ID : MRU_ 431231 | Date : Nov, 2025 | Pages : 245 | Region : Global | Publisher : MRU

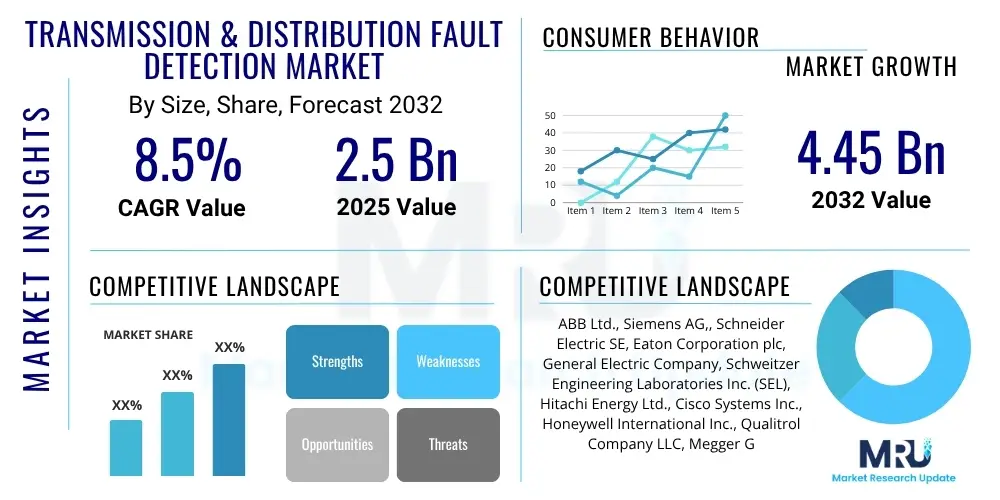

The Transmission & Distribution Fault Detection Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.45 Billion by the end of the forecast period in 2032.

The Transmission & Distribution (T&D) Fault Detection Market encompasses a sophisticated array of technologies and services specifically designed to identify, locate, and diagnose electrical faults across complex power grid infrastructures. These critical systems are indispensable for ensuring grid reliability, minimizing the economic and social impacts of power outages, and safeguarding both personnel and vital equipment from potential damage. Solutions within this market range from intelligent sensors and advanced relays embedded throughout the network to comprehensive software platforms that leverage cutting-edge data analytics, artificial intelligence, and robust communication protocols. These integrated systems are strategically deployed across diverse grid components, including expansive overhead lines, intricate underground cable networks, high-voltage transformers, and complex switchgear configurations, serving the entire spectrum of electricity transmission and distribution operations. The core objective is to provide real-time visibility into the operational status of the grid, allowing for immediate identification and characterization of any anomalies or failures, thereby enabling swift and effective intervention strategies.

Major applications for these sophisticated fault detection systems are multifaceted, primarily focused on significantly enhancing smart grid capabilities, which are crucial for managing modern, dynamic power landscapes. They play an instrumental role in facilitating the seamless and stable integration of an ever-increasing volume of intermittent renewable energy sources, such as solar and wind power, into the conventional grid infrastructure, ensuring energy security and stability. Furthermore, these systems are vital in bolstering the resilience and extending the operational lifespan of aging electrical infrastructure, a pervasive challenge in many developed economies. By providing granular, real-time insights into grid anomalies, these technologies empower utility operators to predict and preempt potential failures, drastically accelerating their response times during actual outage events, and consequently, substantially reducing the duration and impact of service interruptions on consumers and industries. The overarching benefits derived from the adoption of these sophisticated solutions include significant improvements in overall grid stability and reliability, enhanced safety protocols for both field personnel and expensive capital equipment, and substantial reductions in operational and maintenance costs through the strategic shift from reactive repairs to predictive, condition-based interventions. These comprehensive systems are unequivocally indispensable for modern power grids striving for optimal availability, efficiency, and sustainability in the rapidly evolving energy landscape.

Several potent driving factors are currently propelling the robust growth of the T&D Fault Detection Market globally. A paramount driver is the worldwide imperative for extensive grid modernization, characterized by an accelerated focus on implementing smart grid initiatives and the systematic replacement and upgrade of archaic, aging infrastructure that is often decades beyond its design life. This modernization push is critical to meet contemporary energy demands and adapt to new energy paradigms. Concurrently, the escalating and relentless demand for reliable, uninterrupted power supply, consistently fueled by rapid global industrialization, widespread urbanization, and the increasing digitalization of every sector of the economy, further intensifies the need for exceptionally robust and highly responsive fault detection mechanisms. Additionally, the proliferating integration of distributed energy resources (DERs), such as rooftop solar installations, localized wind farms, and battery storage systems, introduces unprecedented levels of complexity and variability into the grid. This dynamic environment makes advanced fault detection absolutely critical for effectively managing variable power flows, preventing grid instability, and ensuring overall system resilience. Furthermore, stringent regulatory mandates across various jurisdictions, emphasizing heightened grid reliability, improved safety standards, and performance-based penalties for prolonged outages, serve as powerful market drivers, compelling utility companies to proactively invest in state-of-the-art fault detection solutions to ensure compliance and avoid financial repercussions. These combined factors create a compelling market environment for continued innovation and adoption in the T&D fault detection sector.

