ID : MRU_ 430736 | Date : Nov, 2025 | Pages : 249 | Region : Global | Publisher : MRU

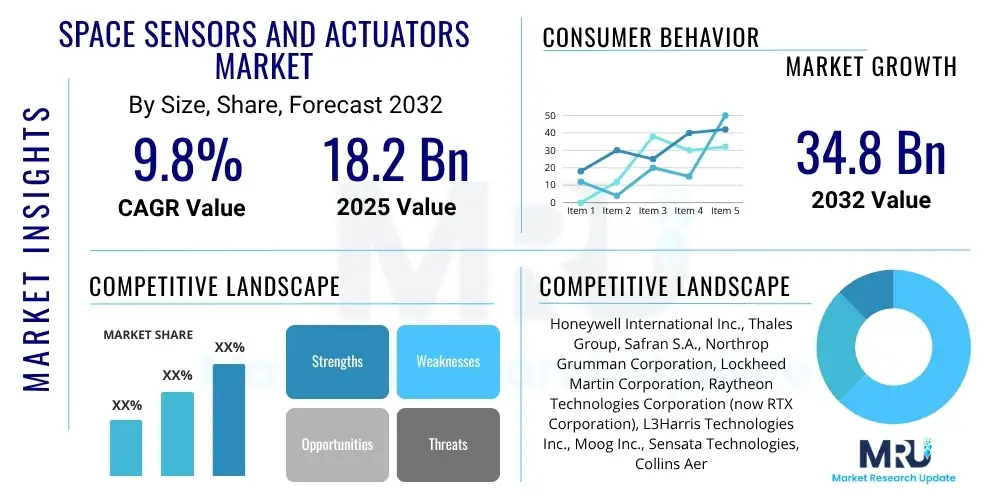

The Space Sensors and Actuators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2032. The market is estimated at $18.2 Billion in 2025 and is projected to reach $34.8 Billion by the end of the forecast period in 2032.

The Space Sensors and Actuators Market encompasses a critical range of sophisticated components essential for the operation, control, and data acquisition of spacecraft, satellites, and other space-borne platforms. These devices are the eyes, ears, and muscles of space systems, enabling everything from precise attitude control and orbital maneuvering to environmental monitoring and scientific data collection. As the global space economy expands, driven by commercialization, national security interests, and ambitious exploration initiatives, the demand for highly reliable, miniaturized, and intelligent sensors and actuators continues its upward trajectory. Their performance directly impacts mission success, longevity, and the quality of information gathered from orbit or deep space.

Space sensors are instruments designed to detect and measure physical quantities within the harsh space environment. This includes optical sensors for imaging and navigation, inertial sensors for attitude determination, thermal sensors for temperature regulation, and radiation sensors for monitoring cosmic rays. Actuators, conversely, are mechanisms that execute physical movements or control actions, such as reaction wheels for spacecraft orientation, thrusters for propulsion and orbital adjustments, gimbals for antenna pointing, and solar array drive assemblies for power optimization. Together, these technologies form the bedrock of modern space infrastructure, allowing for autonomous operation and complex mission profiles.

The major applications for these critical components span across various segments, including Earth observation, telecommunications, global navigation systems, space exploration, and defense intelligence. Benefits derived from advanced space sensors and actuators include enhanced precision in data collection, improved reliability in extreme conditions, extended mission lifetimes, and the enablement of highly autonomous operations. Key driving factors for market growth include the increasing number of satellite launches, particularly for mega-constellations in Low Earth Orbit (LEO), governmental and private investments in space exploration, and the escalating demand for satellite-derived services such as high-speed internet, precise GPS, and environmental monitoring.

The Space Sensors and Actuators Market is experiencing robust expansion, propelled by significant technological advancements and a burgeoning global space industry. Current business trends indicate a shift towards miniaturization, cost-efficiency, and increased integration of Artificial Intelligence and machine learning capabilities into sensor and actuator systems, enhancing autonomy and decision-making in space. The commercial space sector is a particularly dynamic area, with private companies driving innovation in satellite design and deployment, leading to a surge in demand for high-performance, compact components. Consolidations and strategic partnerships are also becoming more prevalent as companies seek to expand their technological portfolios and market reach, fostering a competitive yet collaborative landscape.

