ID : MRU_ 430270 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

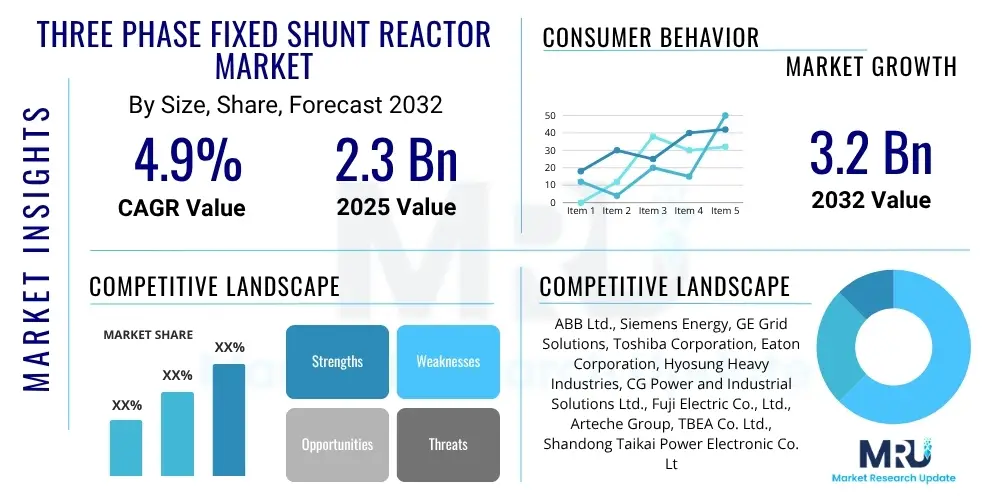

The Three Phase Fixed Shunt Reactor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.9% between 2025 and 2032. The market is estimated at USD 2.3 Billion in 2025 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2032.

The Three Phase Fixed Shunt Reactor Market is a cornerstone of modern electrical power infrastructure, critical for maintaining the operational stability and efficiency of high-voltage transmission and distribution networks globally. These essential electrical apparatuses are designed to absorb reactive power, a necessary function to control and regulate voltage levels, particularly across extensive extra high voltage (EHV) and ultra high voltage (UHV) transmission lines. In scenarios where power lines are lightly loaded or when significant capacitive generation sources, such as long underground cables or large capacitor banks, are present, shunt reactors prevent undesirable overvoltages and ensure the integrity of the power system. Their inductive nature effectively counteracts the capacitive effects inherent in long-distance power transmission, thereby preserving power quality and preventing potential damage to grid equipment.

The operational principle of a three phase fixed shunt reactor involves creating a stable inductive load that helps balance the reactive power within the system. This balancing act is vital for preventing voltage swells, minimizing transmission losses, and improving the overall power factor of the grid. Such reactors are deployed in various applications including large-scale power grids managed by national utilities, where they support system stability and power flow control. They are also increasingly being integrated into industrial grids that require precise voltage control for sensitive machinery, and critically, in the burgeoning renewable energy sector. The integration of intermittent renewable sources like large wind farms and solar power plants often introduces reactive power fluctuations, making shunt reactors indispensable for their seamless and stable connection to the national grid. The market's upward trajectory is primarily driven by an escalating global demand for electricity, ambitious grid modernization initiatives across both developed and developing economies, and the rapid expansion of renewable energy generation capacity, all of which necessitate robust and reliable reactive power compensation solutions to ensure resilient and high-quality power transmission.

These reactors come in various designs, including gapped core, coreless, and air-core types, each optimized for specific applications and operational characteristics. They can be connected directly to the transmission line or to the tertiary winding of a power transformer, providing flexibility in grid integration. The fixed nature of these reactors implies that their reactive power absorption capacity is constant once installed, offering a reliable and straightforward solution for base load reactive power compensation. This contrasts with more dynamic solutions like Static Var Compensators (SVCs) or Static Synchronous Compensators (STATCOMs), which provide variable compensation. The continued relevance of fixed shunt reactors lies in their proven reliability, robust construction, and cost-effectiveness for managing steady-state reactive power imbalances, forming a foundational element in power system engineering.

