ID : MRU_ 431681 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

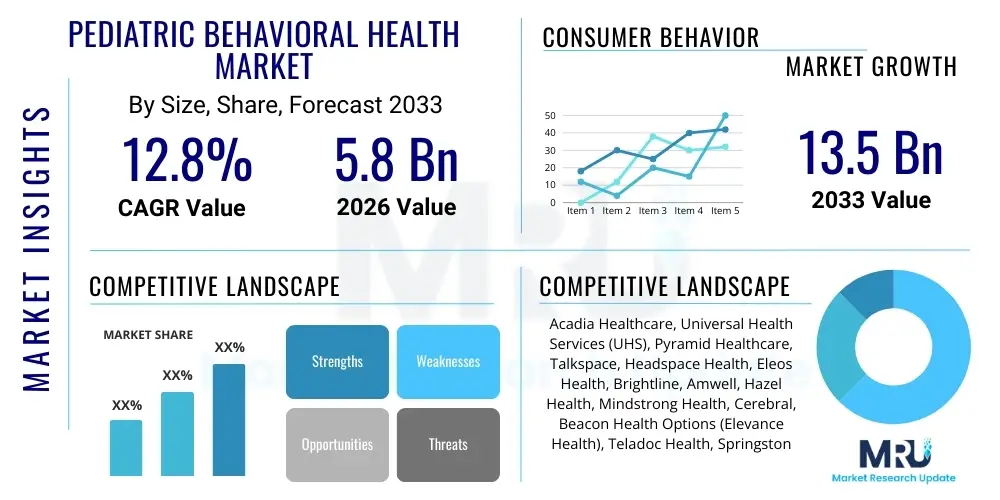

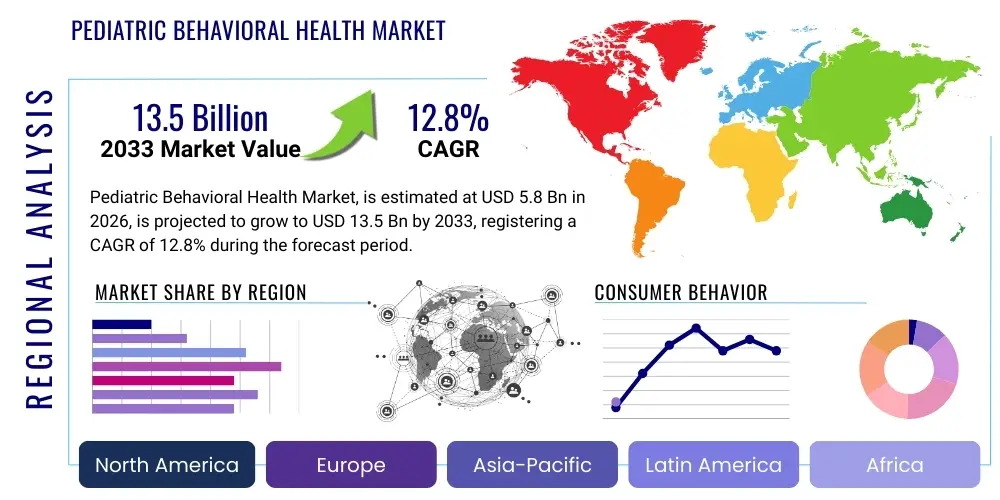

The Pediatric Behavioral Health Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2026 and 2033. The market is estimated at USD 5.8 Billion in 2026 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033. This significant expansion is driven by the increasing global prevalence of developmental, emotional, and behavioral disorders in minors, coupled with enhanced public awareness and improved diagnostic capabilities, shifting the approach from reactive care to proactive intervention and prevention strategies across developed and emerging economies.

The Pediatric Behavioral Health Market encompasses a broad range of services, therapeutic modalities, and supporting technologies aimed at diagnosing, treating, and managing mental, emotional, and behavioral disorders in children and adolescents, typically defined as individuals under the age of 18. This market addresses conditions such as Attention-Deficit/Hyperactivity Disorder (ADHD), Autism Spectrum Disorder (ASD), mood disorders (including anxiety and depression), eating disorders, and substance use issues. The core products and services within this domain include psychiatric consultation, various psychotherapies (Cognitive Behavioral Therapy, Dialectical Behavior Therapy, play therapy), pharmacological interventions, and increasingly, digital health platforms, including telepsychiatry and mobile therapeutic applications. The complexity of treating this population requires highly specialized practitioners and coordinated care models involving schools, families, and primary care providers.

Major applications of pediatric behavioral health interventions are focused on early detection and prevention, aiming to mitigate the long-term impact of mental health challenges on academic performance, social integration, and overall well-being. The market is witnessing a profound shift toward integrated care models, where behavioral health services are seamlessly incorporated into primary care settings (known as collaborative care). This integration is crucial for addressing the existing access crisis, particularly in rural and underserved areas where specialized pediatric psychiatrists are scarce. Furthermore, the rising adoption of standardized screening tools in school systems and pediatric practices is a key driver, facilitating quicker referrals and reducing the duration of untreated illness, thereby improving clinical outcomes and overall market efficiency.

