ID : MRU_ 430400 | Date : Nov, 2025 | Pages : 249 | Region : Global | Publisher : MRU

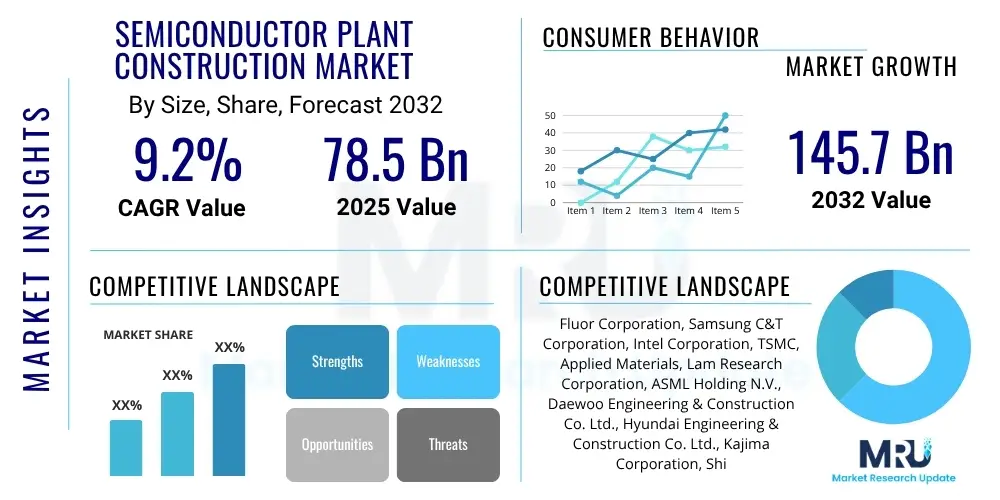

The Semiconductor Plant Construction Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2032. The market is estimated at USD 78.5 billion in 2025 and is projected to reach USD 145.7 billion by the end of the forecast period in 2032.

The Semiconductor Plant Construction Market encompasses the comprehensive range of activities involved in designing, engineering, constructing, and commissioning highly specialized manufacturing facilities known as fabs (fabrication plants). These facilities are critical for producing integrated circuits, microprocessors, memory chips, and various other semiconductor devices essential for modern electronics. The market's product description extends beyond basic building structures to include ultra-clean environments, precise temperature and humidity controls, advanced material handling systems, extensive utility infrastructure (ultra-pure water, specialty gases, high-purity chemicals), and complex electrical and mechanical systems designed to support sensitive semiconductor manufacturing processes. The construction involves highly specialized expertise in cleanroom technology, vibration isolation, and hazardous material management, ensuring operational integrity and product yield.

Major applications for the output of these plants span virtually every sector of the global economy, including consumer electronics (smartphones, laptops, tablets), automotive systems (ADAS, infotainment, electric vehicles), industrial automation, telecommunications infrastructure (5G, data centers), and emerging technologies such as artificial intelligence, machine learning, and the Internet of Things (IoT). The benefits of investing in new semiconductor plant construction are multifaceted, including bolstering national technological sovereignty, creating high-value employment, fostering innovation, and ensuring resilient global supply chains. These facilities are pivotal in enabling continued technological advancement across industries by providing the foundational hardware necessary for next-generation products and services.

Driving factors for market expansion are primarily anchored in the relentless global demand for increasingly powerful and efficient semiconductor chips. This demand is further amplified by significant government incentives, particularly in North America and Europe, aimed at regionalizing semiconductor manufacturing to mitigate geopolitical risks and supply chain vulnerabilities. Technological advancements, such as the transition to smaller process nodes, advanced packaging solutions, and the proliferation of AI and IoT devices, necessitate continuous investment in new, more sophisticated fabrication facilities. Furthermore, the strategic imperative for companies to maintain a competitive edge and expand production capacities to meet burgeoning market needs acts as a substantial impetus for ongoing construction projects worldwide.

The Semiconductor Plant Construction Market is experiencing robust growth driven by a convergence of technological imperatives, geopolitical strategies, and burgeoning end-user demand. Business trends highlight a significant increase in capital expenditure by leading semiconductor manufacturers globally, aimed at expanding production capacities and diversifying geographical footprints. There is a palpable shift towards establishing more resilient and localized supply chains, catalyzed by recent global disruptions and national security concerns. Sustainable construction practices and energy-efficient fab designs are also gaining prominence as companies strive to reduce their environmental impact and operational costs, integrating advanced green building technologies and renewable energy solutions into new projects.

