ID : MRU_ 430514 | Date : Nov, 2025 | Pages : 242 | Region : Global | Publisher : MRU

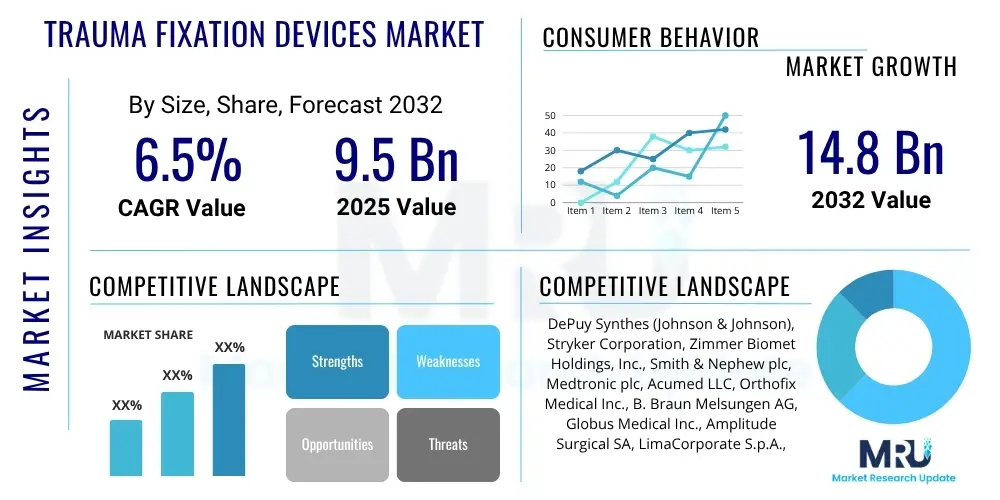

The Trauma Fixation Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at $9.5 billion in 2025 and is projected to reach $14.8 billion by the end of the forecast period in 2032.

The Trauma Fixation Devices Market encompasses a crucial segment of the medical device industry dedicated to the treatment of musculoskeletal injuries resulting from accidents, sports, or other traumatic events. These devices are essential for stabilizing fractures, correcting deformities, and facilitating the healing process, thereby restoring mobility and function to patients. Products include a wide range of internal and external fixation devices such as plates, screws, rods, nails, and pins, each designed for specific anatomical sites and injury types.

Major applications for trauma fixation devices span various orthopedic surgeries, including long bone fractures, complex joint dislocations, spinal trauma, and reconstructive procedures. The primary benefits derived from the use of these devices include immediate stabilization of injured areas, reduction of pain, acceleration of bone union, and minimization of post-operative complications. This ultimately contributes to improved patient outcomes and a quicker return to daily activities.

The market's growth is predominantly driven by several key factors. These include a global increase in the incidence of road accidents and sports-related injuries, a growing aging population more susceptible to falls and fractures, and continuous technological advancements in implant materials and surgical techniques. Furthermore, rising awareness among both medical professionals and patients regarding advanced trauma treatment options significantly contributes to market expansion.

The Trauma Fixation Devices Market is currently experiencing robust growth, propelled by evolving business trends, significant regional shifts, and distinct segment advancements. Key business trends include a notable increase in mergers and acquisitions among major players, signaling consolidation and a drive for expanded product portfolios. There is also a strong emphasis on research and development to create more sophisticated, minimally invasive, and bioresorbable implants, reflecting a broader shift towards patient-centric solutions and reduced surgical invasiveness. Companies are increasingly investing in digital health integration, incorporating smart technologies into their devices for better monitoring and outcomes.

Regionally, North America continues to hold a dominant market share, primarily due to its advanced healthcare infrastructure, high incidence of traumatic injuries, and favorable reimbursement policies. However, the Asia Pacific region is rapidly emerging as the fastest-growing market, driven by its large and aging population, increasing healthcare expenditure, and improving access to advanced medical treatments in countries like China and India. Europe also maintains a substantial market presence, characterized by its mature healthcare systems and high adoption rates of innovative surgical techniques, while Latin America and MEA show promising growth potential as healthcare facilities modernize.

Within market segments, internal fixation devices, particularly plates and screws, currently command the largest share owing to their versatility and effectiveness in treating a wide array of fractures. However, there is a burgeoning trend towards bioabsorbable implants which offer the advantage of eliminating secondary removal surgeries, thereby reducing patient discomfort and healthcare costs. The demand for customized 3D-printed implants is also on the rise, catering to specific patient anatomies and complex fracture patterns, indicating a move towards highly personalized medical solutions within the trauma fixation landscape.

User inquiries regarding Artificial Intelligence's impact on the Trauma Fixation Devices Market frequently revolve around how AI can enhance diagnostic accuracy, optimize surgical planning, facilitate robotic assistance, and personalize patient care. Users are keen to understand the potential for improved patient outcomes, increased surgical precision, and more efficient healthcare workflows. Conversely, concerns often surface regarding data privacy, the high initial investment costs for AI integration, potential job displacement for healthcare professionals, and the complexities of regulatory approval for AI-powered medical devices. The overarching theme is an expectation that AI will bring about a transformative shift, demanding careful navigation of its implementation challenges to fully realize its benefits in this critical medical domain.

