ID : MRU_ 428191 | Date : Oct, 2025 | Pages : 245 | Region : Global | Publisher : MRU

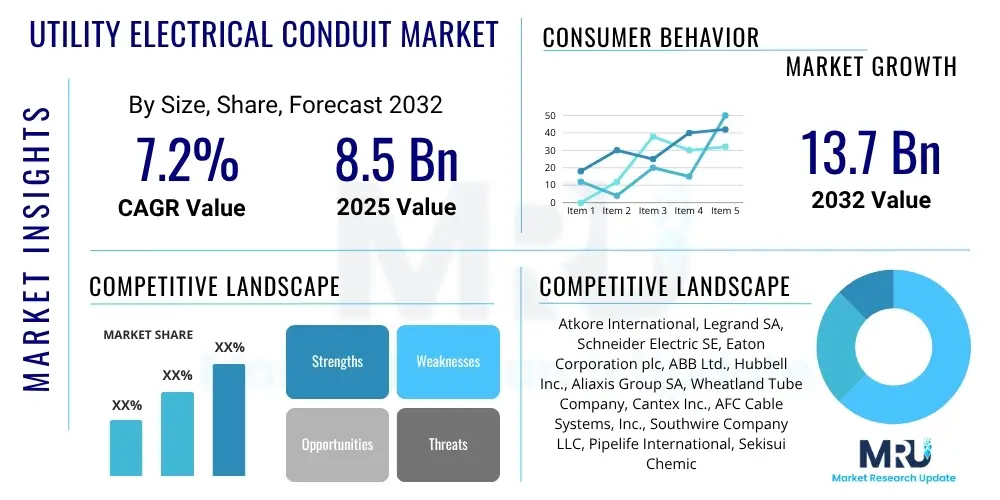

The Utility Electrical Conduit Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2032. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 13.7 Billion by the end of the forecast period in 2032.

The Utility Electrical Conduit Market encompasses the manufacturing, distribution, and installation of piping systems designed to protect and route electrical wiring within utility infrastructure. These conduits are crucial for ensuring the safety, reliability, and longevity of power transmission and distribution networks, telecommunication systems, and various industrial and commercial installations where electrical cables are exposed to environmental stressors or physical damage. They are made from diverse materials, including PVC, HDPE, steel, and fiberglass, each offering specific benefits in terms of flexibility, strength, corrosion resistance, and cost-effectiveness, tailored to different application demands and regulatory standards. The primary objective of these conduits is to shield conductors from moisture, chemicals, impact, and other external factors, thereby preventing electrical faults, ensuring continuous operation, and safeguarding personnel from potential hazards. The market's foundational role in modern infrastructure development underscores its sustained importance.

Major applications for utility electrical conduits span a broad spectrum, from underground residential distribution (URD) and commercial building wiring to high-voltage power transmission lines and intricate data center cable management. In the energy sector, they are indispensable for protecting critical power lines, especially in renewable energy projects like solar farms and wind installations, where robust protection against harsh environmental conditions is paramount. Telecommunications heavily rely on these conduits for fiber optic and data cable protection, facilitating the expansion of broadband networks and 5G infrastructure. The benefits derived from utilizing these conduits are substantial: enhanced electrical system safety, prevention of costly downtimes due to cable damage, prolonged lifespan of electrical wiring, and compliance with stringent electrical codes and regulations. Furthermore, they facilitate easier maintenance, upgrades, and expansions of electrical systems by providing an organized and accessible pathway for wiring.

Driving factors for the Utility Electrical Conduit Market are multifaceted and interconnected. Global urbanization trends, leading to continuous expansion of residential and commercial infrastructure, significantly boost demand for electrical wiring protection. The escalating need for reliable and expanded power grids, coupled with significant investments in renewable energy sources, necessitates extensive utility conduit deployment. Moreover, the rapid growth of the telecommunications sector, particularly the rollout of 5G networks and increased fiber optic deployments, presents a robust demand driver. Government initiatives and regulatory mandates aimed at enhancing electrical safety and infrastructure resilience also play a pivotal role in market expansion. Economic development in emerging markets, characterized by large-scale infrastructure projects, further fuels the market's trajectory, solidifying its essential position in global utility development.

The Utility Electrical Conduit Market is experiencing dynamic shifts influenced by several overarching business, regional, and segment trends. Business trends are largely dictated by the push towards sustainable and smart infrastructure. There is a growing emphasis on the adoption of environmentally friendly conduit materials and manufacturing processes, driven by stricter environmental regulations and corporate sustainability goals. Digitalization and automation in manufacturing processes are leading to improved production efficiency and quality control. Furthermore, strategic partnerships and mergers among key players are becoming more common, aimed at expanding market reach, enhancing product portfolios, and leveraging technological advancements. The competitive landscape is characterized by innovation in material science, focusing on enhanced durability, fire resistance, and ease of installation, all contributing to a more resilient and efficient infrastructure.

