ID : MRU_ 430861 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

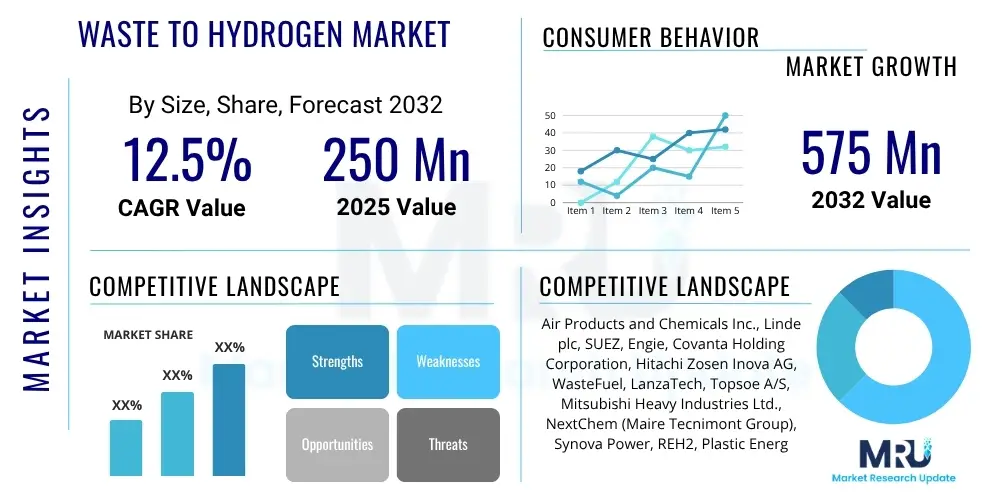

The Waste to Hydrogen Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2032. The market is estimated at USD 250 million in 2025 and is projected to reach USD 575 million by the end of the forecast period in 2032.

The Waste to Hydrogen market represents a burgeoning sector within the broader clean energy landscape, offering a dual solution to pressing global challenges: waste management and the escalating demand for sustainable energy sources. This market is driven by increasing environmental concerns regarding landfill waste, the imperative to reduce greenhouse gas emissions, and the strategic push towards a hydrogen-based economy. The core product involves the conversion of various waste streams, including municipal solid waste, industrial byproducts, agricultural residues, and plastics, into valuable hydrogen gas through advanced thermochemical and biological processes. These innovative technologies enable the valorization of materials previously considered liabilities, transforming them into a high-demand, clean energy carrier.

Major applications for waste-derived hydrogen span across diverse industries. It serves as a crucial feedstock in the chemical and petrochemical sectors for producing ammonia, methanol, and other synthetic fuels. In the energy domain, hydrogen is increasingly vital for power generation, either directly in gas turbines or through highly efficient fuel cells for stationary power and grid balancing. The transportation sector represents a significant growth area, with hydrogen fuel cell electric vehicles (FCEVs) offering zero-emission alternatives for passenger cars, buses, trains, and heavy-duty trucks. Furthermore, the integration of waste-to-hydrogen solutions into existing waste management infrastructure presents opportunities for localized, distributed energy production, enhancing energy security and reducing reliance on fossil fuels.

The benefits of the Waste to Hydrogen market are multifaceted, encompassing environmental, economic, and social dimensions. Environmentally, it significantly reduces landfill volumes, mitigates methane emissions from decomposing organic waste, and offers a path to decarbonize hard-to-abate sectors by providing clean hydrogen. Economically, it creates new revenue streams from waste, stimulates technological innovation, and fosters green job creation. Driving factors for market expansion include stringent waste disposal regulations, robust government incentives and subsidies for hydrogen production and renewable energy, substantial advancements in conversion technologies making processes more efficient and cost-effective, and the burgeoning global demand for hydrogen as a cornerstone of future energy systems. These elements collectively position the Waste to Hydrogen market as a pivotal component in achieving a circular economy and a sustainable energy future.

The Waste to Hydrogen market is undergoing a transformative period, characterized by dynamic business trends, evolving regional priorities, and significant segment-specific advancements. Industry stakeholders are increasingly focused on fostering strategic collaborations and partnerships, combining expertise in waste management, advanced engineering, and hydrogen production to develop integrated, end-to-end solutions. There is a discernible trend towards modular and scalable plant designs, enabling more flexible deployment across various waste availability scenarios and catering to diverse capacities. Furthermore, substantial private and public investments are pouring into research and development, particularly in improving process efficiency, enhancing hydrogen purity, and reducing overall capital and operational expenditures to accelerate commercial viability and market adoption. The emphasis is on creating robust and resilient supply chains for both feedstock and the generated hydrogen.

