ID : MRU_ 427296 | Date : Oct, 2025 | Pages : 245 | Region : Global | Publisher : MRU

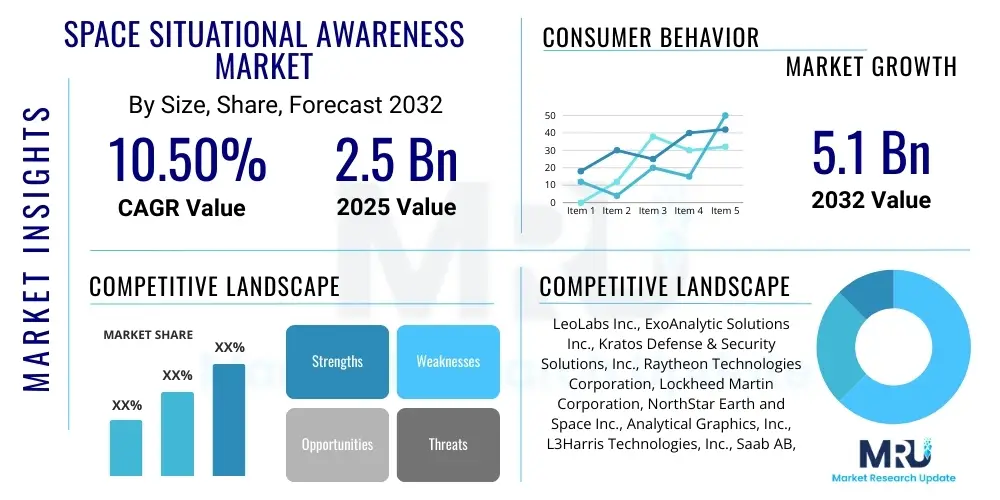

The Space Situational Awareness Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2032. The market is estimated at USD 2.5 billion in 2025 and is projected to reach USD 5.1 billion by the end of the forecast period in 2032.

The Space Situational Awareness (SSA) market encompasses the technologies and services designed to understand, monitor, and predict the space environment, particularly concerning objects in Earths orbit. This includes tracking satellites, space debris, and potential threats to ensure the safety, security, and sustainability of space operations. The core product involves sophisticated sensor networks, data processing algorithms, and analytical software that provide precise orbital information and predictive capabilities.

Major applications of SSA extend across defense, commercial, and civilian sectors. It is critical for collision avoidance to protect operational satellites from a growing array of space debris, for monitoring potential adversarial activities in space, and for assessing the impact of space weather events on satellite performance. Benefits include enhanced operational safety, extended satellite lifespans, improved national security through space domain awareness, and the fostering of sustainable space utilization practices. The imperative to manage an increasingly congested and contested orbital environment drives the markets expansion.

Several key factors are propelling the growth of the SSA market. The rapid proliferation of satellite constellations, particularly in Low Earth Orbit (LEO), for communication and remote sensing, significantly increases the risk of orbital collisions. Furthermore, the growing reliance on space-based assets for critical infrastructure and defense necessitates robust monitoring capabilities. Geopolitical tensions and the increasing weaponization of space also underscore the importance of comprehensive space domain awareness, pushing governments and commercial entities to invest heavily in SSA solutions.

The Space Situational Awareness (SSA) market is experiencing robust growth, primarily driven by the escalating number of objects in orbit, including active satellites and space debris, coupled with the increasing strategic importance of space assets for national security and economic activities. Business trends highlight a significant shift towards commercial SSA services, with private companies leveraging advanced sensor technologies, artificial intelligence, and data analytics to offer cost-effective and comprehensive solutions previously dominated by government agencies. Collaborative efforts between public and private sectors are also becoming more prevalent, aiming to enhance the accuracy and coverage of SSA data.

Regionally, North America maintains its dominance in the SSA market, fueled by substantial government and defense spending, alongside a strong presence of advanced technology companies and research institutions. Europe is also a key player, driven by initiatives from the European Space Agency (ESA) and various national space programs focused on space safety and security. The Asia-Pacific region is emerging as a significant growth area, with countries like China, India, and Japan rapidly expanding their space capabilities and investing in domestic SSA infrastructure to protect their burgeoning satellite fleets.

