ID : MRU_ 429431 | Date : Nov, 2025 | Pages : 251 | Region : Global | Publisher : MRU

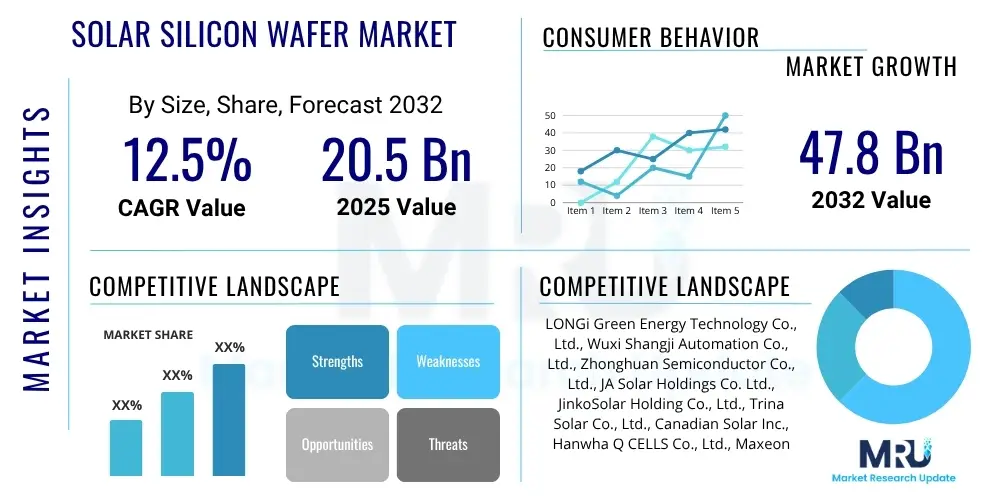

The Solar Silicon Wafer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2032. The market is estimated at $20.5 Billion in 2025 and is projected to reach $47.8 Billion by the end of the forecast period in 2032.

The Solar Silicon Wafer Market stands as the fundamental cornerstone of the burgeoning global solar photovoltaic (PV) industry, representing the essential semiconductor substrate from which all crystalline silicon solar cells are meticulously fabricated. These wafers, which are predominantly derived from ultra-high purity silicon, act as the critical interface responsible for capturing incident sunlight and efficiently converting it into usable electrical energy. The accelerating global imperative to transition towards sustainable and renewable energy sources, coupled with widespread societal recognition of the urgent need to mitigate climate change by moving away from fossil fuels, has profoundly stimulated the demand for solar power, thereby directly and substantially propelling the expansion of the solar silicon wafer market into a central industrial powerhouse. As nations worldwide commit to increasingly ambitious renewable energy targets and regulatory frameworks become more stringent, the role of high-quality, high-efficiency, and cost-effective silicon wafers becomes not merely important, but absolutely paramount to achieving these global energy transition objectives.

The primary product categories within this highly specialized market encompass both monocrystalline and polycrystalline silicon wafers, each distinguished by unique crystal structures, manufacturing processes, and corresponding performance characteristics in terms of efficiency, cost, and aesthetic appeal. Monocrystalline wafers, grown from a single crystal, generally offer higher efficiency and a uniform dark appearance, while polycrystalline wafers, composed of multiple crystal grains, have traditionally been more cost-effective, albeit with slightly lower efficiency. The major applications for these critical wafers are incredibly diverse, spanning the entire spectrum of solar energy deployment, from small-scale residential rooftop installations designed to power individual homes and businesses, to large-scale commercial solar projects powering industrial facilities and corporate campuses, and finally, to expansive, utility-scale solar farms that contribute significantly to national electricity grids. This broad and continuously expanding application landscape underscores the versatility and indispensability of silicon wafers in the clean energy ecosystem.

