ID : MRU_ 431301 | Date : Nov, 2025 | Pages : 245 | Region : Global | Publisher : MRU

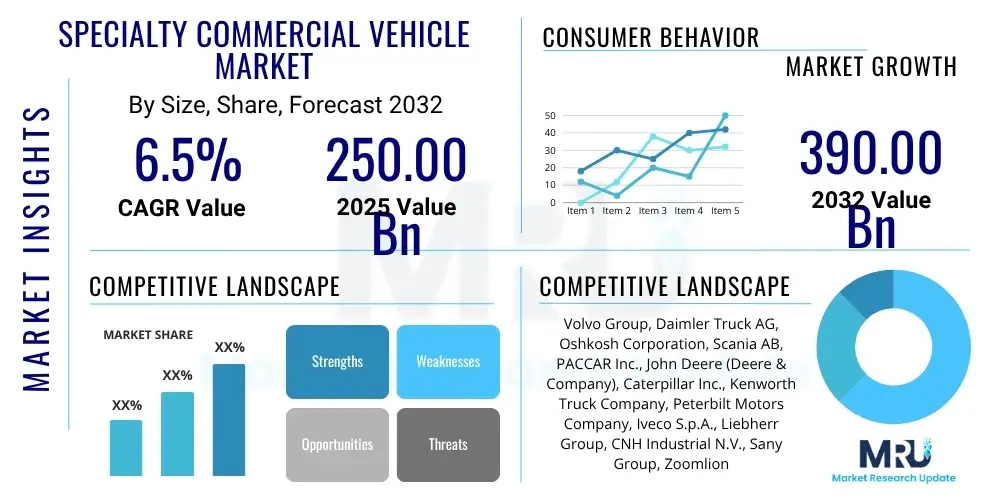

The Specialty Commercial Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at USD 250.00 billion in 2025 and is projected to reach USD 390.00 billion by the end of the forecast period in 2032.

The Specialty Commercial Vehicle Market encompasses a diverse range of vehicles meticulously designed for specific operational tasks that extend beyond conventional transportation. These vehicles are integral to various industrial and public service sectors, playing a crucial role in supporting critical infrastructure development, maintaining public safety, ensuring logistics efficiency, and managing environmental resources. Characterized by their specialized equipment, robust construction, and unique functionalities, they are engineered to perform demanding operations across diverse operational landscapes. This market segment is defined by continuous innovation, aiming to enhance operational efficiency, bolster safety standards, and significantly improve environmental sustainability across all applications. The bespoke nature of these vehicles often involves integrating advanced hydraulic systems, powerful engines, and sophisticated control mechanisms to meet exacting demands.

Products within this market segment are highly varied and include, but are not limited to, refuse collection vehicles for waste management, fire trucks for emergency response, ambulances for critical medical transport, concrete mixers for construction, heavy-duty cranes for lifting, and various forms of agricultural machinery. Other important categories encompass mining trucks, utility maintenance vehicles, and a wide array of construction equipment such as excavators, loaders, and pavers. Each vehicle type is precision-engineered to fulfill the exacting requirements of its intended application, frequently incorporating cutting-edge technology and materials for optimal performance and durability. These specialized vehicles serve as indispensable assets in both highly developed economies and rapidly industrializing regions, underpinning fundamental services and economic activities that are essential for societal advancement and industrial progress, thus driving consistent demand and ongoing development.

Major applications for specialty commercial vehicles span a wide range of sectors including municipal services, construction, logistics, emergency response, agriculture, and resource extraction. For instance, local governments rely on refuse vehicles for efficient waste management and fire trucks for critical public safety, while construction companies extensively utilize concrete mixers and mobile cranes for complex building and infrastructure projects. The inherent benefits derived from these vehicles are multifaceted, encompassing enhanced operational efficiency, significantly improved safety standards for both operators and the public, strict compliance with increasingly stringent environmental regulations, and the capacity to execute tasks that would otherwise be impractical, unsafe, or highly inefficient. Key driving factors propelling sustained market growth include rapid global urbanization, escalating investments in global infrastructure development, the exponential expansion of e-commerce necessitating specialized last-mile logistics solutions, the implementation of stricter environmental norms worldwide, and a persistent drive for technological advancements in vehicle design and functionality, including the widespread adoption of automation and electrification technologies.

