ID : MRU_ 427844 | Date : Oct, 2025 | Pages : 258 | Region : Global | Publisher : MRU

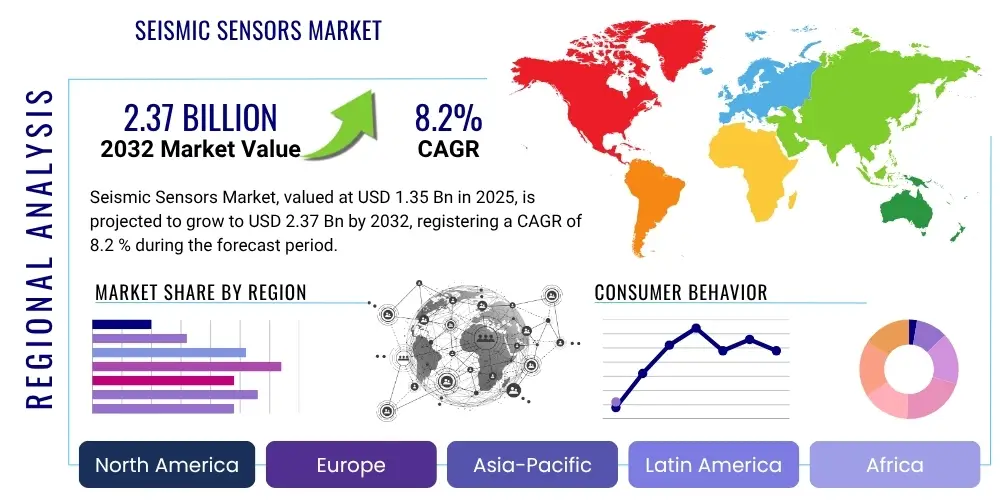

The Seismic Sensors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2032. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 2.37 Billion by the end of the forecast period in 2032. This significant expansion is driven by increasing global demand for energy resources, extensive infrastructure development initiatives, and a heightened focus on natural disaster preparedness and mitigation strategies across various geographies. The adoption of advanced sensing technologies and data analytics further propels this growth trajectory.

The seismic sensors market encompasses a sophisticated range of devices designed to detect and record ground motion, vibrations, and acoustic energy, originating from both natural phenomena and anthropogenic activities. These critical instruments transform ground vibrations into electrical signals, enabling detailed analysis of subsurface structures, earth tremors, and human-induced seismic events. Products within this market segment range from traditional geophones and accelerometers to advanced fiber optic and Micro-Electro-Mechanical Systems (MEMS) based sensors, each tailored for specific applications requiring varying levels of sensitivity, frequency response, and deployment environments.

Major applications for seismic sensors span a broad spectrum of industries, including oil and gas exploration, where they are instrumental in locating hydrocarbon reserves through seismic imaging. In civil engineering, these sensors are vital for structural health monitoring (SHM) of bridges, buildings, and dams, ensuring their integrity and safety against seismic events. Furthermore, they play a crucial role in environmental monitoring, earthquake detection, volcanic activity surveillance, and defense and security applications such as border monitoring and underground nuclear test detection. The benefits derived from seismic sensor deployment include enhanced operational safety, optimized resource exploration, improved predictive capabilities for natural disasters, and the ability to maintain critical infrastructure resilience.

Driving factors for the seismic sensors market are multi-faceted, stemming from persistent global energy demands necessitating more efficient exploration techniques, rapid urbanization leading to increased infrastructure development and associated monitoring requirements, and a growing global awareness of seismic hazards. Technological advancements, particularly in sensor miniaturization, wireless connectivity, and data processing capabilities, have also significantly contributed to the market's expansion. The convergence of these factors creates a robust demand environment for advanced seismic sensing solutions across diverse end-user sectors seeking accurate, real-time geological and structural data.

