ID : MRU_ 434897 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

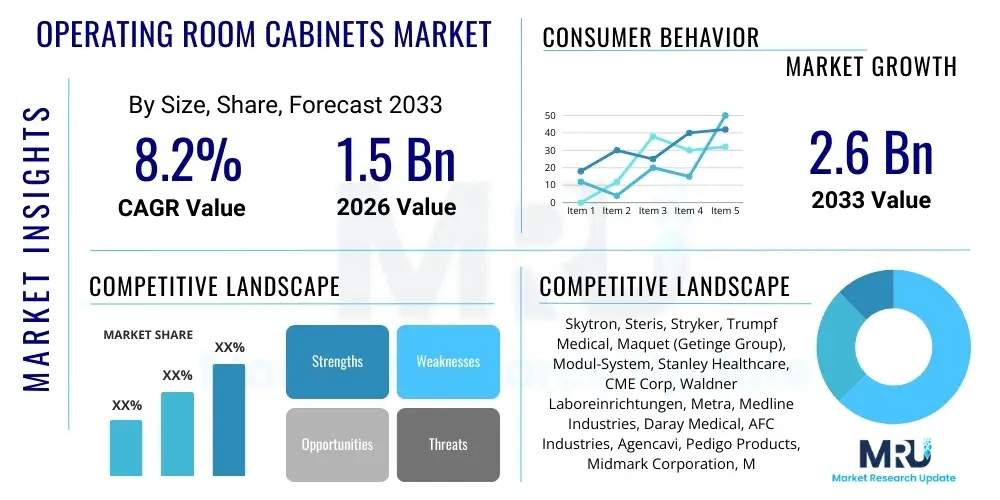

The Operating Room Cabinets Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 2.6 Billion by the end of the forecast period in 2033.

The Operating Room (OR) Cabinets Market encompasses the design, manufacturing, and distribution of specialized storage solutions essential for maintaining sterile environments and organizational efficiency within surgical settings. These cabinets, which include fixed wall units, mobile carts, and hybrid storage systems, are crucial for securely housing surgical instruments, implants, consumables, and personal protective equipment (PPE). The primary function is to provide immediate, accessible, and organized storage, thereby reducing procedure times, minimizing the risk of cross-contamination, and supporting stringent regulatory compliance standards related to inventory management and sterilization protocols in hospitals and surgical centers globally.

Product descriptions typically highlight features such as material composition (predominantly medical-grade stainless steel or specialized polymers), modularity, integrated locking systems for security, and compatibility with standardized sterile processing workflows. Major applications span across various surgical disciplines, including general surgery, orthopedics, cardiovascular procedures, and minimally invasive interventions, where the rapid accessibility of highly specialized tools is paramount. The increasing complexity of surgical procedures and the corresponding rise in the inventory of specialized equipment directly propel the demand for sophisticated, high-density storage solutions capable of optimizing limited OR space.

Key benefits derived from modern OR cabinets include enhanced infection control due to non-porous and easy-to-clean surfaces, improved operational efficiency through visual inventory management systems, and superior protection of high-value surgical assets. The market is primarily driven by the global expansion of healthcare infrastructure, increasing volume of surgical procedures (especially in aging populations), and sustained efforts by healthcare providers to achieve accreditation standards that mandate optimized inventory control and waste reduction. Furthermore, technological advancements, such as the integration of RFID and electronic tracking systems into cabinet designs, are transforming traditional storage units into smart organizational hubs, significantly contributing to market expansion.

The Operating Room Cabinets Market is experiencing robust expansion driven by global imperatives for healthcare efficiency and infection prevention. Business trends indicate a strong shift towards modular and customizable cabinet systems that can adapt to different OR layouts and specialization requirements. Key manufacturers are focusing on integrating advanced materials and smart inventory management technologies, such as utilizing corrosion-resistant coatings and incorporating sensor-based systems for automated tracking of surgical consumables. This modernization trajectory is crucial as healthcare facilities seek to streamline asset management, reduce supply chain complexities, and minimize procedural delays associated with misplaced or unaccounted instruments. Strategic partnerships between cabinet manufacturers and OR integration specialists are becoming commonplace, aimed at providing turnkey solutions for new surgical suite constructions and renovations.

