ID : MRU_ 428033 | Date : Oct, 2025 | Pages : 257 | Region : Global | Publisher : MRU

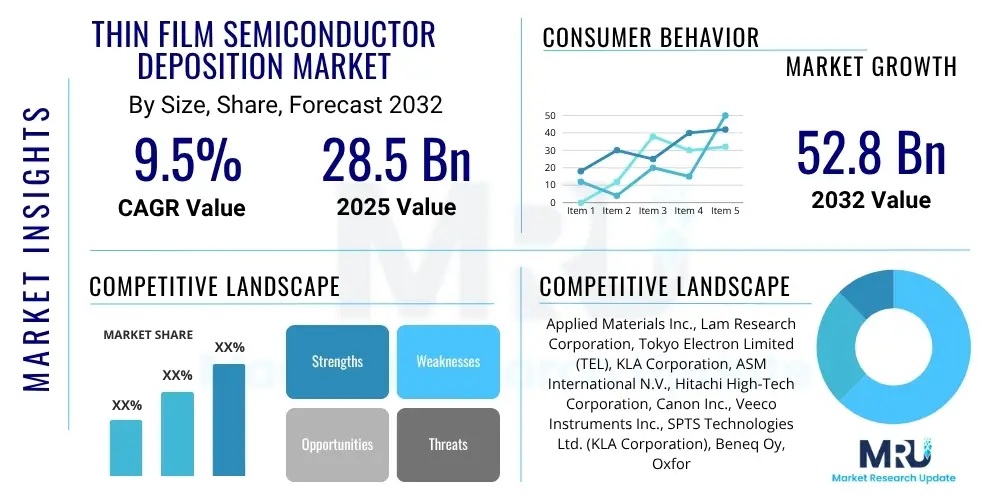

The Thin Film Semiconductor Deposition Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032. The market is estimated at USD 28.5 billion in 2025 and is projected to reach USD 52.8 billion by the end of the forecast period in 2032.

The Thin Film Semiconductor Deposition Market encompasses the specialized processes and equipment used to lay down extremely thin layers of material onto a substrate, typically for the manufacturing of semiconductor devices. These films, ranging from a few nanometers to several micrometers in thickness, are fundamental to creating the intricate structures that enable modern electronics. The precise control over material composition, thickness, and morphology afforded by these techniques is critical for enhancing device performance, miniaturization, and functionality across a myriad of applications, from integrated circuits to advanced sensors.

The core processes involved include Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), and Atomic Layer Deposition (ALD), each offering distinct advantages in terms of film quality, uniformity, conformality, and material compatibility. These deposition methods are extensively employed to form conductive, insulating, and semiconducting layers that are vital for transistor gates, interconnects, dielectrics, and other critical components. The market's robust growth is fueled by an escalating demand for high-performance, compact, and energy-efficient electronic devices, which continually push the boundaries of materials science and manufacturing precision.

Major applications span the entire electronics industry, including advanced logic and memory chips, optoelectronics like LEDs and solar cells, flat panel displays, and various micro-electromechanical systems (MEMS). The benefits derived from thin film deposition are manifold, including improved electrical conductivity, enhanced optical properties, superior mechanical strength, and effective barrier protection. The primary driving factors for this market's expansion are the relentless pursuit of device miniaturization, the proliferation of the Internet of Things (IoT), the emergence of 5G technology, the increasing complexity of artificial intelligence (AI) hardware, and the growing automotive electronics sector, all of which demand increasingly sophisticated and reliable thin film solutions.

The Thin Film Semiconductor Deposition Market is poised for substantial expansion, driven by continuous innovation in semiconductor technology and the pervasive digitalization across industries. Current business trends indicate a strong focus on research and development into novel deposition materials and techniques, aimed at achieving ultra-low power consumption, higher processing speeds, and greater integration density. There is a discernible shift towards advanced packaging solutions and heterogeneous integration, necessitating more sophisticated and precise deposition capabilities. Furthermore, market players are increasingly investing in automation and smart manufacturing processes, including the integration of AI and machine learning, to enhance efficiency, reduce costs, and accelerate development cycles. Mergers and acquisitions remain a strategic tool for consolidating market share and expanding technological portfolios, especially in specialized areas such as ALD and epitaxial growth.