The Transmission & Distribution (T&D) Fault Detection Market is currently experiencing a period of significant expansion, fundamentally reshaped by pervasive business trends towards comprehensive digitalization and enhanced automation across the entire power sector value chain. Utility companies around the globe are strategically channeling substantial investments into intelligent grid solutions, aiming to not only bolster operational efficiency and dramatically reduce costly downtime but also to elevate the quality and reliability of their critical services. The widespread adoption of advanced data analytics, sophisticated IoT-enabled sensors, and real-time monitoring platforms is rapidly becoming a de facto industry standard, fundamentally transforming the traditional approach to fault detection from a largely reactive process into a highly proactive and predictive methodology. This paradigm shift is further influenced by the relentless increase in global energy demands and the imperative for developing highly resilient infrastructure capable of withstanding a multitude of environmental stressors and operational challenges. The competitive landscape within this market is intensely dynamic and fiercely innovative, with leading industry players placing a strong emphasis on developing integrated, end-to-end solutions that offer holistic grid insights and support increasingly autonomous fault management and self-healing network capabilities, thereby setting new benchmarks for grid performance and reliability.

From a regional perspective, the market exhibits highly diverse and dynamic growth patterns, reflecting varying stages of economic development, infrastructure maturity, and regulatory environments. The Asia Pacific region is unequivocally emerging as the primary growth engine, propelled by unprecedented rapid urbanization, vast industrial expansion, and extensive new grid infrastructure development, particularly in economic powerhouses like China and India, alongside robust smart grid project investments across Southeast Asia. In stark contrast, North America and Europe continue to represent historically crucial and high-value markets, primarily driven by the critical and ongoing need to modernize their extensively aging grid infrastructure, facilitate the large-scale integration of high volumes of renewable energy, and rigorously adhere to increasingly stringent reliability and environmental standards. Meanwhile, Latin America and the Middle East & Africa regions are also witnessing an accelerated pace of adoption, largely spurred by ambitious electrification initiatives, rapid economic development, and burgeoning industrial growth, all of which necessitate more stable, secure, and efficient power delivery systems. Each distinct region presents a unique set of challenges and offers specific opportunities, profoundly influencing local technology adoption rates, shaping investment priorities, and guiding strategic partnerships within the specialized domain of fault detection solutions.

An in-depth analysis of segmentation trends within the market clearly highlights a significant and growing demand for advanced software and comprehensive service components, which are increasingly seen as indispensable complements to fundamental hardware installations. While foundational hardware such as sophisticated fault indicators, intelligent protective relays, and robust condition monitoring devices remains absolutely critical for physical detection, the 'intelligence layer' delivered by specialized software platforms is rapidly becoming paramount for sophisticated fault diagnosis, predictive analytics, and overall grid optimization. This software component empowers utilities to move beyond simple detection towards deep analytical insights and automated decision-making. By application, both high-voltage transmission and low-voltage distribution networks are identified as crucial areas of focus; however, the inherent complexity, vast geographical spread, and sheer volume of assets within distribution networks frequently drive a proportionally higher demand for highly advanced, granular, and scalable fault detection solutions. End-users, predominantly an expansive range of public and private utility companies, are increasingly seeking holistic, integrated solutions that can seamlessly streamline their operational workflows, maximize the utilization of existing and new assets, and substantially contribute to overall grid resilience. This reflects a broader industry movement towards comprehensive, smart grid management strategies that prioritize both efficiency and security.

Common user questions regarding AI's profound impact on the Transmission & Distribution Fault Detection Market consistently revolve around its ability to dramatically enhance predictive capabilities, significantly improve accuracy and speed in fault location, and increasingly automate diagnostics and response mechanisms. Users are eager to understand how AI can substantially reduce outage times, optimize operational costs, and fundamentally contribute to overall grid resilience and self-healing functionalities. Simultaneously, there is strong interest in understanding the practical challenges associated with large-scale AI implementation, such as the stringent requirements for high-quality data, the complexities of integrating AI solutions with diverse existing legacy infrastructure, the critical need for specialized skillsets among utility personnel, and inherent cybersecurity risks. Overall, there is a prevailing expectation that AI will indeed lead to a revolutionary era of more intelligent, proactive, and autonomous grid management, but also a clear need for comprehensive clarity on the feasibility, security, and ethical considerations for such mission-critical deployments to ensure trustworthy and effective implementations.

