ID : MRU_ 436210 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

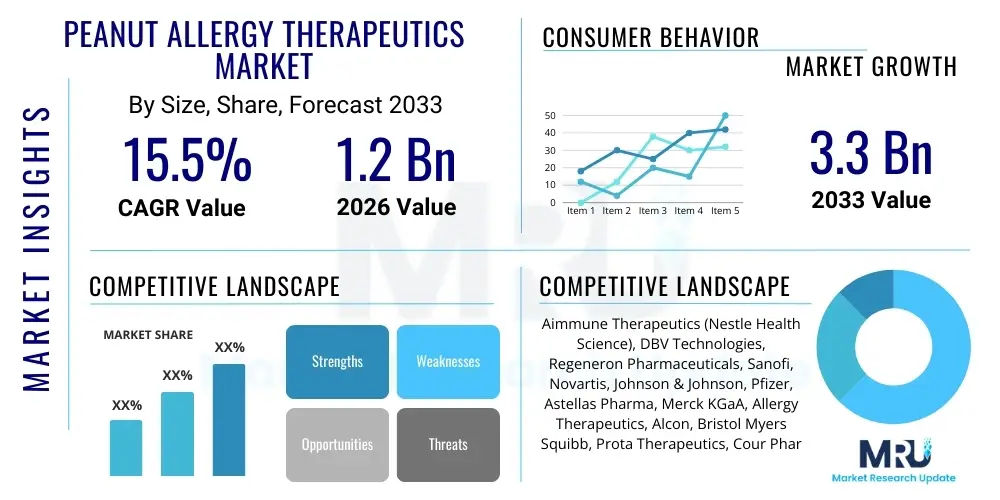

The Peanut Allergy Therapeutics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 3.3 Billion by the end of the forecast period in 2033.

The Peanut Allergy Therapeutics Market encompasses a specialized pharmaceutical and biotechnology sector dedicated to developing and commercializing treatments that mitigate or prevent life-threatening allergic reactions to peanuts. Peanut allergy, one of the most common and severe food allergies, represents a significant unmet medical need globally. The current treatment landscape is rapidly shifting from solely reliance on emergency management (epinephrine autoinjectors) toward proactive, disease-modifying therapies, primarily various forms of immunotherapy. These therapeutics aim to desensitize the patient's immune system to peanut proteins, thereby raising the reaction threshold and offering protection against accidental exposure.

Products within this market range from FDA-approved biological products like oral immunotherapies (OIT) to emerging epicutaneous and sublingual delivery systems. Major applications center around pediatric populations, where peanut allergy prevalence is highest, though adult treatments are also gaining traction. The primary benefit of these advanced therapeutics is enhanced quality of life for patients and reduced anxiety for caregivers, moving beyond symptomatic relief to offering functional immunity. Furthermore, the introduction of standardized, commercially prepared dosing protocols significantly improves safety profiles compared to previous experimental desensitization methods.

Key driving factors propelling market expansion include the rising global incidence of peanut allergies, increasing patient awareness coupled with proactive diagnostic testing, and robust investments in clinical trials leading to novel drug approvals. Regulatory bodies, particularly the FDA and EMA, have streamlined pathways for therapies addressing high-impact allergic conditions, incentivizing pharmaceutical companies. The economic burden associated with managing chronic allergies and emergency room visits also fuels demand for preventative, long-term therapeutic solutions, positioning this market for accelerated growth throughout the forecast period.

The Peanut Allergy Therapeutics Market is currently characterized by significant transformative business trends centered on shifting from diagnostic management to curative or disease-modifying intervention. Key business trends include aggressive mergers and acquisitions focused on securing proprietary drug delivery technologies, particularly in the epicutaneous patch segment, and increasing strategic partnerships between large pharmaceutical corporations and specialized biotech firms to accelerate clinical development timelines. High pricing strategies for novel, approved immunotherapies reflect the significant research and development costs, necessitating rigorous pharmacoeconomic studies to demonstrate long-term value to payers and health systems, which remains a key commercial challenge and opportunity.