The Specialty Commercial Vehicle Market is undergoing significant transformations influenced by global macroeconomic trends and technological paradigm shifts. Current business trends highlight a pronounced shift towards vehicle electrification, with leading manufacturers investing substantial resources into the research, development, and production of electric and hybrid models. This pivot is driven by an imperative to meet evolving sustainability targets, comply with stricter environmental regulations, and capitalize on the long-term benefits of reduced operating costs and lower emissions. Furthermore, the pervasive integration of advanced telematics, Internet of Things (IoT) connectivity, and Artificial Intelligence (AI)-driven solutions is revolutionizing operational paradigms. These technologies facilitate sophisticated functionalities such as predictive maintenance, real-time fleet management, and enhanced safety features, thereby optimizing performance and extending vehicle lifecycles. Customization remains a critical aspect, as end-users frequently demand highly specific vehicle configurations to perfectly align with their specialized operational requirements, fostering a market environment of bespoke designs and flexible manufacturing processes. The emergence of service-oriented business models, where manufacturers offer comprehensive maintenance, telematics, and software services in addition to vehicle sales, is also gaining considerable traction, cultivating deeper customer relationships and establishing recurring revenue streams.

Regional trends indicate robust expansion within the Asia Pacific (APAC) region, primarily attributed to accelerating urbanization, extensive and ongoing infrastructure development projects, and escalating industrialization across key economies such as China, India, and various Southeast Asian nations. This demand is further amplified by supportive governmental initiatives aimed at upgrading municipal services and modernizing the agricultural and construction sectors. North America and Europe, while representing more mature and established markets, are witnessing substantial demand for advanced, environmentally compliant, and technologically sophisticated specialty vehicles. These regions are at the vanguard of adopting electric and autonomous solutions, propelled by stringent emission mandates and a strong emphasis on maximizing operational efficiency and ensuring paramount worker safety. Latin America, the Middle East, and Africa are demonstrating promising growth trajectories, albeit originating from a comparatively lower base, spurred by significant investments in mining, critical energy infrastructure, and public utility development projects. Each geographical region exhibits distinctive market dynamics, shaped by prevailing local economic conditions, specific regulatory frameworks, and unique operational requirements, demanding tailored market approaches.

Segment trends unequivocally underscore the increasing prevalence and adoption of electric propulsion systems across a multitude of specialty vehicle types. This is particularly evident in urban-centric applications such as refuse collection and last-mile delivery services, where the benefits of zero emissions, reduced noise pollution, and lower operational expenditures are highly valued. The construction equipment segment continues to benefit immensely from substantial global infrastructure spending, driving a heightened demand for larger, more efficient, and increasingly automated machinery capable of handling complex projects. Emergency services vehicles are integrating more advanced communication systems, sophisticated medical technologies, and increasingly adopting hybrid and electric powertrains to minimize environmental impact and enhance operational readiness during critical incidents. The waste management sector is undergoing significant evolution with the introduction of smarter, more efficient refuse trucks that incorporate advanced automation for optimized collection routes and improved compaction capabilities. This intricate interplay of business, regional, and segment-specific trends collectively shapes a complex yet highly opportune landscape for the Specialty Commercial Vehicle Market, pointing towards sustained innovation, strategic investments, and substantial growth for all key stakeholders in the foreseeable future.