The Trauma Fixation Devices Market is significantly shaped by a confluence of driving factors, restrictive elements, and emerging opportunities, all undergirded by various impact forces. Key drivers include the escalating global incidence of accidental injuries, a rapidly expanding geriatric population inherently more prone to falls and fractures, and the continuous evolution of sports medicine leading to a higher prevalence of sports-related trauma. Additionally, persistent advancements in biomaterials, implant designs, and surgical techniques, coupled with increasing public awareness regarding advanced and effective treatment modalities, further propel market expansion. These factors collectively create a robust demand landscape for innovative trauma fixation solutions, driving continuous innovation and market growth.

However, the market also faces considerable restraints that temper its growth trajectory. The high cost associated with advanced trauma fixation devices and surgical procedures can be a significant barrier, particularly in developing economies or for patients without adequate insurance coverage. Stringent and often lengthy regulatory approval processes for new devices can delay market entry and innovation. Furthermore, a persistent shortage of highly skilled orthopedic surgeons and trauma specialists, particularly in underserved regions, limits the widespread adoption and optimal utilization of these sophisticated devices. The potential for post-operative complications such as infections, implant failure, or delayed bone union also represents a concern for both patients and healthcare providers.

Opportunities within the market abound, promising future avenues for growth and innovation. The untapped potential of emerging markets, characterized by improving healthcare infrastructure and growing economies, offers significant scope for expansion. The development of novel bioresorbable implants, which naturally degrade and eliminate the need for secondary removal surgeries, presents a compelling value proposition. Furthermore, the advent of smart implants equipped with integrated sensors for real-time monitoring of healing progress, along with the increasing feasibility of customized 3D-printed devices tailored to individual patient anatomies, represent groundbreaking opportunities. The integration of telemedicine for post-operative follow-ups and remote patient monitoring also offers a chance to enhance patient care efficiency and accessibility, contributing to overall market growth and improved patient outcomes.

The Trauma Fixation Devices Market is comprehensively segmented based on various critical attributes, allowing for a detailed understanding of its dynamics and evolving landscape. These segmentations typically include product type, material composition, anatomical site of surgery, and the end-user facilities utilizing these devices. This granular analysis provides insights into market preferences, technological trends, and areas of high demand, enabling stakeholders to make informed strategic decisions and tailor product development to specific market needs. Each segment reflects unique characteristics in terms of market size, growth rate, and competitive intensity, contributing to the overall market complexity.

The categorization by product type distinguishes between internal and external fixation devices, each serving different clinical needs and injury severities. Material segmentation highlights the shift towards advanced biomaterials, offering improved biocompatibility and functional performance. Analyzing by surgery site reveals the prevalence of injuries across different body parts, influencing device design and application. Finally, end-user segmentation identifies the primary healthcare settings where these devices are predominantly utilized, such as hospitals, trauma centers, and ambulatory surgical centers, reflecting the healthcare delivery infrastructure.

The value chain for the Trauma Fixation Devices Market commences with the upstream analysis, involving the acquisition and processing of raw materials crucial for device manufacturing. This segment primarily consists of suppliers providing high-grade biomaterials such as medical-grade stainless steel, titanium alloys, cobalt-chrome alloys, and various bioabsorbable polymers like polylactic acid (PLA) and polyglycolic acid (PGA). These raw materials undergo rigorous quality checks and initial processing before being supplied to component manufacturers who specialize in fabricating intricate parts for trauma implants. The efficiency and quality control at this initial stage are paramount, as they directly influence the safety, efficacy, and longevity of the final product. Strong relationships with reliable suppliers are critical for ensuring a consistent supply of compliant materials and maintaining cost efficiency.

Moving downstream, the value chain progresses through the manufacturing of the actual trauma fixation devices, followed by their distribution and eventual application in clinical settings. Device manufacturers focus on designing, prototyping, testing, and mass-producing a wide array of implants, including plates, screws, rods, and external fixators, adhering to stringent regulatory standards. Following manufacturing, these devices are then channeled through various distribution networks. These networks can be direct, involving the manufacturer's own sales force delivering products to large hospitals and integrated healthcare systems, or indirect, leveraging third-party distributors and wholesalers who possess broader reach, particularly in regional markets and smaller clinics. The effectiveness of these distribution channels is vital for timely delivery and market penetration.

The final stage of the value chain involves the end-users—hospitals, specialized trauma centers, and ambulatory surgical centers—where orthopedic surgeons and trauma specialists implant the devices into patients. The direct sales model allows for close collaboration between manufacturers and key opinion leaders, facilitating product training and feedback. Indirect channels, on the other hand, provide scalability and access to a wider customer base, often through established relationships with local distributors. The entire chain emphasizes quality assurance, regulatory compliance, and efficient logistics to ensure that safe and effective trauma fixation devices reach patients who need them, ultimately supporting positive patient outcomes and sustaining market demand. Post-market surveillance and continuous feedback from end-users also play a crucial role in iterating and improving future product designs and treatment protocols.