Regional trends demonstrate a continued dominance of Asia-Pacific, particularly in Taiwan, South Korea, and China, where major foundries and IDMs are investing heavily in new facilities and expansions. However, North America and Europe are witnessing a renaissance in semiconductor manufacturing, fueled by substantial government initiatives like the CHIPS and Science Act in the US and the European Chips Act. These policies are attracting significant foreign direct investment and fostering domestic manufacturing capabilities, leading to a surge in planned and ongoing fab construction projects across these regions. This regional diversification aims to de-risk the global supply chain and foster technological independence.

Segment trends reveal accelerated investments in advanced logic and memory production, driven by the escalating requirements of AI, high-performance computing (HPC), and 5G technologies. Foundries and Integrated Device Manufacturers (IDMs) are investing heavily in state-of-the-art facilities capable of producing chips at 3nm and 2nm process nodes. Furthermore, there is a growing emphasis on advanced packaging facilities, which are crucial for improving chip performance and integration. The market also sees specialized construction for mature nodes to cater to automotive and industrial applications, where legacy technologies remain critical but face persistent supply shortages. This multifaceted investment across various chip types and manufacturing stages underpins the market's dynamic growth trajectory.

User inquiries regarding the impact of Artificial Intelligence on the Semiconductor Plant Construction Market frequently center on several key themes: how AI drives the demand for new and more advanced fabs, its role in optimizing the construction process itself, and the implications for the design and operational efficiency of these highly complex facilities. Users are keen to understand if AI will lead to a surge in construction projects for specialized AI chips, whether AI tools can streamline project management and reduce costs, and what challenges might arise from integrating AI technologies into traditional construction methodologies. There is also considerable interest in how AI can contribute to the "smart fab" concept, enhancing predictive maintenance, resource management, and overall operational intelligence within the completed plants.

Based on this analysis, the key themes indicate that users expect AI to be both a significant demand driver for the semiconductor industry and a transformative technology within the construction sector. Concerns often revolve around the upfront investment required for AI integration, the need for specialized skills, and data security. Expectations are high for AI to deliver substantial improvements in project efficiency, cost reduction, safety, and the ability to design and build facilities that are inherently smarter and more resilient to operational challenges. The pervasive nature of AI in technology is creating an urgent need for manufacturing infrastructure capable of producing the chips that power it, while simultaneously offering powerful tools to make the construction of that infrastructure more intelligent and efficient.

The Semiconductor Plant Construction Market is significantly shaped by a powerful array of Drivers, Restraints, and Opportunities, which collectively constitute its Impact Forces. Primary drivers include the insatiable global demand for semiconductor chips across diverse end-use applications, ranging from consumer electronics and automotive to advanced computing and AI. This demand is further amplified by geopolitical strategies advocating for supply chain resilience and regionalization, leading governments worldwide to offer substantial incentives and subsidies for domestic fab construction. Continuous technological advancements, such as the development of smaller process nodes and advanced packaging, necessitate constant investment in new, more sophisticated manufacturing facilities capable of handling these complex requirements. Moreover, intense competition among semiconductor manufacturers drives capacity expansion to secure market share and maintain technological leadership, fueling construction activity.

However, the market also faces considerable restraints. The extremely high capital expenditure required for fab construction, often running into tens of billions of dollars, poses a significant barrier to entry and expansion. This financial burden is exacerbated by the long lead times for construction, which can span several years, creating uncertainty in market demand projections. A critical shortage of skilled labor, including specialized engineers, architects, and construction workers with expertise in cleanroom environments, hampers project execution and increases costs. Stringent environmental regulations and the complex permitting processes for large-scale industrial projects add layers of complexity and potential delays. Additionally, global economic fluctuations, inflation, and disruptions in the supply chain for specialized construction materials and equipment can impact project timelines and budgets.

Despite these challenges, abundant opportunities exist. The massive growth potential in emerging technologies like artificial intelligence, machine learning, IoT, and quantum computing is creating a sustained and escalating demand for advanced semiconductors, directly translating into the need for new fabrication facilities. The trend towards regionalization and government-backed initiatives presents a unique opportunity for construction firms to secure long-term projects in strategic locations. Innovation in sustainable construction methods and green fab designs offers a competitive advantage and aligns with corporate environmental goals. Furthermore, the increasing complexity of chips is driving demand for advanced packaging facilities, a distinct and rapidly growing segment within the broader semiconductor ecosystem, providing new avenues for construction specialization. The collective interplay of these forces dictates the pace and direction of market development.