In terms of segments, the market is broadly categorized by component (software, services, hardware), end-user (commercial, government, military), and application (collision avoidance, space weather monitoring, intelligence, surveillance, and reconnaissance (ISR)). The services segment, particularly data analysis and conjunction assessment services, is anticipated to witness the highest growth, reflecting the complex nature of interpreting vast amounts of orbital data. The military and defense end-user segment continues to be a primary revenue contributor, emphasizing the strategic importance of SSA for national security, while the commercial segment is rapidly expanding due to the proliferation of private satellite operators and launch providers.

Users frequently inquire about Artificial Intelligences transformative potential in overcoming the data overload and analytical complexity inherent in Space Situational Awareness (SSA). Key themes revolve around AIs ability to automate the processing of vast datasets from diverse sensors, enabling more rapid and accurate identification, tracking, and characterization of space objects, including previously undetected debris. Concerns also emerge regarding the reliability of AI-driven predictions, the ethical implications of autonomous decision-making in space, and the need for robust, explainable AI models to maintain human oversight in critical situations like collision avoidance or threat assessment. Expectations are high for AI to enhance predictive capabilities for space weather and object behavior, thereby improving the efficiency and safety of global space operations, reducing operational costs, and bolstering national security.

The integration of AI is widely anticipated to enable a proactive approach to space traffic management, shifting from reactive responses to predictive interventions. Users expect AI to streamline data fusion from heterogeneous sensor networks, resolving discrepancies and creating a unified, high-fidelity picture of the orbital environment. This is particularly crucial as the number of active satellites and fragments of space debris continues to grow exponentially, making manual analysis increasingly unsustainable. Furthermore, AI is expected to democratize advanced SSA capabilities, allowing smaller entities and commercial operators to leverage sophisticated analytical tools that were once the exclusive domain of large governmental space agencies.

The Space Situational Awareness (SSA) market is propelled by a confluence of drivers, yet simultaneously constrained by significant challenges, while also presenting substantial opportunities for innovation and growth. The primary drivers include the exponential increase in satellite launches, leading to a severely congested orbital environment, which heightens the risk of collisions and necessitates comprehensive tracking. Furthermore, the growing geopolitical competition in space and the imperative for national security, driven by the weaponization of space and the reliance on space assets for critical infrastructure, are forcing governments and defense organizations to invest heavily in robust SSA capabilities. The commercialization of space, with mega-constellations and private space ventures, also demands reliable SSA services to protect valuable assets and ensure operational continuity.

Conversely, several restraints impede the markets full potential. The high cost associated with developing, deploying, and maintaining sophisticated sensor networks, data processing infrastructure, and highly skilled personnel poses a significant barrier, particularly for smaller nations or emerging commercial entities. The sheer volume and complexity of data generated by SSA systems also present analytical challenges, requiring advanced algorithms and computing power. Additionally, the lack of universally standardized data sharing protocols and regulatory frameworks across international borders creates inconsistencies and limits the effectiveness of global SSA efforts, as space is a shared domain requiring collaborative solutions.

Despite these challenges, immense opportunities exist within the SSA market. Advancements in miniaturization and CubeSat technology are making space-based sensors more accessible and affordable, expanding the reach and resolution of data collection. The rapid evolution of Artificial Intelligence and Machine Learning (AI/ML) algorithms offers unprecedented capabilities for automated data analysis, anomaly detection, and predictive modeling, transforming raw data into actionable intelligence. The burgeoning demand for commercial SSA services from private satellite operators, launch providers, and insurance companies presents a lucrative market segment. Moreover, increasing public-private partnerships are fostering innovation and accelerating the deployment of advanced SSA solutions, leveraging both governmental resources and commercial agility. These market forces collectively shape the trajectory and strategic importance of the SSA sector.

The Space Situational Awareness (SSA) market is meticulously segmented to reflect the diverse technological approaches, varied end-user requirements, and specific applications that define its landscape. This segmentation allows for a granular understanding of market dynamics, identifying key growth areas and niche demands. The market is typically categorized by solution type, platform, end-user, and application, each revealing distinct trends and investment priorities within the broader SSA ecosystem. This structured approach helps stakeholders, from technology providers to policymakers, in strategic planning and resource allocation. The interplay between these segments is crucial for comprehensive space domain awareness.

Understanding these segments is vital for tailoring solutions to specific needs. For instance, defense organizations may prioritize highly resilient ground-based radar systems combined with advanced data analytics for threat detection, while commercial satellite operators might focus on cost-effective, real-time collision avoidance services. The increasing complexity of space operations, coupled with the growth of diverse actors in space, further accentuates the importance of a detailed segmentation analysis. This allows for the development of targeted technologies and service offerings that address the unique challenges and opportunities across the entire SSA value chain, ensuring effective monitoring and protection of assets in an increasingly contested and congested orbital environment.

