ID : MRU_ 429613 | Date : Nov, 2025 | Pages : 251 | Region : Global | Publisher : MRU

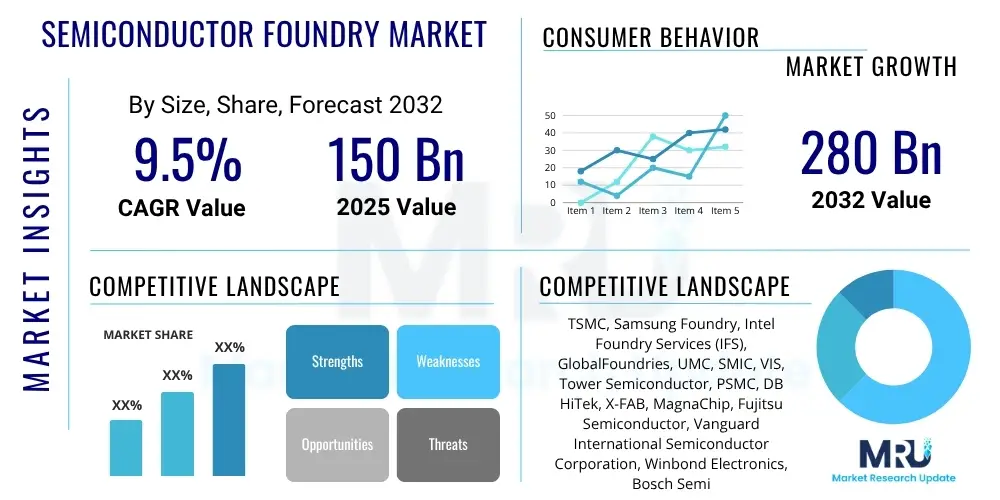

The Semiconductor Foundry Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032. The market is estimated at USD 150 billion in 2025 and is projected to reach USD 280 billion by the end of the forecast period in 2032.

The semiconductor foundry market forms the indispensable backbone of the modern global electronics industry, providing highly specialized manufacturing services for the production of integrated circuits, commonly known as microchips. Foundries are dedicated, high-technology fabrication plants that transform complex design blueprints, typically supplied by fabless semiconductor companies and integrated device manufacturers (IDMs), into functional silicon wafers through intricate processes. This sophisticated sector demands immense capital investment, advanced engineering expertise, and relentless innovation, enabling the broader electronics ecosystem to thrive by democratizing access to cutting-edge manufacturing capabilities without requiring individual companies to bear the prohibitive costs of building and maintaining proprietary fabrication facilities. The sheer complexity and economic scale involved solidify the foundry's role as a linchpin in technological progress.

The primary service offered by semiconductor foundries is wafer fabrication, which involves a multi-stage process of depositing, patterning, and etching materials onto silicon substrates to create intricate circuits. Foundries support a vast spectrum of process technologies, ranging from mature, cost-effective nodes used for power management and legacy devices to leading-edge advanced nodes, currently below 7 nanometers, crucial for high-performance applications. The major applications for chips manufactured by these foundries are incredibly diverse, spanning high-performance computing (HPC), artificial intelligence (AI) and machine learning (ML), advanced automotive electronics including autonomous driving systems, critical 5G communication infrastructure, a wide array of consumer electronics such as smartphones and smart devices, and industrial automation systems. These diverse applications collectively underscore the foundational and pervasive impact of foundry services across the digital economy.