Common user inquiries concerning the impact of Artificial Intelligence (AI) on the Specialty Commercial Vehicle Market frequently center on its potential to significantly enhance operational safety, boost efficiency, and accelerate the progression towards higher levels of autonomy. Users are keenly interested in understanding the tangible, practical applications of AI in real-world operational scenarios, such as its capacity to enable predictive maintenance to minimize costly downtime, its role in optimizing complex route planning for improved fuel economy and more efficient service delivery, and its contribution to the development of advanced driver-assistance systems (ADAS) or even fully autonomous operational functionalities. Furthermore, there is considerable interest in how AI can contribute to improving environmental performance through smarter resource management and substantial reductions in emissions. Alongside these expectations, users express concerns regarding the financial implications of AI implementation, the crucial aspects of data security, and the inherent integration challenges with existing legacy systems. These inquiries collectively highlight a strong anticipation for AI to fundamentally revolutionize the sector by offering intelligent solutions that address long-standing operational hurdles, while also indicating a cautious yet optimistic outlook on the practicalities and broader implications of such advanced technological adoption within this highly specialized and critical industry.

The Specialty Commercial Vehicle Market is intrinsically influenced by a sophisticated interplay of driving forces, inherent restraining factors, emerging opportunities, and broader impact forces that collectively shape its developmental trajectory and market dynamics. Significant drivers include the relentless pace of global urbanization, which concurrently necessitates the expansion and modernization of municipal services and robust infrastructure development. This directly fuels a consistent demand for a wide array of specialized vehicles such as refuse trucks, highly capable concrete mixers, and essential utility vehicles. Furthermore, substantial governmental and private sector investments in critical infrastructure projects worldwide, especially prominent in rapidly developing economies, are creating a strong foundational demand for market expansion. The continuous and exponential evolution of e-commerce platforms is generating an increasing demand for specialized last-mile delivery vehicles and innovative logistics solutions, while increasingly stringent global environmental regulations are progressively compelling manufacturers to develop and adopt cleaner, more energy-efficient, and predominantly electric or hybrid specialty vehicle solutions. Moreover, the fundamental need for enhanced safety protocols and optimized operational efficiency across diverse industries serves as a potent catalyst for the widespread adoption of technologically advanced vehicles equipped with state-of-the-art features and functionalities.

However, several significant restraints continue to pose notable challenges to the accelerated growth of this market. The considerably high initial acquisition cost of many specialty commercial vehicles, often attributable to their bespoke nature, sophisticated integrated technology, and specialized equipment, can frequently act as a formidable barrier for smaller enterprises or municipalities operating with more constrained budgets. The inherent complexity involved in seamlessly integrating nascent technologies, such as advanced telematics, Artificial Intelligence (AI) platforms, or nascent electric powertrains, into existing legacy fleet operations can also serve as a substantial deterrent, demanding considerable upfront investment in specialized training for personnel and the development of requisite supporting infrastructure. Furthermore, a persistent shortage of adequately skilled labor proficient in operating and meticulously maintaining these increasingly complex machines, particularly those incorporating advanced digital and electrical systems, presents an ongoing and critical challenge across various regions. Moreover, intricate regulatory hurdles, particularly pertaining to the deployment of fully autonomous vehicles and specific operational standards that vary significantly across different geographical regions, introduce additional layers of complexity and can considerably impede the timely market adoption of cutting-edge solutions. The substantial investment critically required for developing and expanding adequate charging infrastructure specifically tailored for electric specialty vehicles remains a significant bottleneck in many regions, hindering their widespread adoption.

