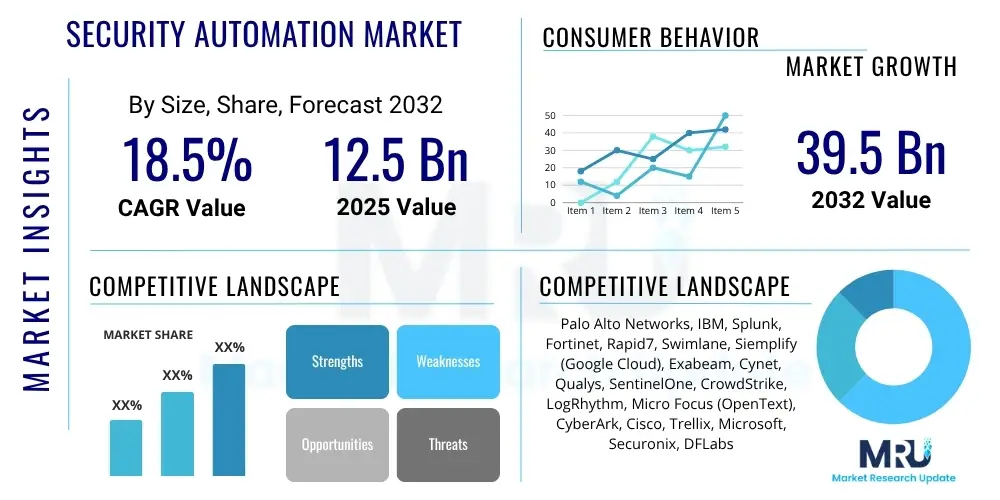

The Security Automation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2032. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 39.5 Billion by the end of the forecast period in 2032.

The Security Automation Market encompasses a rapidly evolving sector focused on leveraging technology to perform security operations with minimal human intervention. This market primarily involves solutions and services designed to automate various cybersecurity tasks, ranging from threat detection and incident response to vulnerability management and compliance auditing. The core objective of security automation is to enhance the efficiency, speed, and accuracy of security operations, thereby reducing the burden on human analysts and improving an organization's overall security posture. As cyber threats become more sophisticated and frequent, the demand for proactive and automated defense mechanisms continues to surge, positioning security automation as a critical component of modern enterprise security strategies.

Products within this market typically include Security Orchestration, Automation, and Response (SOAR) platforms, integrated threat intelligence solutions, automated vulnerability scanners, and AI-driven anomaly detection systems. Major applications span across almost all facets of cybersecurity, including the real-time analysis of security alerts, automated blocking of malicious traffic, rapid containment of security incidents, and continuous monitoring for compliance deviations. These solutions are vital for managing the overwhelming volume of security data and alerts that modern organizations generate, making it feasible to identify and respond to threats that would otherwise go unnoticed or take too long to address manually.

The benefits of adopting security automation are numerous and profound. Organizations experience faster incident response times, significant reduction in manual security tasks, improved consistency in security enforcement, and a considerable decrease in operational costs associated with managing a large cybersecurity team. Furthermore, automation helps bridge the critical skills gap in the cybersecurity industry by enabling existing personnel to focus on more complex, strategic issues rather than repetitive, time-consuming tasks. The market is primarily driven by the escalating sophistication and volume of cyberattacks, stringent regulatory compliance requirements, and the persistent shortage of skilled cybersecurity professionals, all of which compel organizations to seek more efficient and effective security solutions.

The Security Automation Market is experiencing robust growth, propelled by several key business trends. Enterprises are increasingly prioritizing integrated security solutions that offer seamless automation across various security tools and processes. This shift is evident in the rising adoption of SOAR platforms, which centralize and automate workflows, alongside a growing demand for cloud-native security automation that can adapt to dynamic cloud environments. Furthermore, there is a notable trend towards hyperautomation in security, combining technologies like Robotic Process Automation (RPA), Artificial Intelligence (AI), and Machine Learning (ML) to automate more complex and cognitive security tasks, moving beyond simple rule-based automation. The market also sees a strong push towards managed security services (MSSPs) that incorporate advanced automation capabilities, offering organizations a way to leverage cutting-edge security without significant in-house investment.

