ID : MRU_ 431470 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

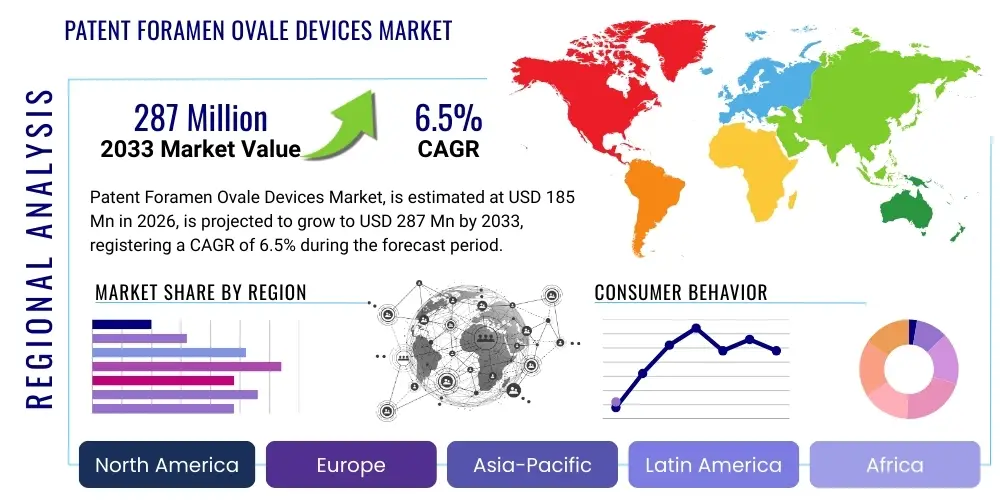

The Patent Foramen Ovale Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 185 million in 2026 and is projected to reach USD 287 million by the end of the forecast period in 2033. This consistent expansion is primarily fueled by the increasing clinical evidence supporting PFO closure in patients who have suffered cryptogenic strokes and the ongoing advancements in minimally invasive transcatheter device technology, which enhance procedural safety and efficacy.

The Patent Foramen Ovale Devices Market encompasses medical implants and associated delivery systems designed to close the PFO, a residual opening between the right and left atria of the heart that persists after birth in approximately 25% of the general population. While often asymptomatic, a PFO is a recognized anatomical risk factor, particularly implicated in cases of cryptogenic stroke (CS) through paradoxical embolism. The primary products in this market are catheter-delivered occlusion devices, typically constructed from metallic alloys such as Nitinol and synthetic fabrics.

Major applications for PFO closure devices center around secondary prevention of recurrent stroke in patients diagnosed with CS, especially those with high-risk anatomical features like a large shunt or atrial septal aneurysm. Furthermore, off-label applications, including the management of severe migraine with aura unresponsive to medication and prevention of decompression sickness in deep-sea divers, contribute significantly to market demand. The chief benefit of these devices is providing a minimally invasive, definitive closure option, reducing the long-term risk of stroke recurrence compared to anticoagulant therapy alone, as demonstrated by landmark clinical trials such as CLOSE and RESPECT.

Key driving factors propelling market growth include the global aging demographic, which increases the overall burden of cardiovascular and cerebrovascular diseases, enhanced diagnostic capabilities, particularly through advanced imaging techniques like transcranial Doppler and transesophageal echocardiography (TEE), and favorable policy changes regarding reimbursement for PFO closure procedures following robust clinical trial data validation. Additionally, patient preference for transcatheter interventions over traditional surgical methods further solidifies the market’s upward trajectory.

The Patent Foramen Ovale Devices Market is characterized by robust growth driven by favorable clinical outcomes and technological innovation. Business trends indicate a strong shift toward devices offering enhanced safety profiles, such as those made from biodegradable or bioabsorbable materials, aiming to minimize the long-term risk of thrombogenicity and metal-related complications. Strategic collaborations between device manufacturers and specialized cardiology centers are central to expanding market penetration and improving physician training on complex delivery systems. Furthermore, the market sees significant consolidation efforts as larger medical device companies acquire specialized PFO device innovators to broaden their structural heart portfolios and gain access to proprietary closure technologies.

