ID : MRU_ 428155 | Date : Oct, 2025 | Pages : 251 | Region : Global | Publisher : MRU

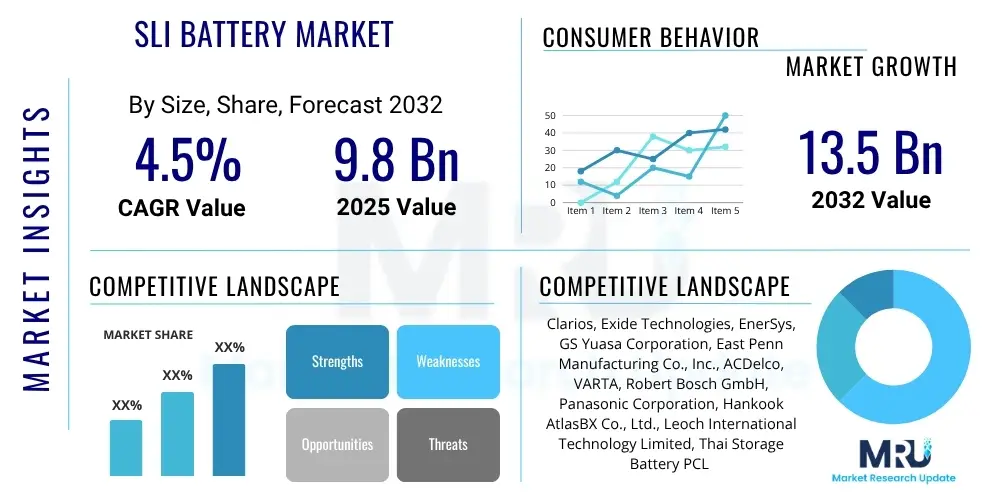

The SLI Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2032. The market is estimated at USD 9.8 billion in 2025 and is projected to reach USD 13.5 billion by the end of the forecast period in 2032.

SLI (Starting, Lighting, Ignition) batteries remain an indispensable component in the vast majority of internal combustion engine (ICE) vehicles globally, serving critical functions that enable vehicle operation. These specialized lead-acid batteries are engineered to deliver a powerful, short burst of current necessary to crank the engine, initiating the combustion process. Beyond starting, they are responsible for supplying consistent power to vehicle lights, various electronic accessories, and onboard computer systems when the engine is idle or operating at low revolutions per minute. Their design prioritizes high discharge rates and robust performance, ensuring reliability across diverse climatic and operational conditions, solidifying their status as a foundational element of modern automotive technology despite the ongoing shift towards electrification.

The primary applications for SLI batteries span a wide spectrum of vehicles, including passenger cars, light-duty and heavy-duty commercial trucks, motorcycles, and specialized off-road or marine vehicles. The inherent benefits of SLI batteries, such as their proven reliability track record, cost-effectiveness in manufacturing and purchase, and ubiquitous availability through extensive global distribution networks, contribute to their enduring market presence. Key driving factors propelling the SLI battery market include the consistent and robust growth in global vehicle production, particularly in emerging economies, alongside the continuously expanding global vehicle parc which creates a perennial demand for replacement batteries, given their finite operational lifespan. Moreover, advancements in lead-acid technology that enhance durability and performance also contribute to sustained demand.

The SLI battery market is currently experiencing a dynamic phase, characterized by a steady underlying demand coupled with significant technological evolution and shifting regional market emphasis. Dominant business trends underscore a concerted industry effort to enhance battery performance metrics, specifically focusing on extending operational lifespans, improving cold-cranking amperage (CCA) capabilities for reliable starting in harsh conditions, and optimizing charge acceptance rates. This focus is driven by increasingly demanding vehicle specifications, consumer expectations for greater reliability, and the growing complexity of onboard electronic systems in modern vehicles. Manufacturers are also prioritizing sustainable production practices and improved recyclability to address environmental concerns and regulatory pressures, aiming for a more environmentally conscious product lifecycle.

Regional trends reveal a bifurcated growth pattern: mature automotive markets in North America and Europe primarily rely on a robust aftermarket for replacement batteries and a gradual transition towards advanced lead-acid technologies like EFB and AGM to support sophisticated start-stop vehicle architectures. In stark contrast, the Asia Pacific region, particularly countries like China and India, exhibits vigorous growth fueled by soaring new vehicle production volumes and rapidly expanding vehicle ownership, creating substantial demand in both OEM and aftermarket segments. Segment trends highlight a resilient demand for conventional flooded lead-acid batteries, but also a discernible migration towards more advanced absorbed glass mat (AGM) and enhanced flooded battery (EFB) types, which are integral to modern fuel-efficient start-stop vehicles, indicating a technological upgrade within the lead-acid battery paradigm to meet evolving automotive requirements and environmental standards.

