ID : MRU_ 433284 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

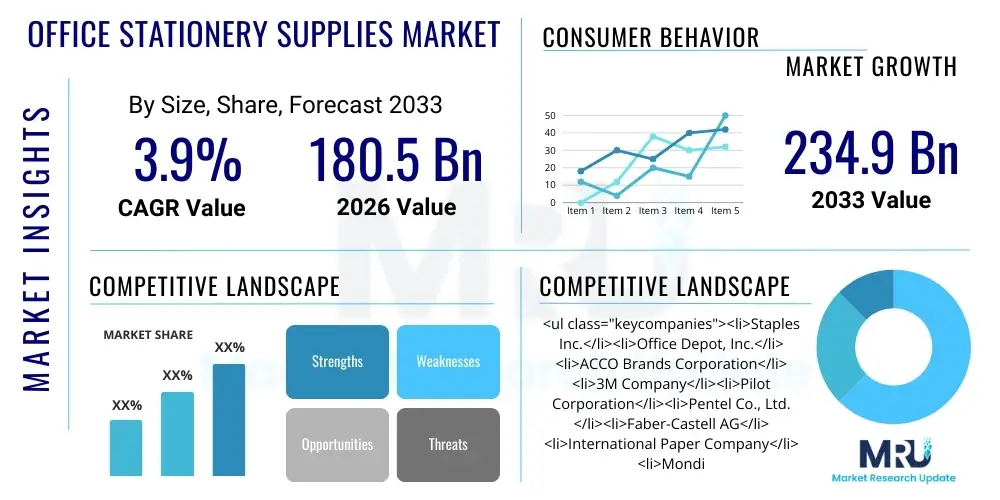

The Office Stationery Supplies Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.85% between 2026 and 2033. The market is estimated at $180.5 Billion in 2026 and is projected to reach $234.9 Billion by the end of the forecast period in 2033.

The Office Stationery Supplies Market encompasses a vast array of consumable and durable goods essential for organizational and administrative tasks across various settings, including corporate offices, educational institutions, government bodies, and home offices. This sector includes traditional paper products, writing instruments, filing and organization systems, technology accessories, and increasingly, specialized ergonomic and sustainable supplies. The market is fundamentally driven by ongoing commercial activities, administrative requirements, and the necessity for record-keeping, despite the increasing digitalization trends globally. Product offerings are continuously evolving to meet modern workplace demands, focusing on quality, efficiency, and environmental responsibility, thereby maintaining relevance even in paper-lite environments.

Major applications of office stationery supplies span documentation and printing, professional correspondence, organizational storage, planning, and artistic or design work. Key benefits derived from these supplies include enhanced workflow efficiency, improved organization, facilitation of effective communication, and maintenance of legal or operational records. Furthermore, high-quality stationery contributes significantly to brand image and employee satisfaction within corporate settings. The utility of these supplies extends beyond routine office tasks into specialized functions like drafting blueprints, specialized academic research documentation, and essential inventory management paperwork, ensuring the market's deep integration into global economic infrastructure.

Driving factors for market expansion include the sustained growth of the Small and Medium-sized Enterprise (SME) sector globally, which necessitates foundational administrative support; the robust expansion of the education sector, particularly in emerging economies; and the accelerating demand for eco-friendly and sustainable stationery products driven by corporate social responsibility (CSR) initiatives and stringent environmental regulations. The rise of the home office segment, spurred by widespread remote work adoption, has further diversified the distribution channels and product focus. Continuous innovation in product materials, packaging, and functional design ensures that the market remains dynamic and responsive to evolving professional needs.

The Office Stationery Supplies Market exhibits resilience despite digital disruption, pivoting towards value-added products, enhanced distribution logistics, and environmental compliance. Key business trends indicate a significant shift in consumer preferences from bulk purchasing of standard items to premium, sustainable, and technologically integrated supplies, such as smart notebooks and recycled paper goods. Manufacturers are focusing heavily on streamlining their supply chains to ensure faster delivery and greater inventory control, leveraging e-commerce platforms as the primary growth channel. Consolidation among major players is ongoing, aiming to achieve economies of scale and penetrate niche segments, particularly the rapidly expanding home office and creative workspace categories.