Regionally, North America maintains the largest market share, attributable to established reimbursement mechanisms, a high prevalence of PFO diagnosis due to sophisticated healthcare infrastructure, and the early adoption of evidence-based closure guidelines, particularly post-2017 FDA approvals. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate. This acceleration is supported by rapidly expanding healthcare expenditure in countries like China and India, increasing awareness of PFO-related stroke risks, and improving access to advanced catheterization labs. European markets also exhibit steady growth, influenced primarily by comprehensive national stroke prevention guidelines and strong utilization of established device platforms.

Segment trends highlight the dominance of occlusion devices (implants) over delivery systems, reflecting their critical role as the definitive therapeutic product. Within applications, the cryptogenic stroke segment remains the primary revenue generator, yet the specialized segments, particularly migraine treatment, offer significant untapped potential as clinical data matures. End-user analysis reveals that hospitals, especially large cardiovascular and neurovascular centers, are the predominant procurement channels, benefiting from high procedural volume and the availability of specialized interventional cardiologists and neurologists skilled in transcatheter PFO closure techniques. The market’s overall momentum is securely linked to continuous data generation proving the superior long-term safety and efficacy of PFO closure in high-risk patient populations.

User inquiries regarding AI's influence in the PFO device domain center on optimizing patient selection protocols, improving procedural guidance, and predicting long-term outcomes. Common questions revolve around whether AI algorithms can more accurately identify which PFO patients are truly high risk for recurrent stroke, thereby maximizing the cost-effectiveness of device implantation, and how machine learning can interpret complex cardiac images (like TEE/ICE) to assist interventionalists in real-time. Key concerns include data privacy related to patient cardiac imagery and the validation needed to ensure AI-driven diagnostic tools meet rigorous clinical standards before impacting treatment decisions. Users expect AI to reduce procedural variability, personalize device sizing, and eventually automate certain aspects of procedural imaging analysis, leading to shorter procedure times and improved safety margins, ultimately expanding the eligible patient pool benefiting from PFO closure devices.

The PFO Devices Market is propelled by strong clinical evidence validating the benefit of PFO closure in secondary stroke prevention, offset by significant regulatory hurdles and cost constraints. The primary drivers include favorable results from large randomized controlled trials (RCTs) which demonstrated the superiority of device closure combined with antiplatelet therapy over medical therapy alone in reducing recurrent stroke. Coupled with this, the increasing global prevalence of cryptogenic stroke, particularly in younger populations, mandates a shift toward definitive intervention. However, the market faces restraints due to the high upfront cost of advanced transcatheter devices and associated hospital procedures, which can be prohibitive in developing economies. Furthermore, the necessity for highly specialized technical skills and rigorous training for interventionalists poses a bottleneck in expanding service availability outside major medical centers. Stringent and often lengthy regulatory approval processes, particularly in regions like the U.S. and Europe, also restrain the rapid introduction of novel device designs, affecting the pace of innovation adoption.

Significant opportunities exist in emerging economies where rising healthcare infrastructure investment and expanding insurance coverage are opening new patient populations previously restricted by economic barriers. Technological advancements focusing on bioresorbable devices represent a major opportunity, aiming to address concerns regarding long-term foreign body presence and late complications like atrial fibrillation. The growing recognition of PFO closure’s potential role in managing severe, refractory migraines also offers a substantial, albeit currently niche, market expansion pathway, contingent upon further positive clinical trial data. Leveraging telemedicine and remote patient monitoring post-procedure presents an opportunity for enhanced follow-up care and early detection of complications.

The core impact forces shaping this market involve a combination of regulatory policy shifts, technological disruption, and clinical consensus evolution. Regulatory bodies worldwide are becoming more aligned with accepting the robust clinical data, leading to broader insurance coverage and inclusion in clinical guidelines. The power of technology lies in creating smaller, more conformable devices with simplified delivery systems. Clinical opinion, driven by interventional neurologists and cardiologists, remains a vital force; widespread acceptance of PFO closure as a standard of care for specific patient subsets ensures sustained demand, overriding residual clinical skepticism that existed prior to recent definitive RCTs.