Driving factors for this market expansion include robust advocacy efforts leading to favorable regulatory reforms and increased insurance parity mandates, compelling commercial and government payers to cover behavioral health services at the same level as physical health services. Technological advancements, particularly in remote monitoring and digital therapeutics, offer scalable solutions to meet the overwhelming demand, overcoming geographical barriers and provider shortages. The COVID-19 pandemic served as a catalyst, significantly amplifying the recognition of pediatric mental health as a public health imperative, resulting in substantial public and private investments aimed at expanding the workforce capacity and developing innovative, culturally competent treatment pathways tailored specifically for minors.

The global Pediatric Behavioral Health Market is currently undergoing rapid transformation, characterized by significant innovation in service delivery and technology integration, moving away from traditional in-office, episodic care toward continuous, digitally-enabled, and preventative frameworks. Key business trends indicate a strong move towards consolidation among specialized providers and technology developers, aimed at creating comprehensive, vertically integrated platforms that can manage the entire patient journey—from screening and diagnosis to long-term therapy and medication management. Investment remains robust in startups focused on validated digital therapeutics (DTx) designed specifically for pediatric populations, targeting conditions like anxiety and depression through interactive, gamified formats. Payers are increasingly shifting payment models from fee-for-service to value-based care arrangements, incentivizing providers to demonstrate measurable improvements in clinical outcomes and resource utilization.

Regional trends reveal that North America, particularly the United States, maintains market dominance due to high healthcare expenditure, established reimbursement policies, and a greater awareness infrastructure, but it also grapples with the most severe provider shortage challenges, fueling the adoption of telehealth. Europe follows, driven by strong public healthcare systems integrating mental health initiatives, particularly in Scandinavia and the UK, focusing heavily on school-based mental health programs and early intervention. The Asia Pacific (APAC) region is poised for the highest growth trajectory, spurred by rapidly increasing middle-class populations, evolving social attitudes towards mental health, and significant governmental investment in child development programs, although regulatory harmonization and cultural stigmas remain considerable hurdles to full market penetration.

Segment trends underscore the supremacy of the therapeutic services segment, which includes psychotherapy and counseling, primarily delivered through outpatient settings, but this is rapidly being challenged by the accelerating growth of the telepsychiatry and digital health sub-segments. By disorder type, the Autism Spectrum Disorder (ASD) segment continues to hold a substantial market share, necessitating highly specialized, long-term intervention programs, while the anxiety and depression segments are expanding the fastest, driven by pandemic-related stress and heightened diagnoses rates among adolescents. Technology solutions that offer scalable, evidence-based interventions suitable for diverse socioeconomic backgrounds and settings are expected to capture the largest share of new market investment over the forecast period.

Common user inquiries regarding the influence of Artificial Intelligence (AI) on the Pediatric Behavioral Health Market center predominantly on its capacity to enhance diagnostic accuracy, personalize treatment protocols, and address ethical concerns related to data privacy and bias in vulnerable populations. Users frequently ask about the reliability of AI-driven symptom trackers and mood monitors, the efficacy of machine learning in predicting risk for severe conditions (like suicidality or psychosis) in early life, and the role of Natural Language Processing (NLP) in analyzing therapeutic sessions to improve provider supervision and outcome measurement. A key theme revolves around whether AI tools can mitigate the severe shortage of specialized pediatric mental health professionals without compromising the human element critical to therapeutic rapport, highlighting a critical tension between automation efficiency and clinical necessity.

The market trajectory is shaped by powerful driving forces rooted in rising prevalence and regulatory support, tempered by significant restraints concerning workforce capacity and fragmentation, yet balanced by enormous technological opportunities. Key drivers include the overwhelming global increase in pediatric mental health conditions and substantial legislative changes mandating insurance parity and expanding access. However, growth is severely constrained by the chronic shortage of fellowship-trained pediatric psychiatrists and licensed clinical social workers, coupled with complex regulatory hurdles surrounding interstate licensing and telehealth provision across different jurisdictions. Opportunities are abundant in the domains of digital therapeutic development, integrating behavioral health into educational systems, and leveraging AI for predictive analytics, promising scalable and cost-effective solutions to address current access deficits. The primary impact force remains the societal prioritization of early intervention, moving the focus upstream from crisis management to preventative mental wellness, which fundamentally redefines the structure of service delivery and investment.