Regionally, North America continues to dominate the market due to its mature technological infrastructure, high cybersecurity spending, and stringent regulatory landscape that mandates robust security practices. Europe also holds a substantial market share, driven by initiatives like GDPR and the increasing awareness of cyber risks among enterprises. However, the Asia Pacific region is projected to exhibit the highest growth rate, fueled by rapid digital transformation, burgeoning IT and telecom sectors, and growing investments in cybersecurity infrastructure across emerging economies like India, China, and Southeast Asian countries. Latin America, the Middle East, and Africa are also witnessing significant, albeit slower, adoption as organizations in these regions increasingly recognize the imperative for automated security measures to protect their digital assets.

Segment-wise, the market is characterized by several dynamic trends. The solutions segment, particularly SOAR, SIEM, and XDR, is experiencing substantial demand as organizations seek comprehensive platforms. Within deployment models, the cloud-based segment is growing faster than on-premises, reflecting the broader industry shift towards cloud infrastructure and the scalability and flexibility it offers for security operations. Large enterprises remain the primary adopters due to their complex security needs and larger budgets, but small and medium-sized enterprises (SMEs) are also increasingly investing in security automation, often through managed services, as they become more aware of cyber threats. Application-wise, threat detection and incident response continue to be critical areas, with a growing emphasis on automating compliance management and SOC optimization to enhance operational efficiency and regulatory adherence.

User inquiries about the impact of AI on the Security Automation Market frequently revolve around its potential to revolutionize threat detection and response, the extent to which it can replace human analysts, and the inherent challenges such as bias and explainability. Common concerns include the reliability of AI in critical security decisions, the ability of AI to adapt to novel and sophisticated attack vectors, and the ethical implications of autonomous security systems. Users also seek clarity on how AI can improve operational efficiency, reduce false positives, and contribute to a more predictive security posture. There is a general expectation that AI will significantly augment human capabilities rather than entirely supplant them, with a focus on intelligent automation that handles repetitive tasks and provides deeper insights, enabling security teams to concentrate on strategic threat hunting and complex incident resolution.

The Security Automation Market is profoundly shaped by a confluence of drivers, restraints, and opportunities. A primary driver is the relentless increase in the volume and sophistication of cyber threats, forcing organizations to adopt automated solutions to keep pace with adversaries. The sheer scale of security alerts generated daily, often overwhelming human analysts, necessitates automation for effective triage and response. Furthermore, the persistent global shortage of skilled cybersecurity professionals compels enterprises to leverage automation to augment their existing teams and bridge critical skill gaps. Stringent regulatory compliance mandates, such as GDPR, HIPAA, and CCPA, also act as significant drivers, as automation facilitates continuous monitoring and reporting required for adherence, reducing the risk of hefty fines and reputational damage. The ongoing digital transformation across industries, leading to expanded attack surfaces and complex IT environments, further amplifies the need for automated security.

Despite the strong tailwinds, the market faces several notable restraints. The high initial investment required for implementing advanced security automation platforms, coupled with ongoing operational costs for maintenance and upgrades, can be a significant barrier for smaller organizations or those with limited IT budgets. Integration complexities with existing legacy security systems and diverse IT infrastructures often pose implementation challenges, requiring substantial customization and expert resources. Concerns regarding false positives and negatives generated by automated systems can erode trust and lead to wasted resources, necessitating continuous fine-tuning. Moreover, the lack of standardized security automation frameworks and the inherent resistance to change within organizations can slow down adoption. Emerging concerns around AI bias and the explainability of AI-driven security decisions also present ethical and operational challenges that need to be addressed as the technology matures.