Despite these discernible challenges, numerous promising opportunities are poised to propel significant future growth within the market. The burgeoning adoption of electrification and the exploration of alternative fuel powertrains, such as advanced hydrogen fuel cells, represent a substantial avenue for groundbreaking innovation and deeper market penetration, directly addressing critical environmental concerns and simultaneously offering significant reductions in long-term operational costs. The ongoing development and refinement of autonomous and semi-autonomous capabilities in specialty vehicles promise to fundamentally revolutionize operational efficiency and drastically improve safety, especially in controlled and repetitive operational environments like large-scale mining sites or modern waste management facilities. Enhanced telematics and advanced Internet of Things (IoT) integration offer unparalleled opportunities for sophisticated fleet management, proactive predictive maintenance, and optimized performance analytics. The consistently growing demand for highly customized vehicles, meticulously tailored to meet precise operational requirements, continues to provide manufacturers with ample scope to differentiate their offerings and capture niche markets. Furthermore, the strategic expansion into rapidly emerging markets, particularly where infrastructure and municipal services are undergoing vigorous development, presents largely untapped potential for significant market expansion. Key impact forces that continuously shape the market include rapid technological advancements, evolving regulatory frameworks, fluctuating global economic conditions, pressing environmental sustainability mandates, and dynamic demographic trends such such as accelerating urbanization and expanding global populations, all contributing to a complex and evolving market landscape.

The Specialty Commercial Vehicle Market is comprehensively segmented to provide a granular and nuanced understanding of its highly diverse components and underlying market dynamics. This strategic segmentation is instrumental in accurately analyzing prevailing market trends, effectively identifying burgeoning growth opportunities, and precisely understanding the specific and often unique needs of various end-user industries across the globe. The market can be meticulously categorized based on several pivotal parameters, including the distinct vehicle type, its primary application, the specific propulsion system utilized, the gross vehicle weight (GVW) capacity, and the ultimate end-user sector. Each delineated segment exhibits unique demand characteristics, specific technological requirements, and a distinct competitive landscape, thereby offering highly specialized market insights for a broad spectrum of stakeholders including manufacturers, component suppliers, and service providers alike. Understanding these intricate segments is absolutely crucial for formulating effective strategic planning, guiding targeted product development initiatives, and successfully navigating market entry strategies within this inherently specialized and critical industry. This allows all stakeholders to develop and deliver highly tailored solutions that precisely meet the exacting operational demands and stringent regulatory standards prevalent across different geographical regions and operational contexts.

The value chain for the Specialty Commercial Vehicle Market is notably complex and multi-faceted, encompassing a comprehensive sequence of stages from the initial sourcing of raw materials to the final deployment by the end-user and subsequent after-sales support. The upstream segment of this extensive value chain is predominantly characterized by raw material suppliers and specialized component manufacturers. Raw material providers are responsible for supplying essential foundational materials such as various high-grade steel alloys, lightweight aluminum alloys, robust plastics, advanced composite materials, and specialized chemicals, all of which are critically important for the structural integrity and functionality of vehicle construction. Following this, component manufacturers play an absolutely pivotal role by specializing in the production of complex and highly engineered parts. These include advanced engines, sophisticated transmissions, heavy-duty axles, resilient chassis components, intricate hydraulic systems, cutting-edge electronic control units (ECUs), specialized pumps, precise lifting mechanisms, and a wide array of application-specific attachments. The unwavering quality, consistent availability, and continuous innovation of these components directly impact the overall performance, unwavering reliability, and crucial cost-effectiveness of the final specialty vehicles. This underscores the paramount importance of cultivating robust and collaborative supplier relationships and establishing an incredibly resilient supply chain. Innovation in materials science and component design at this foundational stage can significantly influence the market's overarching technological progress and its competitive landscape.

Progressing downstream, the value chain seamlessly transitions through the crucial stage of Original Equipment Manufacturers (OEMs), who bear the primary responsibility for the intricate design, precise assembly, and meticulous integration of all these specialized components into fully operational and compliant vehicles. OEMs frequently engage in extensive and continuous research and development activities to incorporate cutting-edge technologies, meticulously optimize vehicle performance parameters, ensure strict compliance with increasingly demanding international safety and environmental standards, and effectively cater to highly bespoke customer requirements. After the rigorous manufacturing process is complete, the effectiveness of the distribution channel becomes absolutely critical. This typically involves a strategic combination of both direct sales approaches and indirect distribution networks. Large-scale fleet operators, governmental agencies, and major industrial clients often engage in direct procurement methods from OEMs or their dedicated sales divisions. This fosters direct, long-term relationships for substantial bulk orders and highly customized vehicle solutions, facilitating closer collaboration on precise vehicle specifications and comprehensive after-sales service agreements, thereby ensuring that the specialized vehicles precisely meet exacting operational demands.