Regional trends highlight varying growth patterns and market maturities. Asia Pacific, particularly countries like China and India, represents a powerhouse of growth due to rapid urbanization, massive infrastructure development projects, and increasing industrialization. Significant government investments in smart cities, renewable energy, and telecommunication networks are propelling this region forward. North America and Europe, while more mature markets, are seeing sustained demand driven by grid modernization initiatives, replacement of aging infrastructure, and stringent safety standards. Latin America, the Middle East, and Africa are emerging as promising markets, buoyed by economic development, growing populations, and increasing access to electricity, though political stability and investment climates can influence the pace of growth. Each region presents unique opportunities and challenges, requiring tailored market strategies to capitalize on local demand drivers.

Segmentation trends reveal significant insights into market dynamics. By material type, PVC and HDPE conduits continue to dominate due to their cost-effectiveness, flexibility, and resistance to corrosion, finding extensive use in underground and demanding environmental conditions. Steel conduits, especially rigid metallic conduits (RMC) and intermediate metallic conduits (IMC), remain critical for applications requiring high mechanical protection and electromagnetic shielding in industrial and commercial settings. Fiberglass conduits are gaining traction in niche applications where lightweight properties and superior corrosion resistance are valued. Application-wise, power utility and telecommunications sectors are the largest consumers, with significant growth in data centers and renewable energy infrastructure. End-user segments, spanning residential, commercial, and industrial, each contribute uniquely, with industrial applications often demanding more specialized and robust conduit solutions, reflecting a diverse and evolving demand landscape across the market.

The integration of Artificial Intelligence (AI) is poised to bring transformative changes across the utility electrical conduit market, impacting various stages from manufacturing to deployment and maintenance. Common user inquiries often revolve around how AI can enhance efficiency, reduce costs, and improve the reliability of electrical conduit systems. Users are keen to understand AI's role in optimizing manufacturing processes, predicting material performance, and streamlining supply chain logistics. There is also significant interest in AI's potential to facilitate the development of 'smart' conduits or systems that can monitor their own integrity, detect potential faults, and integrate seamlessly with broader smart grid initiatives. Furthermore, questions frequently arise regarding AI's ability to assist in demand forecasting for specific conduit types, improving project planning, and mitigating risks associated with large-scale infrastructure projects, ultimately aiming for more intelligent and resilient utility networks.

The Utility Electrical Conduit Market is profoundly shaped by a combination of Drivers, Restraints, Opportunities, and broader Impact Forces that dictate its growth trajectory and competitive landscape. Key drivers include the relentless global demand for energy, spurred by urbanization, industrialization, and population growth, which necessitates robust electrical infrastructure. Significant investments in renewable energy projects, such as solar and wind farms, inherently require extensive conduit systems for power transmission and connection to the grid. The continuous upgrade and modernization of aging electrical grids in developed nations, along with ambitious infrastructure development plans in emerging economies, further fuel the market. Additionally, increasingly stringent safety regulations and electrical codes globally mandate the use of protective conduits, ensuring electrical system reliability and minimizing risks to human life and property. These factors collectively create a strong foundation for sustained market expansion.

However, the market also faces considerable restraints. Volatility in raw material prices, particularly for steel, PVC resins, and HDPE, directly impacts manufacturing costs and profit margins, posing challenges for pricing strategies and market stability. Environmental concerns associated with the production and disposal of certain plastic-based conduits, alongside regulatory pressures to adopt sustainable practices, can lead to increased compliance costs and limit material choices. Intense competition among manufacturers, coupled with the commoditized nature of some standard conduit products, can result in pricing pressures, eroding profitability. Furthermore, the reliance on economic cycles means that downturns in construction and infrastructure spending can temporarily dampen market demand. The complexity of installing certain conduit types and the need for skilled labor can also be a bottleneck, especially in regions facing labor shortages, influencing project timelines and overall costs within the sector.

Despite these challenges, substantial opportunities exist for market participants. The proliferation of smart city initiatives and the widespread rollout of 5G telecommunication networks present immense opportunities for specialized conduit solutions designed for high-density cabling and advanced data infrastructure. The growing adoption of electric vehicles (EVs) and the subsequent expansion of charging infrastructure create a new and significant demand segment for robust electrical conduit systems. Innovations in material science, leading to the development of lighter, more durable, fire-resistant, and recyclable conduit materials, open avenues for product differentiation and market leadership. Expanding into untapped emerging markets with nascent infrastructure development offers long-term growth prospects. Finally, the shift towards modular construction and prefabrication techniques in construction provides an opportunity for conduit manufacturers to offer integrated solutions, simplifying installation and reducing on-site labor, thereby streamlining project execution and enhancing overall market value proposition.

