ID : MRU_ 438960 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

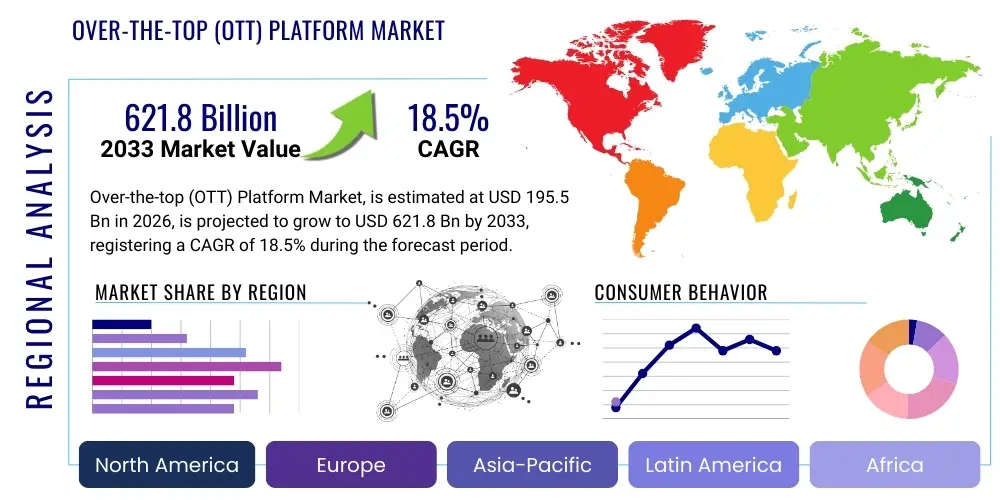

The Over-the-top (OTT) Platform Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 195.5 Billion in 2026 and is projected to reach USD 621.8 Billion by the end of the forecast period in 2033. This substantial expansion is primarily driven by the increasing global penetration of high-speed internet, the widespread availability of smart devices, and a fundamental shift in consumer preference away from traditional linear television toward on-demand, personalized content consumption. The market exhibits robust growth potential, supported by evolving monetization strategies such as AVOD (Advertising-Based Video On Demand) and hybrid models supplementing the established SVOD (Subscription Video On Demand) sector.

The calculation of the market size reflects the combined revenues generated from various OTT segments, including video streaming (VOD), audio streaming, gaming, and communication services delivered over the internet, bypassing traditional distribution networks. The rapid digitalization in emerging economies, coupled with significant investments by major media and technology conglomerates into original, high-quality content production, serves as a core catalyst for market valuation increase. Furthermore, the diversification of content genres, catering to niche audiences, ensures sustained engagement and reduction in subscriber churn, contributing positively to the overall market scale projection over the next seven years.

The Over-the-top (OTT) Platform Market encompasses the ecosystem of content delivery services that transmit video, audio, and other media directly to the viewer over the internet, bypassing conventional broadcasting, cable, or satellite television providers. This market is characterized by direct consumer relationships, enabling personalized viewing experiences and flexible subscription models. Key products include streaming services like Netflix, Disney+, Amazon Prime Video, and various sports and niche content platforms. Major applications span entertainment, education (e-learning platforms), communication (VoIP and messaging services), and gaming. The primary benefits include convenience, access to vast libraries of on-demand content, geographical freedom of consumption, and often, competitive pricing relative to bundled cable packages. Driving factors include the proliferation of 5G and fiber optic networks, rising disposable incomes facilitating digital entertainment expenditures, and the continuous enhancement of user experience (UX) through features like 4K/HDR support and recommendation algorithms.

The Over-the-top (OTT) Platform Market is witnessing an accelerated transformation marked by strategic consolidation and content diversification. Business trends indicate a shift towards hybrid monetization strategies, integrating both SVOD and AVOD to capture wider market segments and maximize average revenue per user (ARPU). Major players are intensely focused on international expansion, particularly in high-growth regions like Asia Pacific and Latin America, necessitating localization and investment in regional original content. Regional trends show North America maintaining dominance in terms of overall revenue and technological innovation, while APAC is poised for the highest growth rate due to increased mobile data usage and a large, untapped consumer base. Segment trends highlight the Video-on-Demand (VOD) segment, especially SVOD, as the largest revenue generator, although the AVOD segment is rapidly gaining traction as advertisers seek highly engaged digital audiences. Technological adoption is centered around AI-driven content recommendations, personalized advertising insertion, and robust Digital Rights Management (DRM) solutions to combat piracy, all contributing to a sophisticated and competitive market landscape.