The Transmission & Distribution Fault Detection Market is critically influenced by a robust interplay of drivers, restraints, opportunities, and broader impact forces that collectively dictate its developmental trajectory and long-term growth potential. A primary driver is the widespread prevalence of aging electrical infrastructure across mature economies, particularly in North America and Europe, which urgently necessitates continuous upgrades and the deployment of highly reliable fault detection systems to prevent widespread outages and ensure consistent power supply. Concurrently, the increasing complexity of modern power grids, spurred by the extensive integration of distributed renewable energy sources and the proliferation of advanced smart grid technologies, demands more sophisticated and instantaneous fault detection capabilities. The global imperative for uninterrupted power supply, fueled by rapid industrialization, urbanization, and the pervasive digitalization of economies, further underscores the critical need for advanced fault detection to maintain grid stability and resilience. Moreover, increasingly stringent regulatory frameworks and performance-based mandates across various jurisdictions, emphasizing elevated grid reliability and imposing significant penalties for prolonged outages, act as powerful market accelerators, compelling utilities to invest proactively in state-of-the-art fault detection solutions to ensure operational compliance and mitigate financial risks.

However, the robust growth trajectory of the market faces several formidable restraints that could impede widespread adoption. The substantial initial capital expenditure required for deploying advanced fault detection systems, encompassing sophisticated sensors, communication infrastructure, and cutting-edge analytical software, represents a significant financial barrier for many utilities, especially in developing regions with limited budgets. Furthermore, a persistent shortage of skilled professionals and specialized engineers, capable of effectively operating, maintaining, and accurately interpreting the complex data generated by these intricate systems, presents a significant operational bottleneck. Cybersecurity concerns are also paramount; as the increasing connectivity and digitalization of grid components for fault detection render them more vulnerable to potential cyberattacks, this raises profound issues of data integrity, system security, and the overall resilience of critical infrastructure. Opportunities for growth are abundant, fueled by relentless technological advancements in IoT, AI, and advanced analytics, alongside supportive government initiatives for grid modernization. The expansion of electricity grids into remote areas and the burgeoning proliferation of electric vehicles (EVs) and energy storage systems also present new demands, compelling the development of adaptive, intelligent fault detection solutions that can respond dynamically to evolving grid conditions. These combined impact forces, including technological evolution, evolving regulatory landscapes, sustained economic growth, and an overarching focus on environmental sustainability, collectively shape the market's development towards a more reliable, efficient, and resilient future.

The Transmission & Distribution Fault Detection Market is extensively segmented to precisely reflect the diverse range of technological offerings, specific application environments, and unique end-user operational requirements across the global power sector. This granular understanding is absolutely crucial for market players to effectively tailor their product and service portfolios, for strategic investors to accurately identify high-potential growth opportunities, and for researchers to conduct comprehensive and insightful market analyses. The market is primarily categorized by the fundamental technology types employed, drawing a clear distinction between physical hardware components, which are essential for the initial detection and measurement of faults, and the sophisticated software and comprehensive services that provide the critical intelligence, analytical capabilities, and operational support necessary for effective fault management. This foundational segmentation helps delineate the core technological backbone of the market, ensuring that specific needs within the complex power ecosystem are addressed.

The intricate value chain for the Transmission & Distribution (T&D) Fault Detection Market begins upstream with highly specialized activities encompassing foundational research and development, innovative design, and precision manufacturing of core technological components. This foundational segment includes specialized sensor technology developers, cutting-edge communication module providers, sophisticated microprocessor designers, and pioneering software algorithm developers. These key players are instrumental in supplying the essential intellectual property and physical components that form the bedrock of any modern fault detection system to subsequent system integrators and comprehensive equipment providers. Innovation at this early stage is absolutely paramount for continually enhancing fault detection accuracy, significantly improving response times, and bolstering the overall reliability and longevity of the entire system. Midstream activities then involve the crucial processes of assembly, meticulous integration, and precise configuration of these diverse components into fully functional, comprehensive fault detection systems. This phase typically encompasses advanced hardware manufacturing, sophisticated software development and extensive customization tailored to specific client needs, and the establishment of resilient, high-speed communication infrastructure. System integrators and original equipment manufacturers (OEMs) play an exceptionally vital role at this juncture, skillfully combining disparate technologies and components into cohesive, interoperable solutions specifically engineered to meet the unique and often complex requirements of diverse grid operators, ensuring seamless interoperability and effective interface with legacy infrastructure.