Regional trends highlight Asia Pacific as the undeniable powerhouse of the thin film semiconductor deposition market, predominantly due to the region's colossal semiconductor manufacturing infrastructure, particularly in countries like Taiwan, South Korea, China, and Japan. This dominance is further cemented by the high concentration of integrated device manufacturers (IDMs) and pure-play foundries that are constantly expanding their production capacities. North America and Europe, while representing smaller manufacturing footprints, remain critical hubs for advanced research and development, equipment innovation, and high-value, specialized applications, particularly in defense, aerospace, and high-performance computing. Emerging markets in Southeast Asia are also gradually increasing their participation in the semiconductor supply chain, attracting new investments in fabrication facilities.

Segmentation trends reveal dynamic shifts across various deposition technologies and applications. Physical Vapor Deposition (PVD) continues to hold a significant market share, largely owing to its versatility and cost-effectiveness for a broad range of metallic and dielectric films. However, Chemical Vapor Deposition (CVD), particularly plasma-enhanced CVD (PECVD), is experiencing robust growth due to its superior conformality and ability to deposit complex dielectric films at lower temperatures, which is crucial for advanced node manufacturing. Atomic Layer Deposition (ALD) is emerging as a critical technology for ultra-thin, highly conformal films with atomic-level precision, finding increasing traction in next-generation memory, logic, and gate stack applications. The application segment for advanced packaging, MEMS, and optical coatings is projected to exhibit the highest growth rates, reflecting the industry's drive towards higher integration, enhanced functionality, and diverse device architectures.

The integration of Artificial Intelligence (AI) is set to revolutionize the Thin Film Semiconductor Deposition Market by addressing some of its most complex challenges, from process control and optimization to material discovery and defect reduction. Users are keenly interested in how AI can enhance the precision and repeatability of deposition processes, particularly for sub-nanometer film thicknesses and intricate 3D structures. Common questions revolve around AI's capability to predict and prevent process variations, optimize recipes for new materials, and accelerate the characterization and qualification of deposited films. There's also significant curiosity about AI's role in predictive maintenance for highly complex deposition equipment, reducing downtime, and improving overall operational efficiency.

The key themes emerging from user inquiries underscore AI's potential to drive efficiency, innovation, and cost savings. Expectations are high for AI to autonomously adapt process parameters in real-time based on in-situ sensor data, moving beyond traditional statistical process control to truly adaptive manufacturing. Users also anticipate that AI will facilitate the rapid screening and optimization of novel materials and precursor chemistries, significantly shortening the materials development cycle. Furthermore, the ability of AI to analyze vast datasets from past deposition runs for pattern recognition and anomaly detection is expected to lead to substantial improvements in yield rates and film quality, directly impacting the profitability and competitiveness of semiconductor manufacturers.

In essence, the overarching user sentiment reflects a strong belief that AI will transform thin film deposition from an expert-driven, empirical science into a more data-driven, intelligent, and autonomous process. This transition is expected to unlock unprecedented levels of precision, speed, and cost-efficiency, enabling the fabrication of next-generation semiconductor devices that are smaller, faster, and more powerful than ever before. The impact will extend across the entire value chain, from equipment design and manufacturing to actual film deposition and post-processing, creating a more resilient and innovative ecosystem.

The Thin Film Semiconductor Deposition Market is shaped by a confluence of powerful drivers, inherent restraints, promising opportunities, and dynamic impact forces. The primary drivers fueling market expansion include the incessant demand for smaller, faster, and more power-efficient electronic devices, which necessitates ever-more precise and complex thin film structures. The proliferation of advanced technologies like the Internet of Things (IoT), artificial intelligence (AI), 5G networks, and autonomous vehicles is creating a massive demand for high-performance semiconductor components, each requiring sophisticated thin film processes. Furthermore, the continuous advancements in advanced packaging technologies, such as 3D integration and fan-out wafer-level packaging, depend heavily on cutting-edge deposition techniques for interconnections and insulation. The growing adoption of renewable energy technologies, particularly solar photovoltaics, and the expansion of data centers globally also contribute significantly to the demand for thin film deposition solutions.