Users frequently inquire about how Artificial Intelligence (AI) enhances personalization, optimizes content discovery, and addresses issues of content overload within the OTT space. Key user concerns revolve around the ethical implications of using viewer data for hyper-targeting, the potential for algorithmic bias in content recommendations, and how AI can improve streaming quality (QoS) and reduce operational costs associated with content delivery. Users also seek information on AI's role in content creation, post-production automation (e.g., subtitling and dubbing), and advanced anti-piracy measures. The consensus expectation is that AI will be the primary differentiating factor, moving beyond simple recommendation engines to predictive analytics that inform investment decisions on original content, streamline workflow efficiency, and drastically improve customer retention by preemptively addressing churn risks.

The OTT market is substantially driven by the global expansion of high-speed internet infrastructure (4G, 5G, and fiber), combined with the rising demand for flexible, on-demand entertainment that cable providers often fail to offer. However, the market faces significant restraints, primarily stemming from intense competition leading to content fatigue and subscription saturation, resulting in high churn rates across platforms. Furthermore, regulatory hurdles, particularly regarding data privacy and content censorship in specific regions, pose challenges to seamless global expansion. Opportunities lie in developing niche content catering to underserved demographics, the rapid growth of the AVOD model, and strategic partnerships with telecommunication operators to bundle services. Impact forces driving the market include technological advancements in streaming codecs (e.g., AV1), enhancing video quality while reducing bandwidth needs, and the pervasive shift towards mobile-first content consumption, making accessibility a critical competitive differentiator.

The Over-the-top (OTT) Platform Market is comprehensively segmented based on content type, platform, monetization model, and end-user, providing a granular view of market dynamics and revenue streams. The content type segmentation differentiates between Video Streaming, Audio Streaming, Gaming, and Communication services, with video remaining the dominant segment, particularly driven by high-budget fictional and documentary productions. Platform segmentation reveals the increasing importance of smart TVs and connected devices (Roku, Apple TV) alongside the foundational role of mobile devices and desktops. This segmentation is crucial for content distributors to optimize application performance and user interfaces across diverse hardware ecosystems, ensuring consistent quality of experience irrespective of the viewing environment.

The monetization model analysis is particularly dynamic, moving away from purely SVOD (Subscription Video On Demand) toward a hybrid ecosystem. AVOD (Advertising Video On Demand) is experiencing rapid growth as companies seek to tap into price-sensitive consumers and diversify revenue streams. TVOD (Transactional Video On Demand), though smaller, remains relevant for premium, new-release content. The ongoing battle between these models defines strategic pricing and content release windows. Furthermore, the end-user segmentation separates individual/household consumers from enterprise users, recognizing the emerging use of OTT technology for internal corporate communications and remote training, although consumer entertainment remains the overwhelming revenue driver.

Understanding these segments allows market participants to tailor their offerings effectively. For instance, platforms focusing on mobile end-users in APAC prioritize data-efficient streaming and localized content, while those targeting North American smart TV users focus on 4K/HDR quality and spatial audio integration. The segmentation framework is vital for accurately assessing competitive intensity and identifying unsaturated market pockets for future investment.

The OTT value chain is intricate, beginning with upstream analysis focusing on content creation, aggregation, and acquisition. This phase involves independent studios, major media houses, and professional content producers who generate the intellectual property (IP) that forms the core offering. Competition in the upstream segment is centered around securing exclusive rights and investing heavily in original content to differentiate platforms. Effective upstream management requires robust contracting and licensing frameworks to ensure global distribution rights and managing royalty payments efficiently. A critical aspect here is the shift from licensing third-party libraries to owning and producing content in-house, significantly raising the barriers to entry for new market entrants.

The downstream analysis focuses on content delivery, consumption, and monetization. This includes the preparation of content (encoding, transcoding, DRM wrapping), infrastructure management (Content Delivery Networks or CDNs), and the final delivery via the platform interface (apps and websites). Distribution channels are predominantly direct-to-consumer (D2C), leveraging proprietary apps across smart devices and mobile operating systems. However, indirect channels, such as partnerships with telecom operators (e.g., bundled packages) or hardware manufacturers (pre-installed apps on smart TVs), play a significant role in customer acquisition and lowering initial distribution costs. The success in the downstream phase hinges on network latency minimization, scalability, and providing a seamless, high-quality user experience (QoE) globally.

The monetization layer, spanning across the value chain, is driven by sophisticated data analytics. Direct monetization involves collecting subscription fees (SVOD) or transactional payments (TVOD). Indirect monetization relies on integrating targeted advertisements (AVOD), requiring partnerships with programmatic advertising platforms and data brokers. The efficient management of this integrated distribution channel—balancing direct customer relationship control with the reach provided by indirect distribution partners—is crucial for maximizing revenue and maintaining market visibility in an increasingly saturated environment.

