ID : MRU_ 429511 | Date : Nov, 2025 | Pages : 255 | Region : Global | Publisher : MRU

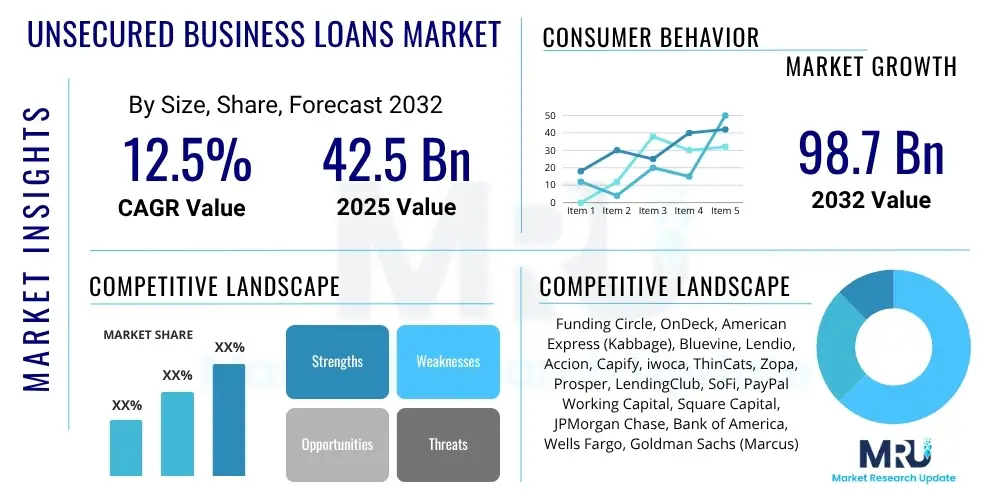

The Unsecured Business Loans Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2032. The market is estimated at USD 42.5 billion in 2025 and is projected to reach USD 98.7 billion by the end of the forecast period in 2032.

Unsecured business loans represent a cornerstone of modern business finance, particularly for Small and Medium-sized Enterprises (SMEs) and burgeoning startups that often operate without substantial tangible assets to offer as collateral. These financial products are inherently characterized by the absence of a collateral requirement, differentiating them significantly from traditional secured lending options. This structural difference not only enhances accessibility for a broader spectrum of businesses but also reflects a higher perceived risk for lenders, which is typically factored into the interest rates and repayment terms offered. The product's fundamental design caters to the agile and often immediate capital needs of businesses that prioritize speed and flexibility over pledging valuable assets, thus safeguarding their existing equity and operational freedom.

The applications for unsecured business loans are remarkably diverse, spanning critical operational expenditures and strategic growth initiatives. Businesses routinely leverage these funds for managing daily working capital requirements, ensuring smooth cash flow, and covering seasonal fluctuations. They are also instrumental in financing inventory purchases, enabling businesses to meet fluctuating customer demand without draining reserves. Furthermore, these loans are frequently applied to marketing and advertising campaigns, business expansion efforts, technology upgrades, or to bridge temporary shortfalls in revenue, acting as a crucial financial lubricant for sustained growth. The undeniable benefits, including expedited approval processes, versatile fund utilization, and the non-requirement of asset pledges, underscore their increasing appeal across various industry sectors, providing a vital lifeline for businesses at different stages of their lifecycle.

The market's robust expansion is propelled by several potent driving factors. A primary catalyst is the persistent global proliferation of SMEs and the relentless wave of new business formations, each requiring initial and ongoing capital infusion. This inherent demand is amplified by the widespread digital transformation across the financial sector, where advancements in online lending platforms and sophisticated financial technology (fintech) have drastically simplified the application process and accelerated disbursement timelines. The prevailing business preference for streamlined, convenient, and rapid access to funding further solidifies this trend. Moreover, in emerging economies, where traditional banking infrastructure might be less developed or more rigid, unsecured digital lending platforms are playing a transformative role in fostering financial inclusion and stimulating local economic growth by offering accessible capital solutions. This growing reliance on digital channels not only enhances borrower convenience but also empowers lenders to reach previously underserved markets, thereby expanding the overall footprint of the unsecured lending ecosystem.