The Space Situational Awareness (SSA) markets value chain is a complex interplay of various stages, starting from upstream data acquisition to downstream service delivery, involving a multitude of specialized actors. Upstream analysis focuses on the collection of raw data, primarily through a diverse array of sensors. This includes the development and deployment of ground-based assets like advanced radars and optical telescopes, as well as space-based sensors, such as dedicated SSA satellites or hosted payloads on commercial spacecraft. Key players in this stage are often defense contractors, space agencies, and specialized sensor manufacturers, responsible for the precision engineering and operational readiness of data collection infrastructure.

Midstream activities involve the critical processes of data processing, fusion, and analysis. This stage transforms raw sensor data into actionable intelligence. It encompasses sophisticated software development for orbital mechanics calculations, AI/ML algorithms for anomaly detection, data fusion platforms that integrate information from heterogeneous sources, and visualization tools that present complex orbital environments in an understandable format. Companies specializing in advanced analytics, software engineering, and cloud computing play a pivotal role here, converting vast datasets into meaningful insights for decision-makers. This stage is crucial for making sense of the ever-growing volume of space-related information.

Downstream analysis focuses on the delivery of SSA services and insights to end-users. This includes providing conjunction assessment reports, space weather forecasts, threat warnings, and comprehensive space traffic management solutions. Distribution channels are varied, encompassing direct contractual agreements with government agencies and defense organizations, commercial service providers offering subscription-based data and analytical tools to satellite operators, and partnerships with launch providers for pre-launch collision risk assessments. Direct channels involve bespoke solutions and high-security data transfer, while indirect channels often leverage secure web portals or API integrations for broader accessibility. The efficiency of these channels determines the timely and effective dissemination of critical SSA intelligence to those who need it most.

The Space Situational Awareness (SSA) market caters to a diverse range of end-users and buyers, each with specific requirements for monitoring and understanding the space environment. Governments and national defense organizations represent a foundational customer base, driven by national security imperatives. These entities require comprehensive SSA capabilities for military operations, intelligence gathering, threat assessment, and the protection of sovereign space assets. Their needs often include highly secure, resilient, and comprehensive systems capable of detecting, tracking, and characterizing a wide spectrum of space objects, including potential adversarial capabilities. Investment in SSA is a direct reflection of strategic national interests in maintaining space superiority and ensuring the integrity of critical space infrastructure.

Beyond traditional governmental clients, the burgeoning commercial space sector forms a rapidly expanding segment of potential customers. This includes a vast array of satellite operators, ranging from established telecommunications companies to operators of large Low Earth Orbit (LEO) mega-constellations for broadband internet. These commercial entities require reliable SSA services to ensure the safety of their multi-billion dollar satellite fleets, primarily for collision avoidance against space debris and other operational satellites. Launch service providers also constitute a significant customer group, as they need accurate pre-launch and in-orbit collision risk assessments to ensure safe deployment of payloads. The economic imperative to protect valuable space assets and prevent costly downtime makes SSA an indispensable operational requirement for these commercial players.

Other vital end-users include international space agencies like NASA and ESA, which prioritize space safety, scientific research, and the sustainable use of outer space. These agencies utilize SSA data for mission planning, orbital debris research, and contributing to global space traffic management initiatives. Additionally, insurance companies specializing in space assets are increasingly becoming indirect customers, leveraging SSA data for risk assessment, policy underwriting, and claims management in the event of orbital incidents. Academic institutions and research organizations also rely on SSA data for scientific study and the development of next-generation space technologies. This broad customer base underscores the universal need for reliable space domain awareness across public and private sectors.

The Space Situational Awareness (SSA) market relies heavily on a sophisticated array of technologies for effective data acquisition, processing, and analysis. At the core are advanced sensor technologies, which include a blend of ground-based and space-based systems. Ground-based sensors, such as powerful C-band, S-band, and X-band radars, are crucial for detecting and tracking objects in various orbital regimes, especially larger debris and active satellites. Alongside these, high-resolution optical telescopes, often located in geographically dispersed networks, provide precise positional data and enable the characterization of space objects. Laser ranging stations contribute to highly accurate orbital parameter determination for specific satellites, complementing the broader tracking efforts.

