ID : MRU_ 428525 | Date : Oct, 2025 | Pages : 248 | Region : Global | Publisher : MRU

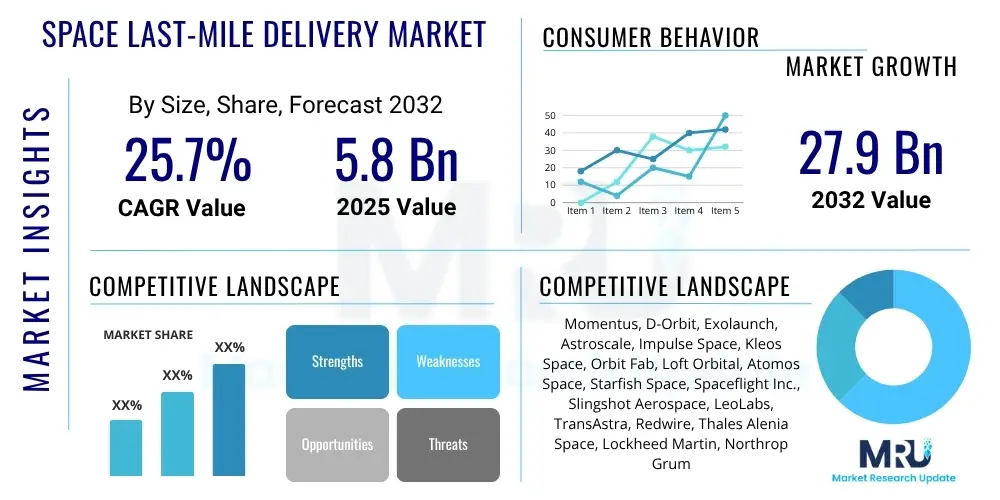

The Space Last-Mile Delivery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.7% between 2025 and 2032. The market is estimated at USD 5.8 billion in 2025 and is projected to reach USD 27.9 billion by the end of the forecast period in 2032.

The Space Last-Mile Delivery Market encompasses the specialized services and technologies designed to transport payloads from a primary launch vehicle's orbit to their precise final orbital destination or beyond. This critical segment addresses the challenge of positioning satellites, instruments, and other space assets with high accuracy and flexibility, often serving missions that require specific orbital altitudes, inclinations, or rendezvous capabilities. It is a vital enabler for the burgeoning new space economy, supporting a diverse range of applications from large constellation deployments to complex in-orbit servicing operations.

Products in this market primarily include Orbital Transfer Vehicles (OTVs) or space tugs, satellite dispensers, and propulsion modules tailored for in-space maneuvers. These solutions offer significant benefits, such as reducing the complexity and cost of primary launch services by allowing multiple payloads to share a single launch and then dispersing them independently. They enhance mission flexibility, extend satellite lifespans through refueling or repositioning, and enable entirely new classes of missions like active debris removal and lunar logistics. The market is propelled by several key driving factors, including the rapid proliferation of small satellite constellations, the increasing demand for in-orbit services, and substantial private and public investment in advanced space infrastructure.

Major applications of space last-mile delivery services span telecommunications, Earth observation, scientific research, defense, and emerging sectors like in-space manufacturing and lunar exploration. By providing precise orbital insertion and maneuverability, these services democratize access to space for a wider array of users and mission profiles. The underlying technology advancements in propulsion, autonomy, and modular spacecraft design are continuously expanding the capabilities and accessibility of these vital space logistics solutions, making last-mile delivery an indispensable component of future space operations.

The Space Last-Mile Delivery Market is experiencing robust growth, primarily fueled by the accelerating deployment of satellite constellations in Low Earth Orbit (LEO) and the increasing sophistication of in-orbit services. Business trends indicate a shift towards greater private sector involvement, with startups and established aerospace firms developing innovative solutions like reusable orbital transfer vehicles and standardized docking interfaces. This influx of private capital is driving competition and accelerating technological advancements, pushing towards more cost-effective and flexible delivery options. Strategic partnerships between launch providers and last-mile delivery specialists are also becoming common, aiming to offer end-to-end space logistics solutions.

Regionally, North America continues to dominate the market, propelled by significant investment from the U.S. government (NASA, Space Force) and a vibrant ecosystem of private space companies. Europe is also a key player, with the European Space Agency (ESA) and various national initiatives fostering innovation in sustainable space logistics and debris mitigation. The Asia Pacific region is rapidly emerging as a significant growth hub, driven by ambitious national space programs in China, India, and Japan, coupled with a growing demand for satellite-based services across the continent. Latin America and the Middle East and Africa, while smaller, are showing nascent interest and investment, particularly in satellite communication and Earth observation capabilities.

Segmentation trends reveal that Orbital Transfer Vehicles (OTVs) are the leading service type, offering unparalleled flexibility for diverse mission requirements. Small satellites represent the primary payload segment, reflecting the current boom in smallsat constellation deployments, though demand for medium to heavy payload delivery for larger, more complex missions is also increasing. The commercial end-use segment is poised for the highest growth, driven by private telecommunications, Earth observation, and IoT companies. Looking ahead, the market is set to benefit from continued technological innovation, a strong push for greater mission autonomy, and an expanding addressable market as space activities become more diverse and accessible.

