ID : MRU_ 427786 | Date : Oct, 2025 | Pages : 245 | Region : Global | Publisher : MRU

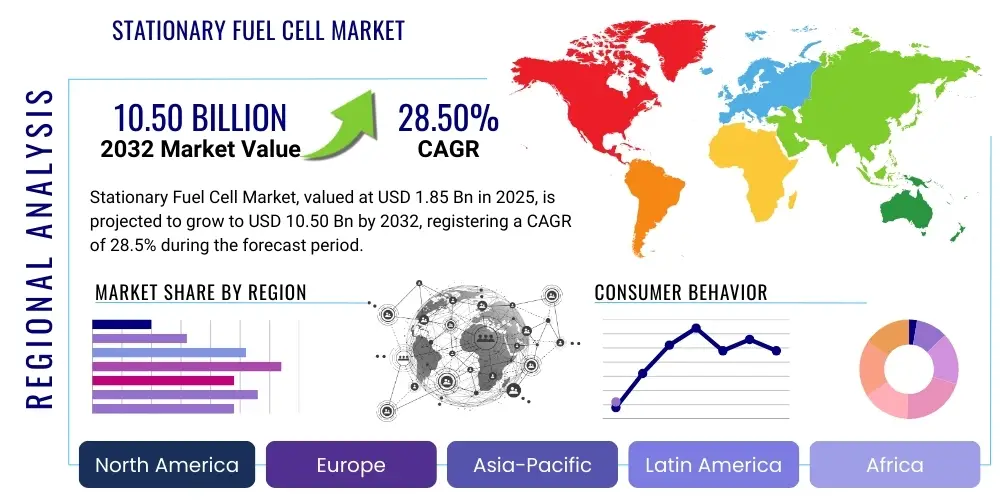

The Stationary Fuel Cell Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2032. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 10.50 Billion by the end of the forecast period in 2032.

The Stationary Fuel Cell Market is an emergent sector positioned at the forefront of the global transition towards sustainable and reliable energy solutions. These advanced electrochemical devices convert chemical energy from a fuel source, typically hydrogen, natural gas, or biogas, directly into electricity with exceptional efficiency and minimal environmental impact. Unlike traditional combustion engines, fuel cells produce electricity through an electrochemical reaction, leading to significantly lower or zero emissions, depending on the fuel used. This characteristic makes them a cornerstone technology for decarbonization efforts across various industries and applications, supporting both grid resilience and distributed power generation models.

Stationary fuel cells encompass a range of technologies, including Proton Exchange Membrane Fuel Cells (PEMFC), Solid Oxide Fuel Cells (SOFC), Phosphoric Acid Fuel Cells (PAFC), and Molten Carbonate Fuel Cells (MCFC, each optimized for specific operational conditions and power outputs. Their primary applications span from providing continuous prime power to critical infrastructure such as data centers, telecommunication towers, and commercial buildings, to offering reliable backup power solutions that ensure operational continuity during grid outages. Furthermore, they are increasingly vital for combined heat and power (CHP) systems, maximizing energy utilization by recovering waste heat for heating or cooling purposes, thereby enhancing overall system efficiency and economic viability.

The burgeoning adoption of stationary fuel cell technologies is primarily driven by an escalating global demand for clean energy, stringent environmental regulations pushing for reduced carbon footprints, and a persistent need for enhanced energy security and grid independence. Benefits such as high efficiency, reduced noise pollution, superior reliability, and the ability to operate independently from the main grid make them an attractive alternative to conventional power generation. Government incentives, along with significant advancements in materials science and manufacturing processes, are further catalyzing market expansion by improving system performance, reducing costs, and expanding the accessibility of hydrogen and other fuel sources.

The Stationary Fuel Cell Market is experiencing robust growth, propelled by a confluence of evolving business trends, distinct regional dynamics, and significant advancements across various technological segments. Businesses are increasingly prioritizing energy independence, operational resilience, and sustainability, leading to a surge in demand for fuel cell solutions in critical applications such as data centers, hospitals, and distributed power generation. Strategic partnerships, joint ventures, and heightened investment in research and development are hallmarks of the current market landscape, fostering innovation in fuel cell design, manufacturing scalability, and system integration. Companies are also focusing on developing fuel-flexible systems capable of utilizing a wider array of feedstocks, including biogas and reformed natural gas, to broaden market applicability and appeal to diverse end-users.

