ID : MRU_ 430769 | Date : Nov, 2025 | Pages : 245 | Region : Global | Publisher : MRU

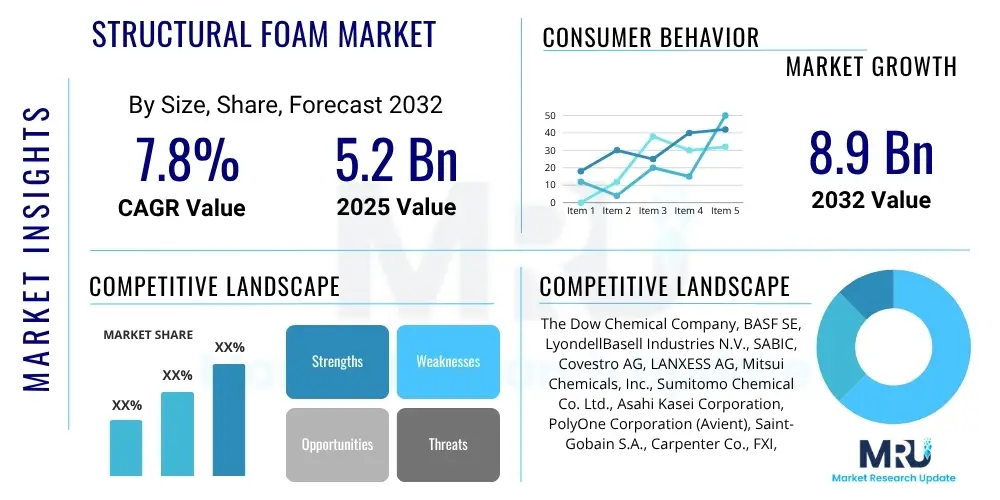

The Structural Foam Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at $5.2 Billion in 2025 and is projected to reach $8.9 Billion by the end of the forecast period in 2032. This growth trajectory is underpinned by a rising demand for lightweight, durable, and cost-effective materials across a multitude of industries, driven by global initiatives for energy efficiency and sustainable manufacturing. The intrinsic properties of structural foam, such as its high strength-to-weight ratio and excellent insulating capabilities, position it as a critical material solution for addressing contemporary industrial challenges.

The market expansion is not uniform across all segments; specific applications and geographical regions are expected to exhibit accelerated growth due to varying industrial development stages and regulatory environments. Innovations in polymer science and processing technologies are continually broadening the scope of structural foam applications, enhancing its performance characteristics, and reducing production costs. These advancements are instrumental in attracting new end-users and solidifying structural foam's position as a preferred material over traditional alternatives, particularly in sectors prioritizing material efficiency and environmental impact reduction.

Structural foam refers to a type of polymer material engineered with a cellular core and a solid integral skin, creating a lightweight yet rigid structure. This unique composition is achieved through specialized injection molding processes where a blowing agent is introduced into the polymer melt, forming gas bubbles within the material as it cools and solidifies. The resultant structure provides an exceptional strength-to-weight ratio, superior rigidity, and enhanced impact resistance compared to solid plastic parts of the same weight. This makes structural foam an ideal choice for applications where both material reduction and structural integrity are paramount, offering a balance of performance and economy.

The product description of structural foam encompasses a diverse range of polymers, including polypropylene (PP), high-density polyethylene (HDPE), polystyrene (PS), acrylonitrile butadiene styrene (ABS), and polycarbonate (PC), among others. The choice of polymer dictates the final mechanical, thermal, and chemical properties of the foam, allowing for tailored solutions to specific application requirements. Manufacturing processes like gas-assist injection molding and co-injection molding further refine the material's properties, enabling the creation of complex geometries with consistent quality and reduced material stress. The ability to customize density, cell structure, and skin thickness provides significant design flexibility, allowing engineers to optimize parts for performance, weight, and cost.

Structural foam finds major applications across a broad spectrum of industries. In the automotive sector, it is utilized for interior components, underbody shields, and cargo management systems due to its lightweighting capabilities, which contribute to fuel efficiency and reduced emissions. The construction industry benefits from its insulating properties and durability in applications such as door cores, wall panels, and decking. Material handling solutions like pallets and containers leverage its robustness and lightweight nature for improved logistics. Furthermore, structural foam is integral in consumer goods for furniture and sporting equipment, in electrical and electronics for casings and enclosures, and in marine applications for buoyancy and structural components. The inherent benefits of structural foam, including significant weight reduction, enhanced part stiffness, superior thermal and acoustic insulation, and cost-effectiveness through material savings and shorter cycle times, are key driving factors for its increasing adoption across these diverse end-use sectors, continuously pushing market growth.