The seismic sensors market is experiencing robust growth fueled by several prevailing business trends, dynamic regional developments, and evolving segment demands. A prominent business trend is the increasing integration of Internet of Things (IoT) capabilities with seismic sensors, facilitating real-time data acquisition and remote monitoring, which significantly enhances operational efficiency and data accessibility. Additionally, there is a strong shift towards developing wireless and autonomous sensor networks that reduce deployment complexities and costs, making seismic monitoring more pervasive and adaptable to challenging environments. The market is also witnessing substantial investments in miniaturized and high-sensitivity sensors, driven by the need for more discreet and precise measurements in urbanized areas and sensitive ecological zones. Furthermore, the adoption of advanced materials and manufacturing techniques is leading to the production of more durable and energy-efficient seismic sensors, broadening their application scope and improving their longevity in harsh operational conditions.

From a regional perspective, the Asia-Pacific region is emerging as a significant growth hub for seismic sensors, primarily due to rapid infrastructure development, escalating energy consumption, and a high susceptibility to natural disasters such as earthquakes and tsunamis. Countries like China, India, and Japan are investing heavily in advanced monitoring systems to safeguard their growing urban populations and critical infrastructure. North America continues to hold a leading position, driven by mature oil and gas exploration activities, substantial governmental funding for geological research, and advanced technological innovation. Europe also presents a strong market, with a focus on environmental monitoring, structural health assessment of aging infrastructure, and robust research and academic collaborations. The Middle East and Africa regions are showing promising growth, largely attributed to extensive oil and gas exploration projects and investments in new urban and industrial developments that necessitate comprehensive subsurface analysis. Latin America's market is primarily influenced by its oil and gas sector and increasing awareness of seismic activity.

Segmentation trends within the seismic sensors market reveal a growing preference for MEMS-based sensors due to their compact size, lower power consumption, and cost-effectiveness, making them ideal for large-scale deployments and distributed sensing applications. The oil and gas exploration segment remains a dominant application area, although structural health monitoring (SHM) and environmental monitoring are exhibiting accelerated growth rates, driven by stringent safety regulations and increasing concerns over climate change impacts. Wireless sensor technologies are gaining considerable traction over wired solutions, particularly in remote or difficult-to-access locations, offering greater flexibility and reduced installation efforts. End-user demand is diversifying, with significant contributions from civil engineering, mining, and government research institutions, alongside the traditional energy sector. This diversification underscores the expanding utility and critical importance of seismic sensors across a broader range of industrial and scientific applications, pushing manufacturers to innovate and offer specialized solutions tailored to distinct sector requirements.

The integration of Artificial Intelligence (AI) is profoundly transforming the seismic sensors market, addressing key challenges and unlocking unprecedented capabilities in data processing, interpretation, and predictive analytics. Users frequently inquire about how AI can enhance the accuracy of seismic data, accelerate the interpretation of complex geological structures, and improve the early warning capabilities for natural disasters. Common concerns revolve around the reliability of AI models in critical applications, the computational resources required for advanced AI algorithms, and the ethical implications of autonomous decision-making based on AI-processed seismic data. However, there is widespread expectation that AI will significantly reduce human error, enable the analysis of vast datasets that are currently intractable, and lead to more proactive and precise responses in various seismic applications, ranging from resource exploration to public safety.

AI's influence is particularly notable in its ability to sift through enormous volumes of raw seismic data with speed and precision far exceeding human capacity, identifying subtle patterns and anomalies that might otherwise be overlooked. This enhances the resolution and reliability of subsurface imaging in oil and gas exploration, leading to more efficient drilling and resource extraction. In structural health monitoring, AI algorithms can learn the normal vibrational patterns of infrastructure and flag deviations indicative of structural fatigue or damage in real-time, enabling predictive maintenance and preventing catastrophic failures. For earthquake monitoring, AI can differentiate between seismic noise and actual seismic events, refine earthquake location and magnitude estimations, and contribute to the development of more accurate short-term prediction models, potentially saving lives and reducing economic losses. The ability of AI to integrate diverse data sources, such as satellite imagery, weather data, and historical seismic records, further augments the contextual understanding and predictive power of seismic analyses, moving beyond simple detection to comprehensive environmental intelligence.

