ID : MRU_ 427808 | Date : Oct, 2025 | Pages : 241 | Region : Global | Publisher : MRU

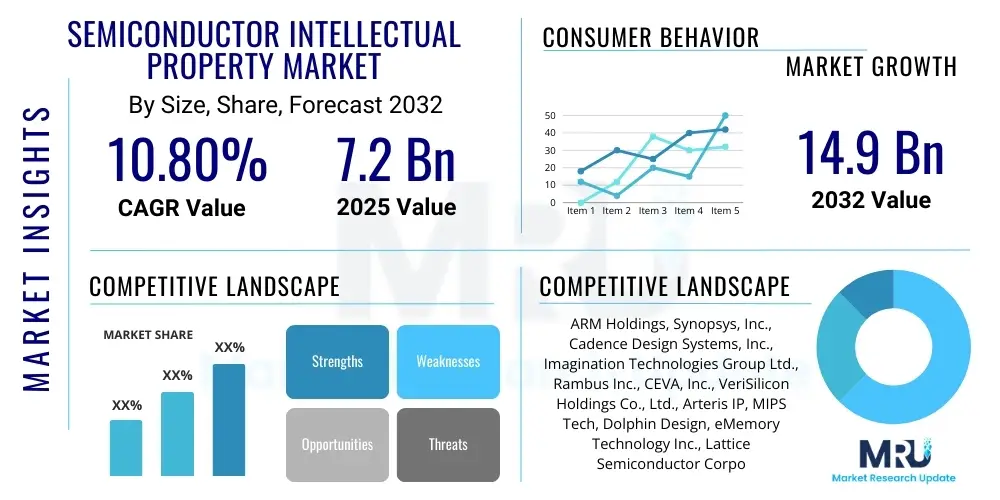

The Semiconductor Intellectual Property Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2032. The market is estimated at USD 7.2 Billion in 2025 and is projected to reach USD 14.9 Billion by the end of the forecast period in 2032.

The Semiconductor Intellectual Property (SIP) market encompasses the licensing and sale of reusable blocks of logic, memory, or physical design that are developed by third-party vendors for integration into larger semiconductor designs. These intellectual property cores, ranging from simple peripheral controllers to complex processor architectures, are crucial for modern chip design, enabling companies to accelerate time-to-market, reduce development costs, and focus on their core competencies. The rapid evolution of application-specific integrated circuits (ASICs) and system-on-chips (SoCs) across diverse industries fuels the continuous demand for a wide array of SIPs, driving innovation and efficiency in semiconductor development.

Major applications for SIP are pervasive, extending across consumer electronics, automotive, telecommunications, data centers, and industrial automation. For instance, advanced processor IP forms the core of smartphones and high-performance computing, while specialized interface IP is vital for connectivity in IoT devices. The benefits derived from utilizing SIP are substantial; they include significantly reduced design cycles, lower manufacturing costs due to optimized designs, and improved reliability through pre-verified and validated IP blocks. This strategic adoption allows chip designers to build highly complex and differentiated products without the need to develop every component from scratch, fostering a more agile and competitive ecosystem.

Several driving factors are propelling the growth of the SIP market. The escalating demand for high-performance, low-power, and compact electronic devices across all sectors necessitates increasingly sophisticated and integrated chip designs. The proliferation of emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), 5G connectivity, and autonomous vehicles creates an urgent need for specialized and optimized IP solutions. Furthermore, the rising complexity of semiconductor manufacturing processes and the associated financial and technical risks encourage companies to leverage external IP to mitigate development burdens, making SIP an indispensable component in the contemporary semiconductor landscape.

The Semiconductor Intellectual Property (SIP) market is experiencing robust expansion, characterized by dynamic business trends, evolving regional landscapes, and significant shifts across its various segments. Strategically, the market is witnessing increased consolidation through mergers and acquisitions, as larger technology firms seek to broaden their IP portfolios and enhance their competitive edge. Collaborations and licensing agreements are also proliferating, allowing IP developers and chip manufacturers to share resources and accelerate the development of advanced solutions. These business strategies are essential for navigating the rapidly changing demands of a technology-intensive industry, emphasizing specialized IP for emerging applications.