The Unsecured Business Loans Market is poised for significant expansion, underpinned by evolving global business trends that emphasize agility, digital integration, and tailored financial solutions for Small and Medium-sized Enterprises (SMEs). A key business trend driving this growth is the pervasive influence of digital lending platforms and advanced fintech innovations, which are systematically reconfiguring the competitive landscape. These technologies facilitate rapid, data-driven loan assessments, offer highly customized loan products, and deliver seamless user experiences, moving away from the often cumbersome processes of traditional banking. The rise of embedded finance, where lending services are integrated directly into business software or e-commerce platforms, is another transformative trend, enhancing convenience and reaching businesses at their point of need, effectively lowering barriers to accessing capital and fueling entrepreneurial activity across diverse sectors. This shift towards seamless, integrated financial solutions is fundamentally altering customer expectations and forcing traditional lenders to innovate rapidly or risk losing market share to agile fintech challengers.

From a regional perspective, the market dynamics vary considerably, reflecting diverse economic conditions, regulatory environments, and levels of technological adoption. North America and Europe, characterized by mature financial infrastructures, exhibit a strong uptake of sophisticated digital lending and advanced data analytics solutions, though they also face heightened regulatory scrutiny regarding data privacy and fair lending practices. In contrast, the Asia Pacific region stands out as a high-growth frontier, fueled by a booming SME segment, rapid urbanization, and an accelerating embrace of digital financial services, particularly in populous economies like India and Southeast Asia. Latin America and the Middle East & Africa are rapidly gaining momentum, driven by increasing smartphone penetration, economic diversification efforts, and governmental initiatives aimed at fostering small business growth, presenting substantial, yet often underserved, market potential for flexible lending products. These regional nuances highlight the importance of localized strategies for market entry and sustained growth for lenders.

Segmentation trends reveal an increasing refinement and specialization of unsecured loan products to precisely match distinct business requirements. There is a discernible focus on serving micro-businesses, freelancers, and rapidly expanding e-commerce ventures, which typically necessitate smaller loan amounts with flexible repayment schedules and streamlined application processes. Lenders are increasingly leveraging sophisticated data analytics, artificial intelligence, and machine learning algorithms to move beyond conventional credit scoring. This enables them to assess a broader spectrum of alternative data points, such as transaction history, online presence, and industry-specific metrics, leading to more granular and accurate risk profiling. This personalized approach to underwriting facilitates the creation of highly targeted and relevant financing solutions for diverse business profiles, enhancing financial inclusion and optimizing the overall lending ecosystem by matching capital more efficiently with demand, thereby fostering a more robust and equitable financial landscape for small businesses worldwide.

Common user inquiries concerning the influence of Artificial Intelligence (AI) on the Unsecured Business Loans Market frequently revolve around its transformative capabilities in refining credit assessment methodologies, significantly accelerating loan approval processes, and robustly enhancing fraud detection mechanisms. Users are keenly interested in how AI can contribute to more equitable and efficient lending decisions, potentially reducing inherent biases in traditional underwriting and expanding access to capital for businesses historically underserved by conventional financing models. The dialogue also extends to the potential for AI to facilitate personalized loan offerings, dynamic interest rate adjustments, and superior risk management capabilities for lenders. While expectations for operational streamlining and enhanced customer experience are high, there are also prevalent concerns regarding data privacy, the transparency of algorithmic decision-making, and the ethical implications of AI deployment, highlighting a strong desire for responsible and balanced innovation within this evolving domain. These questions underscore the market's evolving understanding of AI's multifaceted role.

The Unsecured Business Loans Market is profoundly shaped by an intricate ecosystem of drivers, restraints, opportunities, and external impact forces that collectively dictate its growth trajectory and competitive dynamics. A primary driver fueling market expansion is the continuous surge in the global population of Small and Medium-sized Enterprises (SMEs), which are perpetually seeking agile and accessible capital solutions to fund their operations, growth, and innovation cycles without the encumbrance of pledging tangible assets. This demand is further amplified by the accelerating pace of digital transformation across all economic sectors, which mandates businesses to invest in technology and infrastructure, often requiring quick, uncollateralized financing. The intrinsic ease of access and the rapid disbursement capabilities offered by modern unsecured lending platforms also significantly contribute to their appeal, satisfying the pressing need for immediate capital among entrepreneurs and small business owners. Moreover, the increasing adoption of cloud-based solutions and API integrations streamlines the borrowing process, making unsecured loans even more attractive.