The robust growth of this market is predominantly underpinned by a powerful synergy of driving factors. These include highly supportive government policies, incentives, and renewable energy mandates implemented across numerous countries, which actively encourage the widespread adoption of solar power through subsidies, tax credits, and favorable regulatory environments. Furthermore, the pervasive and intensifying global awareness concerning climate change and environmental degradation serves as a significant moral and economic impetus, driving public and private investment into clean energy technologies. Relentless technological advancements, particularly in areas such as crystal growth, wafer slicing, and cell passivation techniques, continuously aim to enhance wafer efficiency, reduce material waste, and significantly lower overall production costs, thereby making solar energy increasingly competitive. The ever-present imperative for national energy independence and bolstered energy security in many nations further contributes substantially to the sustained and vigorous expansion of the solar photovoltaic sector, underpinning the robust and continually growing demand for solar silicon wafers as the core component of this transformative technology. This dynamic interplay of policy support, technological innovation, environmental stewardship, and geopolitical considerations ensures a resilient, expanding, and strategically vital market outlook for solar silicon wafers.

The Solar Silicon Wafer Market is currently experiencing a period of exceptionally dynamic and robust growth, primarily propelled by the escalating global impetus for renewable energy adoption and a continuous stream of significant technological advancements within the photovoltaic sector. Current business trends clearly indicate a pronounced strategic shift towards vertical integration among prominent industry players, where companies are increasingly consolidating various stages of the supply chain, ranging from upstream polysilicon production and intermediate wafer manufacturing, all the way down to downstream solar cell and module assembly. This comprehensive integration strategy is aimed at achieving multiple critical objectives: enhancing operational efficiency, substantially reducing overall production costs, ensuring greater control over quality, and crucially, securing resilient supply chains in an increasingly volatile global market. Furthermore, there is an unmistakable and accelerating industry-wide focus on the development and widespread adoption of larger wafer sizes and innovative N-type technologies. These advancements are specifically designed to yield higher efficiency rates and superior power output per module, profoundly influencing the strategic investment decisions and long-term technological roadforces across the entire industry. Intense competitive pressures within the market are also acting as a powerful catalyst, fostering rapid innovation, particularly in sophisticated manufacturing techniques such as advanced diamond wire slicing and optimized ingot pulling methods, both meticulously aimed at minimizing material waste and significantly improving manufacturing throughput.

From a regional perspective, the Asia Pacific region unequivocally stands as the undisputed epicenter of the global solar silicon wafer market. China, in particular, continues to lead with unparalleled production capacity, driving a substantial portion of technological innovation, and possessing a colossal domestic demand for solar energy. Other nations within the region, including India, Vietnam, and South Korea, are rapidly solidifying their positions as significant manufacturing hubs and crucial consumption centers. This regional dominance is powerfully underpinned by aggressive national solar energy targets, highly favorable investment policies, and extensive governmental support for the renewable energy sector. Concurrently, North America and Europe are witnessing substantial and sustained market growth, largely driven by increasingly stringent regulatory support, ambitious national decarbonization goals, and a renewed strategic focus on establishing more localized and resilient supply chains. The aim is to reduce historical reliance on foreign imports and foster regional energy independence. Furthermore, the Middle East, Africa, and Latin America are collectively demonstrating promising potential for market expansion, albeit from a relatively lower current base. This growth is spurred by an increasing number of renewable energy projects being initiated to address rapidly escalating energy demands and to fulfill national commitments to reduce carbon footprints.

Analysis of segment trends reveals a definitive and pronounced market shift towards monocrystalline silicon wafers. These wafers currently hold a dominant market share due to their inherently superior energy conversion efficiency and progressively improving cost-effectiveness, effectively displacing older polycrystalline wafers in the majority of new solar installations. Within the monocrystalline segment, there is a clear and accelerating trend towards the adoption of larger wafer sizes. Formats such as 182mm (M10) and 210mm (G12) are rapidly gaining significant market share. This preference for larger sizes is driven by their proven ability to significantly reduce balance-of-system costs and substantially increase the overall power output of individual solar modules. The residential and utility-scale segments remain the largest and most dynamic consumers of solar silicon wafers, with the commercial sector also demonstrating consistent and steady growth. Advanced cell technologies, including Passivated Emitter Rear Contact (PERC), Tunnel Oxide Passivated Contact (TOPCon), and Heterojunction Technology (HJT), which all inherently leverage high-purity and advanced silicon wafers, are fast becoming the new industry standard. These technological advancements are dictating the direction of future investment in manufacturing capabilities and are shaping the competitive landscape for years to come. This complex and highly dynamic evolution across business, regional, and segment landscapes collectively underscores a vibrant market that is not only poised for continuous innovation but also for sustained and significant expansion.