Despite the robust growth prospects, the market faces several notable restraints. The exceptionally high capital expenditure required for advanced deposition equipment and fab construction poses a significant barrier to entry for new players and limits the rapid expansion of existing ones. The inherent complexity of thin film processes, requiring highly specialized expertise in materials science, vacuum technology, and plasma physics, leads to a shortage of skilled labor. Environmental regulations regarding the handling of hazardous precursor gases and the disposal of byproducts present ongoing challenges for manufacturers, necessitating continuous investment in abatement technologies and sustainable practices. Moreover, the vulnerability of the semiconductor supply chain to geopolitical tensions, trade disputes, and unforeseen global events can disrupt the availability of critical materials and components, leading to production delays and increased costs.

Opportunities within the market are abundant and diverse. The development of novel materials, such as 2D materials (e.g., graphene, MoS2) and advanced compound semiconductors, opens new avenues for innovative thin film applications in next-generation devices. The rise of flexible electronics, wearable devices, and biomedical sensors presents unique demands for low-temperature, highly conformal, and biocompatible thin films. Expanding into emerging markets, particularly in regions that are building their domestic semiconductor manufacturing capabilities, offers significant growth potential. Furthermore, the continuous drive for higher integration and miniaturization fosters opportunities for new deposition techniques like area-selective ALD and advanced epitaxial growth, which promise unprecedented control at the atomic level. The increasing focus on energy efficiency also drives demand for thin films in power electronics and advanced battery technologies.

The market is also influenced by several impact forces that can significantly alter its trajectory. Economic shifts, including global recessions or periods of rapid growth, directly affect investment in semiconductor manufacturing capacity and consumer electronics demand. Geopolitical dynamics, such as trade policies, technology export controls, and regional conflicts, can disrupt supply chains, influence manufacturing locations, and impact R&D collaborations. Rapid technological breakthroughs, particularly in material science, AI, and quantum computing, can create entirely new markets or render existing technologies obsolete, necessitating swift adaptation. Finally, societal trends, such as the increasing demand for sustainable manufacturing and the shift towards a more connected world (e.g., smart cities, remote work), drive specific requirements for thin film solutions that are both high-performance and environmentally responsible. Resilience in supply chains and strategic partnerships are becoming increasingly critical for navigating these complex impact forces.

The Thin Film Semiconductor Deposition Market is meticulously segmented based on various critical parameters, reflecting the diverse technologies, materials, applications, and end-use industries that define this intricate ecosystem. This comprehensive segmentation allows for a granular understanding of market dynamics, identifying specific growth opportunities and challenges across different facets of the industry. The primary segments include the type of deposition technology, the materials being deposited, the specific application areas for the thin films, and the end-use industries that utilize these semiconductor devices. Each segment plays a crucial role in the overall market structure, with interdependencies driving innovation and competition.

The technological segmentation is particularly vital, as each deposition method offers unique advantages in terms of film properties, process control, and cost-effectiveness. The evolution of these technologies, from mature PVD techniques to advanced ALD processes, directly correlates with the increasing demands for precision and performance in semiconductor manufacturing. Material segmentation highlights the vast array of substances utilized, ranging from elemental silicon and various metals to complex dielectric compounds and advanced compound semiconductors, each serving distinct functional purposes within electronic devices. Application-based segmentation provides insight into where thin films create the most value, such as in logic, memory, displays, or solar cells, while end-use industry segmentation showcases the broader economic sectors that are underpinned by thin film technology.

Understanding these segments and their interconnections is paramount for market players to develop targeted strategies, optimize their product portfolios, and allocate resources effectively. The rapid pace of technological innovation within the semiconductor industry means that these segmentations are not static; rather, they are constantly evolving with the introduction of new materials, more advanced deposition techniques, and the emergence of novel applications and end-use cases. Analyzing these segments provides a roadmap for future growth and investment, highlighting areas with high potential and those facing saturation or disruption.