Indirect distribution strategies primarily leverage an extensive and well-established network of authorized dealers and specialized distributors. These intermediaries are critically vital for effectively reaching a much broader and more diverse customer base, particularly smaller businesses, independent private contractors, and individual buyers, spanning across vast and varied geographical regions. Dealers play a multi-faceted role by providing essential sales support, facilitating various financing options, and, most crucially, offering localized after-sales services. These services encompass routine maintenance, complex repairs, and the reliable supply of genuine spare parts. The efficiency, geographical reach, and responsiveness of these extensive distribution networks are absolutely fundamental to achieving deep market penetration and ensuring sustained customer satisfaction. Furthermore, the aftermarket segment, which comprehensively includes the provision of spare parts, extensive maintenance services, intricate repairs, and critical technological upgrades, forms another indispensable component of the downstream value chain. This aftermarket support ensures the long-term operational viability, extended asset lifespan, and optimal performance of specialty commercial vehicles throughout their operational duration. This comprehensive and interconnected value chain unequivocally highlights the profound interdependence of various stakeholders, ranging from raw material suppliers to end-users, with each contributing uniquely to the market's overall functionality, efficiency, and consistent growth. The adept and strategic management of this entire chain is utterly essential for optimizing costs, accelerating the pace of innovation, and consistently delivering high-quality, highly specialized solutions to a demanding and diverse global clientele.

The Specialty Commercial Vehicle Market caters to an exceptionally broad and diverse spectrum of potential customers, each possessing unique operational requirements and distinct demands, thereby constituting a highly diversified and complex sector. These end-users are typically organizations or governmental entities that necessitate vehicles specifically engineered and comprehensively equipped to perform tasks extending far beyond general transportation. Such tasks often involve heavy-duty operations, critical emergency response, or highly precise logistical functions that demand specialized capabilities. Their purchasing decisions are meticulously driven by a multitude of factors, including paramount vehicle performance, unwavering reliability, optimal operational efficiency, strict compliance with evolving safety and environmental regulations, and a comprehensive consideration of the total cost of ownership throughout the vehicle's entire operational lifespan. A thorough understanding of the varied and nuanced needs of these diverse customer segments is absolutely paramount for manufacturers and service providers to effectively develop highly targeted products and formulate robust, effective market strategies. This ensures that specialized solutions are perfectly aligned with the unique challenges and strategic objectives of disparate industries. The ongoing relentless push for technological innovation also means that potential customers are continually seeking more efficient, inherently safer, and demonstrably more environmentally friendly options that can enhance their operational capabilities.

Key categories of potential customers include governmental bodies and municipalities, which collectively represent a very significant and consistently growing segment of the market. These entities procure a wide array of specialty vehicles for the provision of essential public services, such as efficient waste collection and comprehensive sanitation programs, critical fire and rescue operations, indispensable emergency medical services, vital public works and infrastructure maintenance, and various essential utility services. Their procurement decisions are frequently influenced by stringent public tender processes, prevailing budgetary constraints, and the terms of long-term service contracts, alongside a rapidly increasing emphasis on adopting green technologies and fostering sustainable operational solutions. Construction companies, spanning the spectrum from large multinational enterprises undertaking mega-projects to smaller, localized contractors, constitute another absolutely major customer group. These companies heavily rely on a diverse fleet of vehicles, including high-capacity concrete mixers, versatile excavators, powerful cranes, and heavy-duty dump trucks, for an extensive myriad of building and critical infrastructure development projects. Their demand is directly correlated with the overall health and growth of the construction sector and global infrastructure spending, exhibiting a strong preference for exceptionally durable, high-capacity, and technologically advanced machinery capable of withstanding harsh operating conditions while significantly enhancing project efficiency and timelines.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 250.00 billion |