Regionally, the Asia Pacific (APAC) market is projected to lead growth, primarily fueled by urbanization, increasing foreign direct investment, and massive governmental and private spending on educational infrastructure. North America and Europe, while mature, demonstrate stable demand driven by the replacement cycle, demand for high-end organization tools, and stringent adherence to green procurement policies, pushing manufacturers to innovate materials. Latin America and the Middle East and Africa (MEA) are emerging as high-potential markets, driven by improving economic conditions and the establishment of new commercial hubs requiring foundational office setups, offering substantial opportunities for entry-level and mid-range products.

Segment trends highlight the sustained importance of paper products, though volumes are shifting towards higher-quality specialized papers and away from commodity printing paper. The writing instruments segment is benefiting from a resurgence in premium and artisanal pens used for professional gifting and personal expression. Crucially, the online distribution channel is dominating market growth, offering competitive pricing, vast product selection, and superior convenience compared to traditional brick-and-mortar office supply superstores. End-user analysis shows that corporate and educational institutions remain the largest consumers, but the home office segment is experiencing the fastest growth rate, compelling retailers to adjust their inventory stocking and marketing strategies.

Common user questions regarding AI's impact on the Office Stationery Supplies Market center on whether artificial intelligence and automation will render physical stationery obsolete, and conversely, how AI can optimize the supply chain for these products. Users are concerned about the future viability of traditional manufacturing processes versus demands for highly customized, on-demand supply fulfillment facilitated by AI-driven inventory management. The key themes revolve around supply chain efficiencies, personalized B2B procurement systems, and the potential for AI-generated insights to predict consumption patterns, thereby reducing waste and enhancing sustainability efforts. Expectations are high regarding AI's role in creating smart, connected office environments where stationery replenishment is entirely automated, minimizing administrative overhead and ensuring optimal stock levels.

The market is primarily driven by the expansion of the global service sector and the steady requirement for tangible documentation, which persists even in highly digitized environments due to legal and compliance necessities. Restraints primarily involve the accelerating adoption of digital substitutes, such as cloud storage and digital note-taking applications, which continually reduce the demand for high-volume paper and filing systems. Opportunities are significantly concentrated in the emerging markets of Asia and Africa, where infrastructure development is rampant, coupled with substantial growth opportunities in the high-margin segment of sustainable and premium office organizational tools. The combined effect of these forces shapes market pricing, competitive intensity, and the required pace of product innovation among major suppliers.

Driving factors include the globalization of business operations leading to increased cross-border documentation and the robust institutional demand from schools and universities globally, particularly for specialized writing and art supplies. Furthermore, regulatory frameworks in several jurisdictions mandate the maintenance of physical records for specific financial and legal transactions, creating a guaranteed baseline demand for paper and filing products. The proliferation of specialized office environments, such as co-working spaces and maker spaces, also generates tailored demand for unique stationery solutions beyond the standard corporate fare, driving product diversification and market expansion into niche sectors.

Impact forces are heavily weighted toward consumer preference shifts regarding sustainability and ethical sourcing. Companies that fail to adapt their product lines to include recycled content, biodegradable materials, or minimal packaging face significant reputational risk and market share erosion, especially in regulated European and North American markets. Conversely, the high cost of implementing circular economy practices and achieving various sustainability certifications acts as a short-term barrier for smaller manufacturers. The volatile price of key raw materials, particularly wood pulp, also exerts continuous pressure on profit margins, requiring manufacturers to employ sophisticated hedging strategies and optimized production techniques to maintain competitive pricing structures.

The Office Stationery Supplies Market is complex and highly fragmented, requiring detailed segmentation to understand underlying consumption patterns and growth pockets. Segmentation is fundamentally structured around product type, distribution channel, and end-user base, reflecting the diverse applications and procurement methods utilized across the professional landscape. The inherent maturity of certain segments, such as basic commodity paper, contrasts sharply with the high growth potential seen in specialized or sustainable product categories, necessitating targeted marketing and investment strategies from suppliers. Understanding the procurement lifecycle for each segment—from bulk institutional buying to individual e-commerce purchases—is paramount for strategic market penetration and accurate forecasting.

The value chain for office stationery supplies is relatively long, starting with raw material procurement and culminating in end-user consumption, with several critical intermediate steps determining final product quality and price competitiveness. Upstream analysis focuses heavily on the sourcing of key materials, primarily wood pulp for paper products, plastics for writing instruments and desk accessories, and specialized chemicals for inks and adhesives. Manufacturers must establish stable, sustainable relationships with material suppliers, often navigating commodity price volatility and increasing regulatory pressure regarding ethical sourcing and environmental impact. Efficiency in converting these raw materials into finished goods, emphasizing lean manufacturing techniques and automation, directly impacts profitability and market responsiveness.

