ID : MRU_ 429825 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

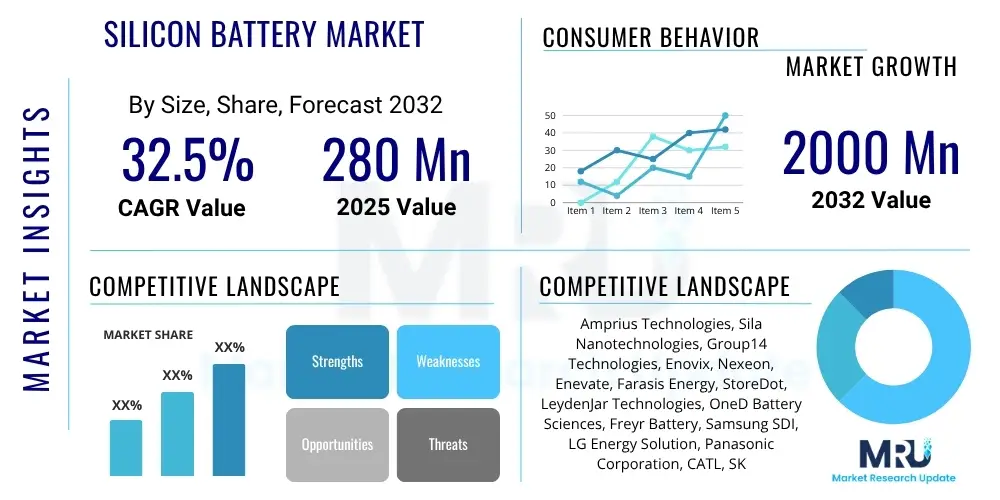

The Silicon Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 32.5% between 2025 and 2032. The market is estimated at $280 million in 2025 and is projected to reach $2000 million by the end of the forecast period in 2032.

The Silicon Battery Market represents a transformative segment within the broader energy storage industry, poised to redefine performance benchmarks for rechargeable batteries. Silicon batteries, utilizing silicon-based anode materials instead of traditional graphite, offer a significant leap in energy density, power output, and charge speed. This innovation addresses the critical demand for more efficient and longer-lasting power solutions across various sectors, driven by rapid technological advancements and increasing energy consumption.

The core product, the silicon battery, leverages the high theoretical specific capacity of silicon, which is ten times greater than that of graphite. Major applications span electric vehicles (EVs), where extended range and faster charging are paramount, to consumer electronics like smartphones, laptops, and wearables requiring slimmer profiles and prolonged operational life. Furthermore, these batteries hold immense potential for grid-scale energy storage, medical devices, and aerospace applications due to their superior performance characteristics. The primary benefits include dramatically increased energy density, enabling smaller and lighter battery packs; significantly faster charging times; and a potentially longer cycle life, translating to enhanced user experience and reduced total cost of ownership. Key driving factors accelerating market adoption include the global push for electrification in transportation, the incessant demand for advanced portable electronic devices, stringent environmental regulations promoting cleaner energy solutions, and substantial investments in battery research and development.

The Silicon Battery Market is currently experiencing a dynamic phase characterized by intense innovation, strategic partnerships, and increasing investor interest, signaling a robust growth trajectory over the forecast period. Business trends indicate a strong focus on overcoming technical challenges such as silicon anode swelling and electrolyte instability, leading to significant advancements in material science and cell design. Companies are actively pursuing collaborations with automotive OEMs and consumer electronics manufacturers to integrate silicon anode technology into next-generation products, thereby accelerating commercialization efforts. The competitive landscape is evolving with established battery manufacturers and innovative startups vying for market share through patented technologies and production scaling.

Regionally, Asia-Pacific is anticipated to remain a dominant force, driven by its robust manufacturing infrastructure, particularly in countries like China, South Korea, and Japan, which are at the forefront of battery production and EV adoption. North America and Europe are expected to witness substantial growth, fueled by strong government initiatives supporting EV mandates, significant R&D investments, and a growing consumer appetite for high-performance electronics. These regions are also focusing on establishing localized supply chains to reduce reliance on foreign imports and enhance energy security. Segment-wise, consumer electronics are expected to be early adopters due to the immediate benefits of smaller, lighter, and longer-lasting devices, providing a critical testing ground for the technology. However, the electric vehicle segment is projected to be the largest and most impactful growth driver in the long term, as silicon batteries directly address the range anxiety and charging time concerns that are crucial for widespread EV adoption. Grid energy storage and specialized industrial applications also present significant untapped potential, further diversifying the market's revenue streams.

