ID : MRU_ 430440 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

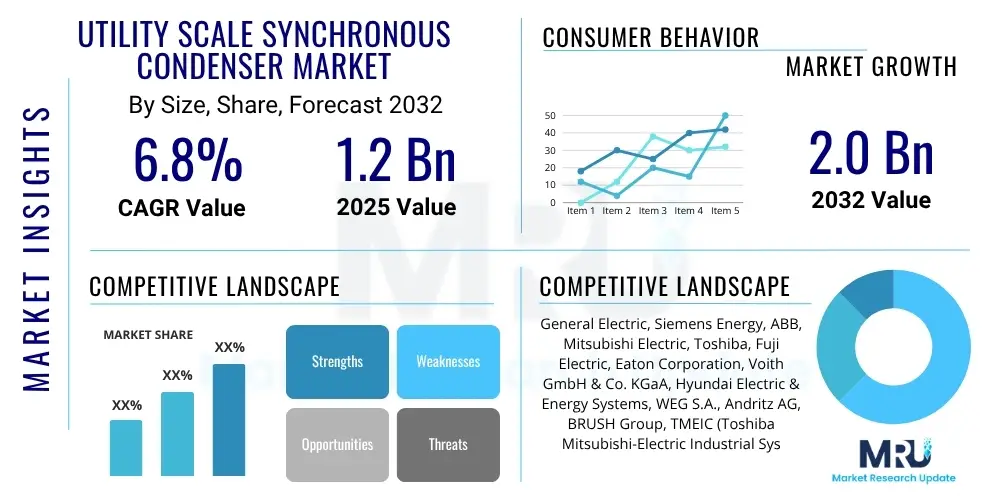

The Utility Scale Synchronous Condenser Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.0 Billion by the end of the forecast period in 2032.

The Utility Scale Synchronous Condenser Market is undergoing significant transformation, driven by the global energy transition and the increasing integration of intermittent renewable energy sources into national grids. A synchronous condenser, also known as a synchronous compensator or synchronous capacitor, is essentially a synchronous motor operating without mechanical load, specifically designed to provide or absorb reactive power to stabilize grid voltage. These critical machines play a pivotal role in maintaining the stability, reliability, and power quality of modern electricity networks, especially in an era marked by distributed generation and the phase-out of traditional fossil fuel-based power plants that historically provided inherent grid inertia.

The core product within this market encompasses large-scale rotating electrical machines that are connected to the power grid, contributing to its overall health by providing reactive power support, voltage regulation, and crucial system inertia. Unlike static compensators such as STATCOMs, synchronous condensers offer the unique advantage of contributing short-circuit current and mechanical inertia, which are vital for mitigating frequency deviations and maintaining grid robustness during fault conditions. Major applications span from supporting long transmission lines and industrial loads to enhancing the operational resilience of renewable energy parks, particularly large offshore wind farms and expansive solar arrays that lack intrinsic inertia.

The primary benefits of deploying utility scale synchronous condensers include enhanced grid stability, improved power quality, increased transmission capacity, and the provision of system strength. They are instrumental in absorbing or injecting reactive power to control voltage levels, which is crucial for efficient power transfer and preventing widespread outages. Driving factors for market expansion include the aggressive global push towards decarbonization, leading to a surge in renewable energy installations, the need to modernize aging grid infrastructure, and increasingly stringent grid codes that mandate minimum levels of system inertia and reactive power capability. These factors collectively underscore the indispensable role of synchronous condensers in securing the future of electricity grids worldwide.

The Utility Scale Synchronous Condenser Market is poised for substantial growth, primarily fueled by the accelerating global transition to renewable energy sources and the associated challenges in maintaining grid stability. Key business trends indicate a strong focus on innovation, with manufacturers developing more compact, efficient, and technologically advanced synchronous condensers capable of seamless integration into complex modern grids. There is a discernible shift towards offering integrated solutions that combine synchronous condensers with advanced control systems and digital monitoring capabilities, providing comprehensive grid support rather than standalone hardware. Furthermore, strategic partnerships between equipment manufacturers, EPC contractors, and utility companies are becoming more prevalent, aimed at delivering turn-key solutions and accelerating project deployment.

Regionally, the market exhibits diverse growth patterns influenced by varying levels of renewable energy penetration and grid modernization initiatives. Asia Pacific is emerging as a dominant region, driven by massive investments in renewable energy infrastructure, rapid industrialization, and expanding transmission networks in countries like China, India, and Australia. Europe, with its advanced grid infrastructure and ambitious decarbonization targets, continues to be a crucial market, focusing on enhancing grid resilience to accommodate high levels of wind and solar power. North America is also experiencing significant growth, primarily due to aging grid infrastructure replacement programs, the integration of large-scale renewable projects, and the imperative to improve grid stability across vast geographical areas. Latin America and the Middle East and Africa are showing promising potential as they embark on their own journeys of grid modernization and renewable energy adoption.