The final stage of the value chain comprises the downstream activities, which are predominantly focused on the strategic deployment, continuous operation, and ongoing maintenance and support of these sophisticated fault detection systems, directly serving the ultimate end-users. This critical phase encompasses a wide array of services, including expert installation and meticulous commissioning, scheduled and corrective maintenance programs, specialized consulting services for system optimization and strategic planning, in-depth data analytics and interpretation to derive actionable insights, and comprehensive training programs designed to equip utility personnel with the necessary skills to effectively manage and utilize these advanced systems. The distribution channels employed are varied and strategically chosen, often encompassing a hybrid approach that includes both direct sales to major national and international utility corporations, allowing for closer client relationships and highly customized solution development, and indirect sales facilitated through an extensive network of regional distributors, specialized value-added resellers, and highly skilled system integration partners. These indirect channels provide broader market penetration, specialized local expertise, and efficient support across diverse geographical regions. The efficacy and responsiveness of these downstream activities are absolutely paramount for maximizing the operational benefits, ensuring the long-term sustainability, and realizing the full return on investment from the fault detection solutions deployed by end-users, thereby guaranteeing continuous grid reliability, optimal performance, and robust energy security for consumers and industries alike in the evolving power sector.

The primary potential customers and ultimate end-users of advanced Transmission & Distribution (T&D) Fault Detection products and comprehensive services are notably diverse, reflecting the expansive and critical application spectrum of these essential grid technologies across the global energy landscape. Foremost among this broad customer base are national, regional, and municipal power utility companies, encompassing a wide array of both publicly owned and privately operated entities. These utilities represent the foundational consumers of fault detection solutions, as they are under immense and continuous pressure to enhance grid reliability, minimize financially impactful outage durations, stringently comply with an ever-evolving set of regulatory standards, and meticulously optimize their substantial operational expenditures. Their strategic investments in fault detection technologies are unequivocally driven by the paramount imperative to ensure the consistent, uninterrupted, and high-quality delivery of electrical power to their vast and diverse customer bases, which range from individual residential consumers to sprawling industrial complexes. As power grids progressively become 'smarter,' more interconnected, and increasingly decentralized with the proliferation of distributed energy resources, these utilities critically require intelligent and adaptive systems that can adeptly manage complex, dynamic power flows and rapidly identify and isolate anomalies and faults, thereby maintaining overall system stability and security.

Beyond the realm of traditional power utilities, the industrial sector constitutes another highly significant and burgeoning segment of potential customers for T&D fault detection solutions. This expansive category includes critical heavy industries such as large-scale manufacturing plants, sophisticated oil and gas facilities, intensive mining operations, and highly sensitive data centers, where even fleeting or momentary power interruptions can lead to catastrophic financial losses, irreparable equipment damage, severe production stoppages, and heightened safety hazards for personnel. These industrial clients frequently own and operate their own intricate internal distribution networks and thus require exceptionally robust, highly reliable, and often ruggedized fault detection systems to diligently protect their mission-critical infrastructure, ensure continuous and uninterrupted production processes, and rigorously safeguard the safety and well-being of their workforce. They consistently prioritize solutions that offer ultra-rapid fault isolation and swift restoration capabilities to emphatically minimize costly downtime and mitigate substantial production losses, often seeking integrated systems that can seamlessly interface with their existing Supervisory Control and Data Acquisition (SCADA) systems and sophisticated Energy Management Systems (EMS). The demand emanating from these specialized industrial sectors is distinctly characterized by a pronounced need for highly reliable, custom-engineered, and often environmentally hardened fault detection solutions that are meticulously tailored to address the specific and demanding operational environments, stringent safety requirements, and unique technical specifications inherent in their respective industrial applications, ensuring maximum operational uptime and asset protection.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2032 | USD 4.45 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG,, Schneider Electric SE, Eaton Corporation plc, General Electric Company, Schweitzer Engineering Laboratories Inc. (SEL), Hitachi Energy Ltd., Cisco Systems Inc., Honeywell International Inc., Qualitrol Company LLC, Megger Group Limited, Ametek Inc., FLIR Systems Inc., Sensemetrics Inc., Detech Inc., Scope Technology, Vanguard Instruments Company Inc., Power Systems & Controls Inc., Arteche Group, NOJA Power Switchgear Pty Ltd., Sentient Energy Inc., Grid Solutions (a GE Renewable Energy business), Doble Engineering Company, ZTE Corporation, Huawei Technologies Co., Ltd., Arbiter Systems, Inc., MTE Meter Test Equipment AG, OMICRON electronics GmbH. |