User inquiries frequently revolve around how Artificial Intelligence (AI) can accelerate the development, optimize the performance, and enhance the lifecycle of silicon batteries. Common questions highlight concerns about the complexity of silicon material science, the need for efficient manufacturing processes, and the desire for intelligent battery management. Users seek to understand AI's role in addressing challenges such as silicon expansion, predicting battery degradation, and tailoring charging profiles for optimal longevity. The overarching expectation is that AI will act as a catalyst, overcoming current limitations and unlocking the full potential of silicon anode technology, thereby speeding up its commercial viability and widespread integration across applications.

The Silicon Battery Market is shaped by a confluence of influential factors, encompassing strong drivers that propel its growth, inherent restraints that pose challenges, and significant opportunities that promise future expansion. Key drivers include the escalating global demand for higher energy density batteries, primarily from the burgeoning electric vehicle sector and the ever-evolving consumer electronics industry, which continuously seeks smaller, lighter, and more powerful devices. The push for faster charging capabilities, coupled with the imperative for longer battery life, also acts as a powerful catalyst for silicon battery adoption. Restraints primarily revolve around the technical complexities associated with silicon anodes, such as the significant volumetric expansion during lithiation/de-lithiation cycles, which can lead to mechanical degradation and reduced cycle life. Manufacturing scalability and the relatively higher production costs compared to conventional lithium-ion batteries also present hurdles. Opportunities, however, are vast and include tapping into new application areas requiring ultra-high performance, such as aerospace, defense, and advanced robotics, as well as developing specialized solutions for grid energy storage and medical implants. The continuous influx of research and development investments and strategic partnerships between material suppliers, battery manufacturers, and end-users are critical impact forces.

The intricate interplay between these forces dictates the market's trajectory. Technological breakthroughs in silicon anode engineering, binder chemistries, and electrolyte formulations are crucial for mitigating restraints and unlocking full potential. Regulatory support for electric vehicles and renewable energy storage, often accompanied by subsidies and incentives, further stimulates demand. The availability of raw materials and the development of robust supply chains are also significant impact forces, influencing production costs and market accessibility. Furthermore, the competitive landscape, with numerous startups and established players investing heavily in silicon battery technology, ensures continuous innovation and refinement of products, driving the market towards greater maturity and widespread commercialization. Addressing the current limitations while strategically leveraging the vast opportunities will be pivotal for sustained market growth and the successful integration of silicon batteries into mainstream applications.

The Silicon Battery Market is meticulously segmented across various dimensions to provide a comprehensive understanding of its structure, dynamics, and growth prospects. These segmentations allow for detailed analysis of market penetration, competitive positioning, and targeted development strategies. The primary segmentation categories include the type of silicon anode technology employed, the diverse range of end-use applications, and the capacity ratings of the batteries, reflecting varied performance requirements across different products. Further segmentation by end-use industry helps to identify the major sectors driving demand and innovation within the market.

Each segment presents unique growth drivers and challenges, influencing investment decisions and product development priorities. For instance, the electric vehicle segment demands high energy density, power, and cycle life, while consumer electronics prioritize miniaturization and fast charging. Understanding these nuances through detailed segmentation analysis enables market participants to tailor their offerings effectively and capitalize on specific opportunities. The continuous evolution of silicon battery technology and its integration into new products will likely lead to the emergence of additional, more granular segments over the forecast period, reflecting the market's maturation and diversification.

The value chain for the Silicon Battery Market encompasses a series of interconnected stages, beginning with the sourcing and processing of raw materials and extending through manufacturing, integration, and final distribution to end-users. At the upstream level, the chain involves suppliers of critical raw materials, primarily silicon (in various forms like silicon nanoparticles, nanowires, or porous silicon), lithium, electrolytes, separators, and cathode materials. These suppliers play a crucial role in providing high-purity, specialized components that meet the stringent requirements of advanced battery chemistry. Research and development institutions also form an integral part of the upstream segment, continually innovating new materials and cell designs to enhance performance and overcome technical challenges. The quality and availability of these upstream components directly impact the cost and efficiency of silicon battery production.

Moving downstream, the value chain progresses through the actual manufacturing of silicon battery cells, which involves sophisticated processes such as anode fabrication, cell assembly, and formation. This stage includes specialized battery cell manufacturers and, increasingly, vertically integrated companies that control multiple steps. Further downstream are battery pack integrators who combine individual cells into larger modules and packs, often incorporating advanced Battery Management Systems (BMS) tailored for specific applications like electric vehicles or grid storage. The distribution channel then connects these manufactured products to the end-users. Distribution can be direct, particularly for large-volume orders to automotive OEMs or major consumer electronics brands, involving direct sales teams and established partnerships. Indirect channels include specialized distributors, value-added resellers, and retail networks for smaller-scale or consumer-facing products. The efficiency and robustness of this entire value chain are critical for the successful commercialization and widespread adoption of silicon battery technology, ensuring consistent quality, competitive pricing, and timely delivery to meet market demand.

