ID : MRU_ 433074 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

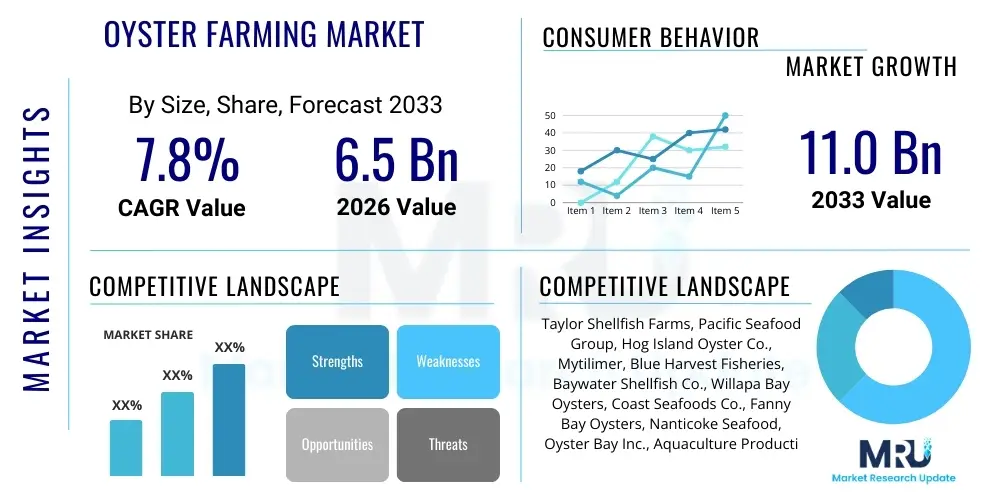

The Oyster Farming Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $6.5 Billion USD in 2026 and is projected to reach $11.0 Billion USD by the end of the forecast period in 2033.

Oyster farming, or ostreiculture, involves the cultivation of oysters for consumption and sometimes for their pearls or shell components. This specialized sector of aquaculture has experienced significant resurgence due to growing global demand for high-protein seafood delicacies and increasing focus on sustainable food production methods. Modern oyster farming techniques are far removed from traditional methods, integrating advanced hatchery practices, selective breeding programs, and diverse grow-out systems such as rack and bag, longlines, and off-bottom cages. The primary species cultivated include the Pacific Oyster (Crassostrea gigas), the European Flat Oyster (Ostrea edulis), and various native species tailored to local ecological conditions. The inherent environmental benefits of oyster cultivation, such as their role in water filtration and habitat creation, further drive institutional and consumer interest, positioning the market favorably for sustained expansion.

The major applications of farmed oysters predominantly center around the food service industry, including high-end restaurants, seafood bars, and specialized retail markets globally. Oysters are valued not only for their unique flavor profile but also for their nutritional density, being rich sources of zinc, iron, and Omega-3 fatty acids. This health benefit profile resonates strongly with modern consumer trends prioritizing functional and natural foods. Furthermore, the oyster farming industry contributes substantially to local economies in coastal regions, supporting jobs in processing, distribution, and associated tourism, thereby reinforcing its socio-economic importance.

Key driving factors accelerating market growth include rapid urbanization and globalization, which have introduced oysters to new consumer bases outside traditional coastal regions, facilitated by robust international supply chains. Technological advancements, particularly in disease management, water quality monitoring, and genetic improvement of oyster strains, have significantly improved yield predictability and reduced operational risks. Furthermore, governmental initiatives and policy support aimed at promoting sustainable aquaculture practices act as strong tailwinds, encouraging investment in resilient and environmentally sound farming operations necessary to meet the burgeoning global seafood demand while adhering to stringent food safety regulations.

The global Oyster Farming Market is characterized by robust growth, driven primarily by strong consumer appetite for premium seafood and innovations in cultivation technology. Current business trends indicate a significant shift towards land-based aquaculture systems and closed containment technologies, although traditional coastal methods remain dominant. Increased investment in genetically modified spat (juvenile oysters) and triploid strains, which grow faster and remain marketable during spawning seasons, is boosting profitability across the value chain. Regulatory changes focused on traceability and quality assurance are pushing farmers toward greater operational transparency and the adoption of advanced monitoring systems, ensuring high standards of safety and freshness from farm to table.

Regional trends highlight the dominance of the Asia Pacific (APAC) region, led by production giants such as China and South Korea, which benefit from extensive coastline infrastructure and long-standing aquaculture traditions. However, North America and Europe are experiencing rapid value growth, fueled by strong demand for niche, high-quality artisanal oysters and the increasing popularity of "Oyster Bars" and raw seafood concepts. The market is also seeing increased consolidation among smaller, localized farms being acquired by larger corporate entities seeking economies of scale and improved distribution networks, particularly targeting markets with limited domestic supply.