Conversely, several formidable restraints temper the market's otherwise vigorous growth. The elevated perceived risk associated with lending without collateral inherently translates into higher interest rates for borrowers, which can sometimes render these loans less attractive compared to secured alternatives, or even pose repayment challenges for financially vulnerable businesses. The ever-evolving and often stringent regulatory frameworks across different jurisdictions, particularly concerning consumer protection, data privacy, and anti-money laundering (AML) compliance, impose substantial operational and compliance costs on lenders, potentially slowing innovation and market entry for smaller players. Furthermore, the intensifying competitive landscape, characterized by both established financial institutions and a proliferation of agile fintech startups, exerts downward pressure on profit margins and necessitates continuous differentiation and technological investment. Economic uncertainties, such as inflationary pressures or periods of recession, exacerbate credit risk, leading lenders to adopt more cautious underwriting practices, thereby restricting the availability of unsecured capital for certain segments and increasing the stringency of eligibility criteria.

Amidst these challenges, substantial opportunities exist to propel the market forward. There is immense, largely untapped potential in serving micro-businesses, freelancers, and segments of the SME market that remain underserved by conventional banking systems due to lack of credit history or insufficient collateral. The continuous innovation in specialized fintech platforms, which leverage alternative data and advanced analytics, can create highly tailored and inclusive financial products for these niche segments. The rapid adoption of embedded finance solutions, where lending is seamlessly integrated into point-of-sale systems or business management software, presents a novel distribution channel that reaches businesses at their moment of need, enhancing convenience and increasing uptake. Moreover, the global shift towards online and mobile-first financial services, driven by a technologically savvy generation of entrepreneurs, further solidifies the long-term growth prospects for digital unsecured lending. External impact forces, including macro-economic stability, ongoing advancements in artificial intelligence and big data analytics for superior risk profiling, and supportive governmental policies aimed at fostering SME growth, will play a pivotal role in shaping the market's future resilience and trajectory, encouraging sustainable innovation and broader financial inclusion.

The Unsecured Business Loans market is meticulously segmented across various dimensions, providing a granular view of market dynamics and enabling lenders to craft highly targeted financial products. This comprehensive segmentation reflects the heterogeneous nature of business financing needs, encompassing differences in capital requirements, organizational structures, industry-specific challenges, and preferred lending channels. By categorizing the market based on key attributes such as loan amount, the legal structure of the borrowing entity, the industry sector, the type of financial provider, and the specific application of funds, stakeholders can gain profound insights into market demand patterns, competitive positioning, and emerging opportunities. This analytical framework is crucial for strategic planning, product development, and effective market penetration, ensuring that diverse business needs are addressed with appropriate and accessible financing solutions.

Each segment within the unsecured business loans market offers unique insights into borrower behavior and lender strategies. For instance, segmenting by loan amount allows providers to design products specifically for micro-enterprises requiring small, frequent injections of capital versus larger SMEs undertaking significant expansion projects. Understanding business types helps in tailoring legal and compliance aspects, while industry-specific segmentation informs risk models and product features, as a retail business might have different needs and risk profiles than a technology startup. The differentiation by provider highlights the competitive landscape between traditional banks, agile fintechs, and peer-to-peer platforms, each with distinct operational models and customer propositions. Finally, segmenting by the intended application of the loan underscores the various pain points businesses seek to address with unsecured capital, from bridging working capital gaps to investing in growth initiatives. This multi-dimensional approach to segmentation allows for a more nuanced understanding of market drivers and inhibitors.

The value chain for the Unsecured Business Loans Market is a complex and highly integrated network of participants and processes, designed to facilitate the flow of capital from originators to borrowing businesses. This chain commences with critical upstream activities, where the foundation for lending decisions is meticulously constructed. Key players in this initial phase include a diverse array of data providers, such as established credit bureaus like Experian, Equifax, and TransUnion, alongside specialized alternative data analytics firms that assess non-traditional metrics like banking transaction data, social media sentiment, or utility payment histories. Technology vendors, supplying robust credit scoring software, identity verification tools, and Know Your Customer (KYC) solutions, are also indispensable at this stage. These upstream components collectively provide lenders with the comprehensive information and analytical capabilities necessary to evaluate borrower creditworthiness, identify potential risks, and ensure regulatory compliance, thereby minimizing fraud and optimizing initial risk assessments before any capital is committed. The quality and breadth of this initial data collection directly impact the accuracy and speed of subsequent lending decisions, forming the bedrock of an efficient unsecured lending process.

