ID : MRU_ 431562 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

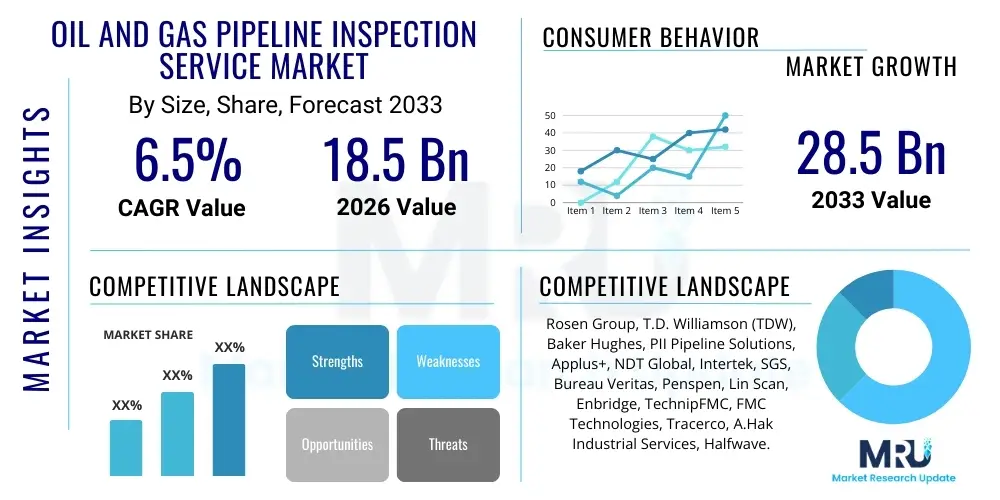

The Oil and Gas Pipeline Inspection Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 28.5 Billion by the end of the forecast period in 2033.

The Oil and Gas Pipeline Inspection Service Market encompasses specialized activities designed to ensure the structural integrity, safety, and operational efficiency of the vast global network of pipelines used for transporting crude oil, natural gas, and refined petroleum products. These services are crucial for preventing catastrophic failures, minimizing environmental damage, and adhering to stringent international regulatory standards. Key inspection services leverage advanced technologies such as Inline Inspection (ILI) tools, often referred to as 'smart PIGs,' as well as non-destructive testing (NDT) techniques like Magnetic Flux Leakage (MFL), Ultrasonic Testing (UT), and Eddy Current testing. The fundamental objective of these inspections is to detect, locate, and characterize pipeline anomalies, including corrosion, cracks, dents, material loss, and girth weld defects, enabling timely maintenance and repair interventions.

The primary product offerings in this sector revolve around comprehensive integrity management systems, which include initial data acquisition, sophisticated data analysis, risk assessment, and ultimately, prescribed preventative maintenance schedules. Major applications span across the entire pipeline lifecycle, from pre-commissioning assessments and baseline surveys to regular operational inspections and post-repair evaluations. Given the increasing age of global pipeline infrastructure, particularly in North America and Europe, the demand for sophisticated diagnostic and preventative inspection services is accelerating. Furthermore, the expansion of new, challenging pipeline projects in deepwater offshore environments and remote terrestrial locations necessitates highly reliable and accurate inspection technologies capable of operating under extreme pressures and temperatures.

Driving factors for market growth include the mandatory compliance with stricter governmental regulations globally, such as those imposed by agencies like the Pipeline and Hazardous Materials Safety Administration (PHMSA) in the U.S. and equivalent bodies in Europe and Asia Pacific. Additionally, the economic imperative to maximize asset life and reduce operational downtime strongly influences investment in proactive inspection services. The benefits derived from these services are substantial: enhanced public safety, reduced operational expenditure through optimized repair strategies, prevention of costly environmental penalties, and guaranteed continuity of energy supply. The convergence of digital transformation, including the integration of real-time data monitoring and AI-driven predictive analytics, is rapidly redefining service capabilities and driving market expansion.

The global Oil and Gas Pipeline Inspection Service Market is experiencing robust growth driven primarily by escalating regulatory pressures concerning pipeline safety and the critical need for asset life extension amid aging infrastructure. Business trends indicate a strong shift toward digitalization, where service providers are integrating specialized software platforms for real-time data interpretation, digital twinning, and predictive maintenance scheduling. There is a noticeable consolidation among leading market players who are acquiring smaller technology specialists to enhance their capabilities in advanced data analysis (Level 3 inspection) and specialized techniques like acoustic resonance testing. Furthermore, the market is characterized by long-term service agreements (LTSAs) between inspection firms and major pipeline operators, ensuring stable revenue streams and continuous demand for recurrent inspection cycles.