The manufacturing process involves specialized production lines for high-volume items (like printer paper) and more artisanal or precision processes for complex goods (like high-quality pens or ergonomic desk tools). Once manufactured, downstream analysis focuses on inventory management, warehousing, and the crucial step of distribution. The market relies on sophisticated global logistics, utilizing large wholesalers, dedicated office supply distributors, and increasingly, integrated e-commerce fulfilment centers. The shift towards online purchasing has compressed the traditional distribution hierarchy, with large players often integrating vertically to manage their own warehousing and delivery logistics, improving speed and reducing costs for B2B contract clients.

Distribution channels are bifurcated into direct and indirect models. Direct channels involve manufacturers selling directly to large corporate clients or through their proprietary e-commerce portals, offering customized pricing and service contracts. Indirect channels utilize third-party retailers, hypermarkets, and specialized stationery stores, which provide wider geographical reach and cater more effectively to the SME and individual consumer segments. The growth of digital marketplaces has intensified competition in the indirect channel, demanding that suppliers offer comprehensive product data, high-resolution imagery, and reliable stock availability, fundamentally transforming how consumers discover and purchase office supplies.

The primary consumers and end-users of office stationery supplies are highly diverse, ranging from institutional purchasers with centralized procurement requirements to individual consumers making decentralized purchases for personal or home use. The largest volume buyers remain the Corporate Office segment, encompassing multinational corporations and SMEs, which require continuous replenishment of consumables like printer paper, toner, and basic filing systems to maintain daily operations. These entities typically prioritize volume discounts, contractual stability, and adherence to corporate sustainability mandates, making B2B relationships characterized by long-term supply agreements and rigorous service level agreements.

The Educational Institutions segment, including K-12 schools, universities, and vocational training centers, constitutes another massive consumer base, characterized by cyclical purchasing patterns tied to academic calendars. Demand from this segment is skewed toward specific products such as notebooks, student planners, bulk writing instruments, and specialized artistic or drafting supplies. Procurement in this sector often involves public tenders or large-scale institutional purchasing, where durability, safety standards, and cost-effectiveness are critical evaluation criteria for suppliers and distributors looking to secure large annual contracts.

Furthermore, the rapidly growing Home Office and Personal Use segment represents a critical emerging customer base, particularly accelerated by global shifts towards remote work. These individual consumers prioritize ergonomic design, aesthetics, brand identity, and convenience, often preferring premium, high-quality items over basic commodity supplies. They primarily utilize online retail channels for purchasing, valuing speed of delivery and ease of returns. The government and public sector also maintain significant demand, driven by bureaucratic necessity, standardized procurement processes, and often favoring suppliers who can meet strict socio-economic procurement goals, such as supporting minority-owned businesses or utilizing environmentally preferred products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $180.5 Billion |

| Market Forecast in 2033 | $234.9 Billion |

| Growth Rate | 3.85% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered |

|

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

While often perceived as a low-tech industry, the Office Stationery Supplies Market relies heavily on advanced manufacturing processes and digital technologies to optimize production, distribution, and product function. In manufacturing, precision engineering is paramount, particularly for complex products like high-quality writing instruments and specialized filing machinery. Technologies such as computer numerical control (CNC) machining and high-speed injection molding ensure consistent quality and mass production capabilities. Furthermore, advancements in material science, including the development of durable, sustainable, and lightweight recycled plastics and innovative ink formulations that are faster drying or water-resistant, drive product differentiation and respond to escalating consumer demands for eco-friendly performance.

In the digital realm, the key technological landscape is dominated by e-commerce platforms and sophisticated Enterprise Resource Planning (ERP) systems. Manufacturers and large distributors leverage advanced ERP and supply chain management (SCM) software to handle complex global logistics, track vast inventories across multiple warehouses, and manage B2B procurement contracts seamlessly. The implementation of Radio Frequency Identification (RFID) tags and barcode scanning technologies is becoming standard practice in large corporate supply environments to automate inventory tracking and reduce pilferage, enhancing operational efficiency for large organizational clients.

The consumer-facing technology landscape involves the integration of stationery with digital tools. This includes the proliferation of "smart" notebooks and planners that use embedded technology or specialized ink/paper systems (like N-code technology) to allow users to digitally scan, store, and organize handwritten notes via cloud services. This hybridization addresses the preference of many professionals for the tactile experience of writing while simultaneously meeting the necessity of digital archiving and sharing, thus bridging the gap between traditional supplies and modern digital workflows. This blend of physical and digital utility represents a significant technological avenue for premium market growth.

