ID : MRU_ 428200 | Date : Oct, 2025 | Pages : 249 | Region : Global | Publisher : MRU

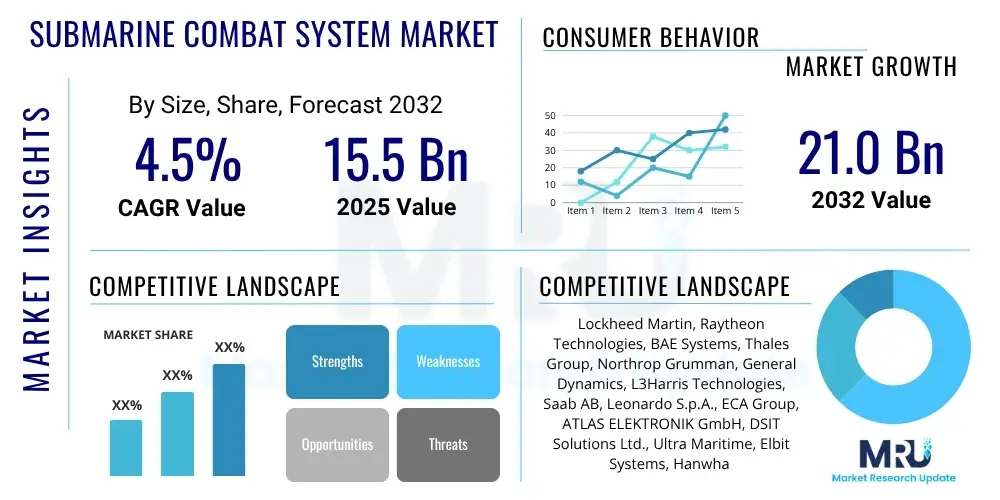

The Submarine Combat System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2032. The market is estimated at USD 15.5 Billion in 2025 and is projected to reach USD 21.0 Billion by the end of the forecast period in 2032.

The Submarine Combat System (SCS) market encompasses the sophisticated suite of integrated technologies and operational capabilities essential for modern undersea warfare. These systems are crucial for submarines to perform a wide array of missions, from anti-submarine warfare (ASW) and anti-surface warfare (ASuW) to intelligence, surveillance, and reconnaissance (ISR) and covert special operations. The inherent strategic value of submarines, coupled with their unique ability to operate covertly for extended periods, places a premium on highly advanced and reliable combat systems that can detect, track, engage, and evade threats effectively in complex maritime environments.

At its core, an SCS integrates various sensors, weapon systems, navigation aids, and communication networks into a unified operational framework. Key components typically include advanced sonar systems for acoustic detection, radar and electronic support measures (ESM) for surface and air threat detection, and sophisticated weapon control systems for torpedoes, missiles, and mines. The product description emphasizes the modularity and adaptability of these systems, allowing for seamless integration into diverse submarine platforms, ranging from conventional diesel-electric (SSK) to nuclear-powered attack (SSN) and ballistic missile (SSBN) submarines. These systems are designed to provide submarine crews with superior situational awareness, enabling rapid and informed decision-making under high-pressure conditions.

The major applications of Submarine Combat Systems primarily revolve around enhancing a nation's naval defense capabilities and projecting power covertly. Benefits derived from these advanced systems include improved stealth and survivability, enhanced target acquisition and tracking precision, superior command and control functionality, and greater operational efficiency. Key driving factors propelling market growth include escalating geopolitical tensions, the imperative for naval modernization programs across various countries, the continuous evolution of maritime security threats, and significant technological advancements, particularly in areas like artificial intelligence, sensor technology, and data fusion, which promise to further revolutionize undersea combat capabilities.

The Submarine Combat System market is characterized by robust growth driven by a confluence of geopolitical shifts and rapid technological innovation, directly impacting business trends. Leading defense contractors are increasingly focusing on strategic mergers, acquisitions, and collaborations to consolidate market share and leverage synergistic capabilities, particularly in sensor technology, artificial intelligence, and cybersecurity solutions. There is a discernible trend towards modular and open architecture systems, facilitating easier upgrades and integration of new technologies, thereby extending the operational lifespan of expensive submarine platforms. Furthermore, investments in research and development are concentrated on enhancing stealth, improving autonomous capabilities, and developing robust decision support systems, reflecting the complex demands of modern undersea warfare and the imperative for superior operational performance and resilience against evolving threats.