Regional trends show North America maintaining dominance due to its extensive network of aging transmission pipelines and rigorous enforcement of integrity management regulations. However, the Asia Pacific region, particularly China, India, and Southeast Asia, is projected to exhibit the highest CAGR, propelled by new pipeline construction for expanding natural gas distribution networks and the requirement for baseline inspections. The Middle East and Africa (MEA) region also presents significant opportunities, fueled by large-scale upstream oil projects and the need to inspect critical export infrastructure in harsh desert and offshore environments. European markets are focusing heavily on transition pipeline integrity management, particularly those handling gas destined for consumption across the continent, prioritizing methane emissions detection alongside structural integrity.

Segment trends reveal that the Inline Inspection (ILI) segment, specifically utilizing advanced smart PIG technology (e.g., Ultra-High Resolution MFL and Phased Array UT), accounts for the largest market share owing to its superior detection capabilities and comprehensive coverage. Within end-users, the natural gas segment is rapidly gaining ground against the traditional crude oil segment, driven by the global transition towards cleaner energy sources and the associated expansion of high-pressure gas transmission lines. The demand for non-metallic pipeline inspection services is also emerging as composites gain popularity in challenging environments. The focus is increasingly shifting from mere defect detection to accurate defect sizing and remaining life estimation, necessitating highly sophisticated analytical tools and skilled technicians.

Common user inquiries regarding AI's influence in pipeline inspection center on how artificial intelligence can move beyond simple data storage to genuinely revolutionize operational efficiency, reduce human error in defect identification, and enable truly predictive maintenance. Key concerns revolve around the accuracy and reliability of automated defect recognition (ADR) algorithms, the required quality and volume of training data, and the integration complexity with legacy inspection hardware (PIGs). Users seek clarity on AI's capability to analyze unstructured inspection data (e.g., complex MFL signals and UT waveforms) across different pipeline materials and conditions, ultimately expecting AI to provide deeper insights into corrosion growth rates and metal fatigue, significantly lowering overall operational risks and costs associated with manual data review.

The market dynamics are defined by a complex interplay of Drivers (D), Restraints (R), Opportunities (O), and associated Impact Forces. The primary drivers include the stringent enforcement of safety regulations globally, the advanced age profile of existing pipeline infrastructure necessitating constant monitoring, and the rising concerns over environmental safety and potential liability stemming from pipeline failures. These factors collectively create a non-negotiable demand for sophisticated inspection technologies that can reliably assess structural integrity. However, the high capital expenditure required for advanced ILI tools, the technical challenges associated with inspecting "unpiggable" pipelines (due to low flow or complex geometry), and the persistent shortage of highly specialized data analysts act as significant restraints on market expansion and service deployment, particularly for smaller operators.

Opportunities for growth are largely concentrated in the technological domain. The development of non-metallic pipeline inspection solutions, the miniaturization of sensors for enhanced accuracy, and the integration of cloud-based platforms for real-time data visualization present substantial avenues for innovation and market penetration. Furthermore, emerging markets in Asia and Latin America, characterized by rapid urbanization and corresponding expansion of energy distribution networks, offer robust opportunities for baseline and initial integrity inspection services. The shift toward utilizing drones and unmanned systems for external pipeline monitoring, particularly leak detection and right-of-way surveillance, also opens new service lines, enhancing efficiency and accessibility.

Impact forces currently shaping the market include technological advancements, which consistently push the boundaries of achievable detection accuracy and coverage. Regulatory mandates act as a crucial external force, ensuring continuous investment regardless of short-term commodity price fluctuations. Economic forces, tied to the volatility of crude oil and gas prices, periodically affect capital spending decisions, impacting the uptake of high-cost, cutting-edge services. Finally, environmental and social governance (ESG) factors are exerting increasing pressure on operators to prioritize safety and sustainability, making comprehensive inspection a core element of corporate responsibility, thereby sustaining long-term market demand.

The Oil and Gas Pipeline Inspection Service Market is critically segmented based on technology, service type, end-use application, and pipeline location, reflecting the diverse operational requirements across the energy sector. Segmentation by technology is the most pivotal, distinguishing between intrusive methods like Inline Inspection (ILI) and non-intrusive External/Non-Destructive Testing (NDT) techniques. The Inline Inspection segment dominates due to its ability to perform comprehensive internal assessments of critical defects over long distances. Service type segmentation differentiates the market based on the function performed, ranging from routine inspection and monitoring to complex repair and maintenance services, often provided as part of an integrated integrity management contract. Understanding these segments is vital for service providers to tailor specialized tools and expertise to address specific challenges, such as stress corrosion cracking in older lines or buckling in deepwater flexibles.

