ID : MRU_ 436495 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

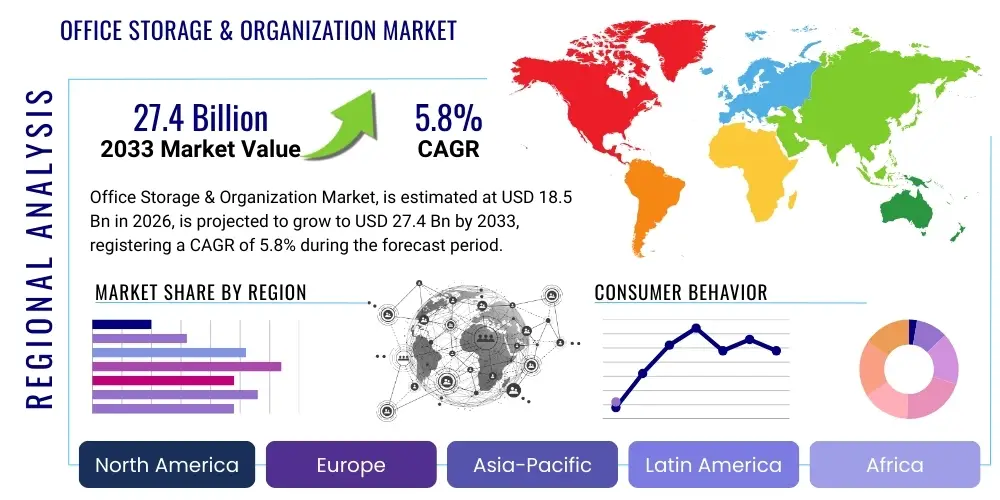

The Office Storage & Organization Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 27.4 Billion by the end of the forecast period in 2033.

The Office Storage & Organization Market encompasses a wide range of furniture and accessories designed to enhance efficiency, maximize space utilization, and maintain order within commercial and home office environments. This market includes essential products such as filing cabinets, shelving units, desk organizers, archival storage systems, and modular solutions. The core function of these products is to manage physical documents, supplies, and equipment effectively, thereby contributing directly to improved workflow and employee productivity across various sectors. The inherent complexity of modern business operations, which often involves a mix of physical records and digital assets, necessitates robust and flexible storage infrastructure.

Major applications for office storage and organization products span corporate headquarters, small and medium-sized enterprises (SMEs), educational institutions, healthcare facilities, and increasingly, dedicated home offices supporting the hybrid work model. The primary benefits derived from these solutions include reduced clutter, easier retrieval of critical information, compliance with data retention regulations, and the creation of aesthetically pleasing and ergonomic workspaces. Furthermore, modern solutions often incorporate features like mobility, modularity, and integrated charging capabilities, reflecting the evolving needs of flexible office layouts and technology integration within the workspace.

Key driving factors accelerating the growth of this market include the global expansion of commercial real estate, particularly in emerging economies, alongside a renewed focus on workplace wellness and ergonomic design. Although digitization continues to reduce the volume of physical paperwork, regulatory mandates requiring long-term archival of certain documents (e.g., legal, financial, and medical records) sustain demand for high-quality, secure storage solutions. Additionally, the proliferation of specialized equipment and supplies in collaborative workspaces drives the need for optimized organization systems that support shared resources effectively and minimize operational downtime.

The Office Storage & Organization Market is experiencing significant transformation, driven primarily by shifts in corporate real estate strategies and the widespread adoption of hybrid work models. Business trends indicate a movement away from traditional, bulky storage towards flexible, modular, and aesthetically integrated solutions that blend seamlessly into open-plan offices and sophisticated home office setups. Manufacturers are focusing heavily on design innovation, incorporating features such as acoustic dampening materials, integrated technology ports, and personalized storage lockers to cater to the transient nature of modern office attendance. This move ensures that physical storage remains relevant even as digital adoption accelerates, serving critical roles in space division and personal security.