Regional trends indicate significant dynamism, with the Asia-Pacific region emerging as a dominant force in market expansion, propelled by extensive naval modernization programs in nations such as China, India, and Australia, all of whom are investing heavily in new submarine fleets and associated combat systems to address regional maritime security challenges. North America continues to be a hub for innovation, leading in advanced research, development, and deployment of cutting-edge technologies for next-generation combat systems, driven by substantial defense budgets and a strategic focus on maintaining technological superiority. European nations are also actively upgrading their existing submarine fleets and investing in new platforms, often through collaborative defense initiatives aimed at sharing costs and expertise, with an emphasis on integrated, multi-mission capabilities.

Segment trends within the SCS market highlight a strong shift towards highly integrated systems that combine diverse sensor inputs for comprehensive situational awareness and enable sophisticated weapon control. The software component, including advanced algorithms for data fusion, artificial intelligence, and machine learning, is experiencing particularly rapid growth as it becomes central to enhancing system intelligence and decision-making capabilities. Furthermore, there is an increasing demand for predictive maintenance solutions and extensive training services, ensuring the optimal performance and readiness of these highly complex systems throughout their operational lifecycle. These trends collectively underscore the market's trajectory towards more autonomous, intelligent, and interconnected submarine combat solutions capable of operating effectively in increasingly challenging and contested undersea environments.

User inquiries concerning AI's influence on the Submarine Combat System Market frequently center on its potential to revolutionize sensor data processing, automate complex tasks, enhance decision-making under duress, and its implications for cybersecurity and ethical autonomous operations. Users express interest in how AI can improve target detection and classification, manage vast amounts of real-time data, and provide predictive insights for maintenance or tactical maneuvering. There are also notable concerns regarding the reliability of AI in critical combat scenarios, the potential for autonomous systems to make decisions without human oversight, and the imperative for robust cybersecurity measures to protect AI-driven systems from sophisticated cyberattacks. These questions collectively underscore a dual perspective: immense anticipation for AI's operational benefits alongside a cautious approach towards its integration challenges and ethical ramifications within highly sensitive defense applications.

The Submarine Combat System market is significantly shaped by a dynamic interplay of drivers, restraints, and opportunities, underpinned by potent impact forces. Key drivers include escalating geopolitical tensions worldwide, leading nations to prioritize maritime security and undersea deterrence. This translates into substantial naval modernization programs, with significant investments in new submarine platforms and advanced combat systems to replace aging fleets or enhance existing capabilities. Furthermore, relentless technological advancements, particularly in areas such as artificial intelligence, quantum sensing, and acoustic stealth, continuously push the boundaries of what is possible in undersea warfare, fostering demand for cutting-edge solutions that provide a decisive operational advantage. The growing importance of undersea warfare, both for intelligence gathering and power projection, solidifies the strategic imperative for state-of-the-art combat systems.

Conversely, several formidable restraints temper market growth. The exceptionally high research and development (R&D) costs associated with developing complex and specialized combat systems, combined with extremely long procurement cycles that can span decades from concept to deployment, create significant financial and temporal barriers. Stringent regulatory compliance and certification processes, necessitated by the critical nature of defense technologies, add further layers of complexity and cost. Moreover, cybersecurity vulnerabilities pose a persistent and evolving threat, requiring continuous investment in robust protection measures against sophisticated state-sponsored attacks. The specialized nature of this field also contributes to a global shortage of skilled engineers and technical personnel, presenting a human capital constraint on innovation and deployment.