The primary end-users and buyers of OTT platform services are globally dispersed individual consumers and households seeking personalized, flexible, and high-quality entertainment and informational content. These consumers are typically technology-literate, possess medium to high disposable incomes, and demand content accessibility across multiple devices, including smartphones, smart TVs, and dedicated streaming sticks. A significant demographic shift involves younger generations (Millennials and Gen Z) who have largely foregone traditional pay-TV subscriptions in favor of curated, low-cost OTT bundles. Market penetration is also accelerating in developing regions where mobile-first viewing populations find OTT platforms to be the most affordable and accessible form of high-quality digital entertainment, driving demand for localized and mobile-optimized subscription tiers.

Beyond entertainment, a rapidly growing segment of potential customers includes corporate and institutional buyers. Enterprises utilize OTT platforms, often customized or white-labeled versions, for internal corporate communication, employee training, and large-scale virtual events. This B2B application requires platforms with enhanced security features, robust live streaming capabilities, and integration with existing enterprise communication tools. Educational institutions and universities represent another key customer segment, using specialized OTT services to deliver distance learning content, archived lectures, and specialized academic materials on demand, highlighting the expansion of OTT beyond purely recreational applications.

Furthermore, niche consumer segments represent significant untapped potential. These include enthusiasts for specific content genres (e.g., horror, documentary, anime), specialized sports viewers, and communities demanding hyper-local content not addressed by global streaming giants. Successfully targeting these potential customers requires focused content aggregation, strategic marketing, and often, highly competitive pricing strategies. The ultimate goal for providers is achieving broad demographic appeal while retaining the fidelity of their core customer base through continuous content refresh and technical innovation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 195.5 Billion |

| Market Forecast in 2033 | USD 621.8 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Netflix, Inc., Amazon.com, Inc., The Walt Disney Company (Disney+), Apple Inc., Warner Bros. Discovery (Max), Paramount Global (Paramount+), Comcast (Peacock), Google LLC (YouTube), Tencent Holdings, Sony Group Corporation, Hulu LLC, Rakuten Group, Inc., DAZN Group, Viacom18 (JioCinema), PPTV, Iflix, Spotify Technology S.A., iQIYI, Inc., Fox Corporation (Tubi), Kakao Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological framework underpinning the OTT market is centered on advanced content processing and delivery mechanisms designed to ensure seamless, high-quality streaming across varied network conditions and device capabilities. Core technologies include sophisticated content delivery networks (CDNs) responsible for minimizing latency by caching content geographically close to the end-user. Video encoding standards, particularly H.265 (HEVC) and the emerging royalty-free AV1 codec, are crucial for optimizing data consumption while maintaining or improving 4K and 8K video quality. Adaptive Bitrate (ABR) streaming protocols, such as HLS (HTTP Live Streaming) and DASH (Dynamic Adaptive Streaming over HTTP), dynamically adjust the streamed video quality based on real-time network throughput, preventing buffering and enhancing the viewer experience. Furthermore, robust Digital Rights Management (DRM) solutions, including Widevine, PlayReady, and FairPlay, are essential security layers preventing unauthorized content copying and distribution, safeguarding intellectual property and licensing agreements.

Beyond content delivery, the technology landscape is heavily influenced by data science and machine learning (ML). Advanced ML models are deployed within recommendation engines to analyze vast amounts of user interaction data, identifying patterns and predicting viewing preferences with high accuracy. This personalization engine is vital for reducing churn and increasing engagement time. Cloud computing infrastructure, provided by major hyperscalers, forms the backbone of the entire operation, enabling instantaneous scalability to manage massive global traffic peaks during major content launches or live events. This cloud dependency allows platforms to operate with reduced capital expenditure on hardware, focusing resources instead on content acquisition and software innovation.

Emerging technologies shaping the future of the OTT landscape include the integration of blockchain for enhanced DRM transparency and potentially decentralized content distribution models, although these are currently nascent. Furthermore, the adoption of 5G networks is enabling ultra-low latency streaming, fostering higher-quality mobile viewing and opening avenues for interactive content and augmented reality (AR) integrations within the viewing experience. Spatial audio technology, such as Dolby Atmos, is becoming standard for premium content, leveraging improved audio quality as a key differentiator. The continuous evolution of these technologies ensures the competitive intensity of the market remains high, driving innovation in delivery efficiency, user interaction, and content protection.

