ID : MRU_ 436417 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

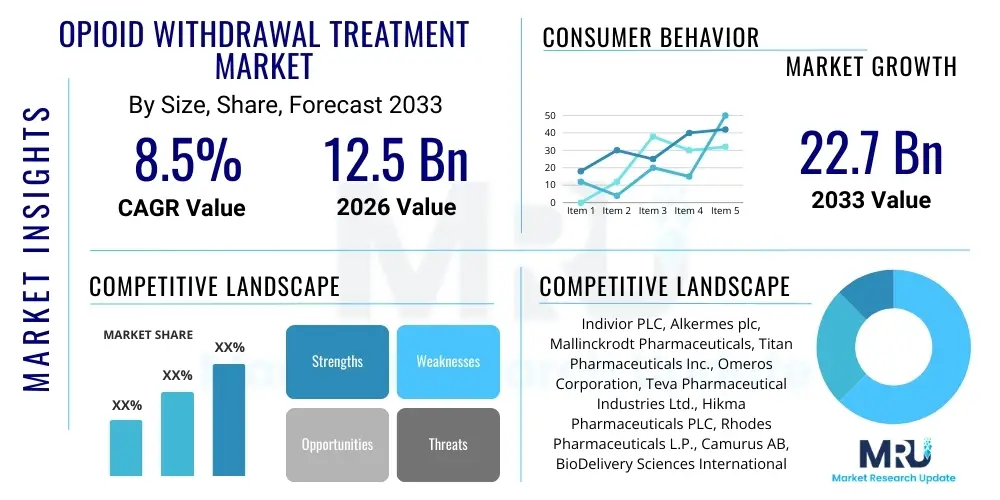

The Opioid Withdrawal Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $12.5 Billion in 2026 and is projected to reach $22.7 Billion by the end of the forecast period in 2033.

The Opioid Withdrawal Treatment Market encompasses the ecosystem of pharmaceutical interventions, behavioral therapies, and medical devices dedicated to managing the acute and protracted symptoms associated with cessation or reduction of opioid use. This field is fundamentally driven by the global opioid epidemic, which necessitates scalable and effective treatment modalities to mitigate relapse rates and improve patient outcomes. Medication-Assisted Treatment (MAT), primarily involving agonists (like Methadone), partial agonists (like Buprenorphine), and antagonists (like Naltrexone), forms the backbone of pharmacological approaches, offering critical support by reducing cravings and stabilizing neurobiological pathways disrupted by chronic opioid exposure. The increasing awareness regarding the chronic nature of Opioid Use Disorder (OUD) among healthcare providers, coupled with favorable regulatory shifts promoting accessibility to MAT, are essential elements defining the market landscape.

The product segment within this market is diverse, ranging from branded and generic forms of established MAT drugs to novel non-opioid medications aimed at alleviating specific withdrawal symptoms, such as Lofexidine for reducing norepinephrine release. Major applications span various clinical settings, including specialized addiction treatment centers, hospital inpatient programs, outpatient clinics, and increasingly, primary care settings, reflecting a trend toward integrated healthcare models. The inherent benefits of effective opioid withdrawal treatment are profound, encompassing reduced mortality rates associated with overdose, enhanced ability to engage in long-term recovery programs, and significant socio-economic improvements related to productivity and reduced criminal justice involvement. Furthermore, the development of long-acting injectable formulations of Naltrexone and Buprenorphine is transforming patient compliance and retention in treatment, offering a substantial advantage over daily oral dosing protocols.

Driving factors for sustained market growth include stringent government mandates globally to address the public health crisis posed by opioids, substantial public and private funding directed toward OUD treatment infrastructure, and continuous research and development efforts aimed at minimizing side effects and enhancing the efficacy of withdrawal management protocols. The expansion of telehealth services for prescription and monitoring of MAT, particularly in rural or underserved areas, also acts as a powerful catalyst. However, market dynamics are often constrained by the stigma associated with addiction, fragmented insurance coverage for comprehensive treatment, and ongoing challenges related to the diversion of MAT medications, necessitating robust regulatory oversight and sophisticated prescription monitoring systems.