From a regional perspective, Asia-Pacific continues to dominate the SIP market, driven by its expansive semiconductor manufacturing capabilities, burgeoning consumer electronics sector, and significant investments in telecommunications and data centers, particularly in China, South Korea, and Taiwan. North America and Europe, while mature, remain critical innovation hubs, especially for high-end processor IP, specialized AI accelerators, and automotive-grade IP. Governments and private entities in these regions are actively funding research and development initiatives, fostering a fertile ground for the creation and adoption of next-generation SIP. Emerging markets, especially in Southeast Asia and Latin America, are also showing increasing potential as their digital infrastructure matures.

Segmentation trends within the SIP market highlight a growing demand for processor IP, particularly for ARM-based and RISC-V architectures, which cater to diverse applications from edge computing to cloud servers. Memory IP, crucial for data-intensive applications, and interface IP, essential for connectivity, are also experiencing significant growth. The shift towards application-specific IP for AI, 5G, and automotive is pronounced, reflecting the industrys need for highly optimized solutions. Furthermore, the adoption of soft macros over hard macros is gaining traction due to their flexibility and customization options, enabling designers to tailor IP to specific performance and power requirements with greater precision.

The pervasive integration of Artificial Intelligence (AI) and Machine Learning (ML) across virtually all industries is profoundly reshaping the Semiconductor Intellectual Property (SIP) market, prompting users to inquire about the impact on design methodologies, performance requirements, and the emergence of new IP types. Users frequently ask how AIs compute-intensive nature drives the need for specialized AI accelerators and efficient processing units, and how this translates into demand for advanced processor, memory, and interface IP. Concerns often revolve around the challenges of designing low-power, high-performance AI chips, the standardization of AI-specific IP, and the potential for AI tools to automate IP design and verification processes. Expectations are high for SIP vendors to deliver highly optimized, scalable, and customizable AI-centric IP solutions that address both edge AI and cloud AI demands, significantly influencing the markets trajectory towards more intelligent and autonomous systems.

AIs influence on the SIP market is multi-faceted, ranging from the architectural demands of AI workloads to the design tools and methodologies employed. The exponential growth in data generation and the increasing sophistication of AI algorithms necessitate more powerful and energy-efficient hardware. This has led to a surge in demand for specialized IP blocks capable of executing complex AI tasks, such as neural network inference and training, at high speeds and low power consumption. Traditional CPU and GPU architectures are being augmented or replaced by custom AI accelerators and Neural Processing Units (NPUs), which rely heavily on proprietary or licensed SIP for their core functionality. This shift drives innovation in processor IP, memory IP optimized for AI data flows, and high-bandwidth interface IP to manage the massive data transfers required by AI applications.

Moreover, AI is not merely a consumer of SIP but also a transformative force in its creation. AI-powered Electronic Design Automation (EDA) tools are emerging, promising to revolutionize the IP design and verification process by automating complex tasks, optimizing layouts, and identifying potential design flaws with greater efficiency and accuracy. This shift towards AI-assisted design shortens development cycles and improves the quality of IP cores. The demand for IP that supports various AI frameworks and standards is also growing, ensuring interoperability and ease of integration. The overall effect is a market rapidly evolving towards more intelligent, customized, and efficient IP solutions, driven by the imperative to support the next generation of AI-enabled devices and infrastructure.

The Semiconductor Intellectual Property (SIP) market is shaped by a complex interplay of driving forces, inherent restraints, and compelling opportunities that collectively determine its growth trajectory and competitive landscape. Key drivers include the ever-increasing complexity of System-on-Chip (SoC) designs, which makes it impractical for companies to develop every component in-house, thus necessitating the licensing of pre-verified IP blocks. The relentless demand for faster time-to-market (TTM) for new electronic products, fueled by rapid technological advancements and consumer expectations, further compels chip designers to integrate existing IP to accelerate development cycles. The proliferation of emerging technologies such as Artificial Intelligence (AI), Internet of Things (IoT), 5G communication, and autonomous vehicles creates an insatiable demand for specialized, high-performance, and low-power IP solutions, serving as a primary catalyst for market expansion.

Despite these strong tailwinds, the SIP market faces notable restraints. The high initial investment required for licensing advanced IP cores can be a significant barrier for smaller companies or startups, limiting their access to cutting-edge technology. Concerns regarding IP infringement and counterfeiting represent a persistent challenge, demanding robust legal frameworks and enforcement mechanisms to protect the intellectual property rights of developers. The scarcity of highly skilled engineers proficient in advanced chip design and IP integration also poses a restraint, hindering innovation and timely product development. Furthermore, the complexities associated with integrating IP from multiple vendors, including compatibility issues and verification challenges, can add unforeseen costs and delays to design projects.