The Structural Foam Market is experiencing robust growth, primarily driven by persistent demand for lightweight materials and advancements in processing technologies. Key business trends indicate a strong focus on sustainable solutions, with manufacturers investing in bio-based polymers and advanced recycling methods to meet evolving environmental regulations and consumer preferences. Companies are increasingly collaborating with end-users to develop customized structural foam solutions that offer optimized performance for specific applications, fostering innovation and market diversification. Furthermore, market consolidation activities, including mergers and acquisitions, are observed as companies seek to expand their product portfolios, technological capabilities, and geographical reach, aiming for greater economies of scale and competitive advantage within this dynamic landscape.

Regional trends highlight Asia Pacific (APAC) as the fastest-growing market, propelled by rapid industrialization, burgeoning automotive and construction sectors, and increasing disposable incomes in emerging economies like China, India, and Southeast Asian nations. North America and Europe, while mature markets, continue to demonstrate steady growth, largely driven by stringent fuel efficiency standards in the automotive industry, a strong emphasis on energy-efficient building materials, and continuous innovation in product design. Latin America and the Middle East & Africa are emerging as promising markets, with growing investments in infrastructure and manufacturing boosting the demand for lightweight and durable structural foam components, albeit from a smaller base.

Segment trends underscore the dominance of polypropylene (PP) and high-density polyethylene (HDPE) as preferred raw materials due to their excellent balance of properties and cost-effectiveness. The automotive sector remains a critical application area, benefiting from the lightweighting potential of structural foam for enhanced vehicle performance and reduced emissions. The material handling segment, encompassing pallets and containers, also shows significant momentum, driven by the need for durable, reusable, and lighter logistics solutions. Continued innovation in manufacturing processes, such as gas counter pressure and co-injection molding, is expanding the functional capabilities of structural foam, allowing for the creation of more complex parts with superior surface finishes and structural integrity, thereby unlocking new opportunities across various end-use industries.

Common user questions related to the impact of AI on the Structural Foam Market frequently revolve around how artificial intelligence can enhance material properties, optimize manufacturing processes, reduce waste, and accelerate product development cycles. Users are keen to understand AI's role in predictive maintenance for molding equipment, improving quality control through automated inspection, and enabling more complex and efficient design iterations for structural foam components. There is also significant interest in AI's potential to facilitate the adoption of sustainable practices, such as optimizing recycling processes and integrating bio-based materials more effectively. Overall, the key themes are about efficiency, innovation, quality, and sustainability, driven by AI's analytical and predictive capabilities.

The Structural Foam Market is significantly influenced by a dynamic interplay of driving forces, inherent restraints, promising opportunities, and broader impact forces. A primary driver is the accelerating global demand for lightweight materials across various industries, notably automotive, aerospace, and consumer goods, as these sectors strive for enhanced energy efficiency, reduced emissions, and improved performance. Structural foam's superior strength-to-weight ratio and design flexibility make it an ideal substitute for heavier traditional materials like metals and solid plastics, contributing to fuel economy in vehicles and easier handling in logistics. The cost-effectiveness derived from material savings and shorter cycle times in production also acts as a powerful incentive for its adoption. Furthermore, continuous advancements in polymer science and processing technologies are expanding the material's property window and application spectrum, enabling the creation of more sophisticated and higher-performing structural foam parts.

Despite its advantages, the market faces several notable restraints. High initial tooling costs associated with specialized injection molding equipment and complex mold designs can be a significant barrier to entry for smaller manufacturers and limit rapid scalability for custom projects. The limitations in high-temperature performance of many common structural foam polymers restrict their use in applications exposed to extreme thermal conditions. Furthermore, material compatibility issues, particularly when blending different polymers or incorporating fillers, can pose manufacturing challenges and impact final product quality. The competition from alternative lightweight materials such as advanced composites, magnesium alloys, and even other plastic molding techniques can also constrain market growth. Moreover, the perceived complexity of designing and manufacturing structural foam parts sometimes deters potential adopters who lack specialized expertise, requiring significant educational efforts from industry players.

Opportunities for market growth are abundant, particularly in the development and commercialization of bio-based and recycled structural foams, aligning with global sustainability initiatives and consumer preferences for eco-friendly products. The integration of additive manufacturing (3D printing) technologies for producing complex molds and prototypes offers avenues for faster innovation and reduced development costs, expanding design possibilities. Furthermore, expanding into new high-value applications such as specialized aerospace components, advanced medical devices, and intricate parts for renewable energy infrastructure represents significant growth potential. The ongoing research into smart foams with embedded sensors or self-healing properties also promises to unlock entirely new functional capabilities, creating premium market segments. Overall, the market's trajectory is shaped by the relentless pursuit of lighter, stronger, and more sustainable material solutions, making structural foam a pivotal technology in modern manufacturing.