The Opioid Withdrawal Treatment Market is characterized by robust expansion, primarily fueled by the accelerating severity of the opioid crisis across North America and increasingly prominent issues in European and Asian geographies. Business trends indicate a strong preference for Medication-Assisted Treatment (MAT) utilizing long-acting formulations, reflecting a strategic shift by pharmaceutical companies towards products that improve adherence and reduce misuse potential. Key industry participants are focusing heavily on securing regulatory approvals for novel non-opioid therapeutics that offer symptomatic relief without addictive properties, thereby diversifying the treatment portfolio beyond traditional controlled substances. Furthermore, strategic collaborations between drug manufacturers and technology providers are enhancing digital health platforms tailored for remote patient monitoring and tele-MAT delivery, optimizing the utilization of existing treatment infrastructure and overcoming geographical barriers to access, which is a major commercial imperative.

Regional trends highlight North America, specifically the United States, as the dominant market due to the high prevalence of Opioid Use Disorder (OUD), significant public expenditure directed toward combating the epidemic (e.g., through federal grants), and a well-established infrastructure for addiction treatment, despite capacity limitations. Europe is emerging as a critical growth region, driven by increasing regulatory support for harm reduction and MAT adoption in countries like the UK, Germany, and France, often incorporating integrated care pathways. Asia Pacific, while currently smaller, is projected to exhibit the highest growth rate, stimulated by rising rates of illicit opioid use, particularly synthetic opioids, and expanding healthcare access in rapidly developing economies seeking to adopt Western treatment standards. This regional diversification is crucial for mitigating risks associated with reliance on singular geographic markets.

Segmentation trends reveal that the pharmacological segment dominates the market, with Buprenorphine-based products, including buprenorphine/naloxone combination therapies, holding the largest market share due to their widespread availability and reduced regulatory hurdles compared to Methadone. However, the non-opioid segment, encompassing medications for symptom management (e.g., alpha-2 adrenergic agonists), is gaining momentum as clinicians seek integrated approaches to managing complex withdrawal symptoms like anxiety, pain, and insomnia. Treatment setting analysis emphasizes the accelerating growth of outpatient settings, aligning with patient preferences for community-based care and the lower cost structure compared to intensive inpatient detoxification units. The shift toward value-based care models also pressures providers to adopt cost-effective, evidence-based withdrawal management protocols that maximize patient retention in follow-up care.

User inquiries regarding Artificial Intelligence (AI) in Opioid Withdrawal Treatment frequently center on its capacity to revolutionize patient management, specifically concerning early identification of individuals at high risk of OUD, personalization of MAT dosages, and prediction of relapse events. Common concerns revolve around data privacy when utilizing sensitive patient information, the ethical implications of algorithmic bias potentially affecting treatment access, and the overall clinical validation required before large-scale deployment of AI tools in such a high-stakes medical domain. Users seek assurance that AI can enhance treatment efficacy by optimizing resource allocation and improving decision support systems for clinicians, moving beyond basic administrative functions to genuine clinical innovation. Key expectations include AI-powered tools for developing highly individualized treatment plans, dynamically adjusting pharmacotherapy based on real-time physiological and behavioral data, and offering remote, scalable monitoring solutions for post-withdrawal care.

AI's primary influence is expected in enhancing the precision and efficiency of treatment delivery. Machine learning algorithms can analyze vast datasets, including electronic health records, socio-demographic factors, and toxicology screens, to predict which patients are most likely to respond positively to specific MAT regimens (e.g., Naltrexone versus Buprenorphine), thereby minimizing trial-and-error treatment initiation. This predictive modeling capability significantly improves the standard of care by allowing clinicians to preemptively address potential barriers to recovery, such as co-occurring mental health disorders or unstable living conditions, which are critical determinants of withdrawal success and long-term sobriety. Furthermore, AI-driven natural language processing (NLP) can rapidly analyze patient notes and behavioral assessments, extracting meaningful patterns that might be missed in traditional manual reviews, offering continuous insight into the patient's state during the critical withdrawal phase.