The intersection of Artificial Intelligence (AI) and the traditional SLI battery market, while not immediately obvious given the mature nature of lead-acid technology, is increasingly drawing attention from industry stakeholders and consumers alike. Common user questions frequently probe into how AI might revolutionize the relatively established manufacturing processes for SLI batteries, seeking improvements in efficiency, quality control, and predictive maintenance. There is also significant curiosity regarding AI's potential to enhance the lifespan and performance characteristics of these batteries, perhaps through advanced material science research guided by AI, or by optimizing charge-discharge cycles within vehicle battery management systems. Users are keen to understand if AI can inject "smart" capabilities into conventional power sources, extending their utility and relevance in an increasingly electrified automotive landscape, even as they acknowledge the primary role of AI in next-generation battery chemistries. This forward-looking perspective seeks to integrate AI not just into future EV batteries but also to refine and extend the capabilities of current, essential SLI technologies, addressing concerns about reliability, environmental impact, and overall cost-effectiveness.

The SLI battery market is fundamentally driven by several robust factors that ensure its continued relevance and growth. Foremost among these drivers is the unwavering demand from the global automotive sector, underpinned by consistent new vehicle production volumes, particularly in burgeoning economies across Asia Pacific and Latin America. The sheer size of the existing global vehicle parc, comprising billions of internal combustion engine vehicles, necessitates a perennial aftermarket for replacement SLI batteries, given their finite operational lifespan, typically ranging from three to five years depending on usage and climate. Furthermore, continuous technological advancements, such as the development of Enhanced Flooded Batteries (EFB) and Absorbed Glass Mat (AGM) technologies, which offer superior performance and durability for modern vehicles with start-stop systems and higher electrical loads, also contribute significantly to market expansion by meeting evolving automotive demands.

However, the market also faces considerable restraints, primarily the accelerating global shift towards electric vehicles (EVs) which utilize fundamentally different battery chemistries for propulsion, albeit still requiring a 12V auxiliary battery, often a sophisticated lead-acid type, for ancillary systems. This long-term transition poses a significant challenge to the conventional SLI market for ICE vehicles. The volatility and fluctuating prices of key raw materials, especially lead, represent another significant constraint, impacting production costs, profit margins, and ultimately consumer pricing. Additionally, increasing competition from alternative battery technologies, even within the 12V auxiliary segment for EVs, could pose future restraints.

Opportunities for growth are abundant, particularly in emerging markets where increasing disposable incomes and expanding middle classes are fueling higher rates of vehicle ownership, thereby stimulating both OEM and aftermarket demand. There is also a substantial opportunity in developing more sustainable and recyclable SLI battery solutions to meet evolving environmental standards and consumer preferences for eco-friendly products, potentially leading to advanced recycling programs and material recovery. The development of maintenance-free SLI batteries and those with extended warranties also presents avenues for market expansion by enhancing consumer convenience and confidence. The ongoing demand for heavier duty SLI batteries for commercial and agricultural vehicles also presents a consistent opportunity.

The impact forces shaping the SLI battery market are diverse and influential. Stringent environmental regulations, particularly regarding lead usage and battery recycling, compel manufacturers to invest in cleaner production processes and efficient closed-loop recycling programs. This regulatory pressure fosters innovation in material science and manufacturing practices geared towards sustainability. The intensely competitive landscape within the SLI battery industry continuously pushes companies to innovate in terms of product design, performance, lifespan, and cost-effectiveness to gain or maintain market share. Moreover, the evolving consumer demand for more reliable, maintenance-free, and higher-performance batteries for increasingly complex vehicle electrical systems also acts as a significant force, compelling manufacturers to adapt and refine their product offerings to cater to these sophisticated requirements.

The SLI battery market exhibits a complex and multifaceted segmentation, allowing for a granular understanding of its various components and underlying dynamics. This segmentation is crucial for market participants to identify lucrative niches, tailor product development, and refine marketing and distribution strategies effectively. The breakdown by different criteria offers insights into how technological advancements, consumer preferences, and automotive industry shifts influence demand across diverse product categories and end-use applications, providing a comprehensive framework for strategic decision-making and competitive positioning within the global market landscape. Each segment carries distinct characteristics, growth trajectories, and competitive intensities, necessitating a tailored approach to capture specific market value and address unique customer needs across different regions and vehicle types.

The value chain for the SLI battery market is a complex ecosystem, beginning with the extraction and processing of fundamental raw materials and culminating in the delivery of finished products to diverse end-users. The upstream segment of the value chain is critical, involving the procurement of primary components such as lead, which is typically sourced from mining operations or, increasingly, from recycled batteries, showcasing a growing emphasis on circular economy principles. Other essential materials include sulfuric acid for the electrolyte, plastics for battery casings (predominantly polypropylene), and various alloys (like calcium, tin, silver) and chemicals for plate grids and active materials. Reliable access to these raw materials at stable prices is paramount for manufacturers, making strong supplier relationships, efficient sourcing strategies, and effective hedging against price volatility key competitive differentiators for sustained production and profitability.