Regionally, the Asia Pacific (APAC) market is poised for the fastest growth, underpinned by rapid urbanization, significant infrastructure development, and the establishment of numerous multinational corporation (MNC) offices, particularly in countries like China and India. North America and Europe, while mature, maintain strong market shares characterized by high demand for premium, sustainable, and technologically advanced storage solutions, often incorporating smart features like electronic locks and inventory tracking systems. Regulatory pressures regarding material sourcing and product lifecycle management are particularly influential in these Western markets, pushing manufacturers towards eco-friendly and circular economy models.

Segment trends highlight strong performance in the modular storage and mobile filing segments, reflecting the need for easily reconfigurable office spaces. Demand for high-security storage, particularly within the banking, financial services, and insurance (BFSI) and legal sectors, remains robust. Furthermore, the ‘Home Office’ end-user segment has grown exponentially, favoring solutions that are dual-purpose, compact, and design-forward, blurring the lines between functional office equipment and residential furniture. Material segmentation shows a growing preference for engineered wood and sustainable plastics over traditional metal cabinets, driven by aesthetic considerations and environmental commitments from corporate buyers.

Common user questions regarding AI's impact on office storage typically revolve around whether AI will completely eliminate the need for physical storage, how smart systems can automate physical asset tracking, and what role AI plays in optimizing the layout and usage of existing storage infrastructure. Users are concerned about the investment needed for integration and the potential redundancy of current physical organization systems. The key themes summarized from this analysis indicate that while AI does not directly replace physical storage, it profoundly changes how storage is managed, accessed, and optimized. AI is expected to significantly reduce misfiling errors and dramatically improve retrieval times by integrating digital inventory with physical location tracking, thereby making the remaining physical storage assets maximally efficient and secure.

AI's primary influence will be in driving the demand for 'smart storage' systems that are interconnected and responsive to organizational workflows. AI algorithms can predict future storage needs based on archival rates and operational cycles, advising facilities managers on optimal stock levels and appropriate storage unit deployment. This predictive capability minimizes wasted space and reduces capital expenditure on unnecessary storage units. Furthermore, in environments such as libraries or large corporate archives, AI-driven robotics and automated retrieval systems, managed by sophisticated software, are streamlining processes that were historically labor-intensive, ensuring that the physical handling of documents is precise and efficient.

The transition is not towards zero physical storage, but towards highly intelligent, integrated storage solutions. AI enables advanced security protocols, analyzing access patterns and flagging anomalous behavior in real-time, greatly enhancing the security of sensitive physical documents. The impact analysis concludes that AI acts as an efficiency multiplier, supporting the strategic management of physical assets within a largely digital workflow, demanding higher quality, connectivity, and data feedback loops from storage products themselves.

The dynamics of the Office Storage & Organization Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming significant impact forces. The primary drivers are centered on the necessity for organizational efficiency, enhanced security protocols for physical documents, and the sustained growth of the commercial sector globally, demanding aesthetically appealing and ergonomic workspaces. Restraints primarily involve the accelerating trend of digitization and cloud storage adoption, which continuously threatens the overall volume demand for traditional physical storage units, coupled with the high initial investment required for advanced, automated storage systems. Opportunities are identified in smart technology integration, offering enhanced management features, and the powerful sustainability movement, requiring manufacturers to develop durable, recyclable, and low-impact storage products that appeal to corporate social responsibility mandates.

The most significant impact force on the market is the ongoing paradigm shift towards flexible, activity-based working (ABW) environments. This shift compels companies to replace fixed, personalized storage with shared, high-density, and often mobile solutions, such as centralized locker systems and communal filing units. This structural change demands innovation in product design, focusing on modularity and adaptability, thereby increasing the value proposition of modern organization systems beyond mere containment. Furthermore, increasing regulatory requirements across industries, such as GDPR and sector-specific data retention laws, act as a constant driver for secure, auditable, and compliant physical storage options, ensuring that even in a digital age, certain records must be securely archived physically.