Despite these challenges, substantial opportunities exist for market expansion and innovation. The continuous integration of emerging technologies, such as advanced sensor fusion, autonomous control systems, and enhanced data analytics, promises to unlock new operational paradigms and performance levels. A growing focus on autonomous and unmanned underwater vehicles (UUVs) presents a burgeoning segment for combat system integration, extending reach and reducing risk to human operators. Furthermore, there is considerable export potential to developing navies seeking to establish or bolster their undersea capabilities, often through strategic partnerships and technology transfers. Opportunities also arise from the ongoing need for upgrades and refits to existing submarine fleets, allowing for the integration of modern combat system elements without the prohibitive cost of entirely new platform construction, thereby extending fleet relevance and operational effectiveness.

The Submarine Combat System (SCS) market is meticulously segmented to reflect the diverse operational needs, technological configurations, and platform specificities inherent to modern undersea warfare. This comprehensive segmentation allows for a granular understanding of market dynamics, identifying key areas of demand, technological innovation, and competitive intensity across various facets of submarine capabilities. The market is typically broken down by system type, which differentiates the primary functions such as detection, electronic warfare, and command, by platform type, acknowledging the distinct requirements of different submarine classes, by component, dissecting the hardware and software elements, and by end-user, identifying the primary customers for these advanced technologies.

The value chain for the Submarine Combat System market is characterized by a highly specialized and interconnected network of participants, reflecting the complexity and strategic importance of these defense technologies. The upstream segment primarily involves foundational technology and component providers. This includes manufacturers of highly specialized raw materials, advanced semiconductors, optical components, acoustic transducers, and other sophisticated sensor technologies. Furthermore, specialized software developers providing core algorithms for signal processing, data fusion, and artificial intelligence play a critical role. Research institutions and defense technology incubators also contribute significantly to the early-stage innovation and development of next-generation capabilities, providing the intellectual and technological bedrock upon which combat systems are built.

The downstream segment of the value chain is dominated by system integrators, prime defense contractors, and naval shipyards. These entities are responsible for integrating a myriad of individual components and subsystems into a coherent, functional submarine combat system. This involves extensive engineering, design, and customization to meet specific platform requirements and national defense specifications. Testing and certification bodies also form a crucial part of this segment, ensuring that the integrated systems meet stringent performance, safety, and regulatory standards before deployment. The interplay between these major players, often through intricate subcontracting and partnership agreements, is fundamental to delivering a fully operational and reliable combat system to the end-user.

Distribution channels in the Submarine Combat System market are almost exclusively direct, driven by the highly sensitive, proprietary, and strategic nature of defense procurement. Sales are typically executed through direct government-to-business (G2B) contracts between national defense ministries or naval procurement agencies and prime contractors. These contracts are often multi-year, high-value agreements that include provisions for initial system delivery, long-term maintenance, training, and subsequent upgrades. Strategic partnerships, often involving technology licensing or joint ventures between international defense companies, serve as an indirect but critical mechanism for market access, especially in regions where local content requirements or specific political considerations are paramount. This direct-to-customer model ensures stringent oversight, security, and customization tailored precisely to national defense doctrines and operational environments.

The primary and most significant potential customers for the Submarine Combat System market are unequivocally national navies across the globe. These include the naval forces of major global powers with established submarine fleets, such as the United States, Russia, China, France, the United Kingdom, and India, all of whom consistently invest in advanced combat systems for their nuclear-powered and conventional submarines. These sophisticated end-users demand cutting-edge technology, superior performance, and robust reliability to maintain a strategic advantage in undersea warfare, driving innovation and substantial procurement budgets. Their requirements often involve customized solutions, seamless integration with existing platforms, and comprehensive lifecycle support.

Beyond the leading naval powers, a substantial and growing segment of potential customers comprises emerging maritime nations and those undergoing naval modernization. Countries in the Asia-Pacific region, for instance, including Australia, South Korea, Japan, and other Southeast Asian nations, are actively expanding or upgrading their submarine capabilities due to increasing maritime security concerns and geopolitical dynamics. These nations seek modern combat systems to enhance their deterrence capabilities, protect critical sea lanes, and project regional influence. Their procurement decisions are often influenced by a balance of cost-effectiveness, technology transfer opportunities, and strategic alliances with established defense suppliers.