Regional trends reveal a varied but consistently upward trajectory for stationary fuel cell deployment. Asia-Pacific stands out as a dominant and rapidly expanding market, driven by ambitious government initiatives to promote hydrogen economy, rapid industrialization, and a substantial increase in electricity demand across countries like Japan, South Korea, and China. North America continues its strong growth, primarily fueled by significant policy support, tax incentives, and the increasing reliance on reliable backup power for its expansive data center infrastructure and telecommunications networks. Europe is making substantial strides, particularly with its green hydrogen strategies and carbon neutrality targets, which are fostering investment in fuel cell technologies for both grid support and decentralized energy systems, particularly in Germany, the UK, and Nordic countries.

Segmentation analysis highlights key areas of technological advancement and market penetration. Solid Oxide Fuel Cells (SOFC) are gaining prominence for their high efficiency in larger-scale power generation and Combined Heat and Power (CHP) applications, particularly where waste heat recovery is beneficial. Proton Exchange Membrane Fuel Cells (PEMFC) remain dominant in smaller power ranges and backup power solutions due to their quicker start-up times and lower operating temperatures. The market is also witnessing a shift towards integrated solutions that combine fuel cells with renewable energy sources like solar and wind, creating hybrid microgrid systems that offer unparalleled reliability and environmental benefits. Continuous innovation in catalyst materials, membrane technology, and power electronics is pivotal in reducing costs, enhancing durability, and improving the overall performance of these diverse fuel cell types, further solidifying their role in the future energy landscape.

The integration of Artificial Intelligence (AI) into the Stationary Fuel Cell Market is a transformative development, addressing common user questions related to efficiency, maintenance, and grid integration. Users are keen to understand how AI can optimize fuel cell performance, extend operational lifespans through predictive diagnostics, and enhance the seamless integration of fuel cell systems into smart grids and microgrids. Key themes revolve around AIs capacity to reduce operational costs, improve reliability, and accelerate the development cycle of new fuel cell technologies, ensuring they meet the evolving demands for sustainable and resilient energy infrastructure. The expectation is that AI will elevate fuel cells from high-potential technology to a cost-effective, highly reliable, and intelligently managed power source.

Users frequently inquire about AIs role in real-time system management, particularly concerning fuel optimization and load balancing in variable demand scenarios. There is significant interest in AIs ability to model complex electrochemical processes, facilitating the design of more efficient and durable fuel cell components and systems. Furthermore, concerns about the initial high capital expenditure of fuel cell installations lead to questions regarding how AI can contribute to cost reduction through optimized manufacturing processes and improved resource allocation. The market anticipates AI to be a critical enabler for predictive analytics, smart control systems, and data-driven material innovation, ultimately making stationary fuel cell solutions more competitive and accessible for a broader range of applications.

The Stationary Fuel Cell Market is primarily driven by an increasing global imperative to mitigate climate change, fostering a strong demand for clean energy alternatives that reduce carbon emissions and reliance on fossil fuels. Growing energy independence goals across nations, coupled with the critical need for resilient and decentralized power generation, further accelerate adoption, particularly in regions prone to grid instability or with evolving energy infrastructures. Robust governmental support in the form of subsidies, tax incentives, and regulatory frameworks aimed at promoting hydrogen infrastructure and renewable energy integration plays a pivotal role in creating a favorable market environment. Furthermore, the relentless rise in global electricity demand, especially from rapidly expanding data centers and industrial facilities, necessitates efficient and reliable power sources, a need perfectly addressed by stationary fuel cells.

Despite these strong drivers, the market faces significant restraints, including the relatively high initial capital expenditure associated with installing fuel cell systems compared to conventional power generation technologies. While operational costs are often lower over the long term, the upfront investment can deter potential adopters, particularly small and medium-sized enterprises. Another considerable challenge is the nascent stage of hydrogen infrastructure in many parts of the world, limiting the widespread availability of hydrogen fuel for fuel cell systems that operate on pure hydrogen. This often necessitates on-site fuel reforming or reliance on natural gas, which, while more readily available, still involves carbon emissions. Public perception and awareness, alongside concerns about the durability and long-term performance of certain fuel cell types, also represent hurdles that require continuous market education and technological advancements to overcome.