| Market Forecast in 2032 | USD 390.00 billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Key Companies Covered | Volvo Group, Daimler Truck AG, Oshkosh Corporation, Scania AB, PACCAR Inc., John Deere (Deere & Company), Caterpillar Inc., Kenworth Truck Company, Peterbilt Motors Company, Iveco S.p.A., Liebherr Group, CNH Industrial N.V., Sany Group, Zoomlion Heavy Industry Science and Technology Co. Ltd., XCMG Group, Terex Corporation, Komatsu Ltd., Hino Motors, Ltd., Foton Motor Group, BYD Company Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape within the Specialty Commercial Vehicle Market is currently undergoing a profound and dynamic transformation, propelled by continuous advancements strategically aimed at significantly enhancing overall performance, elevating safety standards, improving operational efficiency, and bolstering environmental sustainability initiatives. A primary and dominant focus remains on the widespread implementation of vehicle electrification, with leading manufacturers vigorously developing and integrating advanced electric and hybrid powertrains across a diverse spectrum of vehicle types, ranging from urban refuse trucks to heavy-duty construction equipment. This fundamental shift is robustly supported by groundbreaking innovations in high-density battery technology, the development of comprehensive charging infrastructure solutions, and sophisticated power management systems designed to enable extended operating ranges and remarkably faster recharging cycles. Concurrently, the pervasive integration of advanced telematics systems and the Internet of Things (IoT) is rapidly becoming a standard feature, facilitating real-time monitoring of critical vehicle performance metrics, precise fuel consumption tracking, granular driver behavior analysis, and proactive predictive maintenance scheduling. These integrated systems deliver invaluable data analytics, empowering fleet managers to optimize complex operations, significantly reduce operational costs, and markedly improve overall asset utilization, thus propelling the industry towards a more connected, intelligent, and data-driven fleet management ecosystem.

A specialty commercial vehicle is fundamentally designed and extensively equipped for specific tasks that extend beyond general transportation purposes. These vehicles often feature highly specialized bodies, customized equipment, and unique functionalities to perform critical duties across diverse sectors such as construction, emergency services, waste management, utilities, and other highly specialized industries. Common examples include fire trucks, ambulances, refuse collection vehicles, concrete mixers, and various types of cranes.

The primary growth drivers for this market include rapid global urbanization, significant and ongoing investments in infrastructure development worldwide, the exponential expansion of the e-commerce sector, the implementation of increasingly stringent environmental regulations pushing for cleaner vehicles, and continuous technological advancements aimed at improving operational efficiency, enhancing safety across various industry sectors, and reducing overall operational costs.

Technology plays an absolutely critical and transformative role in modern specialty vehicles, encompassing advanced telematics systems for comprehensive fleet management, seamless IoT integration for real-time data acquisition and analysis, Artificial Intelligence (AI) for predictive maintenance and optimized route planning, and sophisticated Advanced Driver-Assistance Systems (ADAS) for significantly enhanced safety. These innovations collectively boost operational efficiency, minimize costly downtime, and dramatically improve overall operational intelligence and safety for highly specialized tasks, leading to more productive and secure work environments.

The Asia Pacific (APAC) region, fueled by rapid urbanization and extensive infrastructure projects, presents the most significant growth opportunities. North America and Europe offer strong demand for technologically advanced, highly efficient, and environmentally compliant vehicles. Additionally, Latin America and the Middle East & Africa (MEA) regions are showing promising growth trajectories due to expanding mining activities, substantial construction projects, and ongoing urban development investments, making them key areas for future market expansion and strategic investment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.