The Semiconductor Plant Construction market is highly diversified and can be analyzed across various segments, reflecting the complexity and specialization required for these advanced manufacturing facilities. Understanding these segmentations provides critical insights into market dynamics, identifying key growth areas and strategic investment opportunities. These segments cover different types of facilities, the specific phases of construction, the cleanroom classifications essential for manufacturing, the diverse end-use applications of the chips produced, and the array of services offered throughout the construction lifecycle.

The value chain for the Semiconductor Plant Construction Market is a complex, multi-layered ecosystem involving specialized expertise and intricate interdependencies from upstream suppliers to downstream operators. Upstream analysis focuses on the foundational elements and resources required before physical construction commences. This includes suppliers of highly specialized raw materials such as ultra-high purity metals, advanced polymers, and specialized concrete formulations designed to meet stringent vibration and chemical resistance requirements. Equipment manufacturers play a crucial role, providing advanced HVAC systems for cleanrooms, ultra-pure water generation systems, specialty gas delivery systems, and sophisticated fire suppression and safety equipment. Furthermore, design software providers (e.g., BIM tools, CAD software) and engineering consultancies specializing in cleanroom design, process layout, and facility integration are vital components, defining the blueprint for the entire project. Early engagement with these upstream partners is critical for successful project execution and cost control.

The core construction phase involves a network of general contractors, specialized subcontractors, and system integrators who translate the designs into physical structures. These entities are responsible for site preparation, civil works, structural erection, and the meticulous installation of complex mechanical, electrical, and process systems. Their role is to ensure that the facility adheres to the exacting standards required for semiconductor manufacturing, including precise environmental controls, vibration isolation, and contamination prevention. Downstream analysis primarily involves the end-users and operators of these facilities: the semiconductor manufacturers themselves. This includes Integrated Device Manufacturers (IDMs) like Intel and Samsung, pure-play foundries such as TSMC, and Outsourced Semiconductor Assembly and Test (OSAT) providers. These entities are the ultimate beneficiaries of the construction process, leveraging the completed fabs to produce their semiconductor devices.

Distribution channels in this market are predominantly direct, characterized by highly customized contracts between semiconductor manufacturers and specialized engineering, procurement, and construction (EPC) firms or general contractors. Due to the bespoke nature and immense scale of these projects, indirect channels are less common for the main construction contracts, though they exist for specific component or service procurements. Direct engagement ensures close collaboration, tailored solutions, and direct oversight, which are critical for meeting the stringent specifications and timelines of fab construction. Partnerships and consortiums between construction companies, equipment suppliers, and technology providers are also common, pooling expertise and resources for mega-projects. This direct, project-specific approach allows for seamless integration of highly specialized technologies and ensures that the finished plant meets the exact operational requirements of the semiconductor manufacturing processes it will house.

The primary potential customers and end-users of the Semiconductor Plant Construction Market are the leading global players in the semiconductor industry, characterized by their significant capital investments and strategic need for advanced manufacturing capabilities. Integrated Device Manufacturers (IDMs) represent a substantial customer segment; these companies design, manufacture, and sell their own semiconductor products, requiring state-of-the-art fabs to maintain their competitive edge and control their supply chain. Prominent examples include Intel, Samsung Electronics, and Micron Technology, all of whom consistently invest billions in new fab construction or expansion projects to support their diverse product portfolios, from CPUs and memory to specialized components.

Pure-play foundries constitute another critical customer base. These companies specialize exclusively in manufacturing chips designed by other fabless semiconductor companies. TSMC, GlobalFoundries, and UMC are prime examples, continually expanding their capacities and technological prowess to serve a vast array of clients across various industries. Their business model inherently drives demand for new, technologically advanced fabs capable of fabricating chips at the latest process nodes, thereby directly influencing the construction market. The increasing trend of outsourcing manufacturing by fabless companies directly fuels the growth of these foundries and, consequently, the demand for new construction.