From a regional perspective, North America continues to dominate the market, primarily due to substantial investments from government space agencies like NASA and the Department of Defense, alongside a thriving ecosystem of private aerospace companies and technology innovators. Europe also maintains a strong market position, supported by the European Space Agency (ESA) programs and robust defense spending, with a focus on environmental monitoring and scientific research. The Asia Pacific region is rapidly emerging as a significant growth hub, driven by ambitious space programs in China, India, and Japan, which are aggressively expanding their satellite fleets and deep space exploration initiatives. Latin America, the Middle East, and Africa represent nascent but growing markets, with increasing interest in satellite-based communication and observation for economic development and security.

Segmentation trends reveal strong growth across various product types and applications. Optical sensors and inertial measurement units are seeing increased adoption for advanced imaging, navigation, and attitude control, while reaction wheels and electric propulsion thrusters are critical for the precise maneuvering and extended lifespan of satellites. The proliferation of small satellites, including CubeSats, is particularly boosting demand for miniaturized and standardized components. Furthermore, applications in Earth observation, telecommunications, and national security remain foundational, while deep space exploration and on-orbit servicing are presenting new opportunities for highly specialized and durable sensor and actuator systems, requiring innovative solutions to withstand extreme environments.

User questions regarding AI's impact on the Space Sensors and Actuators Market frequently revolve around how artificial intelligence enhances data processing, enables autonomous operations, and contributes to predictive maintenance for space assets. Common inquiries also address the challenges of integrating AI into safety-critical space systems, the role of machine learning in optimizing sensor performance, and the potential for AI-driven actuators to improve mission flexibility and responsiveness. Users are keen to understand if AI can significantly reduce human intervention in complex space missions, thereby lowering operational costs and increasing reliability in the face of communication delays and unforeseen events. The expectation is that AI will unlock new capabilities, pushing the boundaries of what is achievable in space exploration and commercial satellite operations, while also considering the cybersecurity implications and ethical considerations of highly autonomous systems.

The Space Sensors and Actuators Market is significantly shaped by a combination of powerful drivers, inherent restraints, emerging opportunities, and broader impact forces. Key drivers include the exponential growth in global satellite launches, particularly for commercial mega-constellations aimed at global internet coverage and Earth observation, which necessitate a vast number of reliable sensors and actuators. Furthermore, increasing government budgets for national security, defense, and ambitious deep space exploration missions consistently fuel demand for advanced and specialized components. The miniaturization trend in satellite technology also acts as a driver, opening new applications and making space access more affordable, while the demand for high-resolution data and precise positioning services from various industries continues to expand, pushing technological innovation in sensors.

Despite the strong growth trajectory, several restraints challenge market expansion. The high cost associated with designing, manufacturing, and testing space-grade sensors and actuators remains a significant barrier, especially for smaller players. The extreme operating conditions in space, including radiation, vacuum, and temperature fluctuations, demand rigorous qualification processes, leading to long development cycles and increased expenses. Additionally, the technical complexity and the need for specialized expertise in aerospace engineering limit market entry and foster a concentrated market structure. Geopolitical tensions and stringent export controls for sensitive space technologies can also impede international collaboration and market access for certain components, affecting supply chains and market dynamics.

Opportunities for growth are abundant and diverse. The burgeoning market for CubeSats and small satellites presents a fertile ground for developing cost-effective, standardized, and high-performance components. Advancements in artificial intelligence and machine learning offer significant potential for enhanced autonomy, predictive capabilities, and optimized performance of sensors and actuators, leading to more efficient and resilient space systems. The growing interest in on-orbit servicing, debris removal, and space tourism opens new niches for specialized robotic sensors and precision actuators. Moreover, the exploration of new frontiers, such as lunar and Martian missions, necessitates the development of next-generation sensors and actuators capable of operating under even more extreme and unique environmental conditions, stimulating significant research and development investments. The increasing involvement of private capital in the space industry, coupled with decreasing launch costs, further amplifies these opportunities.