Segmentation trends reveal that the Pacific Oyster segment holds the largest market share due to its rapid growth rate and adaptability to various farming environments. Methodologically, off-bottom and rack and bag systems are favored for their ability to protect oysters from predators and improve handling efficiency, optimizing growth and reducing labor costs compared to traditional on-bottom methods. The distribution segment is witnessing rapid evolution, with direct-to-consumer (D2C) channels and sophisticated cold chain logistics gaining traction, offering better margins for producers and ensuring maximum freshness for end-users, thus transforming how oysters are marketed and sold to both food service operators and general consumers seeking gourmet ingredients.

Analysis of common user questions regarding the integration of Artificial Intelligence (AI) in oyster farming reveals a strong interest in predictive analytics concerning water quality, disease outbreak forecasting, and yield optimization. Users frequently inquire about how machine learning algorithms can process vast amounts of sensor data (temperature, salinity, pH, dissolved oxygen) to provide actionable insights, thereby minimizing environmental risks and maximizing biological efficiency. Key concerns center around the initial capital expenditure required for installing necessary IoT infrastructure and the need for specialized training to interpret complex AI-generated models. Expectations are high regarding the capability of AI to automate grading, sorting, and inventory management, leading to significant reductions in manual labor and human error, ultimately driving a shift towards "Precision Ostreiculture" as the standard operational model for large-scale production facilities.

AI's influence is expected to dramatically enhance the resilience and sustainability of oyster farming operations. By utilizing predictive modeling based on historical environmental data and real-time monitoring inputs, farmers can proactively adjust farming parameters, such as the depth of submerged racks or the timing of harvest, optimizing growth rates while mitigating risks associated with harmful algal blooms (HABs) or sudden shifts in weather patterns. This sophisticated level of operational control not only safeguards the oyster stock but also enhances the environmental responsibility of the farming entity, aligning with global mandates for sustainable food production and addressing consumer demand for ethically sourced seafood. The ability of AI systems to continuously learn and refine these operational protocols ensures long-term efficiency gains and improved stock health.

The implementation of Computer Vision and machine learning in processing plants is also a focal point of user inquiry. Automated systems capable of rapid visual assessment for size, shape, and quality ensure consistent product grading, crucial for maintaining premium market pricing. Furthermore, AI tools are being developed to monitor the genetic performance of broodstock, assisting in selective breeding programs to enhance disease resistance and desirable traits, such as meat yield and shell robustness. This shift towards data-driven cultivation minimizes waste, improves regulatory compliance through impeccable traceability records, and allows market players to respond dynamically to fluctuating environmental conditions and supply chain disruptions, solidifying AI as a transformative technology in this niche aquaculture sector.

The Oyster Farming Market is propelled by strong Drivers, tempered by significant Restraints, and presents clear long-term Opportunities, all influenced by dynamic Impact Forces. Key drivers include the escalating global demand for high-quality, protein-rich food sources, particularly in developed economies where oysters are viewed as a premium, healthy, and low-fat delicacy. Furthermore, the inherent environmental sustainability of oyster farming—as filter feeders, they clean surrounding waters—is increasingly recognized, attracting both environmentally conscious consumers and governmental support for eco-friendly aquaculture. Opportunities lie in the expansion into non-traditional markets, the development of specialized disease-resistant triploid oyster strains, and leveraging technological advancements like offshore farming systems which allow cultivation in deeper, cleaner waters, thereby mitigating coastal pressures and expanding potential farming area significantly, paving the way for scalable growth.

However, the market faces significant restraints. Disease outbreaks, such as those caused by the OsHV-1 virus, pose substantial risks, leading to mass mortality events and necessitating stringent biosecurity measures which increase operational costs. Environmental volatility, including ocean acidification and increasing frequency of extreme weather events, directly threatens coastal farming infrastructure and oyster health. Regulatory hurdles concerning water lease permits, quality standards, and environmental impact assessments can also create bottlenecks, particularly for new entrants or operations seeking rapid expansion. These complex interactions of biological risks and environmental pressures require farmers to maintain high levels of vigilance and invest heavily in resilient infrastructure and sophisticated monitoring technologies to ensure market continuity and stability, thus adding layers of complexity to operational management.

The impact forces shaping the market include technological advancements, which drive down operating costs and improve yield; stringent food safety regulations, which elevate quality standards and consumer confidence; and shifting demographics, which contribute to a rising middle class globally with greater disposable income for luxury food items. Furthermore, the competitive intensity among seafood producers, coupled with fluctuations in input costs (such as spat and labor), places continuous pressure on pricing strategies and supply chain efficiency. These forces necessitate that market players not only focus on optimizing farming yields but also on building robust cold chain logistics and achieving recognized sustainability certifications (like ASC or BAP) to maintain competitive advantage and secure premium pricing in saturated markets, ultimately defining success within this specialized segment of the seafood industry.