In terms of segment trends, the market is observing a rising demand for high-power rating synchronous condensers, especially for applications involving offshore wind farms and major transmission corridors. The need for advanced cooling technologies, such as hydrogen-cooled systems, is growing for these larger units to maximize efficiency and reduce footprint. Furthermore, there is an increasing emphasis on flexible and modular designs that can be tailored to specific grid requirements, offering utilities greater adaptability. The application segment for renewable energy integration is anticipated to demonstrate the most robust growth, reflecting the global energy paradigm shift, while conventional grid stability applications will continue to form a foundational demand base. The emphasis is on future-proofing grids, and synchronous condensers are critical components in achieving this objective by providing essential services traditionally offered by conventional thermal generators.

User inquiries concerning AI's influence on the Utility Scale Synchronous Condenser Market frequently revolve around optimizing operational efficiency, enhancing predictive maintenance capabilities, and integrating these traditional assets into smarter, more dynamic grids. Common questions explore how AI can improve the control and response times of synchronous condensers, extend their operational lifespan, and whether AI-driven grid management systems will diminish or augment the need for physical inertia providers. Users are keen to understand the extent to which AI can facilitate the seamless integration of synchronous condensers with other grid assets, such as STATCOMs and energy storage systems, for holistic grid stability solutions. The core theme is leveraging AI to make synchronous condensers not only more efficient and reliable but also more adaptive and responsive components within a highly complex, interconnected grid infrastructure, ensuring optimal performance and proactive issue resolution.

The Utility Scale Synchronous Condenser Market is primarily driven by the escalating integration of intermittent renewable energy sources, such as wind and solar power, which inherently lack the rotational inertia provided by conventional generators. This absence of inertia necessitates compensatory technologies to maintain grid frequency and voltage stability, a role perfectly suited for synchronous condensers. The global push for grid modernization and the replacement of aging infrastructure also serves as a significant driver, as older grids were not designed to handle the dynamic challenges posed by decentralized generation. Furthermore, increasingly stringent grid codes and regulatory frameworks worldwide are mandating higher standards for reactive power support, voltage control, and system strength, compelling utilities to invest in robust solutions like synchronous condensers. These forces combine to create a compelling demand for the technology, ensuring its vital role in the energy transition.

Despite strong drivers, the market faces certain restraints, most notably the high upfront capital expenditure associated with the installation of large-scale synchronous condensers. These are substantial pieces of rotating machinery requiring significant civil works, specialized transportation, and complex installation procedures, which can deter potential investors. The availability of alternative technologies, such as Static Synchronous Compensators (STATCOMs) and other power electronics-based solutions, which offer faster response times and smaller footprints, presents a competitive challenge, particularly in scenarios where inertia is not the primary concern. Moreover, the extensive planning and long lead times required for synchronous condenser projects can pose a barrier to rapid deployment, especially in rapidly evolving energy landscapes. These factors necessitate careful economic and technical evaluation by grid operators before committing to synchronous condenser investments.

Significant opportunities exist in the development of hybrid solutions that combine the inertia benefits of synchronous condensers with the fast reactive power response of STATCOMs, offering a comprehensive grid stabilization package. Emerging markets, particularly in Asia Pacific, Latin America, and Africa, present substantial growth avenues as these regions heavily invest in new power generation and transmission infrastructure, often prioritizing renewable energy integration. The increasing adoption of offshore wind power, which often requires robust grid connection solutions due far from grid connection points, also provides a niche but growing opportunity for large synchronous condenser installations. Impact forces such as evolving government policies supporting grid resilience and renewable integration, continuous technological advancements leading to more efficient and compact designs, and global economic trends influencing investment in critical infrastructure will significantly shape the market trajectory. The transition from a centralized to a distributed generation model fundamentally alters grid dynamics, creating an urgent need for solutions that can replicate or enhance the stability services traditionally provided by large fossil fuel plants, positioning synchronous condensers as a key enabler for future energy systems.

The Utility Scale Synchronous Condenser market is meticulously segmented to provide a granular understanding of its diverse components and applications, enabling stakeholders to identify specific growth areas and strategic opportunities. This segmentation typically dissects the market based on distinct characteristics such as the type of cooling employed, the power rating of the unit, the primary application for which it is utilized, and the end-user industry that deploys these critical assets. Such a detailed analysis allows for a comprehensive assessment of demand drivers and competitive landscapes across various market niches. Understanding these segments is crucial for manufacturers to tailor their product offerings, for utilities to make informed procurement decisions, and for investors to gauge market potential.