User inquiries regarding AI's impact on Space Last-Mile Delivery frequently revolve around themes of automation, operational efficiency, enhanced safety, and the optimization of complex orbital maneuvers. Common questions include how AI can reduce mission costs, improve precision, manage growing space traffic, and enable autonomous operations. There is also significant interest in AI's role in addressing challenges like space debris and extending the lifespan of in-orbit assets. Users expect AI to revolutionize the decision-making process, minimize human intervention, and offer predictive capabilities that mitigate risks associated with intricate space logistics, while also expressing concerns about the reliability and security of AI systems in critical space applications.

The Space Last-Mile Delivery Market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities that shape its growth trajectory and operational landscape. Key drivers include the exponential increase in small satellite constellation deployments, particularly for broadband internet and Earth observation, which necessitates precise and flexible orbital insertion services. Concurrently, the burgeoning demand for in-orbit servicing, refueling, and manufacturing capabilities is creating a robust market for advanced maneuvering vehicles. Furthermore, the decreasing costs of primary launch services have made space more accessible, spurring innovation in last-mile solutions. Government investments in national space programs and defense initiatives also play a crucial role, providing foundational support and driving technological advancements.

Despite these growth factors, the market faces several formidable restraints. The extremely high capital investment required for developing and launching sophisticated space infrastructure, coupled with the substantial operational costs, presents a significant barrier to entry and expansion. Stringent regulatory frameworks and complex international licensing requirements add layers of complexity and can slow down innovation and market entry. Moreover, the inherent risks associated with space debris and the ever-present threat of orbital collisions demand rigorous safety protocols and advanced avoidance technologies, which contribute to mission complexity and cost. Technical complexities, particularly in achieving precise autonomous rendezvous and docking, along with reliability concerns for long-duration missions in harsh space environments, also pose significant challenges.

However, substantial opportunities exist for market players to innovate and expand. The emergence of lunar logistics and deeper space missions, including aspirations for asteroid mining and Mars exploration, represents a new frontier for last-mile delivery services. Continued development of reusable in-space vehicles promises to dramatically reduce costs and increase mission flexibility. International collaborations and standardization efforts in areas like docking interfaces and communication protocols can foster a more integrated and efficient global space economy. Additionally, the potential expansion into commercial space tourism, in-space manufacturing, and resource extraction offers new, high-value applications. The continuous integration of AI and advanced automation stands as a transformative impact force, enabling more sophisticated, efficient, and autonomous operations across the entire last-mile delivery value chain, ultimately driving the market towards greater operational autonomy and commercial viability.

The Space Last-Mile Delivery Market is intricately segmented based on various operational and technological characteristics, allowing for a detailed analysis of its diverse components and growth avenues. Understanding these segments is crucial for identifying key market trends, competitive landscapes, and strategic investment areas within the evolving space logistics sector.

The value chain for the Space Last-Mile Delivery Market is complex, beginning with upstream activities related to the foundational components and launch infrastructure. Upstream elements involve the manufacturing of advanced propulsion systems, avionics, guidance, navigation, and control (GNC) sensors, and structural components that constitute the orbital transfer vehicles and satellite dispensers. Key players in this stage include specialized aerospace component suppliers, traditional aerospace contractors, and innovative startups focused on novel propulsion technologies. Additionally, primary launch service providers, such as SpaceX, ULA, Arianespace, and Rocket Lab, represent a critical upstream dependency, as they deliver the payloads into initial orbits from which last-mile operations commence. This segment is characterized by high research and development costs and a need for extreme precision and reliability in manufacturing.

The midstream of the value chain focuses on the integration and operation of the last-mile delivery vehicles themselves. This involves the design, assembly, and testing of space tugs, deployers, and servicing spacecraft, followed by mission planning, ground control operations, and the execution of orbital maneuvers. Companies specializing in orbital logistics and in-space transportation are central here, acting as the primary service providers for customers. Their role often includes managing the complex logistics of getting payloads from a ride-share launch to their precise final orbital slot, performing in-orbit servicing, or initiating de-orbiting procedures. This segment requires advanced autonomous capabilities, sophisticated software, and highly skilled engineering teams to ensure mission success and safety.

Downstream activities involve the direct end-users and the ultimate beneficiaries of last-mile delivery services. This includes satellite operators who rely on these services to position their constellations for optimal performance in telecommunications, Earth observation, and IoT applications. Government and defense agencies are significant downstream customers, leveraging last-mile delivery for secure communications, surveillance, and scientific missions. Scientific research institutions also utilize these services for deploying experimental payloads and probes. Distribution channels are typically direct, involving direct contracts between last-mile delivery providers and their end-user clients. Indirect channels may involve partnerships with primary launch service providers who offer last-mile services as part of a bundled solution, or with satellite manufacturers who integrate last-mile capabilities into their offerings. The efficiency and reliability of the last-mile directly impact the operational success and revenue generation of these downstream entities, making it a critical link in the overall space economy.