North America holds a substantial share of the global office stationery supplies market, characterized by high corporate density, advanced e-commerce penetration, and robust consumer awareness regarding product quality and brand reputation. The market here is mature but stable, driven primarily by the replacement cycle in large enterprises and the strong growth of the professional services sector. A crucial trend is the increasing demand for ergonomic and specialty office supplies catering to the permanently established hybrid work model, requiring personalized desk setups for both office and home environments.

The U.S. market, in particular, is highly competitive, dominated by large retailers and distributors like Staples and Office Depot, who are intensely focused on optimizing their omnichannel strategies. Sustainability is a non-negotiable factor; corporate buyers prioritize suppliers demonstrating clear commitments to sustainable forestry practices (e.g., FSC certification) and circular economy principles. Furthermore, high labor costs incentivize businesses to adopt efficient, durable products that reduce administrative time associated with frequent replacement or maintenance, contributing to the strong demand for premium writing and organizational systems.

The European market is defined by its rigorous regulatory environment concerning environmental standards and product safety, making it a global leader in sustainable stationery practices. Countries like Germany, France, and the UK demonstrate strong demand for ethically sourced and recycled paper products, and non-toxic, refillable writing instruments. Corporate procurement policies across the EU often feature "green procurement" mandates, driving the premiumization of the sustainable segment. The growth is moderate yet steady, supported by strong educational sectors and resilient SME growth across the Eurozone.

However, Europe is also leading the trend towards paper reduction in many administrative functions, posing a fundamental restraint on high-volume paper sales. Consequently, suppliers are pivoting their focus toward high-value, durable organizational tools and aesthetically pleasing desk accessories. The distribution landscape is fragmented, with strong regional players and specialized B2B suppliers maintaining significant local influence, often competing effectively against global mega-retailers by offering specialized customer service and bespoke supply solutions tailored to specific industries like legal or design firms.

APAC is the fastest-growing region globally, fueled by rapid industrialization, expanding commercial real estate markets, and massive investments in public and private education infrastructure, particularly in India, China, and Southeast Asia. The market here is characterized by high volume demand for commodity stationery and a growing, nascent demand for high-end, branded products driven by rising middle-class disposable incomes and the increasing presence of multinational corporations establishing regional headquarters.

The complexity of the APAC market stems from its diverse regulatory landscape and varied distribution challenges, ranging from sophisticated urban logistics in Japan and South Korea to infrastructural hurdles in more remote emerging areas. While price sensitivity remains high for commodity items, the market's sheer size and accelerating rate of new business formation provide unparalleled opportunities. E-commerce platforms, notably in China and India, are essential growth engines, effectively bypassing traditional, often inefficient, retail distribution networks and delivering supplies directly to businesses and individual consumers at scale.

The Latin American market is characterized by medium growth potential, often linked closely to economic stability and infrastructural spending in key countries like Brazil and Mexico. Demand is robust, driven by the expansion of the SME sector and a large, young student population. The market frequently favors locally manufactured or regionally distributed products due to import tariffs and complex logistics, presenting barriers to entry for external players unless established partnerships are formed.

A key trend is the slow but steady adoption of digital procurement systems, replacing cash-based or highly decentralized purchasing. While sustainability consciousness is emerging, price remains the primary determinant for bulk purchasing decisions across many sectors. Investment in modern supply chain infrastructure and localized inventory stocking is crucial for manufacturers seeking to gain a competitive edge in this fragmented and often volatile regional market.

The MEA region is exhibiting strong potential, primarily driven by large government infrastructure projects, the establishment of economic free zones, and rapidly growing education enrollments in key Gulf Cooperation Council (GCC) countries and parts of North Africa. The demand for modern, high-quality office setups is directly correlated with foreign investment and the establishment of international business centers.

The stationery market in the GCC often emphasizes premium, branded products reflective of the region's focus on high-end corporate environments. Africa, conversely, presents a large, largely untapped market where basic, durable, and affordable supplies are paramount. Logistics remains a major challenge across sub-Saharan Africa, necessitating localized partnerships and robust distributor networks to ensure consistent supply chain reliability, making market entry complex but highly rewarding for well-prepared international suppliers focusing on long-term growth.