Regionally, North America maintains the dominant market share, driven by high prevalence rates, advanced healthcare infrastructure, and favorable reimbursement policies for FDA-approved OIT products. Europe is poised for rapid growth, benefiting from regulatory harmonization through the EMA, though product adoption rates vary based on national healthcare funding models and physician acceptance. Asia Pacific (APAC) represents a critical growth frontier, characterized by increasing urbanization, Westernized diets contributing to higher allergy rates, and developing specialized allergy centers in key economies like Japan, Australia, and China, attracting significant foreign investment in clinical trials.

Segmentation trends highlight the dominance of Oral Immunotherapy (OIT) by revenue, primarily due to first-mover advantage and regulatory approval of commercialized products. However, the Epicutaneous Immunotherapy (EPIT) segment is projected to exhibit the fastest Compound Annual Growth Rate (CAGR), driven by its potential for improved patient compliance, reduced systemic side effects, and non-invasive administration appealing particularly to pediatric populations. Furthermore, the rise in personalized medicine approaches utilizing biomarker analysis is segmenting the market based on patient responsiveness and severity, demanding targeted therapeutic development.

Analysis of common user questions related to AI's impact reveals strong interest in personalized dosing and improved diagnostic accuracy. Users frequently inquire about how AI can refine risk stratification for patients undergoing immunotherapy, predict individual response rates to specific treatments, and accelerate the discovery of novel therapeutic targets beyond traditional allergen extracts. There is also significant curiosity regarding AI's role in optimizing clinical trial designs, reducing regulatory hurdles, and enhancing post-market surveillance for long-term safety and efficacy data collection. These inquiries collectively highlight user expectations that AI will move the field towards highly predictive, safe, and individualized treatment regimens, addressing the inherent variability in patient immune responses currently challenging mass-market adoption.

The application of Artificial Intelligence within the Peanut Allergy Therapeutics Market is fundamentally changing research paradigms, moving away from generalized approaches toward precision allergology. AI algorithms are crucial for analyzing the complex, multi-omic datasets generated in modern immunology, including genomics, transcriptomics, and proteomics, which hold the key to understanding why some patients achieve tolerance while others experience persistent reactions or severe side effects during desensitization. By integrating these massive data points, AI can construct sophisticated models capable of predicting immunological outcomes with higher accuracy than conventional statistical methods, thereby ensuring that the right patient receives the right dose of the right therapy.

Furthermore, AI significantly enhances the commercial viability of these expensive and lengthy treatments. In the clinical setting, AI-powered decision support tools assist allergists in navigating the complexities of OIT protocols, ensuring maximum safety and compliance. For instance, an AI tool could monitor factors such as concurrent illness, stress levels, and recent non-adherence, adjusting the required supervision or subsequent dosing increments accordingly. This reduction in clinical variability and improvement in safety profile not only benefits the patient but also strengthens the value proposition to insurance providers, accelerating favorable coverage decisions crucial for market penetration.

The ethical and regulatory aspects of deploying AI in sensitive health fields, particularly concerning potential bias in algorithms trained on limited population data, remain a point of concern. However, industry efforts are focused on developing transparent, explainable AI (XAI) models that provide clinicians with clear justifications for treatment recommendations. This focus on verifiable and interpretable AI outputs ensures clinical adoption rates remain high, fostering confidence among healthcare professionals in leveraging these advanced tools to manage the inherent risks associated with treating severe peanut allergy.

The Peanut Allergy Therapeutics Market is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming significant impact forces. Key drivers include the escalating global prevalence of peanut allergies, particularly in Western nations, which increases the addressable patient pool. This is strongly coupled with successful regulatory approvals of innovative therapies, moving treatments from observational protocols to standardized commercial products. Restraints predominantly revolve around the high cost of current immunotherapies, which challenges healthcare affordability and broad reimbursement coverage, alongside the inherent risks associated with treatment, such as the potential for severe adverse reactions requiring vigilant clinical supervision. Opportunities are found in the development of safer, second-generation therapies like EPIT, exploring combination therapies, and expanding market access into emerging economies, all of which are subject to rigorous regulatory and clinical impact forces.