Ultimately, the end-users and buyers of Submarine Combat Systems are governmental entities, specifically defense ministries, naval procurement agencies, and submarine fleet operators. These entities are responsible for defining operational requirements, managing defense budgets, and overseeing the acquisition, deployment, and sustainment of their nation's submarine assets. The purchasing process is highly complex, involving extensive technical evaluations, competitive bidding, and inter-governmental agreements, underscoring the strategic and long-term nature of these investments. While the core customer base remains sovereign navies, the varied stages of their fleet development and the evolving threat landscape ensure a continuous and diversified demand for advanced submarine combat system solutions globally.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 15.5 Billion |

| Market Forecast in 2032 | USD 21.0 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin, Raytheon Technologies, BAE Systems, Thales Group, Northrop Grumman, General Dynamics, L3Harris Technologies, Saab AB, Leonardo S.p.A., ECA Group, ATLAS ELEKTRONIK GmbH, DSIT Solutions Ltd., Ultra Maritime, Elbit Systems, Hanwha Systems, Kongsberg Gruppen, Honeywell International, Rafael Advanced Defense Systems, Damen Naval, Naval Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Submarine Combat System market is characterized by a rapidly evolving technological landscape, continuously integrating state-of-the-art innovations to enhance performance and survivability in the complex undersea domain. At the forefront are advancements in sensor fusion and big data analytics, which allow for the seamless integration and interpretation of vast quantities of data from diverse acoustic, optical, and electromagnetic sensors. This multi-modal data processing provides a more comprehensive and accurate real-time picture of the operational environment, significantly improving target detection, classification, and tracking capabilities. The ability to sift through noise and discern subtle signatures is critical for maintaining stealth and operational effectiveness against increasingly sophisticated adversaries.

Artificial Intelligence (AI) and Machine Learning (ML) are profoundly impacting the market by transforming decision support, automation, and predictive capabilities. AI algorithms are deployed for intelligent threat assessment, optimizing tactical maneuvers, and enhancing autonomous control systems for certain functions, thereby reducing human workload and reaction times. Furthermore, predictive maintenance powered by ML ensures higher system availability and reduces lifecycle costs by anticipating equipment failures. Quantum sensing technologies, though still emerging, hold immense promise for revolutionizing detection capabilities, potentially offering unprecedented levels of sensitivity for detecting faint magnetic or gravitational anomalies, thereby enhancing stealth and counter-detection measures for future submarine fleets.

Beyond sensing and processing, key technological developments include advancements in stealth technologies to minimize acoustic, magnetic, and thermal signatures, making submarines harder to detect. Secure communication networks, including advanced underwater acoustic communications and satellite links with robust encryption, are vital for maintaining connectivity and data integrity without compromising covert operations. The adoption of Modular Open System Architectures (MOSA) is gaining traction, promoting interoperability, scalability, and ease of upgrades for combat systems, moving away from proprietary closed systems. Additionally, virtual and augmented reality applications are increasingly being utilized for advanced training and simulation, allowing crews to experience highly realistic scenarios and refine their skills in a safe and controlled environment, preparing them for the demands of modern undersea combat.

The market is primarily driven by escalating geopolitical tensions, global naval modernization programs, continuous technological advancements in areas like AI and quantum sensing, and the increasing strategic importance of undersea warfare for deterrence and intelligence.

AI is significantly impacting SCS by enhancing sensor data fusion, enabling predictive maintenance, improving autonomous navigation support, facilitating intelligent threat assessment and classification, and providing advanced decision support for critical tactical operations.

The Asia Pacific (APAC) region is demonstrating the fastest growth due to extensive naval expansion and modernization efforts, followed by North America which leads in R&D and advanced system deployment, and Europe with its focus on upgrades and collaborative defense initiatives.

Key technological advancements include advanced sensor fusion and big data analytics, the integration of AI/ML for enhanced decision-making, the exploration of quantum sensing, development of sophisticated stealth technologies, and the adoption of modular open system architectures (MOSA) for greater flexibility and upgradeability.

Major challenges include exceptionally high research and development costs, protracted procurement cycles, stringent regulatory compliance, the persistent threat of cybersecurity vulnerabilities, and a global shortage of highly skilled technical personnel specialized in this domain.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.