Opportunities for growth are vast and diverse, with significant potential in integrating stationary fuel cells with renewable energy sources to create robust and sustainable microgrids, particularly in remote or off-grid locations. The escalating demand for uninterrupted power in critical infrastructure like data centers, healthcare facilities, and telecommunication networks presents a substantial market niche for reliable backup and prime power solutions. Emerging economies, undergoing rapid urbanization and industrialization, offer fertile ground for decentralized power solutions that can bypass limitations of existing grid infrastructure. Continuous innovation in fuel cell technology, coupled with advancements in hydrogen production, storage, and distribution, are expected to drastically reduce costs and enhance performance, making stationary fuel cells more competitive and ubiquitous in the future energy landscape. These impact forces collectively shape the markets trajectory, emphasizing a push towards sustainability, resilience, and technological innovation as core elements of growth.

The Stationary Fuel Cell Market is extensively segmented by type, application, end-user, and fuel type, providing a granular understanding of its diverse landscape and growth trajectories. Each segmentation highlights distinct technological preferences and market demands, illustrating how different fuel cell chemistries and configurations are optimized for specific operational requirements, power outputs, and environmental considerations. This detailed breakdown enables stakeholders to identify niche opportunities and tailor solutions that best meet the varied needs of a global clientele. The interplay between these segments is crucial for strategic market positioning, driving innovation in areas such as efficiency, cost reduction, and fuel flexibility to address the broadest range of power generation challenges.

Market segmentation also reveals the predominant applications and end-users driving demand, ranging from critical backup power in the commercial sector to large-scale combined heat and power systems for industrial facilities. Understanding these segment-specific trends is vital for manufacturers and service providers to allocate resources effectively, develop targeted marketing strategies, and foster partnerships that leverage complementary strengths. As the market matures, the demand for modular, scalable, and grid-responsive fuel cell solutions is accelerating, prompting further innovation across all segments. This comprehensive analysis underpins strategic decisions aimed at expanding market share, mitigating risks, and capitalizing on the evolving landscape of sustainable energy generation worldwide.

The value chain for the Stationary Fuel Cell Market begins with upstream activities focused on the procurement and processing of raw materials essential for fuel cell components. This critical phase involves sourcing advanced materials such as platinum-group metals for catalysts, specialized polymers for membranes, ceramic materials for solid oxide fuel cells, and various metals and alloys for bipolar plates and balance of plant components. Suppliers in this segment are pivotal, as the quality and cost-effectiveness of these materials directly impact the performance, durability, and overall manufacturing cost of the final fuel cell system. Research and development in material science, focusing on reducing reliance on rare or expensive materials and enhancing component longevity, are continuous efforts at this initial stage of the value chain.

Moving downstream, the value chain progresses through the manufacturing of individual fuel cell stacks, system integration, and ultimately to the distribution and installation of complete stationary fuel cell units. Manufacturers assemble the intricate components into fuel cell stacks and then integrate these stacks with peripheral systems such as fuel reformers, power conditioning units, thermal management systems, and control electronics to create a fully functional power generation solution. The distribution channel plays a crucial role, encompassing both direct sales to large industrial customers, utilities, and government entities, and indirect sales through a network of distributors, resellers, and system integrators who cater to commercial, residential, and smaller-scale applications. Post-installation, the value chain extends to comprehensive after-sales services, including maintenance, repairs, and performance monitoring, ensuring the long-term reliability and efficiency of the deployed systems.

The Stationary Fuel Cell Market primarily targets a diverse range of end-users and buyers who prioritize reliable, efficient, and environmentally sustainable power solutions. Data center operators represent a significant segment, seeking uninterruptible power supplies (UPS) and prime power to maintain continuous operations, minimize downtime, and reduce their carbon footprint. Telecommunication companies are another key customer group, deploying fuel cells for backup power at remote cell towers and critical infrastructure where grid reliability is often compromised or access is limited. Both sectors benefit immensely from the high reliability and continuous operation capabilities of fuel cells, which significantly outperform traditional battery backups or diesel generators in terms of environmental impact and operational longevity.