The Three Phase Fixed Shunt Reactor Market is currently navigating a period of significant transformation, propelled by evolving global energy landscapes and profound technological advancements. Prominent business trends within the market include a heightened emphasis on developing reactors with higher voltage ratings, particularly above 500kV, to support ultra-high voltage transmission corridors and inter-regional power grids. There is also a discernible shift towards intelligent grid integration capabilities, wherein manufacturers are incorporating advanced monitoring, diagnostic, and communication features to enable seamless interaction with smart grid management systems. Strategic consolidations, mergers, and acquisitions are becoming more frequent as key players seek to expand their technological portfolios, enhance geographical reach, and leverage economies of scale. Furthermore, the market is witnessing increased investment in research and development aimed at improving the efficiency, compactness, and environmental sustainability of reactor designs, including the exploration of alternative insulation materials and more advanced cooling technologies.

From a regional perspective, the Asia Pacific region continues to exert a dominant influence on the market, experiencing robust growth fueled by extensive governmental investments in grid expansion and modernization, rapid urbanization, and a surging demand for electricity in countries such as China, India, and Southeast Asian nations. These regions are undertaking ambitious projects to integrate vast new renewable energy capacities, which inherently require substantial reactive power compensation. North America and Europe, while more mature markets, are witnessing steady and sustained demand primarily driven by critical infrastructure upgrade initiatives, the implementation of sophisticated smart grid technologies, and the extensive integration of large-scale renewable energy sources, notably offshore wind farms in Europe. Latin America and the Middle East and Africa (MEA) are also emerging as high-growth regions, propelled by significant investments in new power generation and transmission projects aimed at addressing increasing industrialization and population growth, alongside efforts towards energy diversification.

Segmentation trends reveal that oil-immersed shunt reactors maintain their leading market share, primarily due to their established reliability, cost-effectiveness, and extensive track record in high-voltage applications. However, dry-type reactors are steadily gaining traction, especially in niche applications where environmental considerations, such as fire safety and space constraints, are paramount. This shift is particularly noticeable in urban substations and industrial facilities. In terms of voltage levels, the segment above 500kV is projected to experience the fastest growth, reflecting the global trend towards building ultra-high voltage transmission lines to transmit power over longer distances and to integrate remote generation sources. Application-wise, transmission and distribution utilities remain the largest end-users, but the renewable energy sector is demonstrating the most significant growth potential, underscoring the critical role of shunt reactors in supporting the global transition to cleaner energy. These intertwined trends collectively shape the competitive landscape and strategic imperatives within the three phase fixed shunt reactor market.

Users are increasingly inquisitive about the transformative impact of Artificial Intelligence on the design, operation, and maintenance paradigms within the Three Phase Fixed Shunt Reactor Market. A common thread among these inquiries centers on how AI can transition traditional reactive power compensation strategies into more dynamic, predictive, and autonomous systems. Key themes surfacing from these questions highlight expectations for AI to fundamentally enhance grid reliability, operational efficiency, and equipment longevity. Specific concerns include the precision of AI-driven predictive maintenance, the effectiveness of real-time adaptive control for voltage regulation, and the optimization of reactor deployment strategies based on complex, fluctuating grid conditions. Furthermore, there is growing interest in AI's capability to analyze vast datasets from smart grids to anticipate potential faults, manage transient overvoltages with unprecedented accuracy, and potentially revolutionize the automated design and simulation of more efficient and resilient reactor systems. Stakeholders anticipate that AI integration will lead to substantial reductions in operational expenditures, significant extensions of equipment lifespan, and a robust enhancement of overall grid stability and power quality, thereby future-proofing investments in reactive power compensation infrastructure.