Regionally, North America maintains market dominance, primarily due to high healthcare expenditure, early adoption of advanced sterile processing technologies, and strict regulatory environments mandating superior organizational standards in surgical facilities. However, the Asia Pacific (APAC) region is poised for the highest growth rate, fueled by massive investments in public and private hospital infrastructure across countries like China and India, alongside the rising prevalence of chronic diseases requiring surgical intervention. European markets show stable growth, driven by replacement cycles of aging hospital infrastructure and a strong focus on ergonomic design and sustainability in medical equipment procurement. Latin America and MEA are emerging markets exhibiting gradual uptake, motivated by improving access to advanced medical facilities and increasing urbanization.

Segment trends highlight the dominance of fixed/wall-mounted stainless steel cabinets due to their durability, superior sterile properties, and integration into existing OR architectural designs. However, the fastest-growing segment is expected to be mobile cabinet systems, offering flexibility and immediate accessibility for specialized or temporary surgical setups. Among end-users, hospitals remain the largest segment, but the proliferation of Ambulatory Surgical Centers (ASCs) is accelerating demand for smaller, highly efficient, and easily scalable storage solutions. The trend towards specialized ORs (e.g., hybrid ORs) is also boosting demand for cabinets tailored to house high-tech imaging equipment and robotics accessories, requiring customized size and configuration options to maximize spatial utilization.

User inquiries regarding the impact of Artificial Intelligence (AI) on OR cabinets primarily revolve around inventory automation, predictive maintenance, and operational integration. Users frequently question how AI algorithms can optimize cabinet utilization, specifically asking about real-time tracking accuracy, automated reordering processes, and the role of machine learning in forecasting surgical consumable needs based on scheduled procedures. A core concern is whether AI-enabled smart cabinets will entirely replace traditional inventory personnel and the associated investment required for transitioning to these intelligent systems. Furthermore, there is interest in how AI can integrate cabinet data with Electronic Health Records (EHRs) and Hospital Information Systems (HIS) to achieve seamless procedural documentation and resource allocation across the entire surgical theater, enhancing patient safety and reducing instances of stockouts or overstocking high-value implants.

The Operating Room Cabinets Market is significantly shaped by a confluence of driving factors, critical restraints, and substantial opportunities that collectively define its trajectory. The dominant driving force stems from the global focus on enhancing patient safety and infection control within surgical environments. Regulatory bodies worldwide are imposing stricter guidelines regarding instrument sterilization, segregation of clean and dirty supplies, and organized storage to prevent surgical site infections (SSIs), making modern, easy-to-clean stainless steel and polymer cabinets indispensable tools for compliance. Furthermore, the rising volume and complexity of surgical procedures, fueled by demographic shifts such as aging populations and increased incidence of chronic diseases, necessitate highly organized and rapid access to diverse surgical instruments and technology components, directly spurring demand for optimized storage solutions.

However, the market faces several notable restraints, primarily centered around the high initial investment required for sophisticated, modular, and technology-integrated cabinet systems. Budgetary constraints in public and smaller private healthcare facilities, particularly in developing economies, often lead to the deferral of capital expenditure on non-clinical infrastructure like OR cabinets, opting instead for essential life-saving equipment. Another key restraint is the architectural and spatial limitations of existing operating rooms, where renovation projects to install fixed, high-capacity cabinets can be disruptive and prohibitively expensive. This challenge often forces hospitals to prioritize smaller, less efficient storage solutions or mobile carts, limiting the widespread adoption of full-scale integrated cabinet walls which offer maximum efficiency benefits.