Drivers: The most significant driver is the increasing recognition of the profound quality-of-life impact caused by food allergies, prompting patients and advocacy groups to actively seek disease-modifying treatments. Regulatory fast-tracking for therapies addressing major unmet needs, such as the FDA’s approach to treatments like Palforzia, shortens the time-to-market and incentivizes innovation. Furthermore, robust clinical evidence demonstrating the long-term benefits of sustained unresponsiveness (SU) post-treatment encourages greater acceptance among healthcare professionals, shifting the focus from emergency care to preventative therapeutic intervention. The pharmaceutical industry's capability to manufacture standardized, high-quality peanut protein derivatives ensures consistency and safety across therapeutic batches.

Restraints: Despite the benefits, current therapies face substantial restraints. Patient adherence to lengthy, multi-year treatment protocols remains challenging, often leading to suboptimal outcomes. The requirement for initial dosing and subsequent escalations to occur in specialized clinical settings due to the risk of anaphylaxis adds significant complexity and cost, limiting access primarily to urban centers with specialized allergy clinics. Moreover, market competition from non-traditional or off-label desensitization methods, while less safe, presents a cost barrier that pharmaceutical companies must consistently overcome through superior safety and efficacy data. The complex immunologic mechanisms involved mean that treatments are not universally effective across all patient subsets.

Opportunities & Impact Forces: The greatest opportunities lie in pioneering next-generation treatments that offer improved safety profiles, potentially eliminating the need for strict clinical supervision during dosing, such as certain EPIT candidates. Developing personalized medicine strategies using biomarkers to predict treatment success offers a critical market advantage, optimizing resource allocation. Impact forces include significant investment in public health campaigns aimed at early diagnosis and intervention, alongside pressure from payer groups to demonstrate true cost-effectiveness over a patient's lifetime. Regulatory pressures are also driving manufacturers towards developing therapies effective for younger patient cohorts, ideally starting treatment before significant immunological memory is established, offering the potential for true immunological cure rather than just desensitization.

The Peanut Allergy Therapeutics Market is segmented based on several critical factors, primarily revolving around the treatment type, distribution channel, and the age group of the patient population. Understanding these segments is crucial for market stakeholders to tailor commercial strategies and allocate R&D resources effectively. The treatment type segmentation distinguishes between highly regulated, standardized pharmacological therapies (e.g., OIT, EPIT) and emerging adjuvant treatments or combination approaches that enhance desensitization efficacy or safety. This differentiation allows for a clear analysis of market penetration rates and technology adoption across various clinical settings and patient needs.

Segmentation by distribution channel reflects the inherent risks and requirements of dispensing these complex biological products. Since therapies like OIT require careful monitoring and titration, initial distribution is heavily reliant on specialized hospital pharmacies and allergy clinics. However, as maintenance phases begin and newer, safer delivery systems emerge, the role of retail and online pharmacies is expected to expand, particularly for long-term adherence management. The patient age group segment (pediatric vs. adult) is vital because treatment protocols, dosing, and regulatory approval pathways often differ significantly between these populations, with the pediatric segment currently dominating due to the earlier onset and higher prevalence of peanut allergy in children.

Furthermore, segmentation allows for a nuanced understanding of market dynamics influenced by regional healthcare infrastructures and purchasing power. For example, the prevalence of insurance coverage for specific types of immunotherapy dictates which distribution channels are prioritized. The pediatric segment drives the need for non-invasive, child-friendly formulations (like patches), while the adult segment often requires therapies compatible with existing medical conditions and lifestyle factors. As the market matures, novel segmentation based on allergy severity (mild, moderate, severe) and specific biomarker profiles (e.g., IgE levels, component sensitization) will become increasingly important for targeted marketing and clinical trial enrollment.

The value chain for peanut allergy therapeutics is complex, starting with rigorous upstream activities involving R&D and pharmaceutical manufacturing, progressing through intricate clinical testing and regulatory approvals, and concluding with highly specialized distribution and patient support services. Upstream analysis focuses on sourcing and standardizing the allergen material—high-quality peanut protein extracts—which requires sophisticated processing to ensure consistent potency and safety profiles for use in commercial immunotherapy products. Partnerships between biotech companies and agricultural suppliers or specialized allergen manufacturers are essential in this phase. Innovation in drug formulation, such as micro-encapsulation for OIT or transdermal patch technology for EPIT, constitutes the core value addition upstream.