The benefits derived from leveraging semiconductor foundry services are multifaceted and strategically vital for the industry. For fabless companies, it provides access to the most advanced manufacturing processes and intellectual property (IP) without the colossal capital expenditure and operational burden of owning a fab, significantly reducing barriers to entry and fostering innovation. This model accelerates time-to-market for complex chip designs, allowing rapid iterations and competitive launches. Furthermore, foundries offer economies of scale, leading to more cost-efficient production and enabling specialized companies to focus their core competencies solely on research, design, and market strategy. Key driving factors propelling the market forward include the insatiable global demand for increasingly sophisticated electronic devices, the pervasive rollout of the Internet of Things (IoT) generating billions of connected endpoints, the exponential growth in demand for artificial intelligence capabilities, and the global deployment of high-speed 5G networks. The ever-increasing complexity of chip designs and the spiraling costs associated with developing and equipping next-generation fabrication plants continue to compel more companies to outsource their manufacturing needs to specialized foundry partners, reinforcing this market's upward trajectory.

The Semiconductor Foundry Market is currently experiencing a period of significant expansion and strategic transformation, largely propelled by an unrelenting global demand for advanced integrated circuits essential to modern technological infrastructure. Prominent business trends indicate a critical pivot towards enhancing supply chain resilience and geographically diversifying manufacturing capabilities. Geopolitical considerations are heavily influencing investment decisions, with nations worldwide actively promoting domestic semiconductor production to mitigate future disruptions and assert technological sovereignty. Foundries are concurrently making substantial investments in advanced packaging solutions, such as 2.5D and 3D stacking, which are becoming as crucial as traditional node scaling for achieving superior performance, power efficiency, and integration density in next-generation chips. This competitive landscape is characterized by an intense pursuit of technological leadership, particularly evident in the race to master sub-5nm and future process nodes, necessitating massive research and development expenditures and strategic collaborations across the value chain to sustain innovation.

From a regional perspective, the Asia Pacific continues to hold a dominant position in the global foundry market, primarily attributed to the long-established operational excellence and sheer scale of leading pure-play foundries headquartered in Taiwan and South Korea. This region also sees substantial growth in China's domestic semiconductor industry, driven by national initiatives aimed at achieving self-sufficiency and reducing reliance on foreign technology. However, a noticeable and growing trend involves significant strategic investments across North America and Europe, spearheaded by government incentives designed to onshore advanced manufacturing capacity. Initiatives like the CHIPS Act in the United States and the European Chips Act signify a concerted effort to foster local ecosystems, attract foundry investments, and secure critical supply chains. This global shift, while facing challenges in workforce development and infrastructure, is poised to reshape the geographical distribution of foundry capacities, leading towards a more diversified and distributed global manufacturing footprint by the end of the forecast period.

Analysis of market segmentation trends reveals the pronounced importance of advanced technology nodes, specifically those at 7nm and below, which are witnessing the highest demand. These cutting-edge nodes are indispensable for applications in artificial intelligence, high-performance computing, and premium mobile devices, where processing power and energy efficiency are paramount. While mature nodes (above 28nm) continue to sustain robust demand from pervasive segments such as automotive electronics, industrial IoT, and general-purpose microcontrollers, the growth trajectory for advanced processes remains significantly steeper. By application, the high-performance computing and data center segments are expanding at an accelerated pace, mirroring the explosive growth of cloud services and AI workloads. The automotive sector also presents a strong, consistent demand, driven by the increasing silicon content in electric vehicles and advanced driver-assistance systems (ADAS). Pure-play foundries, owing to their specialized focus and vast scale, continue to capture the lion's share of the market, while IDM foundries strategically augment their internal production with external services to optimize capacity utilization and access niche process technologies.

Common user questions regarding the influence of Artificial Intelligence (AI) on the Semiconductor Foundry Market typically explore how AI is fundamentally reshaping the demand landscape for advanced chips, the intricate technological challenges foundries must overcome to proficiently support AI workloads, and the extensive growth opportunities presented by this transformative technology. Users often seek to discern whether AI represents merely an revolutionary paradigm shift for foundry services. Key themes consistently emerging from these inquiries highlight the critical need for highly specialized process technologies capable of handling immense computational demands, the burgeoning importance of innovative advanced packaging solutions to enhance AI chip performance and integration, and the potential for AI to drive an unprecedented surge in demand for raw computational power. This necessitates substantial and continuous investments in research and development, alongside significant expansions in manufacturing capacity by leading foundries. Furthermore, there is considerable interest in how AI itself can be intelligently integrated into foundry operations to optimize complex manufacturing processes, improve yield rates, and accelerate the overall design and production cycles, pointing towards a synergistic relationship where AI not only drives demand but also enhances supply capabilities within the semiconductor ecosystem.