Significant opportunities exist through the advancement of smart storage technologies and the increasing penetration of Ambulatory Surgical Centers (ASCs). The proliferation of RFID technology, real-time inventory tracking, and electronic locking mechanisms represents a major avenue for manufacturers to offer value-added systems that drastically improve inventory accuracy and loss prevention. The ASC segment, characterized by high volume and a demand for operational cost-efficiency, presents a fertile ground for streamlined, high-density storage solutions optimized for rapid turnover and minimal footprint. Additionally, sustainability and ergonomic design trends offer opportunities for product innovation, focusing on utilizing recyclable materials and designing cabinets that minimize physical strain on surgical staff during instrument retrieval and storage processes, aligning with broader healthcare environmental goals.

The Operating Room Cabinets Market is meticulously segmented based on critical attributes including the cabinet type, the materials utilized in construction, the specific application or surgical discipline, and the end-user setting. This granular segmentation allows market stakeholders to identify specific pockets of demand and tailor product offerings to address specialized needs, such as the requirements of hybrid operating rooms versus general surgical suites. The classification by type (fixed vs. mobile) is fundamental, reflecting the trade-off between permanent, high-volume capacity and the flexibility required for dynamic OR environments or temporary setups. Understanding these segments is vital for predicting growth patterns, as technological integration often varies significantly between traditional fixed units and portable inventory management carts.

Material segmentation, primarily focusing on stainless steel versus polymer/laminate structures, reflects the priority placed on infection control, durability, and cost. Stainless steel dominates high-acuity ORs due to its unparalleled resistance to sterilization chemicals and non-porous surface, crucial for maintaining aseptic conditions. Conversely, polymer and laminate options find traction in areas where corrosion resistance to specific cleaning agents is prioritized or where budgetary considerations are paramount, often seen in smaller clinics or preparatory areas. The application segmentation, ranging from general surgery to highly specialized areas like cardiac and neurosurgery, directly influences cabinet design, requiring specific dimensions and internal configurations to accommodate specialized, often expensive, instrumentation like robotics components or large imaging device accessories.

End-user analysis further refines the market landscape, highlighting distinct procurement drivers between large hospital networks and independent ambulatory surgical centers (ASCs). Hospitals, which conduct the highest volume of diverse surgeries, typically require expansive, fully integrated cabinet systems often procured through large tenders. ASCs, focusing on outpatient procedures, prioritize compact, high-efficiency, often mobile units that support quick procedural turnover and minimal capital investment. The continuous rise of ASCs as a cost-effective alternative to traditional hospital settings is significantly altering the distribution channel dynamics and product design focus for cabinet manufacturers, promoting systems that offer maximum storage density within minimal physical space.

The value chain for the Operating Room Cabinets Market initiates with upstream activities focused on the sourcing and processing of raw materials, primarily high-grade stainless steel (304 or 316), specialized medical-grade polymers, and complex electronic components necessary for smart cabinet integration. Upstream analysis involves establishing stable supply agreements with metals processors and component manufacturers who meet strict quality control standards required for medical devices, particularly focusing on corrosion resistance and ease of sterilization. Manufacturing constitutes the core value-adding step, where design engineering, precision fabrication, welding, and surface finishing (e.g., electropolishing) transform raw materials into complex modular systems, ensuring compliance with ISO standards for medical furniture.

The distribution channel is multifaceted, relying heavily on specialized medical equipment distributors (indirect channel) who possess established relationships with hospital procurement departments and understand the complexities of OR integration and installation. Direct sales channels are often employed by major manufacturers for large-scale, customized projects, particularly when supplying integrated modular walls for new hospital constructions or complete OR renovation projects, allowing for closer control over customization and installation services. Effective logistical management is critical in this phase due, to the large size and weight of many cabinet systems, requiring specialized shipping and handling to prevent damage prior to installation.