The Oyster Farming Market is broadly segmented based on Product Type, Farming Method, and Application, providing a granular view of market dynamics and consumer preferences. Product Type segmentation is crucial as different oyster species possess distinct growth rates, taste profiles, and market prices, influencing regional production dominance. Farming Methods dictate capital investment, environmental interaction, and operational efficiency, with modern methods increasingly favored over traditional approaches due to improved yields and better protection against adverse conditions. Application analysis differentiates between high-volume food service demand and specialized retail distribution, reflecting varying requirements in terms of processing, packaging, and logistics management necessary for quality maintenance.

The segmentation structure assists stakeholders, including investors, producers, and regulatory bodies, in understanding specific niche markets and allocating resources effectively. For example, understanding the growing demand within the 'Food Service' application segment for triploid Pacific Oysters cultivated via 'Rack and Bag' methods in specific geographic areas allows businesses to tailor their production output and marketing strategies for maximum profitability. Furthermore, the differentiation of markets based on the 'Product Type' highlights regional specialization; for instance, European markets maintain strong demand for the native European Flat Oyster, justifying specialized, albeit higher-cost, farming practices compared to the ubiquitous Pacific Oyster.

This detailed segmentation not only clarifies market structure but also aids in strategic forecasting. Analyzing the growth trajectory of the 'Off-Bottom' farming method, for instance, confirms the industry's shift towards minimizing substrate contact and maximizing water flow, which translates into better quality and faster growth. This trend requires complementary investments in specialized equipment and mooring systems. Similarly, tracking the ‘Retail’ segment growth indicates a successful penetration of oysters into everyday consumption habits rather than solely being reserved for luxury dining experiences, pushing demand for more standardized, easy-to-handle packaging and ensuring robust cold-chain integrity all the way to the consumer's household.

The value chain for the Oyster Farming Market is sequential and complex, beginning with upstream activities focused on genetic material and spat production, moving through the grow-out phase (midstream), and concluding with processing, distribution, and consumption (downstream). The upstream segment is dominated by specialized hatcheries and nurseries responsible for spawning and early-stage growth of oyster spat, often involving sophisticated selective breeding programs to ensure disease resistance and rapid growth traits. The quality and reliability of spat supply are critical bottlenecks, making this a high-value, high-technology phase requiring specialized biological and genetic expertise.

The midstream operations, which encompass the actual grow-out phase on aquaculture leases, vary significantly based on the farming method (e.g., rack and bag versus longline). This phase involves significant operational expenses related to infrastructure maintenance, water quality monitoring, labor-intensive flipping and cleaning of baskets (tumbling), and predator control. Efficiency in the midstream is directly tied to environmental stability and the application of precision aquaculture technologies. Successful operations rely on minimizing mortality rates and optimizing the grow-out period to achieve marketable size within the shortest feasible timeframe, requiring skilled aquaculture managers and continuous environmental assessment.

Downstream activities involve harvesting, purification, processing, packaging, and distribution. Given that oysters are often consumed raw, purification (depuration) in controlled tanks is mandatory to meet stringent public health standards. The distribution channel is crucial, utilizing highly specialized cold chain logistics to maintain freshness and safety. Distribution is often segmented into direct channels (farm-to-table, local markets) and indirect channels (wholesalers, large seafood distributors, and exporters). The rise of direct-to-consumer models, facilitated by e-commerce and specialized courier services, is disrupting traditional wholesaler dominance, offering producers higher margins and greater control over branding and quality representation, directly benefiting premium oyster producers.

The primary potential customers and end-users of farmed oysters are concentrated across three key sectors: the High-End Food Service Industry (HORECA), upscale Retail Chains, and the growing segment of direct-to-consumer (D2C) specialty buyers. HORECA establishments, including fine-dining restaurants, luxury hotels, and dedicated oyster bars, represent the largest value segment, demanding premium quality, consistency in size and flavor profile, and reliable year-round supply for their raw bar offerings. Chefs often seek specialized, branded oysters with unique terroir characteristics, creating a strong market for differentiated products and smaller, artisanal producers capable of meeting exacting quality specifications and high freshness requirements.

Retail consumers, purchasing through high-end supermarkets, hypermarkets, and specialty seafood stores, constitute the second major segment. This customer base, which is growing due to increased oyster accessibility and improved packaging, seeks convenience and educational guidance on preparation. Retail penetration requires standardized packaging, detailed labeling regarding origin and freshness date, and competitive pricing, particularly for common species like the Pacific Oyster. Retailers look for suppliers who can guarantee scale and strict compliance with food safety certifications, making large-scale, certified farms preferred partners in this distribution channel.