User inquiries regarding the profound influence of Artificial Intelligence (AI) on the Solar Silicon Wafer Market consistently gravitate towards understanding how AI can be leveraged to dramatically enhance manufacturing precision, optimize the utilization of precious raw materials, and ultimately improve overall operational efficiencies throughout the entire production lifecycle. Common questions frequently explore AI's multifaceted role in sophisticated defect detection mechanisms during the critical wafer production stages, its versatile application in predictive maintenance regimes for complex and capital-intensive manufacturing machinery, and its immense potential to significantly accelerate the research and development pipeline for next-generation wafer technologies through the application of advanced computational simulations and cutting-edge material science research. There is also substantial and growing interest in AI's inherent capacity to streamline highly complex supply chain logistics, ranging from raw material sourcing to finished product delivery, and its ability to provide far more accurate and dynamic demand forecasting, thereby proactively reducing waste, minimizing inventory holding costs, and crucially, improving the overall responsiveness to rapid market fluctuations. Users are particularly keenly interested in quantifiable ways that AI can directly contribute to both significant cost reduction and substantial quality improvement, which are universally recognized as absolutely critical factors for the sustained growth, enhanced competitiveness, and long-term profitability of the global solar industry.

The prevailing and overarching themes consistently emerging from these diverse user queries unequivocally emphasize AI's truly transformative potential across every single stage of the solar silicon wafer value chain. Stakeholders, including manufacturers, researchers, and investors, anticipate that the strategic deployment of AI will lead to groundbreaking advancements in sophisticated process control. This will specifically enable manufacturers to maintain extremely tight tolerances during the highly sensitive ingot growth and delicate wafer slicing processes. Such precision is absolutely crucial for maximizing the yield of high-quality wafers and subsequently enhancing overall cell efficiency. There is a strong and pervasive expectation that AI will significantly bolster and revolutionize quality assurance protocols, moving far beyond traditional, often manual, inspection methods to embrace intelligent, real-time defect identification, classification, and even autonomous correction mechanisms. This advanced capability promises to minimize costly yield losses and ensure consistently superior product quality. Furthermore, the strategic and intelligent application of AI in research and development is widely perceived as a powerful catalyst for accelerating the discovery of novel silicon purification methods, pioneering new materials with enhanced properties, and optimizing existing wafer designs and geometries. This push is aimed at continuously pushing the very boundaries of solar cell performance and energy conversion efficiency. The overarching and shared expectation throughout the industry is that AI will serve as a pivotal key enabler, driving greater automation, achieving unprecedented levels of efficiency, and ultimately fostering superior cost-effectiveness in the intricate and demanding production of solar silicon wafers, thereby making solar energy even more accessible, more competitive, and more widely adopted on a global scale.

The Solar Silicon Wafer Market is intricately shaped by a multifaceted interplay of compelling Drivers, significant Restraints, strategic Opportunities, and a variety of external Impact Forces that collectively define its current growth trajectory, influence its competitive landscape, and determine its future potential. Key drivers that are powerfully propelling the market forward include the accelerating and undeniable global demand for renewable energy sources, driven by growing environmental consciousness and the urgent need for decarbonization. This is further amplified by stringent government policies and attractive financial incentives, such as tax credits, subsidies, and favorable feed-in tariffs, which actively promote the widespread adoption of solar power across residential, commercial, and utility-scale sectors. Furthermore, continuous and rapid advancements in photovoltaic technology, encompassing improvements in wafer efficiency, cell design, and module manufacturing, consistently lead to the production of more efficient and increasingly cost-effective solar cells. The steadily decreasing levelized cost of solar energy solutions, largely attributable to these relentless innovations in wafer production and overall panel manufacturing, makes solar power an increasingly economically viable and attractive energy source worldwide, directly fueling a substantial expansion in installed capacity. Heightened environmental concerns regarding climate change and air pollution, coupled with the imperative for national energy independence and bolstered energy security in many nations, further drive significant national and international investments into solar projects, directly boosting the demand for silicon wafers as the core foundational component of this clean energy revolution.