The Structural Foam Market is comprehensively segmented based on various critical parameters, including raw material type, specific application, end-use industry, and the manufacturing process employed. This detailed segmentation allows for a nuanced understanding of market dynamics, identifying key growth drivers and competitive landscapes within each sub-segment. Analyzing these divisions provides insights into the preferences of different industries for particular material characteristics and processing methods, highlighting areas of strong demand and potential innovation. The diverse nature of structural foam allows it to cater to a wide array of industrial needs, from high-volume automotive parts to specialized electronic enclosures, each driven by unique performance and cost requirements.

The value chain for the Structural Foam Market is a complex ecosystem beginning with raw material sourcing and extending through manufacturing, distribution, and end-use application. Upstream analysis involves key players such as petrochemical companies and polymer manufacturers that supply the base resins, including polypropylene, polyethylene, polystyrene, and ABS. These suppliers are critical as the quality and cost of their virgin and recycled polymers directly influence the final product's performance and market competitiveness. Additionally, manufacturers of blowing agents, both chemical and physical, and suppliers of additives like colorants, UV stabilizers, and flame retardants, form essential components of the upstream segment, ensuring the desired properties and processability of the structural foam. Machinery manufacturers, specializing in high-tonnage injection molding machines and extrusion equipment capable of handling foaming processes, also constitute a vital upstream component, providing the technological infrastructure for production.

Midstream activities primarily encompass the structural foam manufacturers or molders themselves. These entities transform the raw polymers and additives into finished structural foam parts using specialized processing techniques such as gas-assist injection molding, co-injection molding, and various extrusion methods. This stage involves significant capital investment in machinery, tooling, and process expertise to achieve the distinctive cellular core and integral skin structure of structural foam. Downstream analysis focuses on the direct and indirect distribution channels that connect these manufacturers to the end-user industries. Direct distribution often involves large-volume sales to original equipment manufacturers (OEMs) in sectors like automotive, construction, and major appliance manufacturing, where customized parts and long-term supply agreements are common. This direct engagement allows for close collaboration in design and material specification, ensuring optimal integration of the structural foam components into the final products.

Indirect distribution channels typically involve a network of distributors, wholesalers, and specialized agents who cater to smaller businesses or diverse applications across various geographical regions. These intermediaries provide market reach, logistics, and often technical support to a broader customer base, enabling wider market penetration for structural foam products that might not require direct manufacturer interaction. The efficiency of both direct and indirect channels is crucial for the market's overall health, impacting product availability, pricing strategies, and customer service. The strong integration and collaboration among all players in this value chain—from resin suppliers and machinery providers to molders, distributors, and ultimately end-users—are essential for driving innovation, optimizing costs, and responding effectively to evolving market demands for lightweight, high-performance, and sustainable material solutions.

The potential customers for the Structural Foam Market span a wide array of industries, primarily comprising end-users or buyers who seek materials offering an optimal balance of lightweight properties, structural integrity, thermal insulation, and cost-effectiveness. These customers are typically original equipment manufacturers (OEMs), component fabricators, and product designers who are under constant pressure to innovate, reduce product weight, enhance performance, and comply with increasingly stringent regulatory standards. The automotive sector, for instance, represents a significant customer base, with vehicle manufacturers and their tier-1 suppliers continuously looking for solutions to decrease vehicle mass to improve fuel efficiency and reduce carbon emissions. Structural foam's ability to create rigid, lightweight parts makes it invaluable for interior trim, underbody components, and battery enclosures in electric vehicles, where weight savings directly translate into extended range and improved performance.

Beyond automotive, the building and construction industry serves as a substantial segment of potential customers, including developers, architects, and manufacturers of building materials. These buyers utilize structural foam for its excellent insulating properties and durability in applications such as door cores, wall panels, window frames, and modular construction elements. The material contributes to energy-efficient buildings and offers longevity in diverse environmental conditions. Furthermore, the material handling sector, encompassing companies that produce pallets, crates, containers, and various logistics equipment, forms another critical customer group. These customers prioritize structural foam for its high load-bearing capacity, resistance to moisture and chemicals, and lightweight nature, which simplifies transportation and improves operational efficiency in supply chains. The demand for reusable and sustainable material handling solutions further drives their interest in structural foam.