The seismic sensors market is significantly influenced by a complex interplay of drivers, restraints, opportunities, and competitive impact forces, all shaping its growth trajectory and strategic landscape. Key drivers include the ever-increasing global demand for energy, which propels extensive oil and gas exploration activities, particularly in challenging deep-water and unconventional resource areas, necessitating advanced seismic imaging technologies. Simultaneously, rapid urbanization and large-scale infrastructure development projects worldwide require rigorous structural health monitoring to ensure safety and longevity, especially in seismically active zones. A heightened global awareness and concern regarding natural disasters like earthquakes, volcanic eruptions, and tsunamis also contribute substantially to market growth, driving investments in early warning systems and comprehensive monitoring networks. Furthermore, ongoing technological advancements in sensor miniaturization, wireless communication, and data analytics capabilities make seismic sensors more versatile, efficient, and accessible for a broader range of applications, including mining and defense.

However, several restraints temper this growth. The high initial capital investment required for sophisticated seismic sensor systems, coupled with the considerable costs associated with data acquisition, processing, and interpretation, can be prohibitive for smaller organizations or projects with limited budgets. The inherent complexity of interpreting vast and diverse seismic data often necessitates highly specialized expertise, which can be scarce, adding to operational challenges. Environmental and regulatory concerns, particularly in sensitive ecosystems or politically unstable regions, can impose significant restrictions on seismic exploration and deployment activities, leading to project delays or cancellations. Furthermore, competition from alternative subsurface imaging technologies or less expensive, albeit less precise, monitoring methods in certain niche applications, also presents a restraint on market expansion, forcing manufacturers to continuously innovate and demonstrate superior value propositions. The long product lifecycle of some robust seismic equipment can also slow down replacement cycles and new purchases.

Despite these restraints, the market is brimming with opportunities. The emergence of smart cities and intelligent infrastructure initiatives globally presents a massive growth avenue for integrating seismic sensors into urban planning and management systems for continuous monitoring of buildings, bridges, and transportation networks. The rapid expansion of renewable energy projects, particularly geothermal and offshore wind farms, creates a demand for subsurface analysis and structural monitoring to ensure project viability and safety. Furthermore, continuous advancements in Artificial Intelligence (AI) and Machine Learning (ML) offer transformative opportunities for predictive analytics, automated data interpretation, and real-time decision-making, significantly enhancing the value proposition of seismic sensor systems. The exploration of new frontiers in resource extraction, such as deep-sea mining and Arctic exploration, also opens up specialized applications requiring robust and resilient seismic sensing solutions. Moreover, the increasing demand for defense and security applications, including border surveillance and subterranean threat detection, provides a niche but high-value growth segment. These opportunities collectively promise sustained innovation and expansion for the seismic sensors market.

The seismic sensors market is extensively segmented by type, application, end-user, and technology, reflecting the diverse range of products and their specialized uses across various industries. This segmentation provides a granular view of market dynamics, enabling stakeholders to understand specific demand patterns, technological preferences, and growth opportunities within distinct categories. Each segment is driven by unique sets of requirements, ranging from the precision needed in scientific research to the ruggedness demanded by offshore oil and gas exploration. The evolving technological landscape, characterized by miniaturization, wireless connectivity, and advanced data processing, continues to influence the expansion and differentiation of these market segments, fostering innovation and specialized product development tailored to specific industry needs and environmental challenges.

The value chain for the seismic sensors market is a complex ecosystem beginning with upstream activities involving the sourcing of raw materials and the manufacturing of intricate components, extending through the production and assembly of the sensors, and culminating in their distribution, integration, and deployment by downstream entities. Upstream analysis focuses on suppliers of specialized materials such as high-grade metals for casings, piezoelectric ceramics, silicon for MEMS devices, and advanced electronics components like microcontrollers and communication modules. These suppliers form the foundational layer, providing the crucial elements that dictate the performance and reliability of the final seismic sensor products. Component manufacturers, specializing in transducers, amplifiers, and data conversion units, also play a vital role, often operating as specialized firms contributing critical sub-assemblies to the primary sensor manufacturers. The efficiency and quality within this upstream segment directly impact the cost-effectiveness and innovation capabilities of the entire market.