However, despite these strong growth drivers, the market also contends with several notable restraints that possess the potential to temper or impede its overall expansion. One significant challenge is the inherent volatility in the prices of critical raw materials, most notably polysilicon. Fluctuations in polysilicon prices directly impact the production costs and consequently affect the profit margins for wafer manufacturers, introducing an element of financial uncertainty. The establishment and expansion of state-of-the-art silicon wafer manufacturing facilities necessitate exceptionally high initial capital investment, posing a substantial barrier to entry for nascent players and often representing a significant financial strain for existing companies seeking to upgrade or expand their current production capacities. Additionally, the complex and ever-evolving landscape of geopolitical tensions and the implementation of various trade barriers, such as import tariffs and duties on solar components, can severely disrupt global supply chains, increase manufacturing costs, and ultimately raise consumer prices. The intrinsically energy-intensive nature of silicon wafer production, particularly during the polysilicon refinement and ingot growth stages, presents another operational and environmental challenge, as manufacturers are under increasing pressure to reduce their carbon footprint while simultaneously managing potentially high energy expenses.

Notwithstanding these formidable restraints, the market is replete with substantial opportunities for both significant expansion and groundbreaking innovation. Emerging markets across Southeast Asia, Latin America, and Africa present vast and largely untapped potential for large-scale solar energy deployment. This is driven by rapidly growing energy demands due to economic development, increasing efforts for electrification in underserved areas, and often abundant solar irradiance. The ongoing and accelerated development of advanced wafer technologies, specifically the widespread adoption of N-type wafers (such as TOPCon and HJT) and the move towards larger wafer sizes (e.g., 182mm and 210mm), promise superior efficiencies and considerably lower balance-of-system costs. These advancements open up exciting new avenues for product differentiation, enhanced performance, and sustained market leadership. Furthermore, the strategic integration of solar PV systems with advanced energy storage solutions and smart grid technologies offers a powerful synergistic opportunity, which significantly enhances the reliability, dispatchability, and overall attractiveness of solar power as a primary energy source. The astute identification and strategic pursuit of these promising opportunities, coupled with a proactive and effective mitigation of the identified restraints, are absolutely crucial for securing sustained market growth and achieving a formidable competitive advantage in the rapidly evolving solar industry.

The market's trajectory and operational environment are further profoundly shaped by several critical and overarching impact forces. Government regulations and policy frameworks, including national renewable energy targets, permitting processes, and grid connection regulations, play an unequivocally pivotal role, as favorable subsidies, tax credits, and stringent renewable energy mandates directly stimulate market demand and investment. Conversely, sudden or unpredictable shifts in policy or the premature withdrawal of essential incentives can introduce significant market uncertainty and dampen investor confidence. Rapid technological breakthroughs, particularly in areas such as advanced crystal growth techniques, innovative slicing methods (like diamond wire sawing), and cutting-edge surface passivation technologies, directly influence wafer performance, reduce production costs, and enhance overall cost-effectiveness, driving competitive dynamics. Broader macroeconomic conditions, encompassing factors such as global economic growth rates, prevailing interest rates, inflation trends, and currency fluctuations, significantly affect the levels of investment in new solar projects and the financial viability of existing ones. Finally, escalating environmental considerations, including increasingly stringent carbon emission reduction targets, evolving waste management regulations, and the growing adoption of circular economy principles, exert considerable pressure on manufacturers to adopt more sustainable production methods, develop environmentally friendly materials, and implement robust recycling programs throughout the entire life cycle of solar silicon wafers, thereby impacting the entire industry ecosystem.

The Solar Silicon Wafer Market is meticulously segmented to provide a granular and comprehensive understanding of its diverse components, intricate dynamics, and specific areas of growth. This detailed breakdown reflects the various product types, technological specifications, and end-use applications that collectively define the industry landscape. The segmentation framework is essential for conducting an in-depth analysis of market trends, accurately assessing competitive positioning, and effectively identifying both present and future growth opportunities across numerous distinct categories. A primary and fundamental categorization typically revolves around the type of silicon crystal structure, which inherently dictates the wafer’s intrinsic performance characteristics, its visual appearance, and its specific manufacturing process. Further critical differentiation occurs based on the physical dimensions of the wafers, an aspect that is in a state of continuous evolution, with the industry consistently trending towards larger formats designed to significantly enhance efficiency, reduce module assembly costs, and improve overall power output per module.