The Three Phase Fixed Shunt Reactor Market is significantly shaped by a powerful interplay of drivers, restraints, opportunities, and broader impact forces, each contributing to its dynamic evolution. Among the most prominent drivers is the global imperative for renewable energy integration into national grids. As countries strive to meet carbon reduction targets, the increasing deployment of large-scale wind and solar farms introduces variability and inherent reactive power imbalances into the system, creating a critical demand for shunt reactors to stabilize voltage and ensure grid reliability. Concurrently, the extensive modernization and expansion of power transmission and distribution infrastructure worldwide, particularly evident in rapidly industrializing economies in Asia and Africa, further fuel market growth. Aging grid infrastructure in developed nations also necessitates upgrades and replacements, often incorporating advanced shunt reactors to enhance overall network efficiency and resilience. The relentless rise in global electricity consumption, driven by urbanization and industrial growth, inherently demands a more robust and sophisticated power delivery system, thereby solidifying the indispensable role of reactive power compensation.

Despite these robust drivers, the market faces several notable restraints. The substantial initial capital investment required for designing, manufacturing, and installing these large-scale, technically complex electrical components represents a significant barrier, especially for utilities in budget-constrained regions. Furthermore, the inherent longevity and extended operational lifespan of existing shunt reactors, often spanning several decades, means that replacement cycles are relatively infrequent, which can temper consistent market demand. Environmental regulations, particularly those concerning the insulation fluids used in traditional oil-immersed reactors, such as mineral oil, pose another challenge. Concerns over biodegradability and fire safety are pushing manufacturers towards more environmentally friendly and safer alternatives, which may involve higher production costs or necessitate redesigns. These factors collectively require manufacturers and grid operators to carefully balance investment, environmental compliance, and long-term operational costs.

Opportunities within the market are abundant and promising, particularly with the proliferation of smart grid technologies. The integration of shunt reactors with advanced monitoring, control, and communication systems offers a significant avenue for growth, enabling more dynamic and optimized reactive power management. The continuous expansion of high-voltage direct current (HVDC) transmission systems, used for transmitting large blocks of power over long distances or connecting asynchronous grids, also presents unique opportunities for specialized shunt reactor applications. Emerging economies, with their burgeoning infrastructure development and rapid electrification initiatives, represent vast untapped markets for new grid installations. Moreover, ongoing innovations in materials science and reactor design, such as the development of compact dry-type reactors, ultra-high voltage capability, and potentially high-temperature superconducting technologies, promise to enhance performance, reduce footprint, and improve environmental attributes, opening new market segments and applications. The broader impact forces shaping the market include ongoing technological advancements that improve efficiency and reduce costs, evolving energy policies and regulatory frameworks that prioritize grid stability and renewable integration, and fluctuating global economic conditions that influence investment cycles in critical infrastructure projects. These forces collectively dictate the strategic direction and competitive dynamics within the Three Phase Fixed Shunt Reactor Market, necessitating continuous adaptation and innovation from industry participants.

The Three Phase Fixed Shunt Reactor Market is intricately segmented across various dimensions, providing a granular and comprehensive understanding of its diverse landscape. This segmentation is crucial for stakeholders to identify specific market niches, understand varying technological preferences, and tailor strategies to meet the distinct demands of different end-use sectors and voltage requirements. The primary segmentation criteria delineate reactors based on their insulating medium and construction type, the voltage levels they are designed to handle, and their ultimate application within the vast power ecosystem. Each segment presents unique growth drivers, technological considerations, and competitive dynamics, reflecting the multifaceted needs of a modern grid infrastructure.

Understanding these segments allows for targeted market analysis, enabling manufacturers to innovate in specific product categories and allowing utilities to select the most appropriate reactor technology for their particular grid challenges. For instance, the choice between oil-immersed and dry-type reactors often hinges on factors such as environmental regulations, space availability, and fire safety protocols. Similarly, the demand for reactors at different voltage levels is directly correlated with the expansion of various transmission and distribution networks, from local sub-transmission to intercontinental UHV lines. Furthermore, the application segment highlights the diverse roles reactors play, from stabilizing large national grids to ensuring the reliable integration of renewable energy sources, showcasing the pervasive utility of these critical components across the entire power value chain. The detailed breakdown presented below offers a structured view of these key market divisions.