The D2C segment, while smaller in volume, is high-growth and margin-rich. These customers are typically affluent, discerning food enthusiasts who prioritize traceability, freshness, and the story behind the product. They utilize online platforms or direct farm subscription models, demanding ultra-fresh oysters delivered quickly under optimal cold chain conditions. Additionally, secondary potential customers include pharmaceutical companies (utilizing oyster components for supplements due to high mineral content), research institutions (for ecological studies), and the decorative industry (using shells), though these applications currently represent a niche portion of the total market demand and generally focus on co-products or waste utilization rather than primary food production.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $6.5 Billion USD |

| Market Forecast in 2033 | $11.0 Billion USD |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Taylor Shellfish Farms, Pacific Seafood Group, Hog Island Oyster Co., Mytilimer, Blue Harvest Fisheries, Baywater Shellfish Co., Willapa Bay Oysters, Coast Seafoods Co., Fanny Bay Oysters, Nanticoke Seafood, Oyster Bay Inc., Aquaculture Production Technology (APT) Ltd., Signature Oysters, Acadia Aquaculture, Chesapeake Bay Oyster Co., Huitres Geay, Pangea Shellfish Company, Australian Oyster Coast, White Stone Oyster Co., Little Skookum Shellfish Growers. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution in the Oyster Farming Market centers primarily on enhancing biological efficiency, mitigating environmental risk, and optimizing post-harvest handling. In the early stages, significant focus is placed on advanced hatchery technologies, including selective breeding programs utilizing molecular markers and genomic tools to develop genetically superior oyster spat that exhibit faster growth rates, tolerance to temperature fluctuations, and robust resistance to common pathogens like the herpesvirus (OsHV-1). The widespread adoption of triploid oyster technology, which produces sterile oysters that do not spawn, is a critical innovation that ensures high-quality, plump meat is available year-round, circumventing seasonal market dips associated with the spawning period, thereby maximizing profitability and market consistency.

During the grow-out phase, the integration of Precision Aquaculture techniques, enabled by the Internet of Things (IoT) and sensor networks, is transforming operational management. These technologies involve deploying real-time monitoring systems that track crucial water quality parameters (temperature, salinity, pH, chlorophyll-a levels) across the lease area. Data generated by these sensors is fed into cloud-based platforms and analyzed using machine learning algorithms, providing farmers with instant alerts regarding potential environmental threats, such as hypoxic events or the onset of harmful algal blooms (HABs). This proactive management capability allows for timely intervention, such as adjusting rack depths or accelerating harvest, drastically reducing the risk of mass mortality and safeguarding stock integrity, which is paramount for raw consumption markets.

Furthermore, mechanization and automation are increasingly utilized to reduce the high labor costs associated with traditional farming. Automated gear handling systems, such as specialized barges and hydraulic lifts, simplify the processes of flipping oyster bags (tumbling, which chips the shell edge to improve cup depth and shape) and moving racks, enhancing efficiency and minimizing physical strain on workers. Post-harvest, technologies related to depuration (UV and ozone sterilization systems) and advanced sorting/grading machinery utilizing computer vision ensure that every oyster reaching the consumer is purified, consistently sized, and meets rigorous health and aesthetic standards, supporting the market's trajectory towards industrialization and large-scale, high-quality production across diverse geographic regions.

Geographic analysis reveals diverse market characteristics and growth drivers across major global regions, reflecting historical aquaculture traditions, varying consumer demand profiles, and distinct regulatory environments.

The Oyster Farming Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033, driven by increasing global demand for premium seafood and advancements in sustainable farming technologies.

The Asia Pacific (APAC) region, specifically countries like China and South Korea, currently dominates the global oyster farming market in terms of production volume due to extensive aquaculture infrastructure and high domestic consumption rates.

Triploid oysters are sterile, genetically engineered oysters that possess three sets of chromosomes. They are crucial because they do not undergo seasonal spawning, allowing them to maintain high meat quality and marketability throughout the entire year, significantly increasing farm profitability.

Key technological challenges include effectively mitigating the risk of disease outbreaks like OsHV-1, adapting infrastructure to climate change-induced ocean acidification, and the necessity of integrating complex, costly IoT and AI systems for real-time water quality monitoring and yield optimization.

Oysters are natural filter feeders; they improve water quality by removing excess nitrogen, pollutants, and suspended particulates. They also enhance local biodiversity by creating essential marine habitats, making oyster farming an intrinsically sustainable and restorative aquaculture practice.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.