Another critically important dimension for comprehensive market analysis is the specific end-use application for which these meticulously engineered wafers are destined. Solar silicon wafers, as the core and indispensable component, serve as the foundational material for photovoltaic cells, which are subsequently integrated into a wide array of solar energy systems. These applications span a broad spectrum of scale and purpose, ranging from relatively small-scale residential installations, typically mounted on rooftops and primarily designed for individual home energy consumption or self-sufficiency, to expansive commercial projects that provide sustainable power to businesses, offices, and large-scale industrial facilities. At the pinnacle of scale are the massive utility-scale solar farms, which cover vast areas and contribute substantial amounts of clean electricity directly into national grids, playing a pivotal role in the energy transition. Each of these distinct end-use segments possesses its own unique demand drivers, exhibits particular purchasing behaviors, and often necessitates specific technological requirements, all of which directly influence the preferred type and exact specifications of the wafers being procured by manufacturers in that particular segment.

Understanding these detailed segmentations is absolutely crucial for all key stakeholders within the solar industry, including wafer manufacturers, solar cell and module producers, investors, governmental agencies, and policymakers. This granular understanding enables them to accurately identify specific high-growth areas, strategically allocate precious resources with optimal efficiency, and formulate highly targeted marketing, production, and investment strategies. The intricate segmentation of the market clearly highlights the relentless pace of continuous innovation in wafer technology and advanced manufacturing processes, occurring in parallel with the rapidly expanding global adoption of solar energy solutions across a multitude of economic sectors and geographical regions. This comprehensive and detailed breakdown provides a clear, actionable roadmap for navigating the inherent complexities of the solar silicon wafer market, thereby enabling informed decision-making, fostering sustainable technological development, and accelerating the global transition within the broader renewable energy ecosystem.

The value chain for the Solar Silicon Wafer Market represents a meticulously structured, multi-stage industrial process that commences with the fundamental extraction and rigorous purification of raw silicon and extends through a series of increasingly complex manufacturing steps, culminating in the final integration of these wafers into high-performance solar photovoltaic modules. The upstream segment of this extensive value chain is predominantly characterized by the labor-intensive production of metallurgical-grade silicon, which serves as the initial raw material. This is subsequently followed by its intensive chemical purification into hyperpure polysilicon, a critical and foundational material that is absolutely essential for the fabrication of solar wafers. This initial phase, involving high-purity polysilicon production, is inherently energy-intensive and requires substantial technological expertise, significant capital investment in specialized infrastructure, and robust chemical processing capabilities, thereby setting the initial quality benchmarks and influencing the cost structure for the entire subsequent value chain. Key activities within this upstream segment include the mining and sourcing of quartz, its carbothermic reduction to metallurgical silicon, further chemical refining to achieve solar-grade purity (often via the Siemens process or FBR), and then the subsequent conversion of this polysilicon into large monocrystalline or polycrystalline ingots, typically achieved through highly controlled methods such as the Czochralski (CZ) method for single crystals or directional solidification for multicrystalline blocks.

The primary potential customers and ultimate end-users within the intricate ecosystem of the Solar Silicon Wafer Market are a diverse group of entities fundamentally engaged in the manufacturing, assembly, and large-scale deployment of solar photovoltaic technologies. At the very forefront of this customer base are Solar Cell Manufacturers, who unequivocally represent the largest, most direct, and most critical consumers of solar silicon wafers. These specialized companies acquire vast quantities of precisely engineered wafers, which they then meticulously process through various stages—including doping, metallization, and passivation—to transform them into high-performance photovoltaic cells, which are the fundamental and active units responsible for converting captured sunlight into usable electricity. Their purchasing decisions are profoundly influenced by a complex array of factors including, but not limited to, wafer efficiency ratings, the crucial cost per watt metric, specific physical dimensions (such as wafer size and thickness), surface quality, and, critically, the reliability and consistency of the supply chain. These factors directly and significantly impact their own cell manufacturing yields, the overall performance of their final products, and their competitiveness in a fiercely contested global market. The highly stringent technical requirements, coupled with the necessity for extremely high-volume procurement, mean that direct, collaborative relationships and often multi-year, long-term supply agreements between wafer manufacturers and solar cell producers are not just common, but a fundamental aspect of industry operations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $20.5 Billion |