Furthermore, Outsourced Semiconductor Assembly and Test (OSAT) providers also represent a growing segment of potential customers. Companies like ASE Technology Holding and Amkor Technology require specialized facilities for packaging, assembly, and testing of semiconductor devices. As chip designs become more complex and advanced packaging solutions gain prominence, the demand for purpose-built OSAT facilities is on the rise. Additionally, government-funded research institutions and national semiconductor initiatives, particularly in regions aiming to boost domestic chip production, serve as indirect customers, often partnering with or funding private entities for the construction of R&D or pilot production facilities. The consistent and substantial capital expenditure by these industry giants and strategic governmental bodies ensures a robust and ongoing demand for specialized semiconductor plant construction services.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 78.5 billion |

| Market Forecast in 2032 | USD 145.7 billion |

| Growth Rate | 9.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Fluor Corporation, Samsung C&T Corporation, Intel Corporation, TSMC, Applied Materials, Lam Research Corporation, ASML Holding N.V., Daewoo Engineering & Construction Co. Ltd., Hyundai Engineering & Construction Co. Ltd., Kajima Corporation, Shimizu Corporation, Nikon Corporation, KLA Corporation, Tokyo Electron Limited, Bechtel Corporation, Jacobs Engineering Group Inc., M+W Group (Exyte), Chiyoda Corporation, CannonDesign, DPR Construction. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Semiconductor Plant Construction Market is heavily reliant on a sophisticated technology landscape, driven by the imperative to create highly controlled, efficient, and resilient manufacturing environments. Advanced cleanroom technologies form the cornerstone of this landscape, encompassing specialized air filtration systems (HEPA and ULPA filters), stringent particle control protocols, precise temperature and humidity regulation, and advanced materials for surfaces that minimize contamination. These technologies are crucial for achieving ultra-low particle counts, sometimes down to ISO Class 1, which are essential for manufacturing microchips at nanometer scales. Furthermore, localized clean environments, such as mini-environments and standard mechanical interface (SMIF) pods, are increasingly deployed to protect wafers during transport and processing, further enhancing contamination control and optimizing energy usage.

Automation and smart construction technologies are transforming the planning, execution, and operation of semiconductor fabs. Building Information Modeling (BIM) is widely adopted for comprehensive 3D design, clash detection, facility management, and lifecycle information management, enabling seamless collaboration among diverse stakeholders and reducing construction errors. Robotics and automated guided vehicles (AGVs) are utilized for repetitive tasks, material handling, and even precise installation in hazardous or confined spaces, enhancing safety and efficiency. The integration of the Internet of Things (IoT) sensors throughout the construction site and within the completed fab allows for real-time monitoring of progress, equipment health, environmental conditions, and resource utilization, facilitating proactive management and predictive maintenance. This shift towards digital construction and smart fab concepts optimizes construction timelines and future operational efficiency.

Sustainability and energy efficiency are also paramount, driving the adoption of green construction technologies. This includes advanced energy management systems, renewable energy integration (solar panels, geothermal), efficient water recycling and treatment plants (especially for ultra-pure water systems), and the use of low-impact, recycled, or locally sourced construction materials. Waste heat recovery systems, high-efficiency HVAC, and intelligent lighting controls are standard features in modern fab designs. Additionally, specialized technologies for vibration isolation and electromagnetic interference (EMI) shielding are crucial to protect sensitive manufacturing equipment from external disturbances. The continuous evolution of these technologies ensures that new semiconductor plants are not only highly productive but also environmentally responsible and future-proofed for next-generation chip production.

The market is primarily driven by escalating global demand for semiconductor chips across various industries, significant government incentives aimed at regionalizing chip production, continuous technological advancements requiring new manufacturing capabilities, and intense competition among leading semiconductor manufacturers to expand capacity and market share.

Government incentives, such as those provided by the US CHIPS Act and the European Chips Act, significantly boost the market by offering substantial subsidies, tax credits, and financial support to companies investing in new fab construction. These initiatives reduce the financial burden, encourage domestic manufacturing, and enhance supply chain resilience, attracting billions in capital expenditure.

AI plays a dual role: it drives increased demand for advanced semiconductor chips, necessitating new fabs, and it optimizes the construction process itself. AI tools enhance design through generative design, improve project management via predictive analytics, enable automation on site with robotics, and support smart fab operations post-construction for efficiency and maintenance.

Key challenges include the extremely high capital expenditure required, lengthy construction lead times, a critical shortage of skilled labor specializing in cleanroom environments, complex environmental regulations and permitting processes, and potential disruptions in the global supply chain for specialized materials and equipment.

Asia Pacific, particularly Taiwan, South Korea, and China, remains the dominant region with extensive ongoing investments. North America and Europe are experiencing significant growth due to substantial government initiatives aimed at re-shoring and expanding domestic semiconductor manufacturing capabilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.