The Space Sensors and Actuators Market is broadly segmented based on various critical parameters, including component type, specific sensor and actuator technologies, application areas, orbital altitudes, and end-user categories. This multi-faceted segmentation provides a granular view of market dynamics, enabling a deeper understanding of demand patterns, technological preferences, and growth pockets across the diverse landscape of space missions and applications. Each segment possesses unique characteristics, driven by specific technical requirements, operational environments, and strategic objectives of space programs, reflecting the highly specialized nature of the aerospace industry.

The value chain for the Space Sensors and Actuators Market is a complex ecosystem involving multiple stages, beginning from fundamental research and development to final deployment and operational support in space. Upstream activities primarily involve raw material suppliers, such as specialized metal alloys, composites, and semiconductor materials, which form the basic building blocks of these advanced components. This stage also includes manufacturers of highly specialized electronic components, optics, and precision mechanical parts that are crucial for the functional integrity and performance of space-grade sensors and actuators. These suppliers must adhere to extremely stringent quality and reliability standards, often requiring custom development and rigorous testing to meet aerospace specifications.

Midstream in the value chain, specialized companies focus on the design, engineering, and manufacturing of the sensors and actuators themselves. This includes firms that integrate raw materials and components into finished products, performing assembly, calibration, and extensive environmental testing to ensure survivability and performance in the harsh vacuum and radiation environments of space. These manufacturers work closely with prime contractors and system integrators to ensure their components meet precise mission requirements. The intellectual property and proprietary technologies developed at this stage, particularly in areas like high-precision optics, miniaturized IMUs, and efficient propulsion systems, are significant value differentiators.

Downstream activities involve the integration of these sensors and actuators into larger spacecraft and satellite platforms by prime aerospace contractors and satellite manufacturers. Once integrated, these systems are then sold or leased to end-users, which primarily include government space agencies, defense organizations, and a growing number of commercial satellite operators for communication, Earth observation, navigation, and scientific missions. The distribution channel is predominantly direct, with manufacturers engaging directly with prime contractors and government procurement bodies due to the highly customized and high-value nature of these products. Indirect channels might involve specialized distributors for certain standardized components or through larger system integrators who then sell complete satellite solutions, but this is less common for critical, high-performance space-grade sensors and actuators. Post-sales support, including software updates and troubleshooting, also forms a critical part of the downstream value chain, ensuring continued operational efficiency throughout the mission lifetime.

The Space Sensors and Actuators Market serves a diverse yet highly specialized clientele, primarily comprising entities with significant stakes in space exploration, defense, and commercial satellite operations. Government space agencies, such as NASA, ESA, Roscosmos, ISRO, and CNSA, are foundational customers, continually investing in advanced sensors and actuators for their scientific research missions, deep space probes, and human spaceflight programs. These agencies require components that offer unparalleled reliability, precision, and longevity to achieve complex mission objectives, often pushing the boundaries of current technological capabilities. Their procurement processes are typically rigorous, involving extensive testing and long-term contracts with established aerospace suppliers.

Defense organizations and military branches globally represent another major segment of potential customers. They utilize space sensors and actuators for intelligence gathering, surveillance, reconnaissance (ISR), secure communication, missile defense systems, and navigation. The demand here is driven by national security imperatives, requiring robust, resilient, and often classified technologies capable of operating in contested space environments. Aerospace prime contractors, such as Lockheed Martin, Boeing, Northrop Grumman, and Airbus Defence and Space, act as key intermediaries, purchasing these components to integrate into their larger satellite and spacecraft platforms before delivering to government and military clients.