The value chain for the Thin Film Semiconductor Deposition Market is a complex and highly specialized ecosystem, commencing with the foundational raw material suppliers and extending through to the sophisticated end-user applications. At the upstream segment, this chain involves companies that provide the critical inputs necessary for deposition processes. These include manufacturers of high-purity precursor gases, sputtering targets made from various metals and alloys, and specialized chemicals vital for both PVD and CVD techniques. Additionally, suppliers of ultra-pure water, specialty chemicals for cleaning and etching, and high-vacuum components also form part of this crucial initial stage. The quality and purity of these raw materials directly impact the integrity and performance of the deposited thin films, making this segment foundational to the entire value chain.

Moving further along the value chain, the core of the market lies with the equipment manufacturers who design, develop, and produce the highly advanced deposition systems. These systems, whether PVD, CVD, ALD, or epitaxial reactors, are technological marvels incorporating vacuum technology, plasma generation, gas delivery systems, and sophisticated control software. These manufacturers often work closely with semiconductor fabs to customize equipment for specific process requirements and technological nodes. Following the equipment, the actual thin film deposition takes place at integrated device manufacturers (IDMs), pure-play foundries, or specialized contract manufacturers. These entities perform the intricate deposition processes on semiconductor wafers, creating the foundational layers for integrated circuits, memory chips, and other electronic components. They represent the primary "manufacturing" stage where value is added through precision processing.

The downstream segment of the value chain includes companies involved in subsequent processing steps such as lithography, etching, and packaging, ultimately leading to the production of finished semiconductor devices. These devices are then sold to various original equipment manufacturers (OEMs) who integrate them into final products such as smartphones, computers, automotive electronics, and medical devices. The distribution channel for thin film deposition equipment and related services often involves direct sales from major manufacturers to large semiconductor fabs, given the high capital cost and technical complexity. For consumables and spare parts, a network of specialized distributors and service providers ensures timely delivery and technical support. Both direct and indirect channels play vital roles, with direct channels dominating high-value equipment sales and indirect channels providing broader reach for maintenance, parts, and smaller-scale operations, ensuring comprehensive market coverage and support across the globe.

The Thin Film Semiconductor Deposition Market serves a broad spectrum of highly technical and demanding potential customers, primarily comprised of entities at various stages of semiconductor manufacturing and advanced electronics production. These end-users or buyers are characterized by their need for precise, repeatable, and high-quality thin film layers to enable the functionality, performance, and reliability of their sophisticated devices. The ongoing drive towards miniaturization, increased computational power, and energy efficiency across numerous industries directly translates into a constant demand for advanced thin film deposition solutions from these key customer segments.

At the forefront are Integrated Device Manufacturers (IDMs) and pure-play Foundries, which form the backbone of the semiconductor industry. IDMs like Intel and Samsung, who design and manufacture their own chips, and foundries such as TSMC and GlobalFoundries, who produce chips for fabless companies, are continuous and significant consumers of thin film deposition equipment and precursor materials. Their relentless pursuit of next-generation process nodes and advanced packaging technologies directly dictates the demand for the latest and most sophisticated deposition systems. These customers require equipment capable of atomic-level precision, high throughput, and seamless integration into their complex manufacturing lines.

Beyond traditional semiconductor manufacturing, other crucial potential customers include Solar Cell Manufacturers, who rely on thin film deposition for creating photovoltaic layers; Display Panel Manufacturers, particularly for LED, OLED, and LCD technologies; and Data Storage Companies, for magnetic and resistive memory applications. Furthermore, the burgeoning fields of Micro-Electro-Mechanical Systems (MEMS) and advanced medical devices also represent growing customer bases, requiring specialized thin films for sensors, actuators, and biocompatible coatings. Research and Development (R&D) laboratories in academia and industry are also significant buyers, continuously pushing the boundaries of material science and novel device architectures using cutting-edge deposition tools. These diverse customer segments underscore the pervasive and indispensable role of thin film semiconductor deposition across the modern technological landscape.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 28.5 billion |