The value chain for the Utility Scale Synchronous Condenser Market begins with upstream activities involving the sourcing and processing of critical raw materials. This segment includes suppliers of high-grade electrical steel for stator cores, copper for windings, specialized insulation materials, and bearing components. Manufacturers of these fundamental parts play a crucial role in determining the quality and performance of the final product. The robustness and efficiency of the synchronous condenser are highly dependent on the integrity of these foundational components, necessitating strong relationships with reliable and quality-focused suppliers. Ensuring a stable supply chain for these specialized materials is paramount for consistent production and managing manufacturing costs effectively. This initial stage sets the technical specifications and cost base for the subsequent manufacturing processes, highlighting its foundational importance to the entire product lifecycle.

Moving downstream, the value chain encompasses the sophisticated manufacturing, assembly, and testing of synchronous condensers by original equipment manufacturers (OEMs). These companies integrate all the procured components, apply advanced engineering expertise, and conduct rigorous factory acceptance tests to ensure the units meet stringent performance and safety standards. Following manufacturing, the product moves through complex distribution channels, which often involve specialized logistics due to the enormous size and weight of these machines. Installation is a critical step, frequently managed by Engineering, Procurement, and Construction (EPC) firms that oversee project planning, site preparation, civil works, and commissioning. Post-installation, long-term operations and maintenance (O&M) services, including predictive maintenance and spare parts supply, become essential to ensure the continuous and reliable functioning of the synchronous condensers throughout their operational life. This downstream segment is characterized by high levels of technical expertise and project management capabilities.

The distribution channels for utility scale synchronous condensers are predominantly direct, involving direct sales from the OEM to large national or regional utilities and independent power producers (IPPs). This direct engagement facilitates close collaboration on technical specifications, project timelines, and customized solutions, given the strategic importance and high capital investment of these assets. Indirect distribution channels, while less common for the largest units, can involve partnerships with global EPC contractors who integrate synchronous condensers into broader grid expansion or renewable energy projects. These EPCs act as intermediaries, procuring the equipment on behalf of the ultimate end-users and providing comprehensive project delivery. Both direct and indirect models emphasize the need for strong technical support and long-term service agreements, reflecting the critical nature of synchronous condensers in maintaining grid stability and the highly specialized requirements of their deployment and operation. The complexity and bespoke nature of these products mean that sales cycles are typically long, requiring extensive pre-sales consultation and post-sales support.

The primary end-users and buyers of utility scale synchronous condensers are predominantly national and regional Transmission System Operators (TSOs) and Distribution System Operators (DSOs). These entities are responsible for managing the stability, reliability, and security of the electricity grid, making them critically dependent on technologies that provide reactive power support, voltage control, and system inertia. As grids evolve with higher penetrations of renewable energy, TSOs and DSOs face increasing challenges in maintaining these fundamental grid services, driving their demand for synchronous condensers. Their procurement decisions are heavily influenced by regulatory mandates, grid codes, and the imperative to ensure uninterrupted power supply to their service territories. The long-term investment horizon and strategic importance of these assets mean that TSOs and DSOs typically engage in extensive technical evaluations and long-term planning before procurement.

Another significant segment of potential customers includes Independent Power Producers (IPPs), particularly those involved in developing large-scale renewable energy projects such as vast onshore and offshore wind farms, and utility-scale solar installations. These developers are often mandated by grid operators to ensure their projects meet specific grid code requirements for connection, which frequently includes provisions for reactive power compensation and inertia contribution. Synchronous condensers allow IPPs to comply with these stringent grid connection requirements, thereby enabling the successful integration of their intermittent generation assets into the wider transmission network. The need for stable and compliant grid connections directly translates into demand for synchronous condensers from these renewable project developers, especially in regions with high renewable energy targets and robust grid integration policies.