| Regions Covered | North America (U.S., Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC), Latin America (Brazil, Argentina, Rest of Latin America), Middle East, and Africa (GCC Countries, South Africa, Rest of MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Transmission & Distribution Fault Detection Market is defined by a rapidly advancing technology landscape, driven by the imperative for more accurate, faster, and proactive fault identification within complex power grids. At its core are advanced Internet of Things (IoT) sensors, strategically deployed across diverse grid assets to collect real-time data on electrical parameters, temperature, and vibration, providing granular insights crucial for advanced analytics. Alongside, sophisticated Artificial Intelligence (AI) and Machine Learning (ML) algorithms are extensively integrated, processing vast amounts of sensor data, historical records, and environmental information to identify patterns, predict failures, and precisely categorize faults. These AI/ML capabilities enable a significant shift from reactive detection to intelligent diagnosis and prognosis, profoundly enhancing operational intelligence across the grid. Furthermore, robust communication technologies, including high-speed 5G and energy-efficient LoRaWAN, ensure low-latency, high-bandwidth data flow from remote assets to central control centers, critical for real-time monitoring and rapid response. Geographic Information Systems (GIS) provide crucial spatial context for fault locations, while Big Data analytics platforms manage and interpret immense data volumes, supporting operational decisions and long-term grid planning for optimal performance.

The integration of drone-based inspection systems, frequently equipped with thermal and optical cameras, offers an exceptionally efficient method for surveying vast power line stretches and critical infrastructure, enabling the rapid identification of physical damage, vegetation encroachments, or localized hot spots indicative of impending faults, thereby significantly enhancing proactive fault prevention. Specialized technologies like Partial Discharge (PD) detection and advanced waveform analysis also play a vital role in identifying subtle insulation degradation within high-voltage equipment and precisely locating transient faults, which often precede major failures and are difficult to detect using conventional methods. The powerful convergence and synergistic integration of these diverse technologies—ranging from groundbreaking hardware innovations in highly intelligent sensors and secure communication modules to advanced software intelligence in AI/ML algorithms, predictive analytics, and robust data analytics platforms—collectively form the intellectual and operational backbone of contemporary fault detection systems. This profound technological synergy is strategically aimed at creating truly self-healing grids that possess the autonomous capability to automatically detect, precisely isolate, and rapidly restore power in affected sections, thereby significantly enhancing overall grid resilience, dramatically improving operational efficiency, and ensuring superior service continuity. The relentless and continuous development in these key technological domains promises to further revolutionize how global power grids are meticulously monitored, intelligently managed, and proactively maintained, consistently pushing the boundaries of reliability, performance, and sustainability for the future of energy delivery.

Transmission & Distribution (T&D) Fault Detection involves advanced systems to identify, locate, and diagnose electrical faults in power grids. It is essential for ensuring grid stability, minimizing power outages, protecting infrastructure, and enhancing safety for personnel and the public. Efficient fault detection improves reliability, reduces economic losses, and ensures continuous, high-quality power delivery.

Integrating intermittent renewable energy sources, like solar and wind, introduces bidirectional power flows and increased grid variability. This complicates traditional fault detection methods, making it harder to accurately pinpoint fault locations. Advanced fault detection systems are therefore crucial to manage these complexities, maintain grid stability, and ensure reliability in a dynamic, decarbonized energy landscape.

Key benefits include significant reductions in power outage durations, improved customer satisfaction, and minimized economic losses. These technologies enhance overall grid reliability and resilience, enable a strategic shift from reactive to predictive maintenance, lower operational costs by reducing manual inspections, and significantly improve safety for utility personnel through real-time alerts and reduced exposure to hazardous conditions during troubleshooting.

Artificial Intelligence (AI) plays a transformative role by enabling predictive capabilities, analyzing vast datasets to foresee potential faults, and enhancing fault location accuracy. AI algorithms accelerate diagnostic processes, facilitate automated decision-making for grid restoration, and contribute to self-healing grid functionalities. This makes the power system more intelligent, efficient, and robust, leading to faster response times, reduced manual intervention, and optimized resource allocation.

Main challenges include high upfront capital investment for hardware and software, a shortage of skilled personnel, and significant cybersecurity risks associated with increased grid connectivity. Additionally, integrating modern solutions with diverse legacy infrastructure and overcoming issues of a lack of standardized interoperability protocols across different vendor platforms present considerable technical and operational hurdles, slowing widespread adoption.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.