Moving through the value chain, the core manufacturing and assembly processes involve significant research and development to design, calibrate, and test the seismic sensors. This stage is characterized by substantial investment in R&D to enhance sensor sensitivity, frequency response, ruggedness, and connectivity features. Downstream activities involve the distribution channel, which is typically a hybrid model combining direct sales with a network of specialized distributors and system integrators. Direct sales are common for large, customized projects, especially in the oil and gas sector or governmental defense contracts, where close collaboration between the manufacturer and end-user is essential. Indirect channels leverage distributors who have established regional presence and technical expertise, enabling broader market reach and support for smaller-scale projects or diverse customer bases.

System integrators form a critical link in the downstream segment, often responsible for designing comprehensive seismic monitoring solutions, deploying the sensors, installing associated data acquisition systems, and providing ongoing maintenance and data interpretation services. These integrators act as a bridge between the sensor manufacturers and the diverse end-users, tailoring solutions to specific application requirements, whether for hydrocarbon exploration, structural health monitoring, or environmental assessment. The distribution channels for seismic sensors are therefore multifaceted, encompassing specialized resellers, value-added resellers (VARs), and direct sales teams. This intricate network ensures that highly technical products reach their intended applications with the necessary support and expertise, optimizing deployment and maximizing the value delivered to the end-users across various industries globally.

The potential customers for seismic sensors are incredibly diverse, spanning numerous industries and governmental organizations that rely on precise ground motion data for critical decision-making and operational safety. At the forefront are oil and gas companies, which represent a significant end-user segment. These companies utilize seismic sensors extensively for hydrocarbon exploration and reservoir monitoring, employing them in both onshore and offshore environments to map subsurface geological structures and identify potential reserves. Their demand is driven by the continuous need to locate new energy sources and optimize extraction from existing fields, making high-resolution and reliable seismic data indispensable for their core business operations. The investment capabilities of these major energy players often drive innovation and demand for advanced, high-performance sensor technologies.

Beyond the energy sector, civil engineering and construction firms constitute a rapidly growing customer base. As global infrastructure continues to expand and age, seismic sensors are increasingly adopted for structural health monitoring (SHM) of bridges, tunnels, dams, high-rise buildings, and other critical infrastructure. These sensors provide real-time data on structural integrity, detect fatigue, and assess damage from seismic events, enabling proactive maintenance and ensuring public safety. Government agencies and research institutions also form a substantial segment of potential customers, including geological survey organizations, seismological observatories, and universities. These entities use seismic sensors for fundamental research into earth processes, earthquake early warning systems, volcanic activity monitoring, and hazard assessment, contributing to public safety and scientific understanding. Their procurement is often driven by scientific mandates, public safety initiatives, and grant-funded research projects.

Furthermore, mining companies are significant buyers, deploying seismic sensors to monitor rock stability, detect ground movement, and prevent collapses in both underground and open-pit operations, thereby enhancing worker safety and operational efficiency. The defense and security sector also represents a niche but high-value customer group, utilizing seismic sensors for border surveillance, intrusion detection, and monitoring of underground activities, including the detection of covert tunnels or nuclear test sites. Industrial sectors seeking to monitor machinery vibrations, assess foundation stability for heavy equipment, or analyze ground-borne noise and vibration for environmental compliance also procure seismic sensors. This broad array of end-users underscores the versatile utility and indispensable nature of seismic sensing technology across a multitude of applications vital for economic development, environmental protection, and public safety.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2032 | USD 2.37 Billion |