In the context of technology development, AI facilitates the creation of sophisticated digital phenotyping tools. These tools utilize passive data collection from wearables and smartphones to monitor biological markers (like heart rate variability) and behavioral indicators (like sleep patterns or location data) that correlate with stress, craving, and high-risk behavior. For the market, this capability translates into new revenue streams focused on integrated monitoring solutions that bridge the gap between clinical appointments, enhancing patient safety and allowing for timely intervention before a full relapse occurs. However, the integration requires significant investment in standardized data infrastructure and robust cybersecurity measures to maintain patient trust and comply with stringent healthcare regulations across various jurisdictions, posing both a technical challenge and a substantial market opportunity for specialized health tech firms.

The Opioid Withdrawal Treatment Market is fundamentally shaped by a dynamic interplay of Drivers (D), Restraints (R), Opportunities (O), and structural Impact Forces. The primary drivers include the catastrophic global burden of opioid use disorder, necessitating governmental action and large-scale public health initiatives, coupled with legislative mandates promoting the use and accessibility of Medication-Assisted Treatment (MAT), such as the expansion of prescribing waivers for Buprenorphine. Significant growth is also fueled by ongoing advancements in pharmaceutical formulation, particularly the shift toward long-acting injectables that address patient compliance and misuse concerns inherent to oral medications, alongside increasing medical acceptance and destigmatization of addiction as a treatable chronic disease. These drivers create a sustained baseline demand that is resilient to minor economic fluctuations, positioning the market for steady growth.

Restraints primarily revolve around the inherent challenges of access and delivery. These include the significant stigma associated with OUD, which often discourages individuals from seeking treatment; regulatory barriers and complexity surrounding controlled substances, particularly Methadone; and the severe shortage of specialized healthcare professionals, especially in rural and underserved communities, qualified to administer and manage complex MAT protocols. Furthermore, high out-of-pocket costs for proprietary long-acting formulations and variable reimbursement policies across different insurance providers and state Medicaid programs pose financial constraints, limiting widespread patient adoption. The risk of diversion and illicit use of agonist medications, although mitigated by combination products, remains an operational and regulatory concern that necessitates careful monitoring and prescribing practices.

Opportunities for market stakeholders reside in the development and commercialization of entirely novel, non-addictive pharmacotherapies that target specific neurobiological mechanisms underlying withdrawal symptoms without acting on opioid receptors, offering a clean alternative to controlled substances. There is substantial potential in leveraging telehealth and integrated digital platforms to enhance patient monitoring, provide scalable behavioral support, and deliver pharmacotherapy remotely, fundamentally transforming care delivery efficiency and geographical reach. Strategic geographic expansion into emerging markets, particularly in Asia Pacific and Latin America, where OUD prevalence is rising and treatment infrastructure is rapidly developing, presents long-term growth avenues. Additionally, the increasing focus on precision medicine allows for the development of diagnostic tools that predict patient response to specific MAT drugs, optimizing treatment protocols and improving success rates, which commands a premium in the clinical setting.

The Opioid Withdrawal Treatment Market segmentation provides a critical view of the diverse treatment modalities and delivery channels utilized in clinical practice. The market is broadly categorized based on Product Type (Pharmacological Treatments and Non-Pharmacological Treatments), Drug Type (Buprenorphine, Methadone, Naltrexone, and Others), Route of Administration (Oral, Injectable, Transdermal), and Treatment Setting (Inpatient, Outpatient, and Residential Treatment Centers). Understanding these segments is vital for stakeholders to allocate R&D capital efficiently, target specific prescriber groups, and navigate the complex regulatory landscapes governing different drug types. The shift toward long-acting injectables represents a major commercial opportunity, driven by superior patient adherence compared to oral daily doses, while the growth of outpatient settings reflects economic pressures and patient preferences for decentralized, community-based care models.

The value chain for the Opioid Withdrawal Treatment Market commences with the upstream segment, dominated by pharmaceutical research and development (R&D), focusing on the synthesis, clinical trials, and regulatory approval of both established Medication-Assisted Treatment (MAT) drugs and novel non-opioid compounds. This stage involves significant capital expenditure and expertise, primarily carried out by large pharmaceutical companies and specialized biotechs. Key upstream activities include securing active pharmaceutical ingredients (APIs), ensuring quality control, and obtaining patent protection for innovative delivery systems, such as long-acting injectables or transdermal patches. The cost of API production, especially for controlled substances like Methadone and Buprenorphine, is a critical component influencing final market pricing and profit margins. Strong collaboration between academic institutions and industry is essential at this stage to translate basic science findings regarding neurobiology into effective clinical treatments.