Opportunities within the Security Automation Market are abundant and diverse. The rapid advancements and widespread adoption of Artificial Intelligence and Machine Learning are creating new avenues for more intelligent and predictive automation, moving beyond rule-based systems to behavioral analytics and threat intelligence. The expansion of cloud-native security automation solutions is a major opportunity, catering to organizations increasingly migrating their infrastructure to the cloud and requiring security that is agile and scalable. The growing trend of managed security services (MSSPs) offering robust automation capabilities allows businesses to outsource complex security operations, thereby democratizing access to advanced automation. Additionally, the emergence of Extended Detection and Response (XDR) platforms, which unify and automate detection and response across multiple security layers, represents a significant growth area. Increasing focus on securing IoT (Internet of Things) and OT (Operational Technology) environments, along with the broader demand for hyperautomation across enterprise functions, further fuels market expansion and innovation.

The Security Automation Market is comprehensively segmented to provide a detailed understanding of its diverse components, deployment models, target customers, applications, and end-use industries. This segmentation allows for precise analysis of market dynamics, growth drivers, and challenges across various dimensions, reflecting the varied needs and operational contexts of organizations adopting these advanced security solutions. By dissecting the market along these lines, stakeholders can identify specific niches, tailor strategies, and develop products that address the unique requirements of different market participants. The intricate nature of cybersecurity necessitates a multi-faceted approach to automation, leading to a granular market structure that caters to a wide spectrum of organizational sizes, technological landscapes, and threat profiles.

The value chain for the Security Automation Market encompasses a series of interconnected activities that collectively deliver automated security solutions to end-users, starting from foundational technology development to the final deployment and ongoing support. At the upstream end, the chain begins with technology providers specializing in AI/ML algorithms, big data analytics, cloud computing infrastructure, and core cybersecurity research. These entities supply the foundational components, intellectual property, and cutting-edge innovations that power security automation platforms. Software developers and cybersecurity experts then integrate these technologies to create sophisticated solutions, focusing on user experience, interoperability, and the ability to address evolving threat landscapes. This initial phase is crucial for developing robust, scalable, and intelligent automation engines.

Moving downstream, the value chain involves the distribution and implementation of these security automation solutions. Distribution channels are varied, encompassing direct sales by vendors to large enterprises with complex security needs, as well as indirect channels through a network of channel partners, value-added resellers (VARs), and system integrators. These partners play a pivotal role in reaching a broader customer base, offering localized support, and providing tailored integration services that ensure the automation solutions fit seamlessly into diverse IT environments. Managed Security Service Providers (MSSPs) represent another critical downstream player, offering security automation as part of their comprehensive managed services, which is particularly attractive to organizations lacking in-house cybersecurity expertise or resources.

The final stage of the value chain focuses on the end-users or buyers, who consume these security automation products and services. These include enterprises across various industry verticals and government agencies that leverage automation to enhance their security posture, streamline operations, and meet compliance obligations. Post-sales activities, such as ongoing support, maintenance, and continuous threat intelligence updates, are integral to maintaining the effectiveness and longevity of the automation solutions. The efficiency of the entire value chain is heavily dependent on strong collaboration between technology providers, solution developers, channel partners, and end-users, ensuring that the delivered solutions remain relevant and effective against an ever-changing threat landscape. Direct sales offer vendors greater control and direct customer feedback, while indirect channels provide market reach and specialized local expertise, collectively forming a comprehensive delivery ecosystem.

Potential customers for the Security Automation Market span a broad spectrum of organizations across virtually every industry, driven by the universal need to protect digital assets and data from an increasingly sophisticated array of cyber threats. Large enterprises, with their extensive and complex IT infrastructures, vast amounts of sensitive data, and stringent regulatory requirements, represent a significant segment of the market. These organizations often face thousands of security alerts daily, making manual processing untenable, and thus require advanced automation to manage their security operations efficiently. Industries such as Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecom, and Government and Defense are particularly prime candidates due to the high-value data they handle and the severe consequences of security breaches.

Beyond large corporations, Small and Medium-sized Enterprises (SMEs) are emerging as a rapidly growing customer segment. While they may have fewer resources and expertise compared to larger counterparts, SMEs are equally, if not more, vulnerable to cyberattacks and often lack the dedicated cybersecurity staff. Security automation, especially when delivered through managed security services (MSSPs), offers these businesses a cost-effective way to access sophisticated security capabilities, automate compliance, and respond quickly to threats without the need for significant in-house investment. The scalability and flexibility of cloud-based automation solutions make them particularly appealing to SMEs looking to enhance their security posture without heavy upfront capital expenditure or maintenance burdens.