The Space Last-Mile Delivery Market caters to a diverse range of sophisticated customers requiring precise and flexible orbital placement of their assets. The primary segment of end-users consists of commercial satellite operators, particularly those developing and deploying large constellations for broadband internet (e.g., Starlink, OneWeb), Earth observation (e.g., Planet Labs, Maxar Technologies), and Internet of Things (IoT) connectivity. These operators benefit immensely from last-mile services as they allow for shared launch costs and tailored orbital insertion, optimizing their constellation deployment schedules and operational efficiency. The flexibility offered by space tugs enables them to quickly adapt to changing mission requirements or expand existing constellations with minimal disruption.

Another significant customer base includes national space agencies and governmental entities, such as NASA, ESA, JAXA, and national defense organizations. These agencies utilize last-mile delivery for deploying scientific research satellites, secure communication assets, surveillance platforms, and experimental payloads into highly specific orbits. The critical nature of these missions often demands the highest levels of precision and reliability, making specialized last-mile services indispensable. Government interest also extends to capabilities like active space debris removal and in-orbit servicing for national security assets, further driving demand for these advanced logistics solutions.

Furthermore, academic institutions and research organizations represent a growing segment of potential customers, particularly those developing CubeSats and other small satellite missions for scientific experimentation or technology demonstration. These entities often have limited budgets and specific orbital requirements, making the cost-effective and flexible nature of last-mile delivery highly attractive. Emerging sectors like in-space manufacturing, asteroid mining, and future lunar or deep space exploration initiatives also represent significant long-term potential for last-mile delivery services, as they will require sophisticated transport and positioning capabilities beyond Earth's immediate orbit.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 5.8 billion |

| Market Forecast in 2032 | USD 27.9 billion |

| Growth Rate | 25.7% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Momentus, D-Orbit, Exolaunch, Astroscale, Impulse Space, Kleos Space, Orbit Fab, Loft Orbital, Atomos Space, Starfish Space, Spaceflight Inc., Slingshot Aerospace, LeoLabs, TransAstra, Redwire, Thales Alenia Space, Lockheed Martin, Northrop Grumman, Bradford Space. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Space Last-Mile Delivery Market is underpinned by a rapidly evolving technological landscape, with advancements continuously improving the efficiency, cost-effectiveness, and versatility of in-space logistics. A crucial area of innovation is advanced propulsion systems, including highly efficient electric propulsion (such as Hall effect thrusters and ion engines) that enable precise, long-duration orbital maneuvers with minimal propellant mass. Green propellants are also gaining traction as an environmentally conscious and safer alternative to traditional hydrazine, reducing handling risks and operational complexities. These propulsion technologies are vital for the extended mission durations and intricate trajectory corrections required for last-mile delivery.

Another cornerstone technology is autonomous navigation, rendezvous, and docking (AR&D) capabilities. As missions become more complex and involve multiple spacecraft, the ability for vehicles to independently detect, track, approach, and connect with other objects in space is paramount. This relies heavily on sophisticated sensors (Lidar, cameras, GPS/GNSS receivers), advanced algorithms, and onboard computing power, often leveraging artificial intelligence for real-time decision-making and anomaly detection. Furthermore, robotics and dexterous manipulators are increasingly being integrated for in-orbit servicing, refueling, and assembly tasks, allowing for complex operations previously deemed impossible without human intervention.

Modular spacecraft designs and standardized interfaces (e.g., CubeSat deployers, multi-payload adapters) are also critical, enabling greater compatibility and flexibility for integrating diverse payloads onto last-mile delivery platforms. The development of sophisticated ground control systems with advanced mission planning software and real-time telemetry processing is essential for monitoring and managing these intricate in-space operations. Miniaturization of components, 3D printing for on-demand manufacturing of spare parts, and robust communication systems further contribute to the technological maturity of the Space Last-Mile Delivery Market, collectively driving its capability to support a wide array of future space missions.

Space last-mile delivery refers to the specialized services and vehicles that transport payloads from a primary launch vehicle's initial orbit to their precise final orbital destination or beyond, ensuring accurate placement and maneuverability for diverse missions.

It reduces costs by enabling satellite operators to share a single, larger launch vehicle for multiple payloads, and then using in-space tugs to individually deploy each satellite to its specific orbit, thereby optimizing launch expenses and offering greater mission flexibility.

Key technologies include advanced electric and green propulsion systems, autonomous navigation and docking, robotics for in-orbit servicing, artificial intelligence for mission planning, and modular spacecraft designs that facilitate diverse payload integration.

Leading companies in this market include Momentus, D-Orbit, Exolaunch, Astroscale, Impulse Space, and Orbit Fab, among others, alongside traditional aerospace contractors expanding their in-space logistics capabilities.

Challenges include high capital investment, complex regulatory hurdles, the inherent risks associated with space debris and orbital collisions, technical complexities in autonomous operations, and the need for robust reliability in harsh space environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.