Segmentation by end-use application distinguishes between crude oil pipelines, natural gas pipelines, and refined product pipelines. Each commodity presents unique challenges—for instance, natural gas pipelines require specialized focus on stress corrosion cracking (SCC) and methane leak detection, while crude oil lines demand robust solutions for corrosion and wax deposition monitoring. Geographically, the market is split between Onshore and Offshore environments, with offshore services commanding higher pricing due to operational complexities, deep-sea pressures, and the required use of marine vessels and specialized subsea inspection robotics. The combination of these segments dictates pricing structures, regulatory compliance requirements, and the technological readiness level necessary for market participation.

The continuous refinement of segmentation helps in addressing niche market requirements, such as the growing demand for specialized inspection of smaller diameter distribution lines or the high-pressure, high-temperature (HPHT) segment. Operators are increasingly looking for customized solutions rather than generic inspection protocols, driving service providers to specialize further in areas like fitness-for-purpose assessments and probabilistic risk modeling, which sit at the intersection of inspection and analytical services. This trend validates the increasing complexity of market offerings and the necessity for detailed segment tracking to capture accurate market share dynamics.

The value chain of the Oil and Gas Pipeline Inspection Service Market is intricate, involving specialized upstream technology developers, service execution providers, and downstream data interpreters and end-users. Upstream analysis focuses on the manufacturing and continuous innovation of highly specialized inspection tools, particularly smart PIGs and sensor technology. This phase requires significant investment in R&D for developing high-resolution sensors, robust mechanical structures capable of traversing complex pipeline geometries, and advanced data acquisition electronics. Key participants in this stage include specialized engineering firms and technology providers who often hold critical intellectual property related to defect detection algorithms (e.g., MFL signature interpretation for pitting corrosion). The efficiency and accuracy achieved in the upstream manufacturing phase directly determine the quality and cost-effectiveness of the overall service offering.

The core of the value chain is the service execution phase (midstream), where the inspection PIGs are run through the pipeline or external inspection tools (such as NDT devices or ROVs) are deployed. This involves rigorous project management, logistics planning, field mobilization, and the actual physical operation of the inspection run. Critical factors here include managing flow constraints, ensuring PIG passage (piggability), and collecting clean, comprehensive data. Service providers specializing in deployment and field operations form the backbone of this segment. Distribution channels are predominantly direct, involving long-term contracts established directly between the inspection service company and the pipeline owner/operator (the end-user). Indirect channels are less common but may include engineering procurement and construction (EPC) firms that incorporate inspection services into broader infrastructure projects.

Downstream analysis involves the crucial process of data analysis, integrity assessment, and reporting. Raw data collected from the field must be processed, cleaned, analyzed by certified Level 3 analysts, and translated into actionable maintenance recommendations. This highly specialized step adds significant value, transforming raw signals into concrete insights regarding pipeline integrity, remaining life, and required repair prioritization. Technology platforms for data management and visualization, often cloud-based, are essential for efficient delivery. The final end-user (pipeline operator) then leverages this detailed report to implement scheduled repairs, validating the entire service loop and justifying the investment. The integration of AI/ML tools into this downstream analysis phase is rapidly becoming a competitive differentiator, streamlining the interpretation process and enhancing predictive capabilities.

Potential customers for Oil and Gas Pipeline Inspection Services are primarily the owners and operators responsible for maintaining the safety and efficiency of hydrocarbon transport infrastructure globally. These customers fall into several distinct categories based on their operational scope and the type of commodity they handle. Major International Oil Companies (IOCs) and National Oil Companies (NOCs), such as ExxonMobil, Saudi Aramco, Sinopec, and Gazprom, represent the largest and most frequent buyers, requiring inspection services for vast networks spanning upstream, midstream, and downstream operations, including complex offshore segments and long-distance export pipelines. Their demand is driven by regulatory compliance and the need to protect enormous asset bases, typically resulting in multi-year integrity management contracts.

Midstream pipeline operators and transmission companies constitute another crucial customer segment. Companies like Enbridge, Kinder Morgan, TransCanada (TC Energy), and specialized gas distribution utilities focus exclusively on the movement of hydrocarbons across jurisdictions. Their procurement decisions are heavily influenced by federal and regional regulatory bodies (e.g., PHMSA, CER), prioritizing inspection technologies that meet rigorous safety standards and provide high confidence in defect characterization. These operators often seek turnkey solutions that encompass inspection, data analysis, and long-term risk modeling to ensure continuous operational uptime and safety compliance, viewing inspection as a critical operational expenditure rather than discretionary capital spending.