The potential customers for silicon batteries represent a broad spectrum of industries and end-users, each driven by a distinct set of performance requirements and strategic imperatives. Electric vehicle manufacturers stand as a primary and highly significant customer segment, as they constantly seek to improve vehicle range, reduce charging times, and lower overall battery weight to enhance performance and consumer appeal. The adoption of silicon batteries could be a game-changer for these companies, enabling next-generation EV models that effectively compete with traditional internal combustion engine vehicles.

Beyond the automotive sector, consumer electronics giants manufacturing smartphones, laptops, tablets, and wearable devices are keenly interested in silicon batteries for their potential to enable thinner, lighter designs with extended battery life and rapid charging capabilities. Energy companies and grid operators also represent a burgeoning customer base, as they require high-capacity, durable, and cost-effective energy storage solutions to integrate renewable energy sources and stabilize power grids. Furthermore, specialized applications in medical devices, requiring compact, long-lasting, and reliable power sources, alongside aerospace and defense industries seeking high-performance, lightweight batteries for critical missions, complete the diverse portfolio of potential customers ready to adopt silicon battery technology as it matures and becomes more readily available.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $280 million |

| Market Forecast in 2032 | $2000 million |

| Growth Rate | CAGR 32.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amprius Technologies, Sila Nanotechnologies, Group14 Technologies, Enovix, Nexeon, Enevate, Farasis Energy, StoreDot, LeydenJar Technologies, OneD Battery Sciences, Freyr Battery, Samsung SDI, LG Energy Solution, Panasonic Corporation, CATL, SK Innovation, Varta AG, Britishvolt, QuantumScape, PolyPlus Battery Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Silicon Battery Market is characterized by a rapidly evolving technological landscape, where continuous innovation is crucial for overcoming inherent challenges and unlocking the full potential of silicon anode materials. Central to this landscape are advancements in silicon material engineering, focusing on mitigating volumetric expansion during charge-discharge cycles. This includes the development of silicon nanowires, nanoparticles, and porous silicon structures designed to accommodate volume changes without causing mechanical degradation. Additionally, silicon-carbon composite anodes, which combine the high capacity of silicon with the stability and conductivity of graphite, represent a significant technological approach, offering a balance between performance and durability. The careful design of these anode architectures is paramount to achieving desired cycle life and energy density.

Beyond the anode material itself, other critical technologies include advanced binder systems and novel electrolyte formulations. New binder materials are being engineered to maintain the structural integrity of the silicon anode despite repeated expansion and contraction, ensuring electrode cohesion and prolonged performance. Concurrently, specialized electrolyte additives and novel liquid or solid-state electrolytes are under development to form stable solid-electrolyte interphase (SEI) layers on the silicon surface, which is vital for preventing continuous electrolyte consumption and improving battery longevity. Pre-lithiation techniques are also emerging as a key technology to compensate for the initial irreversible lithium loss, thereby enhancing the usable capacity of silicon batteries. Manufacturing innovations, such as advanced coating techniques and dry electrode processes, are also being explored to reduce production costs and improve scalability, further shaping the competitive and technological frontier of the silicon battery market.

Silicon batteries are a type of lithium-ion battery that replaces the traditional graphite anode with a silicon-based material. This modification significantly increases the battery's energy density, allowing for more power in a smaller, lighter package and enabling faster charging times compared to conventional lithium-ion batteries.

The primary advantages of silicon batteries include a much higher energy density, which translates to longer run times for electronics and extended range for electric vehicles. They also offer faster charging capabilities and potentially longer cycle life, making them a superior choice for various high-performance applications requiring efficient and compact power sources.

The main challenges involve the significant volumetric expansion of silicon during charging and discharging, which can lead to mechanical stress, electrode degradation, and reduced battery lifespan. Other hurdles include maintaining stable solid-electrolyte interphase (SEI), higher manufacturing costs, and achieving consistent cycle stability and safety comparable to graphite-based batteries.

Silicon batteries are already seeing limited commercialization in specialized consumer electronics and are undergoing extensive testing for electric vehicle integration. While widespread mass adoption in EVs is anticipated within the next 3-5 years (by 2028-2030), continuous advancements are accelerating their market readiness across various applications.

The primary applications for silicon batteries include electric vehicles (EVs) due to their potential for increased range and faster charging, and consumer electronics such as smartphones, laptops, and wearables, where smaller form factors and longer battery life are highly valued. They also hold promise for grid energy storage, medical devices, and aerospace applications demanding high performance and reliability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.