The downstream segment encompasses clinical commercialization and patient management. Unlike traditional pharmaceuticals, the distribution channel for immunotherapies is highly controlled, often relying on Direct-to-Patient models or specialized distribution networks to ensure temperature control and product integrity. Due to the requirement for medically supervised dosing, specialty pharmacy services, which can manage complex insurance paperwork and coordinate with healthcare providers, are integral. Direct customer interaction involves extensive patient education and compliance programs, where pharmaceutical companies invest heavily to ensure safe self-administration during the maintenance phase, effectively bridging the gap between clinical approval and successful patient outcome.

Distribution channels in this market are bifurcated into direct and indirect routes. Direct distribution involves manufacturers supplying specialty clinics or hospital systems directly for the initial high-risk dosing phases. Indirect channels, primarily retail and online specialty pharmacies, handle the long-term maintenance doses, particularly for therapies that have demonstrated high safety profiles during prolonged use. The key value addition downstream is robust pharmacovigilance and patient support systems (often involving proprietary apps or nurse support lines) that enhance safety and maximize treatment adherence, distinguishing successful market players through superior patient support infrastructure rather than just product efficacy alone.

The primary potential customers and end-users of peanut allergy therapeutics are pediatric and adult patients diagnosed with IgE-mediated peanut allergy, along with the specialized healthcare institutions that manage their care. Pediatric patients represent the largest and most actively growing customer base, driven by high incidence rates and the significant long-term benefit of early intervention. Parents and guardians often act as the key purchasers, heavily influenced by recommendations from pediatric allergists and the perceived safety profile of the treatment. Their purchasing decision is heavily mediated by insurance coverage and out-of-pocket costs, making affordability a critical factor.

Institutional buyers, specifically allergy clinics, university hospitals, and specialized pediatric centers, are also crucial customers, acquiring these therapeutics for administration within their controlled clinical environments. These centers represent high-volume purchasers and act as key opinion leaders (KOLs) who determine treatment protocols and influence broader market adoption. Their purchase decisions prioritize the proven efficacy data, the level of training and support provided by the manufacturer, and ease of integration into existing clinical workflows, especially concerning standardized dosing and risk management protocols.

Furthermore, managed care organizations, private insurers, and governmental health systems (payers) are indirect but powerful customers, as their coverage decisions dictate patient access. Pharmaceutical companies must tailor their market access strategies to demonstrate strong pharmacoeconomic value to these payers, proving that the long-term cost of immunotherapy treatment is offset by the reduction in emergency room visits, hospitalizations, and overall societal burden associated with severe allergic reactions. Therefore, potential customers span the entire healthcare ecosystem, from the individual patient seeking desensitization to the organizations funding and administering the treatment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 3.3 Billion |

| Growth Rate | 15.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Aimmune Therapeutics (Nestle Health Science), DBV Technologies, Regeneron Pharmaceuticals, Sanofi, Novartis, Johnson & Johnson, Pfizer, Astellas Pharma, Merck KGaA, Allergy Therapeutics, Alcon, Bristol Myers Squibb, Prota Therapeutics, Cour Pharmaceutical Development, Intrommune Therapeutics, Genentech (Roche), Teva Pharmaceutical Industries, FAES Farma, DBV Technologies, Camallergy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Peanut Allergy Therapeutics Market is defined by innovations in both delivery mechanisms and immune modulation strategies, moving the field beyond traditional subcutaneous injection methods. The most dominant technology currently commercialized is Oral Immunotherapy (OIT), which involves proprietary manufacturing processes for standardized, highly controlled peanut protein powders encapsulated or mixed for ingestion. Companies focus on optimizing the particle size and purity of these extracts to ensure consistent immunological exposure while minimizing batch-to-batch variation, a crucial factor for regulatory compliance and patient safety during dose escalation.