Downstream activities center on installation, servicing, and long-term maintenance. Post-sale support, including staff training on smart cabinet inventory systems and timely repair services, contributes significant residual value and fosters strong customer loyalty. The end-users, primarily hospitals and ASCs, rely on the durability and reliability of these cabinets for continuous operational efficiency. The feedback loop from downstream users back to manufacturers regarding ergonomic functionality, cleaning efficacy, and technological performance drives product innovation and iterative design improvements, ensuring that subsequent generations of cabinets address evolving clinical and infection control requirements effectively.

The primary end-users and potential buyers of Operating Room Cabinets are institutions heavily involved in surgical patient care and procedural interventions. This overwhelmingly includes large governmental and private hospital networks that manage multiple operating theaters and specialties. These large facilities require high-volume, fixed cabinet solutions integrated into the physical infrastructure, often prioritizing durable materials like stainless steel and seeking advanced inventory tracking capabilities (RFID, sensor technology) to manage thousands of complex, expensive surgical instruments and consumables across various surgical disciplines.

A rapidly expanding segment of potential customers is Ambulatory Surgical Centers (ASCs). These facilities focus on outpatient surgeries, prioritizing operational efficiency, fast turnover times, and minimal footprint. ASCs typically prefer highly modular, flexible, and mobile cabinet systems that can be rapidly reconfigured based on the daily surgical schedule. Their purchasing decisions are often highly sensitive to initial capital cost but prioritize long-term efficiency and compliance with streamlined operational protocols, making them ideal targets for manufacturers specializing in compact, technology-enabled storage solutions.

Other vital customers include specialty surgical clinics, such as dental implant centers, ophthalmic surgery centers, and major university-affiliated medical research centers which conduct specialized or experimental surgical procedures. These institutions often require bespoke cabinet solutions designed to securely house unique, low-volume, high-value equipment or specimens under controlled conditions. Additionally, military field hospitals and humanitarian aid organizations occasionally require rugged, highly mobile, and rapidly deployable cabinet systems designed for extreme environments, representing a niche but high-priority potential customer base focusing on durability and ease of transport.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.6 Billion |

| Growth Rate | 8.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Skytron, Steris, Stryker, Trumpf Medical, Maquet (Getinge Group), Modul-System, Stanley Healthcare, CME Corp, Waldner Laboreinrichtungen, Metra, Medline Industries, Daray Medical, AFC Industries, Agencavi, Pedigo Products, Midmark Corporation, Mizuho OSI, Becton Dickinson (BD), Herman Miller Healthcare. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape within the Operating Room Cabinets Market is rapidly evolving from basic physical storage units to integrated, intelligent inventory management systems. The most significant technological driver is the incorporation of Internet of Things (IoT) sensors and Radio-Frequency Identification (RFID) technology directly into cabinet architecture. These systems allow for passive or active tracking of every item stored within the cabinet, providing real-time data on stock levels, item location, expiration dates, and usage frequency. This integration drastically reduces manual inventory checks, minimizes human error, and ensures compliance with regulatory requirements for asset traceability, ultimately enhancing procedural efficiency and preventing costly delays associated with missing equipment.

Further technological advancements include the development of modular and adaptable designs that accommodate the dynamic nature of modern surgical tools, particularly those associated with robotic and minimally invasive surgery (MIS). Many newer cabinets feature adjustable shelving, specialized drawers for delicate instruments, and integrated power sources for charging specialized batteries or robotic console accessories. Furthermore, sophisticated electronic access control systems, often managed through centralized hospital security networks, are becoming standard. These systems utilize biometric identification or secure digital keypads to restrict access, enhancing the security of high-value implants and narcotics that may be stored adjacent to surgical supplies, providing an auditable trail of cabinet usage.