Furthermore, large industrial operators, particularly those in heavy industries such as mining, petrochemicals, and metals, also represent potential customers. These industries often feature massive, fluctuating electrical loads that can introduce significant disturbances to local grid stability and power quality. By deploying synchronous condensers, these industrial facilities can ensure localized voltage support, improve power factor, and mitigate the impact of their operations on the broader grid, thereby enhancing their operational reliability and potentially reducing utility penalties. While typically smaller in scale than utility-owned units, these industrial applications still represent a valuable niche market for synchronous condenser manufacturers, driven by the need for robust internal grid management and operational continuity. The diversity of these end-users underscores the broad applicability and critical function of synchronous condensers across various segments of the energy ecosystem.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2032 | USD 2.0 Billion |

| Growth Rate | CAGR 6.8% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | General Electric, Siemens Energy, ABB, Mitsubishi Electric, Toshiba, Fuji Electric, Eaton Corporation, Voith GmbH & Co. KGaA, Hyundai Electric & Energy Systems, WEG S.A., Andritz AG, BRUSH Group, TMEIC (Toshiba Mitsubishi-Electric Industrial Systems Corporation), Nidec Corporation, Bharat Heavy Electricals Limited (BHEL), Harbin Electric Corporation, Shanghai Electric Group Co. Ltd., Ansaldo Energia S.p.A., Hitachi Energy, JSW Energy Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The key technology landscape of the Utility Scale Synchronous Condenser Market is continuously evolving, driven by the increasing demands for grid flexibility, efficiency, and reliability in a renewable-heavy energy system. Advanced control systems form the backbone of modern synchronous condensers, utilizing sophisticated algorithms and real-time data analytics to optimize reactive power output, voltage regulation, and inertia contribution. These intelligent control platforms enable precise and dynamic response to rapidly changing grid conditions, ensuring seamless integration with other grid assets and maximizing the operational benefits of the condenser. Furthermore, the development of robust and high-performance bearing technologies, including magnetic bearings, is crucial for reducing mechanical losses, extending operational lifespan, and lowering maintenance requirements, which significantly contributes to the overall efficiency and cost-effectiveness of these large rotating machines.

Innovations in cooling technologies also play a pivotal role, with hydrogen cooling remaining a dominant feature for high-power rating units due to its superior thermal conductivity, allowing for more compact designs and higher power density. However, ongoing research aims to improve air-cooled designs for smaller units, making them more efficient and suitable for a broader range of applications. The integration of synchronous condensers with Flexible AC Transmission System (FACTS) devices, such as STATCOMs, is another significant technological trend. These hybrid solutions leverage the complementary strengths of both technologies: the inertia and short-circuit contribution of synchronous condensers combined with the fast, precise reactive power compensation of STATCOMs, offering a comprehensive and highly responsive grid stabilization package. This synergistic approach ensures optimal grid performance under diverse operating scenarios, addressing both dynamic and static stability challenges effectively.

The advent of digitalization and the Industrial Internet of Things (IIoT) are further transforming the market. Remote monitoring and diagnostics systems, powered by advanced sensors and data communication networks, enable real-time performance tracking, predictive maintenance, and remote troubleshooting of synchronous condensers. This capability enhances operational reliability, minimizes downtime, and optimizes maintenance scheduling, leading to significant cost savings for operators. The creation of digital twins for synchronous condensers allows for virtual modeling and simulation of their behavior under various grid conditions, facilitating optimization of control strategies and asset management. These technological advancements collectively enhance the efficiency, reliability, and cost-effectiveness of synchronous condensers, solidifying their role as indispensable components in the future of utility-scale power grids and reinforcing their position within the modern energy infrastructure.

A utility scale synchronous condenser is a rotating electrical machine designed to absorb or provide reactive power to the grid, crucial for maintaining voltage stability and providing essential system inertia. It is essential because it supports grid resilience, especially with the integration of intermittent renewable energy sources that lack natural inertia, preventing voltage collapses and frequency deviations across the power network.

The increasing deployment of renewable energy sources like wind and solar, which are inherently intermittent and lack rotational inertia, significantly drives the demand for synchronous condensers. These devices fill the gap by providing the necessary reactive power, voltage support, and system strength to stabilize grids increasingly reliant on decentralized, variable generation, ensuring reliable power delivery.

Key advancements include sophisticated AI-powered control systems for optimized reactive power management, improved bearing technologies for enhanced efficiency and lifespan, and the development of hybrid solutions combining synchronous condensers with STATCOMs. Digitalization, including remote monitoring and digital twin creation, also plays a crucial role in improving operational reliability and predictive maintenance.

Synchronous condensers provide both reactive power and crucial mechanical inertia, contributing to short-circuit strength and frequency stability. STATCOMs (Static Synchronous Compensators) offer faster, more precise electronic reactive power compensation but do not provide inertia. Synchronous condensers are preferred when inertia and short-circuit contribution are critical, especially for large-scale renewable integration; STATCOMs are chosen for rapid dynamic voltage support without the need for inertia.

Asia Pacific is expected to lead in market growth due to massive investments in renewable energy and grid expansion, particularly in China and India. Europe also remains a strong market with high renewable penetration and stringent grid stability requirements. North America is experiencing significant demand driven by grid modernization and large-scale renewable energy project integration.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.