A major area of emerging technological innovation is Epicutaneous Immunotherapy (EPIT), which uses a patch delivery system to administer peanut protein antigens directly to specialized dendritic cells in the skin via the epidermis. This non-invasive approach capitalizes on the skin's immune surveillance capabilities, offering localized immune stimulation that is hypothesized to result in fewer systemic adverse reactions compared to OIT. The key technological challenge here is optimizing the patch design, adhesion, and antigen release kinetics to ensure maximum efficacy over a prolonged wear time, demanding specialized material science and pharmaceutical engineering expertise.

Further technological advancements include the utilization of recombinant proteins and hypoallergenic variants, designed through genetic engineering to present critical epitopes while potentially reducing reactivity. Additionally, adjuvant therapies, often involving monoclonal antibodies targeting IgE (like omalizumab) or other key immune mediators, are being developed as supportive technologies to improve the safety and efficacy of concurrent OIT or EPIT. The integration of advanced diagnostics, such as component-resolved diagnostics (CRD) and basophil activation tests (BAT), powered by machine learning, is essential for personalized medicine, ensuring that treatments are technologically linked to precise patient immunological profiles.

Regional dynamics play a crucial role in the adoption and commercial success of peanut allergy therapeutics, largely dictated by healthcare spending, regulatory alignment, and disease prevalence. North America, encompassing the United States and Canada, holds the leading position in the global market. This dominance is attributable to the highest documented prevalence of peanut allergy, coupled with a robust healthcare system that promotes early diagnosis and provides substantial reimbursement coverage for innovative, high-cost biological therapies. The US FDA's stringent yet efficient approval processes for novel OIT products have facilitated rapid market entry, creating a concentrated base of specialized allergy practitioners and sophisticated clinical infrastructure.

Europe represents the second-largest market, characterized by significant variance in adoption rates across member states. Countries in Western Europe, such as the UK, Germany, and France, exhibit high levels of investment in pediatric allergy research and clinical facilities, driving demand. However, the market penetration is sometimes slowed by national health technology assessment (HTA) bodies, which impose rigorous cost-effectiveness scrutiny before recommending national coverage. The transition towards standardized EU-wide regulatory acceptance via the EMA is positively impacting cross-border commercial strategies, albeit slowly, focusing on specialized drug centers.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market, propelled by demographic shifts, increasing industrialization, and changing dietary patterns that are contributing to rising allergy incidence across key economies like China, India, and Australia. Australia, with its high prevalence rates, acts as a pivotal hub for clinical trials and early adoption of Western therapeutics. While the regulatory landscape in developing Asian nations remains fragmented, the increasing willingness of high-net-worth individuals to pay for advanced, life-saving therapies, coupled with government initiatives to improve pediatric health services, makes APAC a critical long-term investment target for global therapeutic providers seeking substantial growth opportunities.

The primary mechanism is desensitization through controlled, repeated exposure to small, increasing doses of peanut protein (immunotherapy). This process aims to modulate the immune system, specifically altering T-cell responses and decreasing IgE affinity, ultimately raising the threshold of peanut exposure required to trigger an allergic reaction.

High treatment costs are a significant restraint, often leading to challenges in patient access and adherence. Approved therapies carry substantial price tags reflecting R&D investment. Lack of standardized, broad insurance coverage, particularly in initial adoption phases, forces manufacturers to continually demonstrate superior cost-effectiveness to payers for wide market penetration.

Epicutaneous Immunotherapy (EPIT) is projected to experience the fastest compound annual growth rate (CAGR). This acceleration is driven by EPIT's non-invasive nature and superior safety profile relative to Oral Immunotherapy (OIT), offering a mechanism that may reduce the incidence of systemic adverse reactions and improve long-term patient compliance, especially in pediatrics.

The regulatory environment, particularly in North America and Europe, significantly influences the timeline by offering fast-track designations for therapies addressing severe unmet needs. While this accelerates initial approval, regulatory bodies still demand extensive, long-term safety data, particularly concerning the sustainability of desensitization and the potential for late-onset side effects.

Adjuvant therapies, particularly anti-IgE antibodies, serve a crucial role by improving the safety and tolerance of traditional immunotherapies. They are often used concurrently with OIT to temporarily suppress overall immune reactivity, allowing for faster or safer dose escalation and reducing the likelihood of severe adverse events during the most critical phases of desensitization.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.