Beyond critical infrastructure, commercial and industrial sectors form a substantial customer base. Commercial buildings, including hospitals, hotels, and large retail establishments, are increasingly adopting fuel cell-based combined heat and power (CHP) systems to simultaneously generate electricity and useful heat, thereby enhancing energy efficiency and reducing utility costs. Industrial facilities, such as manufacturing plants and chemical processing units, utilize fuel cells for robust prime power, energy security, and to comply with stringent environmental regulations. Furthermore, residential users in regions with high electricity costs or a desire for energy independence, particularly those interested in microgrid solutions or self-sufficiency, represent a growing niche. Utilities are exploring stationary fuel cells for distributed generation, grid stabilization, and peak shaving applications, aiming to improve grid resilience and incorporate more renewable energy sources into their portfolios.

The Stationary Fuel Cell Market is characterized by a dynamic and evolving technology landscape, primarily driven by continuous innovation across various fuel cell types, each offering distinct advantages for specific applications. Proton Exchange Membrane Fuel Cells (PEMFCs) are prominent for their relatively low operating temperatures, rapid start-up times, and high power density, making them suitable for smaller-scale backup power, residential, and light commercial applications. Ongoing research focuses on developing more durable membranes, reducing platinum catalyst loading, and enhancing overall system integration to lower costs and extend operational life. Solid Oxide Fuel Cells (SOFCs), conversely, operate at much higher temperatures, which allows for greater fuel flexibility, enabling them to run on natural gas, biogas, or even hydrogen, and are highly efficient for larger-scale prime power and Combined Heat and Power (CHP) applications due to their ability to efficiently utilize waste heat. Innovations in SOFC technology revolve around improved ceramic materials, enhanced stack designs, and integration with carbon capture technologies to further improve their environmental profile.

Other significant technologies within the stationary fuel cell market include Phosphoric Acid Fuel Cells (PAFCs) and Molten Carbonate Fuel Cells (MCFCs). PAFCs are known for their established commercial track record, robustness, and ability to use reformed natural gas, finding applications primarily in commercial and industrial settings requiring reliable, continuous power. Developments in PAFC technology concentrate on increasing power output, reducing system size, and improving electrode performance. MCFCs operate at high temperatures, similar to SOFCs, but utilize a molten carbonate electrolyte, making them adept at large-scale power generation and co-generation, especially in industrial environments where they can efficiently utilize fuels with impurities. The broader technological landscape is also marked by significant advancements in balance of plant components, including power electronics for efficient AC/DC conversion, sophisticated thermal management systems, and intelligent control algorithms. Furthermore, the development of integrated fuel reformers that can extract hydrogen from readily available hydrocarbons at the point of use is crucial for expanding the markets reach by overcoming current hydrogen infrastructure limitations.

Stationary fuel cells are electrochemical devices that convert the chemical energy of a fuel, typically hydrogen or natural gas, directly into electricity and heat through an electrochemical reaction, without combustion. This process results in high efficiency, minimal emissions, and quiet operation, making them an ideal clean energy solution for fixed installations.

Stationary fuel cells are primarily utilized for prime power generation, providing continuous electricity to commercial and industrial facilities, data centers, and telecommunication infrastructure. They are also widely used for reliable backup power, combined heat and power (CHP) systems, and supporting grid stability in microgrid applications, ensuring energy resilience and efficiency.

The market features several types of stationary fuel cells, including Proton Exchange Membrane Fuel Cells (PEMFC), Solid Oxide Fuel Cells (SOFC), Phosphoric Acid Fuel Cells (PAFC), and Molten Carbonate Fuel Cells (MCFC). Each type is characterized by different operating temperatures, fuel flexibility, and efficiencies, catering to specific power generation needs and scales.

Stationary fuel cells offer significant advantages over traditional generators, including remarkably lower or zero emissions, higher energy conversion efficiency, reduced noise levels, and enhanced operational reliability. They provide superior energy security, reduced reliance on grid infrastructure, and often lower long-term operating costs, contributing to environmental sustainability.

The stationary fuel cell market primarily faces challenges related to high initial capital costs compared to conventional power systems, the underdeveloped hydrogen infrastructure required for pure hydrogen fuel cells, and ongoing efforts to enhance the long-term durability and public awareness of the technology. Continued innovation and policy support are crucial for overcoming these hurdles.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.