The midstream segment of the value chain constitutes the core lending operations, where financial institutions transform raw data into actionable loan products and disburse funds. This segment is populated by a wide spectrum of lenders, including traditional commercial banks and credit unions, agile Non-Banking Financial Companies (NBFCs), innovative fintech lending platforms, and burgeoning peer-to-peer (P2P) lending marketplaces. These entities are responsible for the entire loan origination process, which encompasses product design, aggressive marketing campaigns to attract suitable borrowers, meticulous underwriting leveraging advanced algorithms, and efficient fund disbursement. The efficiency of this stage is increasingly powered by advanced technologies such as Artificial Intelligence (AI) for automated underwriting, Machine Learning (ML) for predictive analytics, and cloud computing for scalable infrastructure. The distribution of these unsecured loans is facilitated through various channels, including direct online applications via lender websites or mobile apps, strategic partnerships with financial advisors and brokers who serve as intermediaries, and increasingly, through embedded finance solutions where lending is seamlessly integrated into other business services or platforms, significantly broadening market reach and enhancing user convenience by meeting borrowers where they already conduct their business operations.

Finally, the downstream activities focus on managing the loan lifecycle post-disbursement, ensuring successful repayment and providing ongoing borrower support. This phase involves rigorous loan monitoring, efficient collection of repayments, and dedicated customer service. Tools for automated payment processing, communication platforms for borrower engagement, and sophisticated portfolio management software are critical components here, enabling lenders to track performance and interact effectively with borrowers. In instances of potential default or delinquency, third-party debt collection agencies and specialized recovery services play a vital role in minimizing financial losses for lenders, employing strategies ranging from amicable settlements to legal actions. The overarching trend across the entire value chain is a continuous drive towards digitization and automation, leveraging technologies to streamline processes, reduce operational costs, enhance decision-making accuracy, and ultimately improve the borrower experience. This holistic approach ensures that unsecured business loans are not only accessible but also efficiently managed throughout their entire lifecycle, fostering a more resilient, transparent, and responsive lending ecosystem that adapts to the evolving needs of both lenders and borrowers.

The core demographic of potential customers for unsecured business loans comprises a diverse and expansive array of Small and Medium-sized Enterprises (SMEs), budding startups, and ambitious individual entrepreneurs. These segments frequently find themselves in situations where they require immediate or flexible capital for various operational imperatives and strategic growth initiatives, yet they often lack the substantial tangible assets typically mandated by conventional financial institutions as collateral for secured lending. Startups, in particular, represent a significant proportion of this customer base; they frequently rely on unsecured financing to cover crucial initial operational expenses, acquire essential initial equipment without asset pledges, or fund the development of their first products, given their typically limited asset base in their formative stages, making speed and flexibility of funding paramount.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 42.5 Billion |

| Market Forecast in 2032 | USD 98.7 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Funding Circle, OnDeck, American Express (Kabbage), Bluevine, Lendio, Accion, Capify, iwoca, ThinCats, Zopa, Prosper, LendingClub, SoFi, PayPal Working Capital, Square Capital, JPMorgan Chase, Bank of America, Wells Fargo, Goldman Sachs (Marcus), Metro Bank, OakNorth Bank, Credibility Capital, Quicken Loans (Rocket Mortgage), Spotloan, Fundbox, StreetShares, Fast Capital 360, Oportun, Opportunity Fund, WebBank |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Unsecured Business Loans Market is being profoundly reshaped by a dynamic confluence of advanced technologies that are fundamentally altering how credit is assessed, loans are processed, and customers are engaged. Central to this technological paradigm shift is the ubiquitous adoption and continuous evolution of Artificial Intelligence (AI) and Machine Learning (ML) algorithms. These intelligent systems enable lenders to move beyond traditional, often rigid, credit scoring models by analyzing vast and diverse datasets, encompassing not only historical financial data but also alternative data points such as real-time banking transactions, social media activity, e-commerce sales performance, and even utility payment records. This sophisticated analytical capability facilitates the generation of more granular, accurate, and predictive credit risk profiles, thereby accelerating the underwriting process, reducing manual errors, and enabling highly personalized loan offers with dynamic interest rates tailored to the unique risk appetite and financial health of each business, significantly enhancing both efficiency and inclusivity in lending decisions.