The Semiconductor Foundry Market is robustly propelled by a confluence of powerful drivers that underscore its critical role in the digital age. Foremost among these is the escalating global demand for increasingly sophisticated electronic devices across nearly every sector, including consumer electronics, telecommunications, healthcare, and industrial automation. This demand is particularly intensified by the explosive growth of transformative technologies such as artificial intelligence, which requires massive computational power; the global rollout of 5G networks, necessitating advanced chipsets for connectivity; and the widespread proliferation of the Internet of Things (IoT), connecting billions of devices that rely on embedded silicon. Furthermore, the automotive industry's rapid shift towards electric vehicles, autonomous driving, and advanced driver-assistance systems (ADAS) creates a relentless need for specialized, high-reliability semiconductors. The ingrained efficiency and strategic advantages of the fabless business model continue to expand, with more design companies opting to outsource their manufacturing to specialized foundries, leveraging their immense capital investments and technological expertise, thereby fueling market expansion and innovation.

Despite its significant growth trajectory, the market faces several formidable restraints that temper its expansion and introduce substantial risks. The most prominent restraint is the extraordinarily high capital expenditure required for designing, constructing, and maintaining state-of-the-art fabrication facilities, with each new leading-edge fab costing tens of billions of dollars. This necessitates massive and continuous investment, limiting the number of players capable of competing at the forefront. Geopolitical tensions and evolving trade policies, particularly between major economic powers, pose significant supply chain risks, potentially disrupting the flow of critical raw materials, advanced manufacturing equipment, and skilled labor, creating considerable uncertainty for long-term strategic planning. The inherent cyclical nature of the semiconductor industry, characterized by periodic fluctuations between oversupply and undersupply, introduces market volatility and challenges for accurate capacity planning and investment synchronization. Moreover, the increasing complexity of advanced manufacturing processes can lead to lower initial yields, higher development costs, and extended time-to-market for new technologies, impacting profitability and innovation cycles across the entire value chain.

Significant opportunities abound within the Semiconductor Foundry Market, driven by the emergence of groundbreaking technologies and evolving global dynamics. The advent of next-generation computing paradigms, such as quantum computing and neuromorphic computing, along with the proliferation of edge AI devices, opens entirely new avenues for highly specialized and advanced semiconductor manufacturing. The global push for regional diversification of semiconductor manufacturing capacity, spurred by government incentives (e.g., CHIPS Acts) in North America, Europe, and India, presents new growth prospects for foundries willing to invest outside traditional manufacturing hubs. This strategic realignment aims to build more resilient and localized supply chains. Furthermore, the rapid advancements in advanced packaging technologies, including 2.5D/3D stacking, chiplets, and hybrid bonding, offer lucrative growth opportunities by enabling higher performance, higher integration density, and greater design flexibility without solely relying on traditional transistor scaling. Strategic partnerships and collaborative research initiatives between foundries, equipment suppliers, material providers, and fabless companies are also accelerating the development of innovative process technologies and market-specific solutions, collectively creating a robust landscape for sustained market expansion and technological leadership.

The Semiconductor Foundry Market is meticulously segmented across various crucial dimensions, offering a detailed and granular understanding of its complex structure, underlying growth drivers, and competitive dynamics. These segmentations are indispensable tools for market participants to analyze specific trends, identify high-growth niches, and assess the competitive landscape within distinct areas of the foundry business. Key categories include segmentation by technology node, reflecting the level of manufacturing sophistication; by application, showcasing the diverse end-use industries; by foundry type, differentiating between pure-play and IDM models; and by wafer size, indicating manufacturing scale and capability. This comprehensive breakdown facilitates a nuanced strategic analysis, enabling stakeholders to discern where the most significant growth opportunities reside, anticipate future investment priorities, and refine their technology roadmaps and market penetration strategies for optimal impact.