Market stakeholders must strategically navigate the balance between cost optimization and technological integration. The ability to integrate storage furniture seamlessly with office technology (e.g., smart locks, mobile application access, integrated power solutions) determines market leadership. The overall impact force matrix suggests that while digitization exerts downward pressure on volume, it concurrently elevates the demand for value-added, smart, and premium storage solutions that function as sophisticated tools for organizational management rather than simple containers, thereby maintaining positive revenue growth in the long term.

The Office Storage & Organization Market is systematically segmented across various dimensions, including product type, material, end-user, and distribution channel, providing a comprehensive view of consumer behavior and market penetration. Product segmentation is crucial, differentiating between high-volume standard items (like filing cabinets and standard shelving) and specialized, high-value systems (like mobile shelving and secure archival units). This differentiation helps manufacturers tailor production and marketing efforts to specific functional needs. Material segmentation, covering metal, wood, plastic, and composite materials, reflects buyer priorities related to durability, cost, and aesthetic integration within the workspace design.

End-user analysis is particularly important for strategic market targeting. Corporate offices remain the largest segment, but the growth rate in the Institutional segment (government, healthcare, education) is stable due to mandatory archival needs. The fastest-growing segment is the Home Office, demanding specialized, compact, and multi-functional organization solutions that prioritize aesthetics and residential integration. Furthermore, distribution channels, encompassing B2B direct sales, retailer networks, and increasingly robust e-commerce platforms, dictate pricing strategies and logistical complexities across different regions, with e-commerce showing accelerated adoption due to convenience and wider product selection for smaller businesses and individual home office setups.

The Value Chain for the Office Storage & Organization Market commences with upstream activities involving the sourcing and processing of raw materials, primarily steel, specialized plastics, and engineered wood components. Raw material costs and stable supply relationships with high-quality metal fabricators and wood panel suppliers significantly influence the final product cost and manufacturing efficiency. Manufacturers must manage complex global supply chains to ensure compliance with quality standards and sustainable sourcing initiatives, particularly for wood products where certification (e.g., FSC) is increasingly mandated by corporate buyers. Price volatility in base metals remains a critical upstream risk factor that directly impacts manufacturer profitability and necessitates robust hedging strategies.

The midstream phase focuses on manufacturing and assembly, which includes high-precision metal fabrication, surface treatment (powder coating), lamination, and the integration of locking mechanisms and electronic components (for smart storage). Key differentiation occurs at this stage through modular design, quality control, and the deployment of lean manufacturing practices to reduce waste and improve throughput. High capital investment is required for automated machinery capable of producing durable, aesthetically complex products. Successful manufacturers leverage proprietary design patents and advanced tooling to ensure product longevity and competitive differentiation in the marketplace.

Downstream activities center on distribution and sales. The market relies heavily on a dual distribution channel: large B2B sales through dedicated contract furniture dealers and direct procurement for customized corporate fit-outs, and a growing retail channel supported by large office supply superstores and increasingly powerful e-commerce platforms. Direct and indirect sales methods serve different end-users; B2B channels typically handle bulk orders and bespoke solutions, while e-commerce targets SMEs and the home office segment efficiently. Strong after-sales service, including assembly, installation, and warranty provisions, completes the value delivery, driving customer loyalty and repeat corporate business.

The primary consumers and end-users of Office Storage & Organization products are highly diverse, spanning the entire commercial and institutional landscape. Corporate entities, ranging from large multinational corporations (MNCs) that require extensive centralized archival systems and sophisticated personal storage solutions (lockers), to small and medium-sized enterprises (SMEs) needing cost-effective, adaptable filing options, represent the largest customer base. These customers prioritize durability, security, and systems that seamlessly integrate into modern architectural designs, often procuring through specialized B2B contract furniture vendors for customized solutions.

Institutional customers constitute another critical segment, encompassing government agencies (federal, state, and local), educational establishments (universities, schools), and healthcare providers (hospitals, clinics). These sectors have unique, non-negotiable requirements for long-term document retention, robust security measures, and compliance with strict regulatory standards (e.g., HIPAA in healthcare). The demand here is often driven by tender processes and focuses on high-capacity, durable, often mobile archival systems capable of secure, long-term preservation of sensitive records.