The midstream component involves the manufacturing, supply chain logistics, and specialized distribution necessary to handle controlled substances. Manufacturers must adhere to rigorous regulatory standards (such as DEA quotas in the U.S. for Schedule II and III drugs) and implement secure packaging and tracking systems to prevent diversion and ensure product integrity. Distribution channels are highly regulated, involving both direct sales to large hospital systems and indirect distribution through specialized pharmaceutical wholesalers and distributors who possess the necessary licenses for handling controlled substances. The complexity of the supply chain increases for temperature-sensitive injectable formulations, requiring sophisticated cold chain management and inventory controls to maintain product efficacy up to the point of administration in clinical settings.

The downstream segment centers on patient access and administration, involving treatment providers (hospitals, specialized clinics, primary care offices), retail and specialty pharmacies, and payers (government programs and private insurance). Direct distribution often occurs for bulk hospital supply or specialized clinics, whereas indirect channels utilize pharmacies for dispensing oral medications to outpatients. Treatment effectiveness heavily relies on the quality of clinical administration, patient counseling, and integration with behavioral therapies, which represent the final value-add service. Potential customers, or end-users, are individuals suffering from Opioid Use Disorder (OUD), whose access is ultimately determined by insurance coverage, geographical availability of certified providers (especially those with Buprenorphine waivers), and the affordability of co-payments for long-term treatment. Telehealth platforms are rapidly integrating into the downstream, offering a novel, streamlined distribution channel for monitoring and remote prescribing, transforming how patient care is delivered and monitored post-withdrawal.

The primary potential customers and end-users of Opioid Withdrawal Treatment products are individuals diagnosed with Opioid Use Disorder (OUD), encompassing a wide demographic spectrum spanning various ages, socio-economic statuses, and geographical locations. Within this core group, distinct subsets exist based on the severity of their disorder and preferred treatment pathway. These include patients requiring medically supervised detoxification in an inpatient or residential setting, typically involving the acute management of severe withdrawal symptoms using short-term pharmacotherapy such as Lofexidine or monitored opioid tapering. A much larger segment comprises patients seeking long-term maintenance therapy, where medications like Buprenorphine or Naltrexone are utilized for extended periods to prevent relapse, reduce cravings, and support psycho-social integration.

Beyond the direct patients, the key institutional buyers and influencers of these products include specialized addiction treatment centers and clinics, which represent significant bulk purchasers of all MAT formulations, particularly long-acting injectables for maximizing patient compliance. General hospitals and emergency departments are increasingly becoming critical customers, especially for initiating MAT immediately following an overdose event or during acute medical crises. Furthermore, governmental public health bodies, such as state and federal departments of health, act as major financial customers, procuring large quantities of treatment drugs through federal grants and state-run programs aimed at expanding access, especially within the correctional system and community health centers, thereby driving demand in public sector purchasing.

The rise of integrated behavioral health practices and primary care physicians (PCPs) with X-waivers (for prescribing Buprenorphine) signifies a major expansion in the customer base. PCPs are increasingly positioned as frontline providers of MAT, requiring a continuous supply of oral and sublingual formulations for outpatient management. Potential customers also include managed care organizations (MCOs) and private insurance companies, who drive utilization patterns through formulary decisions, preferring cost-effective, evidence-based treatments that demonstrate long-term positive outcomes, thus favoring long-acting products that reduce the need for costly hospitalizations and emergency interventions associated with relapse.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $12.5 Billion |