Regionally, the market exhibits varied maturity levels and growth trajectories. Europe stands at the forefront, driven by ambitious circular economy policies, stringent waste disposal regulations, and aggressive decarbonization targets outlined in its hydrogen strategy. North America, particularly the United States and Canada, is experiencing rapid growth due to supportive government incentives, significant industrial waste streams, and investments in hydrogen infrastructure. The Asia Pacific region is emerging as a critical growth engine, propelled by massive urban waste generation, rapid industrialization, and increasingly proactive national hydrogen strategies in countries like Japan, South Korea, China, and India. Latin America and the Middle East and Africa regions, while currently smaller, present immense untapped potential, fueled by growing populations, escalating waste management challenges, and nascent but developing clean energy ambitions, particularly in hydrogen production for export and domestic use.

Segmentation trends reveal a strong emphasis on thermal conversion technologies, such as gasification and pyrolysis, for their versatility in handling diverse waste types and their potential for higher hydrogen yields. Biological methods, including anaerobic digestion and fermentation, are gaining traction for organic-rich waste streams, offering lower energy inputs and synergistic production of other valuable co-products. In terms of waste types, municipal solid waste (MSW) and industrial waste remain dominant feedstocks, though plastic waste is rapidly gaining prominence due to its abundance and the urgency of addressing plastic pollution. Application-wise, the market is seeing increased adoption in the industrial sector for chemical feedstock, alongside significant growth in the mobility sector as hydrogen fuel cell technology matures. Power generation applications, particularly for decentralized energy solutions and grid stabilization, are also expanding, reflecting the market's adaptability and broad utility in the transition to a sustainable energy landscape.

Users are keenly interested in understanding how artificial intelligence can transform the Waste to Hydrogen market, particularly regarding efficiency, cost reduction, and operational resilience. Key questions revolve around AI's ability to optimize complex conversion processes, manage the inherent variability of waste feedstocks, and improve the overall economic viability of these sustainable technologies. There is significant expectation that AI will provide solutions for real-time monitoring, predictive maintenance, and intelligent control systems, addressing current operational challenges and accelerating the commercial deployment of waste-to-hydrogen plants. Users seek clarity on how AI can streamline the entire value chain, from waste collection and sorting to hydrogen purification and distribution, ultimately contributing to a more sustainable and economically competitive hydrogen economy.

The Waste to Hydrogen market is profoundly shaped by a confluence of driving forces, significant restraints, emerging opportunities, and broader impact forces. A primary driver is the global waste management crisis, with increasing waste generation and diminishing landfill space compelling countries to seek innovative disposal and valorization solutions. Concurrently, aggressive decarbonization goals set by governments and corporations worldwide are accelerating the transition towards clean energy carriers like hydrogen, making waste-derived hydrogen an attractive option for its potential to be carbon-neutral or even carbon-negative. Supportive governmental policies, including subsidies, tax incentives, and regulatory mandates for renewable energy and waste diversion, provide crucial financial and legislative impetus. Furthermore, continuous technological advancements in conversion processes, such as improved catalysts, reactor designs, and purification methods, are enhancing efficiency and reducing the cost of hydrogen production from diverse waste streams, making the proposition more economically viable and competitive.

Despite significant potential, the market faces several notable restraints. High capital expenditure (CapEx) for plant construction and associated infrastructure remains a major barrier, often requiring substantial initial investment which can deter smaller players. Operational complexities are inherent, particularly in managing the highly heterogeneous and variable nature of waste feedstocks, which necessitates sophisticated pre-treatment and robust conversion technologies to ensure consistent hydrogen output. The nascent state of standardized hydrogen infrastructure, including storage, transportation, and refueling networks, presents a logistical challenge for broad market adoption. Public perception and acceptance, often influenced by Not-In-My-Backyard (NIMBY) sentiments regarding waste processing facilities, can also impede project development. Moreover, competition from other hydrogen production methods, particularly green hydrogen from electrolysis powered by dedicated renewables, requires waste-to-hydrogen solutions to continually improve their cost-effectiveness and scalability.

Significant opportunities abound within the Waste to Hydrogen market, offering pathways for substantial growth and innovation. The vast, untapped resource of waste, globally generating billions of tons annually, represents a sustainable and readily available feedstock, positioning waste-to-hydrogen as a long-term solution to both waste and energy challenges. The broader emergence of a global green hydrogen economy, characterized by increasing demand and supportive policy frameworks, creates a strong market pull for all forms of low-carbon hydrogen. There is a substantial opportunity for synergistic integration with existing waste treatment facilities, allowing for co-location benefits and leveraging established infrastructure to reduce project costs and accelerate deployment. Additionally, the development of decentralized waste-to-hydrogen plants offers a pathway to localized energy independence, reducing transmission losses and enhancing energy security for communities. Impact forces such as escalating regulatory pressures to achieve net-zero emissions, growing environmental consciousness among consumers and industries, increasing concerns over energy security and geopolitical stability driving diversification of energy sources, and rising investor confidence in sustainable technologies are collectively pushing the market forward, fostering innovation and attracting substantial capital towards waste valorization initiatives.