The value chain for the Three Phase Fixed Shunt Reactor Market is a complex ecosystem, beginning with the meticulous sourcing of specialized raw materials and extending through sophisticated manufacturing processes, intricate distribution networks, and crucial post-sales support. At the upstream stage, the market is heavily reliant on a global network of suppliers providing high-quality electrical steel, primarily grain-oriented electrical steel (GOES), which forms the core of the reactor due to its excellent magnetic properties. High-purity copper or aluminum conductors are essential for the windings, ensuring minimal resistive losses. Furthermore, a wide array of insulating materials, including specialized transformer oils, cellulosic papers, epoxy resins, and porcelain or composite bushings, are procured to ensure the dielectric strength and thermal management required for high-voltage operation. The quality and availability of these materials directly impact the final product's performance and cost. Manufacturers of critical components such as tap changers, cooling systems, protective relays, and advanced monitoring sensors also form a vital part of the upstream supply chain, necessitating strong relationships with a diverse supplier base to ensure a steady influx of high-specification parts.

Midstream activities encompass the design, engineering, and manufacturing of the three phase fixed shunt reactors. This phase involves highly specialized engineering expertise to optimize electromagnetic design, thermal management, and mechanical robustness. Manufacturing facilities must adhere to stringent international standards (e.g., IEC, ANSI) and employ advanced production techniques for core assembly, coil winding, insulation application, tanking, and final assembly. Rigorous testing, including routine, type, and special tests, is conducted to ensure compliance with performance specifications and reliability requirements before dispatch. This stage also often includes significant R&D investments to innovate designs, improve efficiency, and develop environmentally friendly solutions. The downstream segment of the value chain primarily focuses on the delivery, installation, and commissioning of these reactors. The principal customers are typically national and regional transmission and distribution (T&D) utilities, large industrial corporations, and developers of utility-scale renewable energy projects. These organizations often engage directly with the manufacturers or through specialized Engineering, Procurement, and Construction (EPC) contractors who manage the entire project lifecycle, from design to commissioning. The installation process itself is complex, requiring specialized heavy lifting equipment and expert field teams.

The distribution channel within this market is predominantly characterized by direct sales, especially for large, high-value projects involving major utilities. Manufacturers often maintain dedicated sales teams and technical support personnel who engage directly with end-users, offering customized solutions, technical consultations, and long-term service agreements. This direct engagement ensures that complex technical requirements are met and that bespoke solutions can be delivered. Indirect channels, while less prevalent for the primary reactor units, do exist for specific components or for smaller-scale projects, often involving specialized electrical equipment distributors or system integrators who may bundle reactors with other substation equipment. Post-sales services, including maintenance, spare parts supply, and condition monitoring, form a critical part of the value chain, ensuring the long-term operational integrity and efficiency of the reactors. The high capital cost and critical role of shunt reactors mean that reliable after-sales support significantly influences customer purchasing decisions and builds enduring relationships within the market.

The primary potential customers and end-users of Three Phase Fixed Shunt Reactors are multifaceted entities operating across the power generation, transmission, and distribution sectors, alongside a growing segment of large industrial consumers and renewable energy developers. National and regional transmission system operators (TSOs) and distribution system operators (DSOs) collectively represent the largest and most critical segment of the customer base. These entities are entrusted with the monumental task of maintaining grid stability, ensuring reliable power delivery, and managing voltage profiles across extensive networks. Shunt reactors are indispensable tools for these operators, as they effectively regulate voltage on long transmission lines, mitigate reactive power surges caused by varying load conditions or the capacitive effects of underground cables, and prevent damaging overvoltages that could jeopardize grid assets and operational continuity. Their procurement decisions are often influenced by grid expansion plans, modernization initiatives, regulatory mandates for power quality, and the increasing integration of diverse power generation sources.