Space-based technologies are rapidly gaining prominence, offering advantages like persistent surveillance and the ability to track objects beyond Earths atmospheric interference. This involves dedicated SSA satellites equipped with various sensors, as well as hosted payloads on commercial or governmental spacecraft that can perform observation tasks. The miniaturization of technology has enabled the deployment of CubeSats and small satellites carrying SSA payloads, increasing sensor network density and reducing costs. These platforms can provide unique viewing geometries and fill gaps in ground-based coverage, particularly for objects in low inclination orbits or those obscured by atmospheric conditions.

Beyond data collection, the analytical and processing capabilities form another critical technological pillar. Artificial Intelligence (AI) and Machine Learning (ML) algorithms are increasingly vital for handling the immense volume and velocity of SSA data. These technologies enable automated object identification, anomaly detection, predictive orbital modeling, and sophisticated data fusion techniques that integrate information from disparate sources into a coherent picture. Cloud computing infrastructure provides the necessary scalability and computational power for storing, processing, and analyzing vast datasets in real-time. Furthermore, advanced data visualization tools and secure communication networks are essential for delivering actionable intelligence to end-users in a timely and understandable format, ensuring effective decision-making in a rapidly evolving space environment.

The global Space Situational Awareness (SSA) market exhibits distinct regional dynamics driven by varying levels of space activity, defense spending, technological capabilities, and regulatory frameworks. Each region contributes uniquely to the markets evolution, with specific countries leading in innovation, investment, and the adoption of advanced SSA solutions. Understanding these regional highlights is crucial for market participants to tailor strategies and identify growth opportunities.

North America, particularly the United States, stands as the dominant region in the SSA market. This leadership is underpinned by substantial governmental and defense expenditures, robust research and development initiatives, and the presence of numerous key players in the aerospace and defense sectors. The U.S. Space Force and various defense contractors are at the forefront of developing advanced SSA capabilities, driven by national security interests and the protection of extensive space assets. Canada also contributes significantly with specialized expertise and commercial SSA ventures.

Europe represents another mature and influential market, propelled by the European Space Agency (ESA) and national space programs across the United Kingdom, France, Germany, and Italy. These countries are actively investing in independent SSA capabilities to enhance space safety, manage space traffic, and foster international cooperation. The European Unions efforts to establish a robust SSA framework further solidify its market position, focusing on both governmental and commercial applications.

The Asia-Pacific region is emerging as a high-growth market, characterized by rapidly expanding space programs and increasing satellite deployments, particularly in China, India, and Japan. These nations are investing heavily in domestic SSA infrastructure to protect their burgeoning space assets and support their ambitious space exploration and commercialization goals. The regions growing economic power and strategic interests in space are fueling significant demand for advanced SSA technologies and services.

The Rest of the World, including countries in Latin America, the Middle East, and Africa, is gradually increasing its engagement in the SSA market. While currently smaller in scale, these regions are developing nascent space capabilities, driven by a desire for independent satellite operations, regional security, and economic development. Partnerships with established SSA providers and the adoption of more affordable commercial solutions are common approaches in these developing markets, indicating future growth potential.

Space Situational Awareness (SSA) refers to the comprehensive understanding and monitoring of objects and conditions in Earths orbit. This includes tracking active satellites, space debris, and natural phenomena like space weather, to ensure the safety, security, and sustainability of space operations and assets.

SSA is critical for preventing collisions between operational satellites and the growing volume of space debris, protecting valuable space infrastructure, and monitoring potential threats in space. It ensures the longevity of satellites, supports national security, and facilitates the safe and sustainable utilization of outer space for various applications.

AI significantly enhances SSA by automating the processing of vast amounts of sensor data, improving the accuracy of object detection and tracking, and providing predictive analytics for collision avoidance and space weather forecasting. AI enables more efficient data fusion, anomaly detection, and decision support for human operators.

Key challenges include the rapidly increasing volume of space debris and active satellites leading to orbital congestion, the high cost of deploying and maintaining advanced sensor networks, the complexity of data processing and analysis, and the need for greater international cooperation and standardized regulatory frameworks for data sharing and space traffic management.

The primary users of SSA solutions include government defense organizations and military forces, national and international space agencies, commercial satellite operators (including LEO mega-constellation providers), private launch service providers, and to a lesser extent, academic institutions and space insurance companies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.