The Utility Electrical Conduit Market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for targeted analysis of specific product types, applications, and end-user demands, offering invaluable insights for strategic planning and market development. The market can be broadly categorized by material type, which dictates performance characteristics and suitability for various environments; by product type, differentiating between rigid and flexible forms; by application, identifying the primary end-uses; and by end-user, delineating the industries or sectors consuming these products. Each segment exhibits unique growth patterns and competitive dynamics, reflecting the varied requirements across the extensive utility and infrastructure landscape. Understanding these segments is paramount for stakeholders aiming to optimize their product offerings, penetrate new markets, and align with evolving industry standards and consumer preferences.

The value chain for the Utility Electrical Conduit Market is an intricate network of activities that transforms raw materials into finished conduit products and delivers them to the end-users. It commences with the upstream analysis, which focuses on the procurement of fundamental raw materials. This includes petrochemical derivatives such as PVC resin and HDPE pellets for plastic conduits, various grades of steel for metallic conduits, and glass fibers and resins for FRP conduits. Key suppliers in this stage are chemical companies, steel manufacturers, and specialized material producers. The quality, availability, and cost fluctuations of these raw materials directly impact the manufacturing process and the final product's pricing. Robust supplier relationships, strategic sourcing, and effective inventory management are critical in this initial phase to ensure a stable and cost-effective supply, underpinning the entire production cycle and influencing market competitiveness.

Following raw material acquisition, the value chain moves into the manufacturing and processing stage. This involves extrusion, molding, welding, and finishing operations performed by conduit manufacturers. These companies convert raw materials into various types and sizes of conduits, often incorporating specialized coatings, threads, or fittings based on application requirements. Significant investment in advanced manufacturing technologies, quality control processes, and research and development for new material compounds or designs is crucial at this stage to produce durable, compliant, and innovative products. Manufacturers also focus on achieving economies of scale and operational efficiencies to maintain competitive pricing while adhering to stringent industry standards and certifications. The capacity to innovate and adapt to evolving regulatory landscapes or customer needs directly influences a manufacturer's market position and growth potential, making this a highly competitive and technologically driven phase.

The downstream analysis primarily encompasses distribution, sales, and post-sales support, directly linking manufacturers to end-users. Distribution channels are diverse, including direct sales to large utility companies or major construction projects, indirect sales through wholesalers, distributors, and electrical supply houses, and increasingly, online platforms. Wholesalers and distributors play a vital role in market penetration, providing logistics, inventory management, and regional availability. Direct sales channels are often employed for highly customized or large-volume orders, allowing for closer customer relationships and tailored solutions. Furthermore, installation contractors, electricians, and engineering firms are critical intermediaries who specify and implement these conduits in various projects. Post-sales services, such as technical support, warranty provisions, and training, enhance customer satisfaction and foster brand loyalty. The efficiency and reach of these distribution channels are paramount for market access and ensuring products reach a broad spectrum of utility, commercial, and industrial clients effectively and reliably.

The Utility Electrical Conduit Market caters to a wide array of potential customers, all of whom share a common need for robust and reliable protection for their electrical wiring infrastructure. These end-users or buyers are diverse, ranging from large-scale government entities and public utilities to private sector enterprises across various industries, as well as individual contractors involved in construction and maintenance. Each customer segment has specific requirements influenced by factors such as project scale, environmental conditions, regulatory compliance, and budget constraints. Understanding these diverse customer needs is critical for manufacturers and suppliers to tailor their product offerings, marketing strategies, and distribution channels, ensuring their solutions effectively meet the demanding requirements of modern electrical installations. The continuous evolution of infrastructure globally ensures a sustained demand base for these essential products.

Primary potential customers include national and municipal power utility companies responsible for electricity generation, transmission, and distribution. These entities continuously invest in new power lines, substation upgrades, and grid modernization projects, requiring vast quantities of conduits for both underground and overhead applications. Telecommunication companies, including internet service providers and mobile network operators, constitute another major customer segment, driving demand for conduits to protect fiber optic cables, coaxial lines, and data wiring for 5G rollout and broadband expansion. Their continuous need for robust, interference-free cabling protection in diverse environments, from urban centers to remote areas, makes them significant buyers. The rapid expansion of data centers, with their intricate and high-density cabling requirements, also represents a growing and specialized customer group, demanding high-performance conduit solutions that can handle significant heat loads and ensure reliable operation in critical IT infrastructure.