Moreover, organizations in critical infrastructure sectors like Energy and Utilities, Manufacturing, and Healthcare are increasingly becoming key buyers. These sectors are highly susceptible to operational disruptions from cyberattacks, which can have severe real-world consequences beyond data loss. Security automation helps these entities protect their operational technology (OT) and critical control systems, ensuring continuity and safety. The continuous push for digital transformation across all industries, the growing adoption of cloud services, and the expansion of IoT devices also create new attack surfaces, making security automation an indispensable investment for any organization seeking to maintain a resilient and proactive defense against the evolving threat landscape, irrespective of their size or specific vertical.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2032 | USD 39.5 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Palo Alto Networks, IBM, Splunk, Fortinet, Rapid7, Swimlane, Siemplify (Google Cloud), Exabeam, Cynet, Qualys, SentinelOne, CrowdStrike, LogRhythm, Micro Focus (OpenText), CyberArk, Cisco, Trellix, Microsoft, Securonix, DFLabs |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Security Automation Market is characterized by a dynamic and innovative technology landscape, constantly evolving to counter sophisticated cyber threats and enhance operational efficiency. At its core, the market heavily relies on Security Orchestration, Automation, and Response (SOAR) platforms, which serve as central hubs for aggregating security alerts, automating incident workflows, and coordinating responses across disparate security tools. These platforms leverage playbooks and runbooks to standardize and accelerate incident handling, significantly reducing the mean time to respond (MTTR). Complementing SOAR are advanced Security Information and Event Management (SIEM) systems, which provide centralized logging, real-time analysis of security events, and correlation capabilities that feed into automation engines, enabling more informed and automated decision-making.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is a foundational technological shift in security automation. AI/ML algorithms are employed for behavioral analytics, anomaly detection, predictive threat intelligence, and reducing false positives in alert triage. These capabilities allow automation solutions to identify subtle indicators of compromise that human analysts might miss, adapt to new threat patterns, and prioritize risks more effectively. Furthermore, Extended Detection and Response (XDR) platforms are gaining prominence, unifying visibility and control across endpoints, networks, cloud environments, and identity. XDR platforms inherently incorporate automation to correlate data, streamline investigations, and orchestrate comprehensive responses, offering a more holistic approach than traditional EDR or SIEM solutions alone.

Other critical technologies shaping the market include Robotic Process Automation (RPA) for automating repetitive, rule-based security tasks, API integrations to ensure seamless communication between various security tools, and threat intelligence platforms that provide contextual information about emerging threats. Cloud-native security automation solutions are also vital, offering scalability, flexibility, and integration with cloud-specific security services. Technologies enabling Identity and Access Management (IAM) automation, vulnerability management automation, and automated compliance auditing are also crucial, allowing organizations to manage user access, identify security weaknesses, and ensure regulatory adherence with greater efficiency and accuracy. The convergence of these technologies creates a powerful ecosystem for intelligent, proactive, and resilient cybersecurity.

Security automation refers to the use of technology to automatically perform cybersecurity tasks and processes, such as threat detection, incident response, vulnerability management, and compliance auditing, with minimal human intervention.

Organizations benefit from faster incident response times, reduced manual effort, improved consistency in security enforcement, significant cost savings, and the ability to effectively manage the cybersecurity skills gap by augmenting human capabilities.

AI significantly enhances security automation by enabling advanced anomaly detection, predictive threat intelligence, intelligent alert triage, and automated incident response, moving beyond rule-based automation to more adaptive and learning systems.

Key challenges include high initial investment costs, complex integration with existing legacy systems, the potential for false positives/negatives, a lack of standardized frameworks, and organizational resistance to adopting new automated workflows.

Industries such as Banking, Financial Services, and Insurance (BFSI), Healthcare, IT & Telecom, and Government & Defense particularly benefit due to their high volume of sensitive data, stringent regulatory requirements, and the critical need for rapid threat response.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.