| Growth Rate | 8.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Geospace Technologies, Sercel (CGG), ION Geophysical, Schlumberger, Baker Hughes, Halliburton, Seiscom (GE), Micro-Epsilon, TE Connectivity, Honeywell, Meggitt (Parker Hannifin), PCB Piezotronics, Endevco (Amphenol), Guralp Systems, Kinemetrics, Reftek, SmartSolo (DTCC), OmniSeis (Nodality), Spectra-Physics, Metrohm |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The seismic sensors market is characterized by a dynamic and continuously evolving technology landscape, with advancements primarily focused on enhancing sensitivity, improving data acquisition capabilities, reducing power consumption, and enabling more versatile deployment options. Micro-Electro-Mechanical Systems (MEMS) technology stands as a cornerstone, revolutionizing the market by facilitating the production of miniaturized, lightweight, and cost-effective sensors. MEMS-based accelerometers and geophones offer comparable performance to traditional, larger sensors while consuming significantly less power, making them ideal for large-scale, distributed wireless sensor networks and long-duration monitoring projects where space and power are constrained. These compact sensors are driving the proliferation of seismic monitoring in urban environments and integrated structural health monitoring systems, expanding their applicability beyond traditional seismic exploration. Their inherent robustness also contributes to greater resilience in harsh operating conditions, further bolstering their adoption across diverse sectors.

Another pivotal technological development is the pervasive integration of the Internet of Things (IoT) and wireless communication protocols into seismic sensor systems. IoT connectivity enables real-time data transmission from remote or difficult-to-access locations to centralized processing centers or cloud platforms, eliminating the need for extensive cabling and reducing installation complexities and costs. This capability supports continuous, unattended monitoring, which is crucial for applications such as earthquake early warning systems, critical infrastructure surveillance, and long-term environmental studies. Wireless sensor networks (WSNs) facilitate rapid deployment and redeployment, offering unparalleled flexibility for temporary surveys or rapidly evolving monitoring needs. The development of low-power wide-area network (LPWAN) technologies like LoRaWAN and NB-IoT is further extending the range and battery life of these wireless seismic systems, making them more practical for expansive geographical coverages and prolonged operational periods.

Furthermore, the application of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is fundamentally transforming the way seismic data is processed, interpreted, and utilized. AI-powered analytics can rapidly sift through vast datasets, identify subtle patterns, filter out noise, and automate the detection of seismic events or anomalies, significantly improving the accuracy and efficiency of interpretation. Cloud computing infrastructure provides the necessary computational power and storage capacity to handle the enormous volumes of data generated by modern seismic sensor networks, enabling sophisticated real-time processing and collaborative analysis across geographically dispersed teams. Fiber optic sensing technology, offering immunity to electromagnetic interference, high sensitivity, and the ability to operate in extreme environments, is also gaining prominence, particularly in applications requiring long-distance monitoring or deployment in hazardous conditions. These technological advancements collectively contribute to more intelligent, robust, and accessible seismic monitoring solutions, continuously pushing the boundaries of what is possible in geophysical and structural analysis.

Seismic sensors are primarily used for detecting and recording ground motion and vibrations. Their main applications include oil and gas exploration, structural health monitoring of infrastructure, earthquake detection and early warning systems, environmental monitoring, and defense and security purposes.

Seismic sensors, such as geophones and accelerometers, work by converting ground vibrations into electrical signals. Geophones measure ground velocity, while accelerometers measure ground acceleration. These signals are then recorded and analyzed to provide insights into subsurface structures, seismic events, or structural integrity.

The market offers various types of seismic sensors, including traditional geophones (coil-and-magnet type), accelerometers, hydrophones (for underwater seismic activity), fiber optic sensors, and Micro-Electro-Mechanical Systems (MEMS) based sensors. Each type is designed for specific applications and environmental conditions.

Key technological advancements include the miniaturization of sensors through MEMS technology, integration with IoT for real-time and wireless data transmission, application of AI and Machine Learning for advanced data processing and predictive analytics, and improvements in fiber optic sensing for harsh environments. These innovations enhance performance, reduce costs, and expand application areas.

The future outlook for the seismic sensors market is highly positive, driven by continued demand for energy exploration, global infrastructure development, increasing focus on natural disaster preparedness, and continuous technological innovations like AI integration. The market is expected to witness significant growth, especially in emerging economies and smart city initiatives, with a shift towards more intelligent, connected, and autonomous sensing solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.