The Patent Foramen Ovale Devices Market segmentation provides a granular view of product utilization, defining market dynamics based on the types of devices, their intended clinical applications, and the healthcare settings where procedures are performed. This analysis is essential for manufacturers tailoring their research and development efforts and for healthcare providers optimizing device procurement. The segmentation highlights the intrinsic link between device design innovation, clinical needs, and procedural environment. For instance, the transition toward next-generation devices, such as those that are entirely biodegradable, is reshaping the product segment, aiming for enhanced patient outcomes and reduced long-term risk profiles, which subsequently influences adoption rates across various end-user settings.

The segmentation by application clearly demonstrates the overwhelming economic impact of secondary stroke prevention, although emerging applications like refractory migraine treatment are critical indicators of future diversification potential. Device closure for cryptogenic stroke remains the foundational revenue stream, attracting the majority of R&D investment and clinical trials. Conversely, the segmentation by end-user reflects the capital-intensive nature of PFO closure; specialized hospitals with comprehensive structural heart programs and cardiac catheterization laboratories dominate service provision. Understanding these segments allows stakeholders to strategically allocate resources, focusing on regions and customer types most receptive to high-value cardiovascular interventions. The continued refinement of diagnostic techniques also inherently influences the market, driving demand for devices designed for increasingly subtle or complex PFO anatomies identified through advanced imaging.

The value chain for PFO devices begins with rigorous upstream activities dominated by specialized research and development (R&D) focused on material science, including biocompatible alloys like Nitinol and innovative biodegradable polymers. Manufacturing involves complex, precision-engineering processes in highly controlled environments to ensure device integrity and sterilization, adhering to stringent quality standards mandated by regulatory bodies like the FDA and EMA. This phase is characterized by high barriers to entry due to the technical expertise and capital required for compliant production facilities. Downstream activities involve distribution channels, which are typically highly controlled and managed, relying heavily on direct sales forces and specialized medical device distributors who maintain close relationships with interventional cardiologists and hospital procurement departments.

Distribution channels in this market are predominantly indirect, utilizing specialized distributors who handle inventory, logistics, and technical support due to the devices' complexity and high value. However, major manufacturers often employ direct sales representatives for high-volume accounts and training purposes, especially in North America and Western Europe, ensuring direct communication regarding clinical outcomes and technical updates. The relationship between manufacturers and healthcare professionals is crucial, often involving training centers and clinical workshops to disseminate best practices for transcatheter implantation. The complexity of the procedures necessitates significant physician education, making clinical support a critical component of the distribution channel’s added value.

The end-user segment, consisting primarily of specialized cardiac centers and hospitals, drives the final stage of the value chain. Their purchasing decisions are influenced not only by device cost and clinical efficacy but significantly by reimbursement policies and the availability of specialized staff. Due to the involvement in life-saving procedures, the emphasis remains heavily on device quality, proven clinical track record, and robust after-sales support, rather than solely on price. The structure of the value chain, from specialized R&D to tightly controlled distribution, reflects the high-risk, high-reward nature of the structural heart device industry.

Potential customers for Patent Foramen Ovale devices are primarily healthcare institutions and medical specialists focused on structural heart disease and cerebrovascular prevention. The key decision-makers include interventional cardiologists, who perform the transcatheter closure procedure, and neuro-intervention specialists or neurologists, who often diagnose the cryptogenic stroke and refer patients for cardiac evaluation. Institutional buyers encompass tertiary care hospitals, university medical centers, and specialized heart institutes that maintain dedicated cardiac catheterization laboratories equipped for complex structural heart procedures. These institutions invest in PFO devices as part of their comprehensive offerings for stroke prevention and cardiovascular disease management.

The ultimate end-users/buyers are patients diagnosed with a PFO who have suffered a recent cryptogenic ischemic stroke or transient ischemic attack (TIA) and meet specific anatomical criteria, as defined by major clinical guidelines. Furthermore, a smaller but significant segment includes highly symptomatic migraine patients for whom alternative treatments have failed, provided their PFO is deemed anatomically amenable to closure, although this remains a more scrutinized area. Due to the high cost and invasiveness of the procedure, device selection and usage are entirely dictated by physician referral, insurance coverage, and institutional protocols, making the specialized physician the true gateway to market demand.