The electrical and electronics industry, including manufacturers of consumer electronics, industrial equipment, and telecommunication infrastructure, also represents a growing segment of potential customers. They rely on structural foam for durable, lightweight enclosures and housings that provide protection for sensitive components while also offering thermal management and design flexibility. Similarly, the consumer goods sector, including manufacturers of furniture, sporting goods, and lawn & garden equipment, values structural foam for its aesthetic versatility, ergonomic possibilities, and cost-effective production of complex shapes. Lastly, emerging applications in the marine industry for boat components and the medical sector for device housings are broadening the customer base, underscoring structural foam's adaptability and broad appeal across diverse, high-performance applications where material innovation is key to product success.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $5.2 Billion |

| Market Forecast in 2032 | $8.9 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | The Dow Chemical Company, BASF SE, LyondellBasell Industries N.V., SABIC, Covestro AG, LANXESS AG, Mitsui Chemicals, Inc., Sumitomo Chemical Co. Ltd., Asahi Kasei Corporation, PolyOne Corporation (Avient), Saint-Gobain S.A., Carpenter Co., FXI, Inc., Armacell International S.A., Rogers Corporation, Sekisui Chemical Co., Ltd., Recticel NV/SA, Wanhua Chemical Group Co., Ltd., Mitsubishi Chemical Corporation, Borealis AG. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The structural foam market is continuously evolving, driven by advancements in polymer science and processing technologies aimed at improving material properties, expanding application versatility, and enhancing manufacturing efficiency. A pivotal technology in this landscape is Gas-Assist Injection Molding (GAIM), which involves injecting an inert gas, typically nitrogen, into the polymer melt during the molding process. This technique creates hollow sections within the part, reducing material usage, part weight, and cycle times, while also minimizing sink marks and warpage. GAIM is particularly effective for large, thick-walled parts where uniform cooling and reduced internal stresses are crucial, providing superior dimensional stability and aesthetic quality for complex geometries without increasing part weight or cost excessively.

Another significant advancement is Co-injection Molding, also known as sandwich molding, which allows for the simultaneous injection of two or more different polymer melts into the same mold. In the context of structural foam, this often involves injecting a solid skin material and a foamed core material, or two different foamed materials. This technology enables the production of parts with varying material properties across their cross-section, such as a rigid, impact-resistant outer skin and a lightweight, insulating foamed core. Co-injection molding offers unparalleled design flexibility, allowing engineers to combine specific performance characteristics in a single component, optimize material usage, and create multi-functional parts that were previously unattainable with conventional molding techniques, thus pushing the boundaries of what structural foam can achieve.

Beyond molding processes, the development of advanced blowing agents and polymer formulations also plays a critical role. The shift towards more environmentally friendly physical blowing agents (e.g., CO2, nitrogen) over chemical blowing agents (CBAs) is gaining traction, driven by sustainability concerns and regulatory pressures. Furthermore, innovations in polymer compounding, including the incorporation of specialty additives, reinforcing fibers, and nano-fillers, are enhancing the mechanical, thermal, and electrical properties of structural foams. The integration of microcellular foaming techniques allows for even finer cell structures, leading to superior strength-to-weight ratios and improved surface finishes. These technological innovations collectively contribute to the expansion of structural foam into new, demanding applications and reinforce its position as a high-performance, versatile material solution for modern industrial needs, continually driving market growth and product differentiation.

Structural foam is a specialized polymer material characterized by a cellular core and a solid integral skin, providing a high strength-to-weight ratio. Unlike traditional solid plastics, structural foam achieves significant weight reduction while maintaining or enhancing stiffness and impact resistance due to its internal foamed structure, making it ideal for lightweighting applications.

The primary benefits of structural foam include exceptional weight reduction, improved stiffness and rigidity, enhanced thermal and acoustic insulation properties, and significant cost savings through material efficiency and faster production cycles. Its design flexibility also allows for complex geometries and integrated features, optimizing part consolidation.

The automotive industry is a leading consumer, utilizing structural foam for lightweighting vehicles to improve fuel efficiency. Other major industries include building and construction for insulation and durable components, material handling for pallets and containers, and electrical and electronics for protective housings and enclosures.

Common manufacturing processes for structural foam include Gas-Assist Injection Molding (GAIM), which introduces inert gas into the melt to create hollow sections, and Co-injection Molding, which simultaneously injects different materials to form a solid skin and a foamed core. Traditional injection molding with chemical or physical blowing agents is also widely used.

The market outlook for structural foam is positive, driven by increasing demand for lightweight and energy-efficient materials. Sustainability trends are particularly influential, fostering innovation in bio-based and recycled structural foams, which are expected to drive significant growth and adoption across various eco-conscious industries in the coming years.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.