| Market Forecast in 2033 | $22.7 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Indivior PLC, Alkermes plc, Mallinckrodt Pharmaceuticals, Titan Pharmaceuticals Inc., Omeros Corporation, Teva Pharmaceutical Industries Ltd., Hikma Pharmaceuticals PLC, Rhodes Pharmaceuticals L.P., Camurus AB, BioDelivery Sciences International Inc., Dr. Reddy's Laboratories Ltd., Pfizer Inc., Amneal Pharmaceuticals Inc., Mylan N.V. (Viatris), Novartis AG, Sun Pharmaceutical Industries Ltd., Mayne Pharma Group Limited, VeriTeQ Corporation, Axsome Therapeutics, Inc., Collegium Pharmaceutical, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Opioid Withdrawal Treatment Market is rapidly evolving, driven by the need for enhanced patient compliance, reduced diversion risk, and optimized symptom management. The most critical technological advancements center on drug delivery systems, specifically the development of long-acting injectable and implantable formulations. These technologies, exemplified by extended-release Buprenorphine (e.g., weekly or monthly injections) and Naltrexone (monthly injections), utilize specialized polymer matrices or liposomal encapsulation to ensure sustained, therapeutic drug release over prolonged periods. This innovation fundamentally bypasses the need for daily dosing, significantly improving adherence rates and eliminating the potential for diversion or misuse associated with daily oral formulations, thereby enhancing the overall clinical efficacy of Medication-Assisted Treatment (MAT). The complexity and proprietary nature of these sustained-release technologies grant companies a significant competitive advantage and higher pricing power within the market.

Another pivotal technological area involves the development of advanced non-opioid medications targeting the neurochemical imbalances underlying acute withdrawal. Treatments like Lofexidine, an alpha-2 adrenergic agonist, are engineered specifically to modulate the exaggerated norepinephrine outflow that causes common withdrawal symptoms such as anxiety, muscle cramping, and tachycardia, offering a pharmacological solution that lacks opioid receptor activity. Future technology focuses heavily on novel molecular targets, including compounds acting on kappa opioid receptors or utilizing glutamate receptor modulation, aiming to develop non-addictive medications that can effectively block or mitigate severe withdrawal discomfort. The successful clinical deployment of these novel mechanisms requires rigorous biomarker research and sophisticated clinical trial designs to validate efficacy against traditional MAT.

Finally, the proliferation of digital health technologies is transforming care delivery. This includes the use of telehealth platforms for remote prescribing, video consultation, and continuous clinical supervision, drastically expanding access to MAT, especially in geographically isolated areas. Furthermore, connected health devices, such as smart pill bottles, wearable sensors, and remote monitoring systems, are being integrated to track physiological indicators related to stress, sleep, and potential cravings. These technologies provide clinicians with real-time objective data, enabling proactive intervention and personalized care adjustments. The adoption of electronic health record (EHR) integration tools that facilitate seamless data exchange and adherence monitoring across multiple providers is essential for supporting the continuity of care required for successful long-term opioid withdrawal management and recovery.

The primary revenue driver is the Pharmacological Treatments segment, specifically Medication-Assisted Treatment (MAT) utilizing Buprenorphine-based products, including both sublingual films/tablets and long-acting injectable formulations, due to their proven efficacy in reducing withdrawal symptoms and preventing relapse. The Outpatient Treatment Setting segment is experiencing the fastest growth, reflecting efforts to decentralize care and improve patient accessibility and cost-effectiveness.

Long-acting injectable formulations, such as those for Buprenorphine and Naltrexone, are profoundly impacting market dynamics by increasing patient adherence, significantly reducing the risk of medication diversion, and improving retention rates in treatment. These proprietary products command higher pricing and are increasingly favored by payers and providers aiming for superior clinical outcomes and reduced need for daily supervision, driving the premium segment of the market.

The regulatory outlook for novel non-opioid withdrawal treatments is highly favorable, driven by a strong unmet clinical need for non-addictive solutions. Regulatory bodies like the FDA are expediting the approval pathways for drugs like alpha-2 adrenergic agonists (e.g., Lofexidine) and other compounds targeting symptomatic relief, encouraging pharmaceutical innovation that moves away from traditional controlled substances, thereby lowering regulatory burden for prescribers.

North America, particularly the United States, holds the largest market share. This dominance is attributable to the extreme severity and high prevalence of the opioid epidemic, combined with aggressive public health funding initiatives, extensive infrastructure for addiction treatment, and high insurance coverage rates that facilitate widespread access and utilization of prescription MAT drugs and advanced drug delivery systems.

Telehealth plays a critical and expanding role by enhancing geographical access to Medication-Assisted Treatment (MAT), particularly in rural and underserved areas. It allows for remote patient monitoring, video consultations, and remote prescribing of Buprenorphine, significantly improving continuity of care, reducing barriers related to transportation and stigma, and ultimately increasing the scalability and efficiency of treatment delivery across the healthcare continuum.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.