Following raw material procurement, the manufacturing and assembly phase constitutes the core of the value chain where value is significantly added. This stage involves sophisticated processes including lead smelting and refining, grid casting or stamping, precise plate pasting with active materials, specialized curing processes, cell assembly, inter-cell welding, and final battery enclosure with robust terminals and ventilation systems (for flooded types). Quality control and technological innovation are vital here, influencing battery performance, lifespan, safety, and cost-effectiveness. Manufacturers invest significantly in automation, precision engineering, and rigorous testing protocols to ensure consistent product quality, optimize production efficiency, and adhere to stringent industry standards and environmental regulations, striving for zero-defect output and enhanced product durability. Research and development in this stage also focus on improving energy density and cold-cranking capabilities.

The downstream segment focuses on distribution and sales, which bifurcate into two primary channels: direct sales to Original Equipment Manufacturers (OEMs) and indirect sales to the aftermarket. OEM sales involve long-term contracts with major automotive manufacturers for integration into new vehicles. These relationships demand high volumes, consistent quality, and just-in-time delivery. The aftermarket, which is often larger by volume and value, relies on an extensive network of independent distributors, wholesalers, auto parts retailers (both brick-and-mortar and online platforms), independent repair shops, and authorized service centers. This robust, multi-tiered distribution infrastructure is essential for ensuring wide product availability, convenient access for consumers requiring replacement batteries, and efficient logistics for battery collection and recycling, driven by the sheer scale of the global vehicle parc and the necessity for timely replacements.

The primary and most significant customer segment for SLI batteries comprises the global automotive industry, specifically the Original Equipment Manufacturers (OEMs). These manufacturers integrate SLI batteries as a standard component into every new internal combustion engine (ICE) vehicle produced, ranging from compact passenger cars and SUVs to heavy-duty commercial trucks and specialized agricultural vehicles. For OEMs, factors such as consistent supply volume, highly competitive pricing, strict compliance with specific vehicle electrical system requirements, and guaranteed long-term reliability and performance are paramount in their purchasing decisions, often leading to long-standing contractual relationships and collaborative product development with battery suppliers. The demand from this segment is directly correlated with global vehicle production volumes, making it a critical barometer for the SLI battery market's health and future trajectory.

Beyond the OEM segment, a vast and continuously growing customer base exists within the aftermarket. This includes millions of individual vehicle owners who require replacement SLI batteries as their existing ones reach the end of their operational life, typically every 3-5 years, influenced by driving conditions, climate, and maintenance. This segment is characterized by a high volume of transactions and a strong emphasis on brand reputation, product availability, ease of purchase, and warranty support. Fleet operators, managing diverse collections of vehicles for commercial, logistical, or governmental purposes, also represent a significant aftermarket customer group, often purchasing batteries in bulk and prioritizing extreme durability, consistent performance, and extended lifespans to minimize vehicle downtime and operational costs across their extensive vehicle rosters.

The distribution to these aftermarket customers is facilitated by a broad and intricate network of auto parts retailers, encompassing both large national and international chains as well as smaller independent stores, alongside rapidly growing online e-commerce platforms. Additionally, authorized dealership service centers and a multitude of independent automotive repair shops serve as crucial points of sale and installation for replacement SLI batteries. Furthermore, niche potential customers include operators of specialized vehicles such as agricultural machinery, construction equipment, marine vessels, and recreational vehicles (RVs). Although smaller in overall volume, these segments contribute to a steady demand for robust and often specialized SLI battery types specifically designed for their unique operational conditions, demanding performance requirements, and environmental exposures, underscoring the pervasive need for reliable starting and auxiliary power across various mobility and industrial applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 9.8 Billion |

| Market Forecast in 2032 | USD 13.5 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Clarios, Exide Technologies, EnerSys, GS Yuasa Corporation, East Penn Manufacturing Co., Inc., ACDelco, VARTA, Robert Bosch GmbH, Panasonic Corporation, Hankook AtlasBX Co., Ltd., Leoch International Technology Limited, Thai Storage Battery PCL (3K Batteries), Amara Raja Batteries Ltd., FIAMM Energy Technology S.p.A., Camel Group Co., Ltd., Sebang Global Battery Co., Ltd., Showa Denko Materials Co., Ltd. (formerly Hitachi Chemical), Banner Batteries, CSB Battery Co., Ltd., Trojan Battery Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The SLI battery market's technological landscape, while rooted in the mature lead-acid chemistry, is far from static, with continuous innovations focused on maximizing performance, extending lifespan, and enhancing reliability under increasingly demanding operational conditions. A significant area of development lies in the refinement of plate alloys. Manufacturers are consistently researching and adopting advanced lead alloys, such as calcium-calcium, lead-tin-calcium, and even silver alloys, which are designed to significantly reduce water loss (minimizing maintenance requirements), improve corrosion resistance for extended durability, and enhance conductivity for superior cold-cranking performance. These metallurgical advancements directly impact the battery's ability to withstand harsh temperatures and frequent charge-discharge cycles, thus improving overall longevity and ensuring reliable starts in diverse climates.