The value chain of the Semiconductor Foundry Market is an intricate, multi-tiered ecosystem beginning with upstream activities that are foundational to the entire wafer fabrication process. This segment includes highly specialized equipment manufacturers such as ASML (for lithography), Applied Materials (for deposition, etching, and other processes), Lam Research (for etching and deposition), and KLA Corporation (for inspection and metrology). These companies are vital for providing the precision machinery and advanced tools necessary to produce the intricate microscopic structures on silicon wafers. Concurrently, material suppliers form another critical upstream component, providing ultra-pure silicon wafers (from industry giants like Shin-Etsu Chemical and SUMCO), photoresists, specialty chemicals, high-purity gases, and various other consumables essential for cleanroom manufacturing. The quality, reliability, and timely delivery of these upstream inputs directly dictate the foundry's output quality, yield rates, and overall operational efficiency. Deep, collaborative relationships between foundries and these upstream partners are paramount for accelerating technological advancements and ensuring the resilience and stability of the global semiconductor supply chain.

Moving through the central part of the value chain, the core foundry operation involves the highly complex and capital-intensive process of fabricating integrated circuits. Foundries execute billions of individual steps, from photolithography and etching to deposition and ion implantation, to translate design files provided by customers into tangible silicon chips. Downstream, the value chain extends to the primary customers of these foundries: fabless semiconductor companies. These design-centric firms, including industry leaders like Qualcomm, Nvidia, AMD, and Broadcom, rely entirely on pure-play foundries to manufacture their cutting-edge chip designs, enabling them to focus their resources on innovation and intellectual property development. Integrated Device Manufacturers (IDMs) such as Intel and Samsung also increasingly utilize external foundry services, either to supplement their internal fabrication capacity during periods of high demand, access advanced process nodes not yet available in-house, or to diversify their manufacturing footprint strategically. Further downstream are the Original Equipment Manufacturers (OEMs) and Original Design Manufacturers (ODMs) who integrate these fabricated chips into a vast array of final products, from consumer electronics like smartphones and laptops to complex systems for data centers, automotive, and industrial applications. The performance, cost-effectiveness, and timely availability of foundry services directly influence the innovation cycles and production capabilities of these end-product manufacturers, underscoring the foundry's indispensable role.

The distribution channels within the semiconductor foundry market are predominantly characterized by direct engagement, involving long-term strategic partnerships and highly customized contractual agreements between foundries and their major clientele. Given the bespoke nature of semiconductor manufacturing, the colossal investments required, and the criticality of intellectual property protection, transactions are rarely transactional or spot-market purchases. Instead, they typically involve multi-year capacity commitments and detailed technical collaboration. Direct communication channels ensure close coordination on design specifications, process optimization, yield enhancement, and comprehensive supply chain management, fostering a high degree of trust and shared risk. While direct sales to major customers form the bulk of the business, indirect channels can occasionally involve design service companies, intellectual property (IP) vendors, or electronic design automation (EDA) tool providers who act as intermediaries or facilitators. These entities often aid smaller fabless companies or those with limited in-house design resources in preparing their designs for foundry compatibility, thereby indirectly influencing the foundry's project pipeline. The inherently intricate and capital-intensive characteristics of the industry necessitate a profoundly collaborative and direct relationship between all key participants across the entire value chain.