Staples Inc. is a globally recognized retailer and distributor, primarily operating in North America, focusing on office products, technology services, and business solutions. The company has strategically shifted focus from large-format retail stores to a robust B2B delivery model and e-commerce platform, ensuring seamless contractual supply management for large corporate and educational accounts. Staples emphasizes an expansive private label portfolio alongside national brands, leveraging strong procurement power and advanced logistics to maintain competitive pricing and fulfillment speed.

Office Depot, Inc. is a major integrated business services and product provider offering a vast range of stationery, technology, and facility supplies across retail, online, and B2B contract channels. The company has prioritized diversifying its service offerings, moving beyond traditional stationery into high-growth areas like tech support, printing solutions, and managed IT services to secure larger corporate partnerships and increase customer lifetime value. Their strategic focus includes enhancing their digital capabilities to streamline the complex procurement needs of hybrid working environments.

ACCO Brands Corporation is a leading designer, marketer, and manufacturer of branded academic, consumer, and business products worldwide, owning globally recognized names like Swingline, Five Star, GBC, and Kensington. The company excels in high-margin segments like filing, organizational systems, and specialized presentation equipment, maintaining strong market positions in both North America and Europe. ACCO's growth strategy centers on strategic brand acquisitions and continuous innovation in product design, particularly emphasizing durability and aesthetic appeal for modern workspaces.

3M Company is a diversified technology company renowned for its innovative products, notably the Post-it Notes and Scotch brands, which dominate the adhesive and organizational category within the stationery market. 3M's strength lies in its extensive material science expertise, enabling the creation of unique, high-performance office supplies that transcend commodity status. Their market strategy focuses on leveraging their global R&D capabilities to continuously introduce innovative, functional office solutions that integrate seamlessly into daily workflow processes.

Pilot Corporation is a global leader in writing instruments, headquartered in Japan, famous for high-quality, refillable pens, and innovative ink technologies such as the FriXion erasable pens. Pilot maintains a strong brand reputation built on precision engineering, reliability, and environmental stewardship through refill programs. Their market success is driven by a deep understanding of writing culture and continuous technological advancements in ink flow systems and ergonomic design, securing leading positions in both professional and educational markets worldwide.

Pentel Co., Ltd., another Japanese powerhouse in writing instruments, is celebrated for its mechanical pencils, markers, and specialized art supplies, known for exceptional quality and durability. Pentel holds key patents in rollerball and gel pen technology, positioning them as a top choice for technical and artistic professionals. The company strategically focuses on maintaining high manufacturing standards and promoting products that offer superior writing experiences, ensuring strong loyalty among niche and mass-market consumers alike.

Faber-Castell AG, a long-established German manufacturer, specializes in premium writing instruments, pencils, and professional art materials, boasting a rich heritage dating back centuries. They are globally recognized for their commitment to sustainable forest management, ensuring that their pencils are sourced from certified, environmentally responsible operations. Faber-Castell targets the high-end consumer and professional art segments, where brand pedigree, material quality, and environmental ethics are critical purchasing factors.

International Paper Company is the world's largest paper and packaging company, serving as a critical upstream supplier of pulp and uncoated free sheet paper essential for the stationery market, particularly printer paper and notebooks. Their market influence stems from economies of scale and control over key raw material supplies. The company is actively investing in sustainable forest management and manufacturing efficiencies to address the market's increasing demands for environmentally certified paper products.

Mondi Group, a multinational packaging and paper company based in the UK and South Africa, supplies sustainable paper and packaging solutions to commercial and industrial customers globally. Mondi plays a crucial role in the office supplies value chain by providing high-quality, specialized office papers and innovative packaging solutions that contribute to the sustainability profiles of finished stationery products. Their strategic focus is on vertical integration and developing biodegradable packaging materials.

KOKUYO Co., Ltd. is a dominant Japanese manufacturer offering a wide range of office products, furniture, and stationery, with a strong focus on innovative organizational tools and aesthetically pleasing desk accessories. KOKUYO is known for highly functional, design-led products that appeal to the discerning modern worker, emphasizing organization, minimalism, and integration into efficient office layouts. Their strategy involves expansion across Asia and capitalizing on design leadership.

Dixon Ticonderoga Company is best known for its iconic Ticonderoga pencil brand, a staple in the North American education sector. The company specializes in writing and art materials, maintaining a strong foothold in the educational and creative segments. Their market approach leverages the established brand recognition and targets institutional purchasing contracts, emphasizing reliability and value in their core product lines.