| Market Forecast in 2032 | $47.8 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | LONGi Green Energy Technology Co., Ltd., Wuxi Shangji Automation Co., Ltd., Zhonghuan Semiconductor Co., Ltd., JA Solar Holdings Co. Ltd., JinkoSolar Holding Co., Ltd., Trina Solar Co., Ltd., Canadian Solar Inc., Hanwha Q CELLS Co., Ltd., Maxeon Solar Technologies, REC Solar Holdings AS, Shin-Etsu Chemical Co., Ltd., Hemlock Semiconductor Operations LLC, Tokuyama Corporation, Daqo New Energy Corp., GCL Technology Holdings Limited, Shunfeng International Clean Energy Limited, Risen Energy Co., Ltd., Aiko Solar Energy Co., Ltd., Meyer Burger Technology AG, Silicor Materials |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Solar Silicon Wafer Market is fundamentally defined and continuously reshaped by an exceptionally dynamic and rapidly evolving technological landscape, which is relentlessly driven by the industry's singular pursuit of achieving ever-higher efficiency rates, substantially lower production costs, and significantly enhanced product durability. At the very core of advanced wafer manufacturing lie sophisticated ingot growth technologies. The Czochralski (CZ) method remains the predominant technique for producing monocrystalline silicon ingots, renowned for its ability to yield high-purity ingots with an exceptionally uniform crystal structure, which is critical for maximizing solar cell performance. The Float Zone (FZ) method is also employed for producing ultra-high purity silicon, primarily for specialized applications, though it is less common for standard solar wafers due to its higher production costs. Ongoing advancements in these intricate crystal growth techniques are rigorously focused on improving intrinsic crystal quality, increasing the physical size and weight of the ingots to achieve economies of scale, and significantly reducing the substantial energy consumption during the lengthy and highly controlled growth process. These improvements directly translate into superior wafer performance, reduced material waste, and a more favorable overall cost-effectiveness for the final product.

A solar silicon wafer is a meticulously engineered, ultra-thin slice of semiconductor material, predominantly composed of highly purified silicon, which serves as the indispensable foundational substrate for the subsequent fabrication of photovoltaic solar cells. Its fundamental purpose is to effectively absorb incident sunlight and efficiently convert that solar radiation directly into electrical energy, making it the absolute core and active component of all modern solar panels.

The manufacturing of solar silicon wafers is a complex, multi-stage industrial process that commences with the rigorous purification of metallurgical-grade silicon into hyperpure polysilicon. This polysilicon is then meticulously grown into large, cylindrical monocrystalline ingots or block-shaped polycrystalline ingots. Subsequently, these ingots are precisely sliced into extremely thin wafers using advanced diamond wire cutting technology, followed by critical steps such as cleaning, surface texturization, and often chemical doping to optimize their optical and electrical properties for peak performance in solar cells.

The primary types of solar silicon wafers are monocrystalline and polycrystalline. Monocrystalline wafers are derived from a single crystal, offering superior efficiency, a uniform dark appearance, and excellent performance, especially in hot conditions. Polycrystalline wafers, made from multiple crystal grains, have been traditionally more cost-effective but typically exhibit slightly lower average efficiencies. A significant modern trend involves advanced N-type wafers (e.g., TOPCon, HJT), which are now gaining prominence for their even higher efficiencies and reduced degradation.

The significant growth of the solar silicon wafer market is primarily driven by the accelerating global demand for clean, renewable energy, robust government policies and attractive financial incentives supporting solar power adoption, continuous and rapid technological advancements leading to enhanced efficiency and reduced costs in photovoltaic manufacturing, escalating environmental concerns surrounding climate change, and the strategic pursuit of national energy independence and security initiatives worldwide.

Key emerging trends and technological advancements include the widespread adoption of larger wafer sizes (such as 182mm M10 and 210mm G12) to significantly boost module power output and lower system-level costs. There's also a rapid shift towards N-type wafer technology for superior cell efficiency and reduced degradation, a focus on ultra-thin wafer designs to minimize silicon consumption, and increasing integration of advanced automation and Artificial Intelligence (AI) in manufacturing processes to enhance precision, yield, and overall cost-effectiveness.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.