The potential customer base for the Semiconductor Foundry Market is expansive and highly diverse, fundamentally comprising entities that specialize in designing integrated circuits but choose to outsource their actual manufacturing to specialized fabrication facilities. This group predominantly includes a substantial number of fabless semiconductor companies, which represent a cornerstone of the modern electronics industry. These companies, ranging from established giants like Nvidia, Qualcomm, Broadcom, and AMD to a multitude of agile startups focusing on emerging fields such as AI, IoT, and edge computing, rely entirely on pure-play foundries for the precise and high-volume fabrication of their innovative chip designs. The increasing technological complexity, the spiraling costs associated with building and operating advanced semiconductor fabs, and the intense competitive pressure for faster product cycles make outsourcing manufacturing to foundries an economically compelling and strategically indispensable choice for these design-centric players, enabling them to concentrate their core competencies on intellectual property creation and market differentiation.

Beyond the traditional fabless model, Integrated Device Manufacturers (IDMs) also constitute a significant and growing segment of potential customers for semiconductor foundries. While IDMs, such as Intel and Samsung, historically possess and operate their own large-scale fabrication plants, they are increasingly leveraging external foundry services for a multitude of strategic reasons. This includes accessing cutting-edge process nodes that may not yet be available in their internal fabs, managing fluctuations in demand by offloading production during peak periods, diversifying their manufacturing risk, or strategically sourcing specific components to optimize their overall product portfolio. This strategic outsourcing by IDMs underscores the advanced capabilities, unparalleled economies of scale, and cost-efficiency that leading foundries offer, even to companies with significant internal manufacturing capacities. This dynamic interaction between IDMs and pure-play foundries signifies a nuanced and evolving interplay within the broader semiconductor ecosystem, driving further market complexity and specialization.

Furthermore, an expanding array of system-level companies and even Original Equipment Manufacturers (OEMs) are progressively becoming direct or indirect customers of foundries. Tech behemoths like Apple, Google, Amazon, and Microsoft are increasingly designing their own custom silicon, specifically tailored for internal use in their proprietary devices, cloud data centers, or advanced AI accelerators. These custom chip designs are then sent to foundries for fabrication, highlighting a trend towards vertical integration in design coupled with horizontal specialization in manufacturing. The automotive sector, undergoing a transformative shift towards electric vehicles, autonomous driving capabilities, and sophisticated in-car infotainment systems, demands a growing volume of highly specialized and reliable chips. This drives closer collaborations between automotive OEMs or their Tier 1 suppliers and foundries to develop customized, robust, and safety-critical semiconductor solutions. This broadening customer base reflects the foundry market's fundamental and expanding role in supporting innovation and enabling technological advancements across an increasingly diverse spectrum of industries that rely heavily on state-of-the-art semiconductor technology for their product differentiation, performance, and strategic advantage.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 150 billion |

| Market Forecast in 2032 | USD 280 billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TSMC, Samsung Foundry, Intel Foundry Services (IFS), GlobalFoundries, UMC, SMIC, VIS, Tower Semiconductor, PSMC, DB HiTek, X-FAB, MagnaChip, Fujitsu Semiconductor, Vanguard International Semiconductor Corporation, Winbond Electronics, Bosch Semiconductor, STMicroelectronics, NXP Semiconductors, Infineon Technologies, Powerchip Semiconductor Manufacturing Corporation (PSMC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Semiconductor Foundry Market is characterized by a relentlessly evolving and profoundly complex technological landscape, constantly pushing the boundaries of scientific discovery and engineering ingenuity to deliver integrated circuits that are smaller, faster, more power-efficient, and increasingly capable. Extreme Ultraviolet (EUV) lithography stands as the paramount foundational technology, enabling the precise patterning of features at resolutions of 7nm and below, which is absolutely critical for the fabrication of next-generation microprocessors, high-density memory, and advanced AI accelerators. Foundries are making monumental investments in EUV infrastructure, associated R&D, and supply chain development to maintain their competitive edge, master the intricate complexities of EUV tools, and effectively support the most advanced chip designs demanded by high-performance computing (HPC), artificial intelligence (AI), 5G communication, and cloud computing applications. The imminent transition from established FinFET (Fin Field-Effect Transistor) architectures to Gate-All-Around (GAAFET) transistors at 3nm and beyond represents another pivotal technological shift, promising significantly improved gate control, enhanced current flow, and superior power efficiency, thereby defining the future trajectory of transistor scaling and performance enhancement.