The Waste to Hydrogen market is meticulously segmented across various dimensions, including technology, waste type, and application, providing a granular view of its structure, growth dynamics, and strategic opportunities. This segmentation is crucial for stakeholders to understand the diverse pathways to hydrogen production from waste and to identify niche markets or technologies that align with their operational capabilities and market objectives. The market's complexity reflects the wide array of waste compositions and the different hydrogen purity and volume requirements for various end-use applications. Analyzing these segments helps in identifying which conversion methods are best suited for specific waste streams and which applications offer the most promising growth trajectories, thereby enabling targeted investment and development strategies.

The value chain for the Waste to Hydrogen market is a multi-stage process encompassing the entire journey from waste feedstock acquisition to hydrogen delivery to the end-user, involving several critical components and stakeholders. Upstream activities are centered on the efficient collection, sorting, and pre-treatment of diverse waste materials. This involves a complex logistical network for gathering municipal, industrial, or agricultural waste, followed by sophisticated sorting technologies to separate valuable components and remove contaminants. Pre-treatment steps such as shredding, drying, pelletizing, or gasification feedstock preparation are crucial to ensure a consistent and optimized input for the conversion process, directly impacting the efficiency and yield of hydrogen production. These initial stages are often capital-intensive and require robust infrastructure for effective waste management.

Midstream activities involve the core conversion technologies where waste is transformed into hydrogen. This typically includes advanced thermal processes like gasification, pyrolysis, or plasma arc gasification, or biological methods such as anaerobic digestion and fermentation. Following the primary conversion, the raw syngas or biogas undergoes extensive purification and conditioning processes to remove impurities, convert carbon monoxide to carbon dioxide (via water-gas shift reaction), and separate hydrogen. This purification stage is paramount to achieve the high purity levels required for most industrial applications and especially for fuel cells. Specialized companies focusing on technology development, engineering, procurement, and construction (EPC) play a significant role in designing and implementing these complex conversion and purification facilities, ensuring optimal operational parameters and safety standards.

Downstream activities focus on the handling, storage, and distribution of the produced hydrogen to end-users. Hydrogen can be compressed, liquefied, or converted to ammonia or liquid organic hydrogen carriers (LOHCs) for efficient storage and transportation. The distribution channels for waste-derived hydrogen are evolving, ranging from direct pipeline networks for large industrial consumers located in proximity to the production plant, to trucking liquefied or compressed hydrogen to more dispersed end-users. The development of dedicated hydrogen refueling stations is crucial for the expanding fuel cell vehicle market. Both direct and indirect distribution channels are utilized; direct sales involve producers supplying hydrogen directly to major industrial off-takers or power plants, while indirect channels involve partnerships with industrial gas suppliers, energy trading companies, or specialized logistics providers who manage the delivery to a broader customer base, including smaller businesses and hydrogen refueling stations, thus ensuring market reach and efficient supply chain integration.

The Waste to Hydrogen market caters to a broad spectrum of end-users and buyers, spanning across various industrial, municipal, and energy sectors, all seeking sustainable solutions for both waste management and clean energy supply. Industrial facilities, such as refineries, chemical plants, and steel mills, represent a significant customer base due to their substantial existing demand for hydrogen as a crucial feedstock in their production processes. These industries are increasingly pressured to decarbonize their operations and source hydrogen from sustainable origins. Municipalities and local governments are also key buyers, primarily driven by the imperative to manage escalating urban waste volumes while simultaneously seeking to generate revenue and provide cleaner energy for public services, including public transport fleets using hydrogen fuel cell vehicles.

Furthermore, energy companies and independent power producers are emerging as critical customers, leveraging waste-to-hydrogen technologies to generate electricity, either for grid injection or for localized power solutions, contributing to a diversified and resilient energy mix. The logistics and transportation sectors are increasingly exploring hydrogen as an alternative fuel for heavy-duty trucks, buses, trains, and even maritime vessels, making them significant potential off-takers for waste-derived hydrogen as they aim to reduce their carbon footprint. The agricultural sector also presents a unique opportunity, particularly for on-site energy generation from agricultural residues and animal waste, and for local ammonia production for fertilizers. Data centers and other critical infrastructure facilities are considering hydrogen fuel cells as reliable, clean backup power solutions, further diversifying the customer landscape for waste-to-hydrogen initiatives. These varied applications underscore the broad market appeal and the strategic importance of waste-to-hydrogen solutions in supporting a global transition towards a circular economy and sustainable energy systems.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 250 million |