The rapidly expanding segment of individual buyers, primarily supporting the Home Office setup, represents a significant growth vector. These customers value aesthetics, space efficiency, and dual functionality, often choosing products that resemble residential furniture while providing necessary organizational capabilities. Procurement in this segment is heavily driven by online retail, ease of assembly, and affordability, contrasting sharply with the B2B sector's focus on bespoke design and large-scale installation services.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 27.4 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Herman Miller (MillerKnoll), Steelcase Inc., Knoll Inc., Haworth, Inc., The HON Company, IKEA Systems B.V., Ricoh Company, Ltd., Godrej & Boyce Mfg. Co. Ltd., Bisley, Fellowes Brands, Acme Furniture Industry, Spacesaver Corporation, Kardex Remstar, Lista International, OFS Brands, Inc., Tennsco Corp., Sauder Woodworking Co., Kimball International, Inc., KI, Flexsteel Industries Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Office Storage & Organization Market is shifting from purely mechanical systems to integrated smart solutions, enhancing both security and management efficiency. Key technological adoption focuses primarily on Internet of Things (IoT) integration, enabling connectivity within storage units. This includes the implementation of smart locking systems that use biometric authentication or mobile app control, replacing traditional keys and greatly improving access security and audit trails. Furthermore, sensor technology is increasingly utilized for real-time occupancy monitoring of lockers and storage bays, allowing facilities managers to optimize space allocation dynamically in shared office environments. This shift aligns storage infrastructure with overall smart building management systems, contributing to operational intelligence.

Radio-Frequency Identification (RFID) and Near-Field Communication (NFC) technologies are central to advanced asset tracking within the storage domain. By tagging physical assets and documents, organizations can precisely locate items within complex shelving or archival systems, drastically reducing retrieval time and minimizing loss. This technology supports the transition to automated inventory management, where software monitors stock levels of supplies and alerts purchasing departments when replenishment is required, eliminating manual checks. The use of advanced materials science is also prominent, focusing on lightweight yet durable composites and modular construction techniques that facilitate easy reconfiguration and mobility of storage units without compromising structural integrity or requiring heavy tools for dismantling.

Further innovation is seen in the development of sophisticated mobile shelving systems (compactors) that utilize electronic controls and safety sensors, maximizing filing density in smaller footprints while ensuring user safety. The software layer controlling these systems often includes features for integration with organizational Enterprise Resource Planning (ERP) or Document Management Systems (DMS), allowing digital records to be cross-referenced with their physical storage location. This technological convergence ensures that physical storage systems are future-proofed, offering seamless integration into the digital workflows that dominate modern business environments, making them indispensable components of an intelligent workplace ecosystem.

Regional dynamics heavily influence the demand for specific types of office storage and organization products, reflecting differences in office culture, regulatory compliance, and economic development stages.

Hybrid work is shifting demand away from large, personalized storage units toward centralized, flexible solutions like high-density mobile shelving and personal employee lockers (hoteling storage). This change prioritizes shared resources and modular systems that maximize space utilization for fewer physical items.

Key advancements include the integration of IoT for smart locking mechanisms, biometric access control, and RFID technology for real-time asset tracking. These technologies enhance security, streamline inventory management, and integrate physical storage systems with digital workplace applications.

The Asia Pacific (APAC) region, driven by rapid urbanization, substantial growth in commercial real estate development, and expanding corporate presence, offers the most significant growth opportunities for both traditional high-capacity filing and new smart organization systems.

The primary constraint is the continuous acceleration of digitization and cloud storage adoption, which progressively reduces the volume of physical paperwork retained by organizations, thereby limiting the overall unit demand for standard, low-value storage products.

Sustainable office trends favor materials such as recycled steel, certified engineered wood (FSC certified), and recyclable plastics. Manufacturers are focusing on durable products with longer lifecycles and transparent sourcing to meet strict corporate social responsibility mandates.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.