Beyond the traditional realm of front-end wafer fabrication, advanced packaging technologies are rapidly ascending in importance, becoming equally pivotal in enhancing overall chip performance, integration capabilities, and system-level power efficiency. Innovative techniques such as 2.5D and 3D stacking, the burgeoning concept of chiplets, hybrid bonding, and fan-out wafer-level packaging (FOWLP) allow for the heterogeneous integration of disparate chip functions or multiple individual dies onto a single, compact package. This groundbreaking approach effectively circumvents some of the physical limitations associated with traditional Moore's Law scaling, enabling higher bandwidth, significantly lower power consumption, and much greater design flexibility. These innovations are indispensable for meeting the escalating demands of specialized compute architectures for AI and demanding data center environments, where high-speed communication between logic and memory is paramount. Leading foundries are aggressively expanding their capabilities and service offerings in these advanced packaging domains, providing comprehensive, end-to-end solutions that extend well beyond basic wafer processing to encompass full-scale chip integration and system-in-package (SiP) solutions, thereby adding substantial strategic value to their customers' product development.

Further integral components of the key technology landscape include continuous advancements in material science and the exploration of novel transistor structures to achieve unprecedented levels of performance and efficiency. Research and development into wide-bandgap semiconductors like gallium nitride (GaN) and silicon carbide (SiC) is revolutionizing power electronics, enabling more efficient power conversion and management for applications in electric vehicles, data centers, and renewable energy. Simultaneously, breakthroughs in areas such as silicon photonics are paving the way for ultra-fast optical data transfer within and between chips, critical for overcoming bottlenecks in high-bandwidth, low-latency applications. Moreover, the progressive integration of Artificial Intelligence and Machine Learning algorithms directly into the foundry's operational processes is profoundly optimizing manufacturing efficiency, improving defect detection and yield prediction, enhancing process control, and accelerating the overall design and production cycles. This synergistic pursuit of technological breakthroughs across materials, sophisticated lithography techniques, innovative transistor architectures, and advanced packaging solutions collectively ensures the semiconductor foundry market's enduring role at the forefront of global technological innovation, supporting the development of increasingly complex, powerful, and indispensable electronic systems across virtually every industry.

A semiconductor foundry is a specialized factory that manufactures integrated circuits (chips) for other companies based on their designs. It is critical because it enables fabless design companies to innovate without the immense capital cost of building their own fabs, accelerating technological advancement across various industries by providing access to cutting-edge manufacturing processes.

The market's growth is primarily driven by the escalating demand for advanced electronics across consumer, automotive, and industrial sectors, alongside the rapid expansion of AI, 5G, and IoT technologies. The inherent advantages of the fabless business model also fuel consistent demand for outsourced, specialized manufacturing services globally.

AI is significantly impacting the market by driving exponential demand for high-performance computing chips and specialized AI accelerators. It necessitates continuous advancements in cutting-edge process nodes and advanced packaging, creating both intricate technological challenges and substantial growth opportunities for foundries to innovate and expand capacity.

The Asia Pacific region, particularly Taiwan and South Korea, is dominant due to the presence of major foundries and a mature ecosystem. North America and Europe are increasingly important, with governments investing heavily to boost local manufacturing capabilities and enhance supply chain resilience for strategic technological independence.

Key technological trends include the widespread adoption of Extreme Ultraviolet (EUV) lithography for sub-7nm nodes, the transition to Gate-All-Around (GAAFET) transistors for superior performance, and the increasing reliance on advanced packaging techniques like 2.5D/3D stacking and chiplets to improve integration and power efficiency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.