| Market Forecast in 2032 | USD 52.8 billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials Inc., Lam Research Corporation, Tokyo Electron Limited (TEL), KLA Corporation, ASM International N.V., Hitachi High-Tech Corporation, Canon Inc., Veeco Instruments Inc., SPTS Technologies Ltd. (KLA Corporation), Beneq Oy, Oxford Instruments plc, AIXTRON SE, CVD Equipment Corporation, Ulvac, Inc., Kurt J. Lesker Company, Picosun Oy, Plasmalab Ltd., Samco Inc., centrotherm international AG, Jusung Engineering Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Thin Film Semiconductor Deposition Market is characterized by a dynamic and continuously evolving technology landscape, where innovation is paramount to meeting the ever-increasing demands of advanced electronics. The core technologies, Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), and Atomic Layer Deposition (ALD), are constantly being refined and enhanced. PVD techniques, including sputtering (DC, RF, reactive) and evaporation (thermal, e-beam), remain critical for metallic and barrier layers, with advancements focusing on improved target utilization, uniformity, and reduced particulate generation. For CVD, techniques like Plasma Enhanced CVD (PECVD), Low-Pressure CVD (LPCVD), and High-Density Plasma CVD (HDPCVD) are seeing continuous development to achieve better conformality, lower deposition temperatures, and wider material versatility for dielectric and insulating films, crucial for advanced interconnects and gate stacks. Metalorganic CVD (MOCVD) is especially vital for compound semiconductors such as GaN and GaAs used in power and RF applications.

Atomic Layer Deposition (ALD) represents a leading edge in thin film technology, offering unmatched precision and conformality at the atomic scale. Innovations in ALD focus on increasing deposition rates (e.g., spatial ALD), developing new precursor chemistries for novel materials (e.g., high-k dielectrics, 2D materials), and expanding its application from memory devices to logic, advanced packaging, and even flexible electronics. Epitaxial growth techniques, such as Molecular Beam Epitaxy (MBE) and Vapor Phase Epitaxy (VPE), are indispensable for growing single-crystal semiconductor layers with precise control over doping and alloy composition, crucial for high-performance transistors and photonics. These advanced techniques are foundational to enabling the performance gains required by next-generation devices, particularly in areas like quantum computing and advanced sensors.

Beyond the core deposition methods, the technological landscape also includes advancements in ancillary and complementary systems. This encompasses sophisticated metrology tools for in-situ and ex-situ film characterization, ensuring precise thickness, composition, stress, and electrical properties. Advanced plasma sources and reactor designs are continually being developed to optimize process efficiency, film quality, and throughput. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into deposition systems is a significant trend, enabling real-time process control, predictive maintenance, and accelerated materials discovery. Environmentally conscious designs and process chemistries are also gaining traction, driven by sustainability concerns and regulatory pressures. Overall, the key technology landscape is defined by a relentless pursuit of greater control, higher performance, broader material versatility, and improved operational efficiency, underpinning the entire semiconductor manufacturing ecosystem.

Thin film deposition is a manufacturing process where extremely thin layers of material (nanometers to micrometers) are applied to a substrate. It is crucial in semiconductors as these films form the functional components (conductors, insulators, semiconductors) of integrated circuits, enabling device miniaturization, enhanced performance, and complex functionalities essential for modern electronics.

The main types include Physical Vapor Deposition (PVD) like sputtering and evaporation, Chemical Vapor Deposition (CVD) such as PECVD and LPCVD, and Atomic Layer Deposition (ALD). Each technique offers distinct advantages in terms of film quality, conformality, material versatility, and process control, catering to different application requirements in semiconductor manufacturing.

Thin film deposition directly impacts semiconductor performance by controlling critical parameters like electrical conductivity, dielectric strength, optical properties, and barrier protection. Precise control over film thickness, uniformity, and material composition via these processes is essential for achieving the desired device speed, power efficiency, reliability, and functionality in advanced integrated circuits.

The market's growth is primarily driven by the increasing demand for advanced electronic devices, miniaturization trends, the proliferation of technologies like IoT, AI, and 5G, and the expansion of automotive electronics and data centers. These factors necessitate continuous innovation in deposition processes to produce smaller, faster, and more powerful semiconductor components.

Recent advancements include enhanced precision with Atomic Layer Deposition (ALD) for ultra-thin films, improved process control through AI and Machine Learning integration, development of new precursor materials for novel film properties, and advancements in plasma-enhanced techniques for lower temperature processing. These innovations aim to meet the complex requirements of next-generation semiconductor devices and advanced packaging solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.