Material science innovation also plays a critical role, although it is less visible than digital technology. Manufacturers are utilizing advanced antimicrobial coatings and seamless construction techniques to create cabinets that actively resist microbial growth and facilitate easier, more effective cleaning and sterilization protocols. This focus on material technology directly supports the market driver of infection control. The future trajectory involves greater integration with hospital supply chain management software (ERP/HIS), allowing the cabinet itself to initiate automated replenishment orders when stock levels fall below preset thresholds, transforming the physical storage unit into a self-managing component of the hospital logistics ecosystem.

Regional variations in healthcare spending, technological adoption rates, and regulatory frameworks significantly influence the Operating Room Cabinets Market structure. North America, encompassing the United States and Canada, currently holds the largest market share, characterized by high rates of complex surgical procedures, substantial capital investment in healthcare infrastructure, and stringent regulations demanding precise sterile processing and inventory control. The emphasis in this region is on integrating advanced, high-tech cabinet solutions featuring RFID and seamless hospital system connectivity. Furthermore, the robust expansion of the Ambulatory Surgical Center (ASC) sector in the U.S. drives continuous demand for efficient, scalable, and procedure-specific mobile cabinet systems, ensuring market stability and continued growth driven by technological upgrades.

Europe represents a mature market with steady growth, primarily fueled by the necessary modernization and replacement of aging hospital facilities across key economies such as Germany, the UK, and France. European purchasing trends prioritize ergonomic design, sustainability, and adherence to European Union quality standards (CE Mark). While adoption of fully integrated smart cabinet systems is strong in specialized university hospitals, many facilities maintain a preference for highly durable, long-life stainless steel modular units. Government procurement bodies often prioritize cost-effectiveness and proven long-term reliability alongside strict adherence to hygienic design principles, making the region a key market for high-quality, standardized cabinet solutions designed for optimal workflow.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally due to massive government and private sector investments aimed at expanding and upgrading healthcare infrastructure to meet the demands of rapidly growing populations and rising medical tourism. Countries like China, India, and Japan are building numerous new multi-specialty hospitals and surgical centers, creating vast greenfield opportunities for fixed, high-capacity OR cabinet installations. While cost sensitivity remains a factor in certain developing segments of APAC, the push towards achieving international accreditation standards (JCI) is compelling major hospital chains to adopt advanced sterile processing and storage technologies, including modern stainless steel cabinetry and basic inventory tracking systems, driving significant incremental market growth over the forecast period.

The primary material preferred for high-standard Operating Room Cabinets is medical-grade stainless steel, typically 304 or 316. This material is chosen for its superior durability, exceptional corrosion resistance against sterilization chemicals, non-porous surface, and ability to withstand high-frequency cleaning, which are all critical factors in maintaining strict aseptic control and preventing Surgical Site Infections (SSIs).

Technology is significantly impacting efficiency through the integration of RFID (Radio-Frequency Identification) tags and IoT sensors within smart cabinet systems. These technologies provide real-time, automated tracking of instruments and supplies, minimizing manual counting errors, ensuring stock availability, preventing asset loss, and enabling seamless integration with hospital Enterprise Resource Planning (ERP) systems for automated replenishment.

The Ambulatory Surgical Centers (ASCs) segment is the primary driver of demand for mobile OR cabinet systems. ASCs require flexible, highly efficient storage solutions that support rapid procedure turnover, minimal footprint utilization, and the ability to customize instrument sets based on a dynamic daily schedule, making mobile and modular carts essential for their operational model.

The main restraint affecting the adoption of advanced, integrated OR cabinet solutions globally is the high initial capital expenditure (CapEx) required. Advanced systems, which incorporate stainless steel construction, specialized hardware, and smart technology integration (RFID/IoT), represent a significant investment, often forcing smaller or public healthcare facilities to defer purchase due to budgetary constraints.

Modern OR cabinet designs address infection control challenges through several features, including utilizing seamless, crevice-free stainless steel construction to eliminate harborage points for microbes, incorporating sloped tops to prevent dust accumulation, and using antimicrobial powder coatings. Furthermore, modular shelving and drawers are designed for easy removal and effective terminal cleaning and disinfection.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.