The burgeoning commercial space sector is rapidly expanding the customer base. This includes commercial satellite operators building and deploying mega-constellations for global broadband internet, Earth imaging companies providing high-resolution data for various industries, and private entities engaged in space tourism, asteroid mining, and on-orbit servicing. Companies like SpaceX, OneWeb, Amazon Kuiper, and Planet Labs are significant buyers, often prioritizing cost-effectiveness, miniaturization, and rapid production alongside performance. Research institutions and universities also represent a niche segment, acquiring sensors and actuators for experimental CubeSats and scientific payloads, contributing to the advancement of space technology and human knowledge. These diverse end-users collectively drive innovation and demand across the entire spectrum of space sensors and actuators.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $18.2 Billion |

| Market Forecast in 2032 | $34.8 Billion |

| Growth Rate | 9.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., Thales Group, Safran S.A., Northrop Grumman Corporation, Lockheed Martin Corporation, Raytheon Technologies Corporation (now RTX Corporation), L3Harris Technologies Inc., Moog Inc., Sensata Technologies, Collins Aerospace (Raytheon Technologies), BAE Systems plc, Blue Canyon Technologies (a Raytheon Technologies company), Maxon Motor AG, Microchip Technology Inc., TDK Corporation, Curtiss-Wright Corporation, Teledyne Technologies Incorporated, Leonardo S.p.A., Astroscale Holdings Inc., AAC Clyde Space AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Space Sensors and Actuators Market is characterized by a rapidly evolving technological landscape driven by the relentless pursuit of enhanced performance, reduced size and weight, and increased autonomy for space missions. Miniaturization stands as a paramount technological trend, enabling the proliferation of small satellites and CubeSats by allowing more powerful capabilities to be packed into smaller, lighter, and more cost-effective packages. This involves advances in Micro-Electro-Mechanical Systems (MEMS) for inertial sensors and micro-thrusters, as well as compact optical systems that maintain high resolution. Concurrently, the development of advanced materials, including composites and specialized alloys, is crucial for improving durability, radiation hardness, and thermal management in extreme space environments, ensuring components can withstand harsh conditions for extended periods.

Another significant technological frontier is the integration of artificial intelligence and machine learning directly into sensor and actuator systems. This enables on-board data processing, autonomous decision-making, predictive maintenance, and adaptive control, significantly reducing the reliance on ground control and improving mission responsiveness and efficiency, particularly for deep space missions with considerable communication delays. Furthermore, advancements in precision engineering and additive manufacturing (3D printing) are revolutionizing the production of complex and customized sensor and actuator geometries, allowing for rapid prototyping, reduced lead times, and optimized designs for specific mission profiles. These manufacturing innovations also facilitate the creation of components with internal structures that enhance performance, such as optimized cooling channels or integrated wiring, which were previously impossible with traditional manufacturing methods.

High-precision control systems are continuously being refined, especially for attitude determination and control, rendezvous and docking, and fine pointing of instruments. This includes more accurate star trackers, gyroscopes, and reaction wheels, alongside the development of electric propulsion systems that offer higher specific impulse and longer operational lifetimes for orbital maneuvers. Emerging technologies such as quantum sensing, which promises unprecedented accuracy for navigation and scientific measurements, are also on the horizon. The convergence of these technological innovations is creating a new generation of intelligent, resilient, and highly capable space sensors and actuators, fundamental for the ambitious future of space exploration and commercial utilization.

Market growth is primarily driven by the increasing number of satellite launches, particularly commercial mega-constellations, escalating government and private investments in space exploration, and rising demand for satellite-based services like communication and Earth observation.

Key applications include Earth observation and remote sensing, satellite communication, global navigation systems, scientific space exploration, defense and intelligence, and emerging areas like on-orbit servicing and manufacturing.

AI significantly enhances market capabilities by enabling autonomous operations, optimizing sensor data processing, improving predictive maintenance for actuators, and facilitating smarter spacecraft control and decision-making for complex missions.

Major challenges include the high cost of development and manufacturing for space-grade components, stringent technical requirements, long qualification cycles due to harsh space environments, and complex regulatory frameworks affecting global trade.

North America currently leads due to significant government and commercial investments, followed by Europe with strong space agency programs. The Asia Pacific region is rapidly growing, driven by major national space initiatives and increasing commercial satellite deployment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.