The primary potential customers and end-users within the Trauma Fixation Devices Market are healthcare institutions and medical professionals who specialize in orthopedic and trauma care. Hospitals represent a significant segment of these buyers, particularly those with dedicated emergency departments and orthopedic surgery units, as they handle a high volume of acute trauma cases requiring immediate surgical intervention. These institutions procure a broad range of fixation devices to address diverse fracture patterns and musculoskeletal injuries, driven by patient volume, complexity of cases, and budget allocations.

Specialized trauma centers, often affiliated with larger hospital systems or operating independently, constitute another critical customer segment. These centers are equipped with advanced facilities and specialized personnel trained to manage severe and complex trauma, necessitating a constant supply of high-quality and innovative trauma fixation devices. Their purchasing decisions are often influenced by clinical efficacy, surgeon preference, and the availability of advanced technological solutions. Furthermore, ambulatory surgical centers (ASCs) are increasingly becoming important customers, especially for less complex, elective orthopedic procedures that may still involve the use of fixation devices, seeking cost-effective and efficient solutions.

Individual orthopedic surgeons and trauma specialists, while not direct institutional buyers, heavily influence procurement decisions within hospitals and centers. Their preferences, based on training, clinical experience, and familiarity with specific product lines, significantly impact which brands and types of fixation devices are regularly ordered. Military hospitals also represent a distinct customer base, often requiring specialized and robust fixation solutions for battlefield injuries. Ultimately, the end-users are the patients themselves, whose demand for effective and rapid recovery drives the entire market ecosystem, ensuring continuous innovation and supply of these critical medical devices.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $9.5 billion |

| Market Forecast in 2032 | $14.8 billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DePuy Synthes (Johnson & Johnson), Stryker Corporation, Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Medtronic plc, Acumed LLC, Orthofix Medical Inc., B. Braun Melsungen AG, Globus Medical Inc., Amplitude Surgical SA, LimaCorporate S.p.A., Invibio Biomaterial Solutions, CONMED Corporation, Arthrex, Inc., Wright Medical Group N.V. (acquired by Stryker), Integra LifeSciences Holdings Corporation, Meril Life Sciences Pvt. Ltd., Crossroads Extremity Systems, OsteoMed, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Trauma Fixation Devices Market is continuously evolving, driven by significant advancements in medical technology that aim to improve patient outcomes, enhance surgical precision, and accelerate recovery. One of the most impactful technological innovations is the widespread adoption of 3D printing for creating custom-made implants. This technology allows for the fabrication of patient-specific plates, screws, and other fixation devices that perfectly match complex anatomical contours, especially beneficial for intricate fractures or congenital deformities. Such personalization significantly improves fit, reduces operative time, and minimizes complications, marking a major leap from standardized off-the-shelf implants. These customized solutions leverage advanced imaging data and sophisticated design software to ensure optimal biomechanical performance tailored to the individual patient.

Another crucial area of technological advancement lies in the development of novel biomaterials. The shift from traditional metallic alloys to bioresorbable materials, such as polylactic acid (PLA) and polyglycolic acid (PGA), is transforming the market. Bioresorbable implants gradually degrade and are absorbed by the body over time, eliminating the need for a secondary surgery to remove the device once healing is complete. This reduces patient discomfort, lowers healthcare costs, and minimizes the risk of long-term implant-related complications. Furthermore, advancements in surface coatings and material science are leading to implants with enhanced biocompatibility, osteoconductivity, and antibacterial properties, promoting faster bone healing and reducing infection rates at the surgical site.

Beyond materials and manufacturing, the integration of smart technologies is also making inroads into trauma fixation. The emergence of smart implants equipped with micro-sensors is poised to revolutionize post-operative monitoring. These sensors can provide real-time data on bone healing progression, load bearing, and implant stability, transmitting crucial information wirelessly to healthcare providers. This allows for proactive intervention if complications arise and enables more precise rehabilitation protocols. Additionally, advancements in minimally invasive surgical techniques, often augmented by navigated surgery systems and robotic assistance, reduce tissue trauma, decrease hospital stays, and accelerate patient recovery. The convergence of these technological innovations is creating a landscape of more effective, safer, and personalized trauma care.

Trauma fixation devices are medical implants and instruments used in orthopedic surgery to stabilize fractures, correct deformities, and facilitate the healing of musculoskeletal injuries, thereby restoring bone function and patient mobility.

Market growth is primarily driven by the increasing incidence of road accidents and sports injuries, a growing geriatric population prone to falls, technological advancements in implant design and biomaterials, and rising awareness of advanced treatment options.

Key types include internal fixation devices like plates, screws, rods, wires, and intramedullary nails, as well as external fixation devices such as unilateral, bilateral, hybrid, and circular fixators.

Technology significantly impacts the market through innovations like 3D printing for customized implants, the development of bioresorbable materials, smart implants with sensors for monitoring, and advancements in minimally invasive surgical techniques.

North America currently leads the market, while Europe holds a substantial share. The Asia Pacific region is projected to be the fastest-growing market due to improving healthcare infrastructure and increasing patient volumes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.