AmazonBasics represents Amazon's extensive private-label brand, offering a wide array of generic, functional office supplies, cables, and basic equipment at highly competitive prices. The brand utilizes Amazon's vast e-commerce reach and data analytics to quickly identify high-demand, low-differentiation products, providing a cost-effective alternative to national brands and placing significant downward pressure on commodity pricing across the online market.

W.B. Mason Co., Inc. is one of the largest privately held office product dealers in the United States, known for its personalized, highly efficient B2B direct delivery service model. They compete effectively against national superstores by offering superior local customer service, rapid delivery, and customized supply solutions, establishing strong, long-term relationships with mid-to-large-sized regional businesses.

BIC Corporation is a French-based global manufacturer famous for its high-volume, affordable writing instruments (pens, markers, correction fluids), lighters, and shavers. BIC dominates the mass-market, convenience-driven segment, prioritizing cost-effectiveness, reliability, and wide distribution across retail channels globally. Their strategic advantage lies in their massive production scale and powerful brand recognition in developing and developed markets.

Lamy GmbH, a German manufacturer, is distinguished by its modern design philosophy and commitment to high-quality fountain pens and luxury writing instruments. Lamy successfully bridges the gap between functional writing tools and design accessories, appealing strongly to professionals, architects, and designers globally. Their focus on distinctive industrial design and premium materials allows them to command high-margin sales in specialized retail and professional gifting markets.

Ryman Group is a prominent UK-based high-street retailer specializing in stationery, office supplies, and business services, operating a significant number of physical stores alongside a growing online presence. Ryman targets both consumers and SMEs, leveraging convenient high-street locations and a diverse product range that includes technology accessories and printing services, maintaining a strong regional footprint in the competitive UK market.

Daiso Industries Co., Ltd., the Japanese dollar store giant, offers an enormous volume of affordable, non-premium office stationery and organizational supplies globally. While their products are low-cost, their immense scale and high store density, particularly in Asia, make them a significant volume player that influences pricing and consumer expectations in the economy segment of the market.

Schwan-STABILO is a German group famous for its STABILO brand of highlighters, pens, and colored pencils, holding a dominant position in the European educational and creative segments. They are recognized for their bright colors, ergonomic design, and durability. The group maintains a sharp focus on innovation within the writing and coloring category, often introducing products that cater to specific user needs like children's early writing or professional illustrating.

Lyreco SAS is a major global distributor of office supplies and workplace solutions, operating primarily through direct B2B contractual relationships across numerous countries. Lyreco excels in integrated supply chain management, offering comprehensive solutions that include safety products, catering supplies, and sustainability reporting for large international clients, focusing heavily on reliable, consolidated procurement services.

Corporate Express, often operating under various parent company structures (historically owned by Staples or other large entities), specializes in B2B distribution and contractual supply, primarily targeting large governmental and corporate accounts with complex, centralized procurement needs. Their expertise lies in large-scale logistics, customized catalog creation, and efficient desktop delivery services tailored to enterprise environments.

Demand for sustainable stationery is driven by stringent environmental regulations in North America and Europe, widespread corporate social responsibility (CSR) mandates requiring green procurement, and increasing consumer awareness regarding the ecological impact of traditional paper and plastic use. This push favors recycled, biodegradable, and ethically sourced office supplies.

The home office boom has significantly shifted market distribution dominance to the online retail channel. Individual remote workers prioritize convenience, quick delivery, and personalized shopping experiences offered by e-commerce platforms, leading distributors to invest heavily in robust "last mile" delivery logistics and optimized inventory stocking for smaller, individualized orders.

The Asia Pacific (APAC) region offers the highest growth potential, fueled by massive population growth, expanding industrialization, urbanization, and continuous government investment in the educational infrastructure across key economies like China, India, and Southeast Asia. This creates vast, unmet demand for both commodity and specialized office products.

No, while digitalization restrains the growth of commodity paper volume, it is not expected to eliminate demand entirely. Physical stationery remains essential for legal documentation, compliance requirements, short-term note-taking, and professional correspondence. The market is adapting by shifting focus towards high-quality, specialized paper and organizational systems rather than basic consumables.

Smart stationery, such as digitally integrated notebooks and pens (e.g., N-code technology), bridges the gap between traditional writing and digital archiving. These hybrid products cater to professionals who prefer the tactile experience of physical writing but require the organizational and sharing efficiency of cloud storage, positioning them as a key growth area in the premium segment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.