As the market matures, Ambulatory Surgical Centers (ASCs) are increasingly becoming potential customers, particularly those affiliated with large hospital networks, aiming to capitalize on the shift toward outpatient cardiac procedures. This shift is driven by efforts to reduce healthcare costs and improve patient convenience. However, the high-risk nature of structural heart interventions means that the majority of procedures will continue to be centralized in large hospitals, which can provide immediate, multi-disciplinary emergency support, solidifying their status as the primary procurement channel for advanced PFO closure devices and delivery systems.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 185 million |

| Market Forecast in 2033 | USD 287 million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Abbott Laboratories, Boston Scientific Corporation, Medtronic Plc, W. L. Gore & Associates, Inc., Cardinal Health (acquired Access Closure), LifeTech Scientific Corporation, Occlutech AG, PFM Medical AG, Bard Peripheral Vascular (BD), Hangzhou Lekang Medical Devices Co., Ltd., Shanghai Shape Memory Alloy Materials Co., Ltd., MicroPort Scientific Corporation, Venus Medtech (Hangzhou) Inc., Starway Medical Technology, Inc., Cardia, Inc., Terumo Corporation, Edwards Lifesciences Corporation, Cook Medical, Getinge AB, Sorin Group (LivaNova PLC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the PFO Devices Market is defined by continuous innovation in material science and procedural guidance systems aimed at enhancing efficacy and safety. The foundational technology involves self-centering and self-expanding devices, primarily utilizing Nitinol (nickel titanium) frames due to its superelasticity and shape memory properties, allowing for minimal invasiveness during delivery and optimal conformability upon deployment within the complex cardiac anatomy. Current technological progression is focused on reducing the metal mass implanted to minimize the long-term risk of endothelial damage and subsequent thrombus formation. Next-generation devices integrate low-profile designs and specialized anchor mechanisms to ensure secure closure while minimizing interaction with surrounding cardiac structures, which is critical for reducing the incidence of post-procedural complications such as device erosion or atrial fibrillation.

A significant area of technological focus is the development and commercialization of bioresorbable or biodegradable PFO closure devices. These devices, often constructed from materials like poly-L-lactic acid (PLLA) or magnesium alloys, are designed to maintain structural integrity long enough for the PFO tract to naturally seal and heal, after which the device material dissolves harmlessly. This addresses a major long-term patient concern associated with permanent metallic implants. While still a nascent segment, biodegradable devices hold immense promise for capturing future market share by eliminating the need for lifelong foreign body management and related anticoagulant therapy, provided their acute closure rates remain comparable to established metallic devices.

Furthermore, procedural technology, specifically advanced imaging, plays a pivotal role in device success. Intracardiac echocardiography (ICE) has increasingly replaced traditional transesophageal echocardiography (TEE) for intra-procedural guidance, offering high-resolution imaging without the need for general anesthesia, improving patient comfort and procedural efficiency. Hybrid procedures combining fluoroscopy with advanced 3D anatomical mapping technologies are also becoming standard, allowing interventionalists to accurately size the PFO, select the appropriate device, and monitor deployment in real time, contributing directly to reduced procedural time and radiation exposure, thereby improving overall outcomes and accelerating market adoption.

The PFO Devices Market exhibits distinct regional dynamics, dictated by healthcare expenditure, regulatory environments, and the clinical acceptance of PFO closure guidelines.

The primary application driving market demand is the secondary prevention of recurrent stroke in patients who have experienced a cryptogenic ischemic stroke (CS) and are found to have a Patent Foramen Ovale (PFO), especially when anatomical risk factors suggest high probability of paradoxical embolism.

Bioresorbable devices represent a significant technological shift, as they eliminate the need for a permanent metallic implant. They promote natural tissue closure and then safely dissolve, minimizing long-term risks such as device erosion or chronic inflammation, thereby appealing to patients concerned about foreign body permanence.

North America currently leads the global PFO Devices Market in terms of revenue, primarily due to high procedure volumes, well-established insurance and reimbursement infrastructure, and the early adoption of robust clinical guidelines supporting PFO closure for stroke prevention.

The main restraining factors include the high procedural cost associated with transcatheter intervention, the need for specialized training and infrastructure, and ongoing variability in reimbursement policies, particularly in emerging economies and for off-label applications like migraine treatment.

Advanced imaging, particularly Intracardiac Echocardiography (ICE), plays a critical role by providing real-time, high-resolution visualization for accurate PFO sizing, optimal device selection, and monitoring precise deployment, significantly improving procedural success rates and safety without requiring general anesthesia.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.