Beyond these core utility and telecom sectors, the construction industry is a perpetual and significant customer. This includes large general contractors involved in commercial and industrial building projects, residential developers constructing new communities, and specialized electrical contractors undertaking wiring installations. Industrial facilities, such as manufacturing plants, chemical processing sites, and mining operations, require heavy-duty conduits capable of withstanding harsh conditions, chemicals, and mechanical stress. The oil and gas sector, both onshore and offshore, similarly demands highly durable and corrosion-resistant conduit systems for their critical electrical and instrumentation wiring. Government agencies, involved in public infrastructure projects like roads, bridges, tunnels, and public transport systems, also consistently procure electrical conduits to ensure the safety and longevity of public utilities and services, underscoring the broad and fundamental reliance on these protective systems across the entire economic landscape.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2032 | USD 13.7 Billion |

| Growth Rate | 7.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Atkore International, Legrand SA, Schneider Electric SE, Eaton Corporation plc, ABB Ltd., Hubbell Inc., Aliaxis Group SA, Wheatland Tube Company, Cantex Inc., AFC Cable Systems, Inc., Southwire Company LLC, Pipelife International, Sekisui Chemical Co. Ltd., Mitsubishi Chemical Corporation, Dura-Line (Orbia), JM Eagle, Electri-Flex Company, Allied Tube & Conduit (part of Atkore), Calpipe Industries, Inc., Prime Conduit Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Utility Electrical Conduit Market's technology landscape is characterized by continuous advancements aimed at enhancing performance, durability, ease of installation, and environmental sustainability. A significant area of focus is material science, where innovations are leading to the development of new polymer blends and composite materials. These advancements result in conduits with improved mechanical strength, higher resistance to extreme temperatures, UV radiation, and corrosive chemicals, alongside enhanced fire retardant properties. For instance, the evolution of specialized PVC and HDPE compounds with added stabilizers and fire retardants allows for wider application in challenging environments. Similarly, fiberglass reinforced plastic (FRP) conduits are benefiting from advanced resin systems that offer superior strength-to-weight ratios and exceptional corrosion resistance, making them ideal for aggressive industrial and underground applications. Research into recyclable and bio-degradable materials also represents a forward-looking technological trend, addressing growing environmental concerns and regulatory pressures.

Manufacturing processes are also undergoing significant technological transformation. Automation and precision engineering are being increasingly adopted to improve the consistency and quality of conduit production. Advanced extrusion and molding techniques allow for the creation of more complex geometries and tighter tolerances, leading to conduits with smoother inner walls for easier cable pulling and improved overall system integrity. The development of co-extrusion technologies enables the creation of multi-layered conduits that combine the benefits of different materials, such as a tough outer layer for protection and a slick inner layer for reduced friction. Furthermore, inline quality control systems, utilizing sensors and artificial intelligence, are becoming standard to detect defects early in the production process, minimizing waste and ensuring product specifications are met rigorously. These manufacturing efficiencies contribute directly to cost-effectiveness and product reliability, which are critical competitive factors in the market.

Beyond the physical conduit, smart technologies and digital integration are emerging as pivotal trends. The concept of "smart conduits" involves embedding sensors or RFID tags within the conduit system to enable real-time monitoring of various parameters, such as temperature, moisture ingress, or even cable integrity. This facilitates predictive maintenance, early fault detection, and optimized network management, particularly beneficial for smart grid applications and critical telecommunication infrastructure. Digital design tools, such as Building Information Modeling (BIM), are also revolutionizing the planning and installation of conduit networks, allowing for highly accurate routing, clash detection, and material optimization during the design phase. These digital advancements streamline project execution, reduce errors, and enhance the overall efficiency and intelligence of utility electrical conduit deployments, aligning with the broader trend of digitalization across the infrastructure sector.

Common materials include PVC (Polyvinyl Chloride), HDPE (High-Density Polyethylene), various types of steel (Rigid Metallic Conduit, Intermediate Metallic Conduit, Electrical Metallic Tubing), and FRP (Fiber Reinforced Plastic) or Fiberglass. Each material offers distinct properties for specific application requirements.

The market provides the essential physical infrastructure to protect and route critical electrical and data cables within smart grids. Future developments include smart conduits with embedded sensors for real-time monitoring, enabling predictive maintenance and more efficient grid management.

Key applications include power utility infrastructure (transmission and distribution), telecommunications (fiber optics, data cables for 5G), oil & gas, mining, and various construction projects (commercial, industrial, residential). They are crucial for protecting electrical wiring in diverse environments.

Asia Pacific (APAC) is currently the fastest-growing region, driven by rapid urbanization, extensive infrastructure development projects in countries like China and India, and significant investments in renewable energy and telecommunication networks.

Key advancements include innovative material science for enhanced durability and sustainability, advanced manufacturing processes for improved efficiency and quality, and the integration of smart technologies like embedded sensors for monitoring and digital design tools such as BIM for streamlined project execution.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.