Another crucial technological frontier involves advancements in separator materials and construction within the battery cells. Traditional paper or plastic separators are being augmented or replaced by more advanced solutions, including specialized polyethylene envelopes that effectively prevent internal short circuits and reduce the shedding of active material from the plates, which is a common cause of battery failure. For more demanding applications, particularly in Enhanced Flooded Batteries (EFB) and Absorbed Glass Mat (AGM) batteries, glass mat technology (which absorbs the electrolyte, immobilizing it) plays a pivotal role. These innovations contribute significantly to the battery's ability to resist vibration, prevent stratification of the electrolyte (a common issue in flooded batteries), and maintain performance during partial state-of-charge operation, which is critical for vehicles equipped with sophisticated start-stop systems that frequently cycle the battery.

Furthermore, the continuous drive for improved manufacturing processes and design optimizations remains a cornerstone of technological progress across the SLI battery industry. This includes innovations in grid design, such as radial grids or expanded metal grids, which enhance current flow, increase power density, and improve overall electrical efficiency. Advancements in active material formulations, including the precise use of specific carbon additives to the lead paste, are also being explored to significantly improve charge acceptance and deep-cycling capabilities, particularly relevant for EFB and AGM technologies which endure more rigorous operational cycles. These collective technological refinements aim to deliver SLI batteries that are not only more powerful, durable, and reliable but also more environmentally friendly through optimized material usage and improved recyclability, ensuring their continued relevance and competitive edge in the evolving automotive ecosystem.

An SLI (Starting, Lighting, Ignition) battery is a crucial lead-acid battery designed for internal combustion engine (ICE) vehicles. Its primary function is to deliver a massive surge of electrical current for a short duration to crank the engine and initiate combustion. Additionally, it provides stable power for the vehicle's electrical systems, including lights, radio, dashboard, and various accessories, when the engine is off or idling, ensuring constant electrical supply and optimal vehicle operation. It is indispensable for the reliable functioning of a conventional vehicle's electrical system and engine start-up sequence.

The market primarily offers three distinct types: traditional Flooded Lead-Acid batteries, which are cost-effective, require occasional maintenance, and are common in older vehicles or basic new models; Enhanced Flooded Batteries (EFB), designed with improved cycle life and charge acceptance for entry-level start-stop vehicles; and Absorbed Glass Mat (AGM) batteries, a premium solution offering superior deep cycling, vibration resistance, and cold-cranking performance, ideal for advanced start-stop systems, luxury vehicles, and those with high electrical demands. Each type caters to specific performance, maintenance, and budget requirements within the automotive sector.

Several critical factors impact an SLI battery's lifespan and performance, including driving habits (frequent short trips prevent full charging, leading to sulfation), ambient temperature (extreme heat and cold accelerate degradation), battery type and quality (AGM generally lasts longer than flooded), maintenance practices (regular cleaning of terminals, checking connections), and the overall health of the vehicle's electrical system (e.g., faulty alternator can overcharge or undercharge). Overcharging, deep discharging, and excessive vibration can also severely reduce its longevity, making proper vehicle maintenance and appropriate battery selection essential for extending battery life and ensuring reliable operation.

While propulsion in EVs relies on high-voltage traction batteries, SLI battery manufacturers are adapting by focusing on specialized 12V auxiliary batteries for EVs, which power essential low-voltage systems like lights, infotainment, and safety features. Furthermore, the robust aftermarket demand for SLI batteries in the vast existing fleet of internal combustion engine vehicles ensures continued relevance for the foreseeable future. Innovation in advanced lead-acid technologies like AGM, offering improved cycle life, faster recharge, and reliability, also helps manufacturers address the evolving needs of hybrid and sophisticated start-stop ICE vehicles, ensuring the technology remains a critical part of the automotive ecosystem, even in its transition.

Key drivers include consistent global new vehicle production, particularly in emerging markets, and the vast existing vehicle parc creating strong aftermarket replacement demand due to the finite lifespan of batteries. Technological advancements in lead-acid chemistry, enhancing performance and durability for modern vehicles, also contribute to market growth. Major restraints include the long-term industry shift towards electric vehicles, which reduces future demand for conventional SLI batteries in propulsion applications, and the volatility in raw material prices, particularly lead, which can impact production costs and market stability. Environmental regulations also significantly influence market dynamics, pushing for more sustainable production and recycling practices, shaping technological development.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.