However, abundant opportunities exist within the SIP market, particularly in the development of custom and application-specific IP tailored for niche and high-growth segments. The increasing adoption of open-source IP, such as the RISC-V architecture, presents a significant opportunity for market diversification and fostering innovation through community-driven development, potentially reducing licensing costs and increasing flexibility. Strategic alliances, collaborations, and mergers and acquisitions among IP vendors and semiconductor companies offer avenues for expanding product portfolios, gaining market share, and consolidating expertise. Emerging markets, with their rapidly expanding digital infrastructure and growing industrial automation, present untapped potential for SIP adoption, especially for cost-effective and energy-efficient solutions, making the SIP landscape dynamic and ripe for strategic investment and innovation.

The Semiconductor Intellectual Property (SIP) market is comprehensively segmented across various dimensions, including IP type, design method, and end-user industry, providing a granular view of market dynamics and growth opportunities. This detailed segmentation allows for a deeper understanding of specific market needs and trends, guiding strategic development and investment. Each segment reflects unique technological requirements, application scenarios, and competitive landscapes, collectively painting a complete picture of the SIP ecosystem. Understanding these segments is crucial for IP vendors to tailor their offerings, for chip designers to select appropriate IP, and for investors to identify high-growth areas within the market.

The Semiconductor Intellectual Property (SIP) markets value chain is a complex ecosystem involving multiple stages, starting from conceptualization and design tools to final integration into end products, with diverse players at each step. The upstream segment of this value chain is dominated by Electronic Design Automation (EDA) tool vendors, who provide the critical software and methodologies necessary for designing, verifying, and integrating IP cores. These tools are indispensable for IP developers to create robust, efficient, and error-free IP blocks. Additionally, independent IP design houses and research institutions play a vital role upstream by innovating new IP architectures and specialized functionalities that address evolving market demands, often collaborating with EDA tool providers to optimize their design flows.

In the midstream, the core activities revolve around IP development, licensing, and manufacturing. This segment includes dedicated SIP vendors, who specialize in creating and licensing a broad portfolio of IP ranging from processor cores to complex interface solutions. Foundries and Integrated Device Manufacturers (IDMs) also play a crucial role by providing the manufacturing capabilities and often integrating licensed IP into their own chip designs. The distribution channel for SIP is predominantly direct, involving direct licensing agreements between IP providers and chip design companies. These agreements can be highly customized, offering different tiers of access and support based on the licensees specific needs, ensuring tailored solutions and ongoing technical assistance throughout the design and production phases.

The downstream segment of the value chain involves the ultimate integration of SIP into a complete System-on-Chip (SoC) by chip designers, fabless semiconductor companies, and IDMs, followed by the deployment of these chips into final electronic products. These end-users, across various industries such as consumer electronics, automotive, and telecommunications, are the ultimate beneficiaries of SIP, leveraging it to create differentiated products with reduced development costs and accelerated time-to-market. Indirect distribution channels, while less prevalent for core IP, might include design service providers who integrate and customize IP for their clients, thereby extending the reach and application of various SIP blocks into a wider array of specialized products and solutions.

The Semiconductor Intellectual Property (SIP) market primarily serves a diverse array of end-users and buyers who are actively involved in the design and manufacturing of semiconductor chips across various industries. These potential customers are typically organizations that require pre-designed, verified, and reusable blocks of intellectual property to develop their own complex System-on-Chips (SoCs) or Application-Specific Integrated Circuits (ASICs). The primary goal for these customers is to significantly reduce their design cycles, mitigate development risks, lower overall production costs, and accelerate their time-to-market for innovative electronic products, making SIP an indispensable resource in a highly competitive and technologically driven landscape.

Key segments of potential customers include fabless semiconductor companies, which specialize exclusively in the design and sale of semiconductor chips without owning manufacturing facilities. These companies heavily rely on licensed SIP to build their products, integrating various processor, memory, and interface IP blocks into their designs before outsourcing fabrication to foundries. Integrated Device Manufacturers (IDMs), which design, manufacture, and sell their own chips, also constitute a significant customer base. While IDMs possess internal IP development capabilities, they frequently license external SIP to augment their portfolios, particularly for highly specialized or new technological components, ensuring they remain at the forefront of innovation and market trends.