An unsecured business loan is a type of financial product where the borrower is not required to provide any collateral, such as real estate, inventory, or equipment, to secure the funds. This stands in stark contrast to a secured loan, which mandates specific assets to be pledged as security against the borrowed amount. Lenders offering unsecured loans primarily assess a business's creditworthiness, financial history, cash flow stability, and overall operational health to determine eligibility and loan terms, often making them a more accessible option for startups and businesses with limited tangible assets. The key differentiation lies in the absence of an asset-backed guarantee, which typically results in a faster application process but may involve higher interest rates due to the increased risk for the lender. This flexibility makes it attractive for immediate capital needs without encumbering existing business assets.

The primary advantages of unsecured business loans include rapid access to capital, often with approval and disbursement occurring much faster than secured alternatives, allowing businesses to respond quickly to opportunities or urgent needs. They also offer significant flexibility in how the funds can be utilized across various business operations, without restrictions tied to specific collateral, enabling diverse strategic investments. Furthermore, businesses retain full ownership of all their assets, as nothing is pledged, reducing the risk of asset forfeiture in case of repayment challenges and preserving financial independence. However, potential drawbacks include generally higher interest rates to compensate lenders for the increased risk exposure, and sometimes stricter eligibility criteria concerning credit scores and revenue stability. Loan amounts may also be smaller compared to secured options, and repayment terms can be shorter, requiring efficient cash flow management from the borrower to avoid defaults.

Unsecured business loans are particularly well-suited for a broad spectrum of Small and Medium-sized Enterprises (SMEs), including nascent startups, individual entrepreneurs, and businesses operating in service-oriented or e-commerce sectors. Startups frequently leverage these loans to cover initial operational expenses, acquire essential non-collateralized equipment, or fund product development in their early stages when tangible assets are scarce, making speed and flexibility of funding paramount. Service-based businesses, such as consulting firms, marketing agencies, or IT service providers, which typically possess fewer physical assets, find unsecured financing ideal for working capital or expansion without tying up crucial intellectual capital. Additionally, the rapidly expanding e-commerce sector and online retail businesses, characterized by their need for agile financing to scale operations swiftly or manage pronounced seasonal demand fluctuations, increasingly turn to unsecured options for quick, non-collateralized capital injections to maintain their competitive edge and sustain growth in dynamic digital marketplaces.

Lenders evaluate a multifaceted set of factors to determine eligibility and establish interest rates for unsecured business loans. Primary considerations typically include the business's credit score (both personal and business), its financial history and stability demonstrated through bank statements, revenue consistency, and profitability. The time in business, industry sector, and debt-to-income ratio are also crucial. Increasingly, lenders, especially fintech platforms, leverage advanced analytics, Artificial Intelligence, and Machine Learning to assess alternative data points such as real-time cash flow, online reviews, social media presence, and operational efficiency. This comprehensive approach allows for a more accurate risk assessment, leading to personalized loan offers and dynamically adjusted interest rates that reflect the borrower's unique risk profile and ability to repay, ensuring a more bespoke and fair lending experience for diverse business applicants.

Artificial Intelligence is profoundly revolutionizing the unsecured business loans market by enhancing efficiency, accuracy, and accessibility across multiple operational facets. AI-powered algorithms enable significantly faster and more precise credit risk assessments, moving beyond traditional metrics by analyzing vast and diverse datasets including alternative data sources. This leads to expedited loan application processing and near-instantaneous approval decisions, greatly benefiting businesses needing rapid capital. AI also plays a critical role in bolstering fraud detection capabilities, identifying suspicious patterns with high accuracy, and thereby protecting lenders from financial losses. Furthermore, it facilitates the creation of highly personalized loan offers and dynamic interest rates tailored to individual business needs and risk profiles, optimizing financial solutions. Overall, AI drives operational efficiency for lenders, improves the customer experience through automated support, and fosters continuous innovation in product development and market responsiveness, making unsecured lending smarter and more inclusive.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.