In addition to large corporations, smaller independent pipeline and utility companies, particularly those involved in localized distribution of natural gas, are increasingly becoming customers, driven by expanding distribution networks and heightened public safety scrutiny. Furthermore, refineries and petrochemical complexes often require specialized inspection for associated short-run pipelines and in-plant piping systems, though these requirements differ in scale and technology from large transmission line inspections. The key factor uniting all these potential customers is the mandatory requirement to maintain asset integrity to prevent catastrophic incidents, environmental harm, and business interruption, making the inspection service market relatively resilient to short-term economic fluctuations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 28.5 Billion |

| Growth Rate | CAGR 6.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Rosen Group, T.D. Williamson (TDW), Baker Hughes, PII Pipeline Solutions, Applus+, NDT Global, Intertek, SGS, Bureau Veritas, Penspen, Lin Scan, Enbridge, TechnipFMC, FMC Technologies, Tracerco, A.Hak Industrial Services, Halfwave. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the pipeline inspection market is defined by continuous innovation aimed at increasing detection accuracy, enhancing speed, and overcoming complex operational constraints like multi-diameter pipelines and low-flow systems. The dominant technology remains Inline Inspection (ILI), utilizing specialized "smart PIGs." Within ILI, Magnetic Flux Leakage (MFL) remains the workhorse for detecting metal loss (corrosion, pitting), with the trend shifting towards Ultra-High Resolution (UHR) MFL to accurately size smaller defects. Ultrasonic Testing (UT), particularly Phased Array UT and Circumferential UT (C-UT), is gaining prominence as it offers superior sizing of defects, specifically focusing on cracks, stress corrosion cracking (SCC), and laminations, overcoming the inherent limitations of MFL in crack detection. These PIGs are increasingly equipped with inertial measurement units (IMUs) and GPS integration to provide highly accurate mapping of defect locations.

Outside of ILI, the market is rapidly adopting advanced non-destructive testing (NDT) techniques for specific applications, particularly in unpiggable lines or localized integrity checks. Key emerging NDT technologies include Advanced Ultrasonic Backscatter Technique (AUBT), Long Range Ultrasonic Testing (LRUT), and Guided Wave Testing (GWT), which can screen long segments of pipe from a single location. Furthermore, fiber optic sensing systems, which are permanently installed along the pipeline, are utilized for continuous, real-time monitoring of strain, temperature, and leak detection, moving the industry toward preventative, 24/7 monitoring capabilities rather than episodic inspections. The technological advancements are largely focused on ensuring that inspection tools can handle higher pressures, temperatures, and operate reliably in environments like deepwater pipelines.

The digitalization layer sits atop these hardware advancements. This involves integrating sensors with high-speed data acquisition systems and applying sophisticated data processing algorithms. The deployment of robotics, including specialized tethered crawlers and autonomous underwater vehicles (AUVs) equipped with UT or Eddy Current sensors, is transforming offshore and terminal inspection capabilities. The overarching technological trend is the transition from purely mechanical and signal-processing inspection tools to fully integrated cyber-physical systems that leverage cloud computing, artificial intelligence, and sophisticated data visualization platforms to provide faster, more detailed, and predictive integrity assessments. These technological developments are critical to meeting evolving regulatory demands for heightened safety standards and proactive risk mitigation.

Inline Inspection (ILI), often utilizing 'smart PIGs' (Pipeline Inspection Gauges), is the process of sending automated instruments through the pipeline interior. It is preferred because it can cover long distances quickly, collect comprehensive internal data on corrosion and cracking (e.g., MFL, UT), and assess the pipeline under operational conditions, providing a full volumetric survey of the pipe wall.

AI significantly impacts integrity management by enabling Automated Defect Recognition (ADR), which accelerates data processing and reduces human error. Robotics, particularly drones and specialized crawlers, enhance accessibility to traditionally 'unpiggable' lines and remote offshore infrastructure, improving the frequency and quality of external visual and NDT data collection.

'Unpiggable' pipelines face challenges due to complex geometries, multi-diameter sections, low flow rates, or lack of launching and receiving facilities. Inspection providers overcome this using advanced methods like tethered robotic crawlers, external NDT techniques (LRUT), or specialized low-flow/bi-directional PIG technologies that adapt to non-standard operational parameters.

North America leads the global demand for pipeline inspection services, primarily due to its vast, mature pipeline infrastructure and exceptionally rigorous regulatory framework, particularly concerning pipeline safety and integrity management mandates enforced by organizations like PHMSA in the United States.

Key regulatory drivers include the global push for mandatory integrity management programs, stricter enforcement of regulations requiring precise defect sizing and crack detection (e.g., following recent global pipeline failures), and legislative moves emphasizing environmental protection, particularly methane emissions detection and control in gas transmission lines.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.