Beyond traditional chip manufacturers, system integrators and large original equipment manufacturers (OEMs) with in-house chip design capabilities are emerging as vital potential customers. Companies in the automotive, telecommunications, and consumer electronics sectors, for example, are increasingly designing their own custom chips for specialized applications like ADAS, 5G modems, or AI accelerators. These OEMs leverage SIP to gain a competitive edge by creating highly optimized and differentiated products. Additionally, design service providers and electronic design houses, which offer bespoke chip design services to smaller companies, frequently license and integrate SIP on behalf of their clients, thereby acting as indirect consumers of IP and extending its reach across the broader electronics industry.

The Semiconductor Intellectual Property (SIP) market is characterized by a dynamic and evolving technology landscape, driven by continuous innovation in chip architectures, design methodologies, and manufacturing processes. At the heart of this landscape are foundational processor architectures, such as ARM Holdings widely adopted ARM architecture, which forms the basis for a vast array of mobile, embedded, and increasingly server and automotive applications. The open-source RISC-V instruction set architecture (ISA) has emerged as a significant disruptor, offering unparalleled flexibility, customization, and cost advantages, leading to its rapid adoption for specialized applications, AI accelerators, and IoT devices. This growing diversity in processor IP necessitates a robust ecosystem of compatible memory, interface, and peripheral IP to support a wide range of end-user requirements.

Beyond processor cores, the technology landscape is heavily influenced by advancements in memory and interface IP. High-Bandwidth Memory (HBM) and DDR5/LPDDR5 memory controllers are critical for data-intensive applications like AI, high-performance computing (HPC), and graphics, driving the need for sophisticated memory IP solutions. Concurrently, high-speed interface IP, including PCIe Gen5/Gen6, USB4, and various Ethernet standards, is essential for enabling rapid data transfer and connectivity in complex SoCs, facilitating the integration of diverse functionalities. The move towards advanced packaging technologies, such as 2.5D and 3D integration, also profoundly impacts SIP, requiring IP blocks to be designed with explicit considerations for inter-die communication, power delivery, and thermal management within heterogeneous integrated systems.

Furthermore, the technology landscape of SIP is increasingly shaped by advancements in Electronic Design Automation (EDA) tools and methodologies, which are crucial for the efficient design, verification, and integration of IP blocks. Innovations in AI-driven EDA are streamlining design processes, automating layout generation, and enhancing verification accuracy, thereby accelerating the development of next-generation IP. Security IP, including hardware roots of trust, cryptographic accelerators, and secure enclaves, is gaining paramount importance due to the escalating threats in connected devices and data centers. The convergence of these technological advancements, from architectural innovations to design tools and security features, collectively defines the cutting-edge of the SIP market, enabling the creation of highly complex, secure, and performant semiconductor solutions for the future.

The primary driving force is the increasing complexity of System-on-Chip (SoC) designs, coupled with the urgent need for faster time-to-market and reduced development costs across various industries. The proliferation of AI, IoT, 5G, and autonomous vehicles also creates an insatiable demand for specialized, high-performance, and low-power IP solutions, accelerating market expansion significantly.

AI is profoundly impacting SIP by driving demand for specialized AI accelerator IP cores and Neural Processing Units (NPUs) optimized for high-performance and low-power AI workloads. It also necessitates advanced memory IP for data-intensive AI operations and high-speed interface IP. Furthermore, AI is revolutionizing SIP design through AI-driven Electronic Design Automation (EDA) tools, enhancing efficiency and accuracy.

The Asia-Pacific region dominates the Semiconductor Intellectual Property market. This dominance is attributed to its vast semiconductor manufacturing infrastructure, a booming consumer electronics sector, significant investments in telecommunications, and strong government support for technological advancements in key countries like China, South Korea, and Taiwan. This leads to high volume production and consumption of chips utilizing diverse SIP solutions.

Key challenges include the high initial investment cost for licensing advanced IP cores, which can be prohibitive for smaller entities. Persistent concerns about IP infringement and counterfeiting, along with a global shortage of highly skilled engineers proficient in advanced chip design and IP integration, also act as significant restraints. Additionally, complex integration issues when combining IP from multiple vendors can cause delays and increased costs.

Significant opportunities exist in developing custom and application-specific IP for niche, high-growth segments such as edge AI, specialized automotive electronics, and industrial IoT. The rise of open-source IP architectures like RISC-V offers avenues for innovation, reduced costs, and increased flexibility. Strategic alliances and mergers provide growth pathways, while emerging markets present untapped potential for cost-effective and energy-efficient SIP solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.