North America currently holds the largest market share in the global OTT Platform Market, primarily driven by early adoption of streaming technology, high broadband penetration, and the presence of the world's leading content creators and technology innovators. The region boasts a highly mature competitive environment, characterized by intense competition between major domestic players such as Netflix, Amazon Prime Video, Disney+, and Max. Market saturation has forced providers to pivot towards aggressive content investment, diversification into AVOD tiers, and focusing heavily on subscriber retention through unique bundled offerings. Innovation in this region often sets global trends, particularly regarding personalized advertising technologies and advanced video quality standards (4K, HDR). The maturity of the infrastructure and the consumer willingness to pay for multiple subscriptions underpin the region's high revenue contribution.

Asia Pacific (APAC) is projected to exhibit the highest Compound Annual Growth Rate (CAGR) during the forecast period. This explosive growth is fueled by a massive, digitally connecting population, increasing affordability of smartphones, and the rollout of widespread 4G and 5G networks, especially in populous markets like India, China, and Southeast Asia. The APAC market is highly fragmented, necessitating deep localization of content, subtitles, and user interfaces due to vast linguistic and cultural diversity. Monetization strategies are often mobile-first and price-sensitive, with AVOD models and low-cost, short-term subscriptions proving highly successful. Regional players like Tencent, iQIYI, and Hotstar dominate local markets, creating significant barriers to entry for global giants who must strategically partner or acquire local content assets to gain meaningful traction.

Europe represents a sophisticated and geographically diverse market, characterized by stringent data protection regulations (GDPR) and complex intellectual property laws enforced across numerous countries. While Western Europe (UK, Germany, France) mirrors North American trends with high SVOD saturation and a shift to hybrid models, Central and Eastern European markets offer higher growth potential. European consumers show a strong affinity for local language content, prompting global players to invest heavily in European original productions to comply with local content quotas and appeal to regional tastes. The market structure involves strong national broadcasters launching their own OTT services, competing effectively against international platforms.

Latin America (LATAM) is rapidly emerging as a critical growth engine, benefiting from rising middle-class disposable incomes and substantial improvements in digital infrastructure. The region is largely mobile-centric, with high demand for accessible pricing. Piracy remains a significant challenge, driving innovation in advanced DRM and platform security measures. The market is primarily dominated by global U.S. players, but regional content and local sports rights are increasingly critical acquisition targets for differentiation. Economic volatility in certain countries necessitates flexible payment models, including integration with prepaid mobile plans, to sustain subscriber growth.

Middle East and Africa (MEA) present a region with varied growth profiles. The Middle East (GCC countries) shows high ARPU potential due to affluent consumer bases and high technology adoption, driving demand for premium, multi-platform content. Africa, particularly Sub-Saharan Africa, is nascent but holds immense future potential, driven entirely by mobile internet connectivity. Challenges include low average bandwidth, necessitating highly optimized, low-data streaming formats, and regulatory environments that vary significantly between countries. Local content acquisition and strategic partnerships with telecom providers are essential strategies for market penetration across the continent.

The global OTT Platform Market is projected to grow at a robust CAGR of 18.5% between 2026 and 2033. This growth rate is primarily fueled by rising internet penetration globally, the shift to mobile-first consumption, and ongoing investment in high-quality original content by major platforms to attract and retain subscribers.

Monetization is shifting significantly toward hybrid models. While Subscription Video On Demand (SVOD) remains dominant, there is a substantial acceleration in the adoption of Advertising Video On Demand (AVOD) and tiered pricing structures. This allows platforms to cater to diverse consumer segments, maximize average revenue per user (ARPU), and mitigate subscriber churn due to subscription fatigue.

North America currently holds the largest revenue share in the OTT Platform Market due to its early establishment, high consumer expenditure on digital entertainment, and the presence of global industry leaders. However, the Asia Pacific (APAC) region is forecasted to exhibit the fastest growth rate driven by expanding mobile connectivity and a large, digitally evolving population.

AI is a critical competitive differentiator, primarily used to enhance user experience through hyper-personalized content recommendations and optimized advertising insertion (programmatic AVOD). Furthermore, AI is vital for operational efficiency, assisting in automated content encoding, real-time quality assurance, and sophisticated anti-piracy protection across global distribution networks.

Key restraints include the phenomenon of subscription saturation and content fatigue, where consumers are overwhelmed by too many platform choices, leading to high churn rates. Other major constraints involve content piracy globally, which erodes revenue, and regulatory fragmentation, particularly regarding data privacy and content censorship laws across different operational territories.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.