Beyond the core utility sector, major industrial facilities constitute another significant customer segment. Industries characterized by heavy inductive loads, such as steel mills, aluminum smelters, chemical plants, mining operations, and large manufacturing complexes, are highly susceptible to voltage fluctuations and poor power quality. These facilities rely on a stable and consistent power supply to protect their sensitive machinery, ensure uninterrupted production processes, and avoid costly downtime. Three phase fixed shunt reactors are deployed in these industrial grids to stabilize internal voltage, improve the power factor, and prevent harmonic distortions, thereby enhancing operational efficiency and extending the lifespan of industrial electrical equipment. Their demand is often driven by expansion projects, upgrades to existing power infrastructure, or a need to comply with internal power quality standards and external utility grid codes. The bespoke nature of industrial power systems often requires custom-engineered reactor solutions, making direct manufacturer engagement crucial for these customers.

Furthermore, the burgeoning global renewable energy sector represents a rapidly expanding customer base for fixed shunt reactors. Developers and operators of large-scale renewable energy projects, particularly utility-scale wind farms (both onshore and increasingly offshore) and large solar power plants, are significant buyers. Intermittent renewable generation sources frequently introduce substantial reactive power into the grid, which can lead to voltage instability if not properly managed. Shunt reactors play a critical role in controlling voltage levels at the point of common coupling, compensating for the reactive power generated or absorbed by inverter-based resources, and ensuring the stable and efficient integration of these green energy sources into the wider national power network. As renewable energy capacity continues to grow exponentially worldwide, so too will the demand for robust reactive power compensation solutions. Engineering, Procurement, and Construction (EPC) contractors specializing in large-scale power infrastructure projects also act as significant indirect buyers, procuring reactors on behalf of their end-client utilities and renewable energy developers, often playing a pivotal role in the specification and selection process based on project requirements and budget constraints.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 2.3 Billion |

| Market Forecast in 2032 | USD 3.2 Billion |

| Growth Rate | 4.9% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens Energy, GE Grid Solutions, Toshiba Corporation, Eaton Corporation, Hyosung Heavy Industries, CG Power and Industrial Solutions Ltd., Fuji Electric Co., Ltd., Arteche Group, TBEA Co. Ltd., Shandong Taikai Power Electronic Co. Ltd., Xian XD Transformer Co. Ltd., Bharat Heavy Electricals Limited (BHEL), Raychem RPG Pvt. Ltd., Ganz Transformers and Electric Rotating Machines Ltd., Mitsubishi Electric Corporation, Prolec GE, EFACEC Power Transformers, Tamini Trasformatori S.r.l., Koncar Power Transformers Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Three Phase Fixed Shunt Reactor Market is in a perpetual state of technological evolution, driven by the relentless pursuit of enhanced efficiency, superior reliability, and greater environmental compatibility within power systems. A critical area of focus is the development and adoption of advanced insulation materials. These innovations include composite insulators, advanced cellulosic papers, and synthetic ester oils for oil-immersed reactors, which offer superior dielectric strength, enhanced thermal performance, and improved biodegradability compared to traditional mineral oils. These materials contribute to more compact reactor designs, reduce overall weight, and augment safety features by minimizing fire risk and environmental impact, thereby expanding deployment possibilities, particularly in sensitive urban or environmentally protected areas. Manufacturers are also increasingly integrating sophisticated smart monitoring and diagnostic systems into reactors, often leveraging Internet of Things (IoT) sensors and advanced data analytics. These systems provide real-time insights into critical operational parameters such such as winding temperature, oil levels, partial discharges, and vibration, enabling condition-based monitoring. This data-driven approach empowers grid operators with unprecedented visibility into reactor health, facilitating predictive maintenance strategies that reduce unplanned outages and optimize asset utilization.