| Market Forecast in 2032 | USD 575 million |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Air Products and Chemicals Inc., Linde plc, SUEZ, Engie, Covanta Holding Corporation, Hitachi Zosen Inova AG, WasteFuel, LanzaTech, Topsoe A/S, Mitsubishi Heavy Industries Ltd., NextChem (Maire Tecnimont Group), Synova Power, REH2, Plastic Energy, Green Hydrogen International (GHI), HydrogenPro AS, Wood Group PLC, Waste Management Inc., Veolia Environnement S.A., Brightmark LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Waste to Hydrogen market is characterized by a dynamic and evolving technology landscape, primarily driven by innovation aimed at improving efficiency, scalability, and economic viability. The dominant technologies can be broadly categorized into thermochemical and biological conversion methods. Thermochemical processes, notably gasification and pyrolysis, are widely explored for their ability to handle a broad range of waste types, including mixed municipal solid waste, industrial refuse, and plastics. Gasification, which converts waste into a hydrogen-rich syngas at high temperatures with controlled oxygen or steam, is continually advancing with new reactor designs, such as fluid bed and circulating fluid bed systems, and enhanced gas cleaning and purification technologies to produce fuel-cell-grade hydrogen. Plasma arc gasification represents a high-temperature variant offering superior waste destruction and contaminant removal, producing high-quality syngas with minimal residues, albeit at higher energy inputs.

Pyrolysis, another thermochemical route, involves heating waste in the absence of oxygen to produce bio-oil, char, and syngas. While the primary product is often bio-oil, the syngas can be further processed to extract hydrogen. Recent advancements in catalytic pyrolysis are focusing on direct hydrogen production or higher yields of specific chemicals, improving the overall value proposition. Biological methods, such as anaerobic digestion and fermentation, are particularly suited for organic-rich waste streams like food waste, agricultural residues, and sewage sludge. Anaerobic digestion produces biogas, primarily methane and carbon dioxide, which can then be converted to hydrogen via steam methane reforming (SMR) or dry reforming. Fermentation directly produces hydrogen through microbial action, often at lower temperatures and pressures, presenting a more environmentally benign option, with ongoing research focused on enhancing microbial efficiency and hydrogen yield.

Beyond these core conversion technologies, the market is also seeing innovation in pre-treatment methods, critical for standardizing diverse waste feedstocks and optimizing conversion processes. This includes advanced sorting, drying, and size reduction techniques. Post-conversion, hydrogen purification technologies, such as pressure swing adsorption (PSA) and membrane separation, are vital for achieving the high purity required for various applications, especially fuel cells. Furthermore, the integration of carbon capture and utilization (CCU) technologies with waste-to-hydrogen plants is gaining traction to maximize the decarbonization impact by capturing CO2 produced during syngas processing. The trend is towards modular, decentralized plant designs that can be deployed closer to waste sources and hydrogen demand centers, reducing logistical costs and improving overall energy efficiency, making these technologies more accessible and economically attractive for a wider range of projects.

Waste to Hydrogen technology involves converting various types of waste materials, such as municipal solid waste, industrial byproducts, and agricultural residues, into hydrogen gas. This process utilizes advanced thermochemical methods like gasification and pyrolysis, or biological methods such as anaerobic digestion and fermentation, to generate clean hydrogen, simultaneously addressing waste management and clean energy demands.

The primary technologies for producing hydrogen from waste include thermal conversion methods such as gasification (converting waste into syngas at high temperatures with controlled oxygen/steam) and pyrolysis (thermal decomposition in the absence of oxygen). Biological methods like anaerobic digestion (producing biogas from organic waste, which is then reformed) and fermentation (direct hydrogen production by microbes) are also significant.

Waste to Hydrogen offers substantial environmental benefits, including significant reduction in landfill volumes and associated methane emissions, a potent greenhouse gas. It helps in the decarbonization of energy and industrial sectors by providing a clean hydrogen source, and it promotes a circular economy by valorizing materials that would otherwise contribute to pollution and waste accumulation.

The Waste to Hydrogen market faces challenges such as high initial capital investment, the complex and variable nature of waste feedstocks requiring extensive pre-treatment, the need for robust and reliable conversion technologies, and the nascent stage of hydrogen infrastructure development for storage and distribution. Public acceptance and competition from other hydrogen production methods also pose hurdles.

The Waste to Hydrogen market is projected for significant growth, driven by increasing global waste generation, stringent environmental regulations, supportive government policies for hydrogen and circular economy initiatives, and continuous technological advancements improving efficiency and reducing costs. Rising demand for clean hydrogen across transportation, industrial, and power generation sectors will further fuel its expansion towards a sustainable energy future.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.