Furthermore, the application of digital twin technology is rapidly gaining traction within the market. By creating virtual replicas of physical reactors, digital twins allow engineers to simulate performance under a myriad of operational and fault conditions, optimize design parameters before physical construction, and predict maintenance requirements with high accuracy. This capability significantly streamlines the design process, accelerates prototyping, and improves the overall lifecycle management of shunt reactors, enhancing their reliability and longevity. Innovations in cooling systems are also a key technological frontier. While conventional oil-forced air cooling (OFAF) remains prevalent, research is ongoing into more efficient and sustainable cooling methods, including enhanced natural convection designs, advanced fan technologies, and the exploration of novel heat exchange materials. These efforts aim to improve thermal management, especially for ultra-high voltage and high-power reactors, allowing for more compact footprints and extended operational life under diverse climatic conditions.

Looking ahead, while still in research and early developmental stages, high-temperature superconducting (HTS) technology holds considerable promise for future generations of shunt reactors. HTS reactors could offer ultra-compact designs with virtually no resistive losses, leading to unprecedented energy efficiency and significant space savings within substations. Although the commercialization challenges related to cooling infrastructure and cost remain, continued advancements in HTS materials and cryogenics could revolutionize reactive power compensation. Additionally, advancements in magnetic core materials, such as improved amorphous metals or new grain-oriented steels with lower core losses, are continuously sought to enhance reactor efficiency and reduce energy consumption during operation. These technological shifts collectively underscore the industry's commitment to delivering more intelligent, sustainable, and high-performance solutions for grid stabilization, directly addressing the evolving demands of a modern, interconnected, and increasingly renewable-powered electricity grid.

A three-phase fixed shunt reactor is an electrical device designed as a constant inductive load that is permanently connected in parallel (shunt) to a high-voltage power transmission or distribution line. Its primary function is to absorb reactive power generated by the capacitive effects of long transmission lines, underground cables, or lightly loaded systems. By doing so, it helps to regulate voltage levels, prevent overvoltages, and improve the overall power factor and stability of the electrical grid, thereby ensuring reliable and high-quality power delivery.

Shunt reactors are essential for modern power grids because they play a crucial role in maintaining voltage stability, improving power quality, and minimizing transmission losses. With the increasing integration of intermittent renewable energy sources like large wind and solar farms, the grid experiences more dynamic reactive power imbalances. Shunt reactors counterbalance these fluctuations, ensuring that voltage remains within operational limits, facilitating the stable connection of renewables, and enhancing the overall resilience and efficiency of the power infrastructure.

Environmental regulations significantly influence the Three Phase Fixed Shunt Reactor Market, particularly concerning the insulating fluids used in oil-immersed reactors. Strict rules regarding biodegradability, fire safety, and leakage prevention are compelling manufacturers to develop and adopt more environmentally friendly alternatives, such as natural ester oils, or to invest in dry-type reactor technologies. These regulations drive innovation towards greener, safer, and more sustainable reactor solutions, impacting design, material selection, and ultimately, market offerings.

Key technological advancements shaping the future of shunt reactors include advanced insulation materials for improved performance and reduced environmental impact, smart monitoring and diagnostic systems leveraging IoT and AI for predictive maintenance, and digital twin technology for optimized design and lifecycle management. Furthermore, research into high-temperature superconducting (HTS) technology promises ultra-compact and highly efficient reactors, although its commercialization is still a long-term prospect. These innovations aim to enhance reliability, efficiency, and sustainability.

The Asia Pacific region is expected to drive the highest demand for shunt reactors due to extensive grid expansion, rapid industrialization, and aggressive renewable energy integration initiatives, particularly in China and India. North America and Europe will see steady demand driven by aging infrastructure upgrades, smart grid implementation, and the integration of large-scale renewable projects, such as offshore wind farms. Emerging economies in Latin America and MEA are also poised for significant growth through new power infrastructure investments and energy diversification strategies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.