The Pediatric Behavioral Health Market is segmented across several critical dimensions, allowing for granular analysis of patient needs and market dynamics, including segmentations by disorder type, service type, delivery channel, and end-user. The segmentation by disorder type, encompassing high-volume conditions like ADHD and specialized areas like Eating Disorders, dictates the specialization of providers and the required technological tools. Service types distinguish between therapeutic, pharmacological, and support services, reflecting the multidisciplinary nature of treatment. The delivery channel segmentation, spanning inpatient, outpatient, and increasingly dominant home-based care (via telehealth), highlights the crucial shift in accessibility models. This multi-faceted segmentation structure is essential for stakeholders, from policymakers to commercial providers, in accurately allocating resources, developing targeted products, and optimizing patient pathways to ensure comprehensive care coverage across the diverse pediatric population.

The value chain for pediatric behavioral health is complex, starting with extensive upstream activities focused on research, curriculum development, and specialized workforce training, primarily driven by academic medical centers and professional associations. Upstream activities involve pharmaceutical research for psychotropic medications tailored for children, and the rigorous development and validation of digital therapeutic software and diagnostic tools. The highly regulated nature of pediatric care mandates extensive clinical trials and validation processes, significantly impacting the initial cost and time-to-market for new interventions. Key upstream stakeholders include specialized university departments, pharmaceutical companies, and health technology developers focused on evidence-based pediatric protocols and safety profiles.

The middle segment of the value chain is dominated by the delivery of services, involving specialized pediatric behavioral health centers, general hospitals, and an increasingly diversified network of community-based and virtual care providers. This segment focuses on patient acquisition, screening, diagnosis, and the implementation of multi-modal treatment plans (combining therapy, medication, and family support). Distribution channels are transitioning rapidly; while traditional delivery relies on direct patient interaction in clinical settings, the rise of telehealth platforms (indirect channel) and school-based integrated services (direct and indirect partnership channels) has decentralized access. Managed care organizations and government payers exert significant influence here, determining coverage parameters, provider networks, and reimbursement rates, which directly impact service availability and financial viability for clinicians.

Downstream activities involve continuous patient monitoring, outcomes assessment, long-term maintenance, and family engagement. This segment heavily relies on digital tools, remote monitoring devices, and robust electronic health records (EHRs) capable of securely tracking longitudinal patient data and coordinating care across various providers (pediatrician, school counselor, therapist, psychiatrist). Direct channels are maintained through ongoing patient-provider relationships, while indirect channels include educational resources, support groups, and peer coaching platforms provided by non-profits or tech companies. Ensuring the continuity of care and transitioning adolescents into adult mental health services constitute critical and often challenging final steps in the value chain, requiring standardized protocols and interoperable systems across different healthcare settings.

The primary end-users and buyers in the Pediatric Behavioral Health Market are highly diversified, extending far beyond the immediate patient and their families to include large institutional purchasers and government entities responsible for public welfare and education. Families and caregivers represent the direct consumers, often funding care through out-of-pocket payments or insurance co-pays, seeking specialized expertise and accessible services that fit into their daily schedules. However, institutional buyers, such as managed care organizations (MCOs) and private health insurance companies, act as crucial financial intermediaries, dictating the scope of covered services, preferred provider networks, and the economic viability of new therapeutic approaches, especially digital health solutions that promise cost efficiencies and scalability.

A rapidly growing customer segment comprises public sector entities, including state and federal governments, local school districts, and child protective service agencies. School systems are increasingly becoming essential points of care delivery, purchasing bundled services, training, and technology platforms to support student mental wellness mandates. These entities prioritize evidence-based programs that demonstrate effectiveness in large cohorts, focusing on prevention and early intervention models to reduce long-term societal costs associated with untreated mental illness. Furthermore, major academic medical centers and specialized children's hospitals are key customers for advanced technologies and specialized clinical training programs, as they often serve as regional hubs for the most complex pediatric behavioral cases, requiring state-of-the-art diagnostic and treatment modalities.

Finally, primary care physicians (PCPs) and general pediatricians represent a significant, though indirect, customer base. While not purchasing the end-service directly, they are the main referral sources and often the first point of contact for families seeking help. PCPs are increasingly adopting integrated behavioral health models, making them key customers for consultation services, standardized screening tools, and training programs designed to enhance their capacity to manage mild-to-moderate behavioral health issues in-house. Therefore, market penetration strategy often involves enabling PCPs with the necessary resources to confidently screen, stabilize, and efficiently refer complex cases to specialized behavioral health providers, thereby expanding the overall market reach and improving patient outcomes through collaborative care structures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Acadia Healthcare, Universal Health Services (UHS), Pyramid Healthcare, Talkspace, Headspace Health, Eleos Health, Brightline, Amwell, Hazel Health, Mindstrong Health, Cerebral, Beacon Health Options (Elevance Health), Teladoc Health, Springstone, Rogers Behavioral Health, Newport Healthcare, The Key Program, RethinkCare, Woebot Health, Akili Interactive Labs |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape within the Pediatric Behavioral Health Market is rapidly evolving, driven by the imperative to increase accessibility, enhance engagement, and improve data-driven outcomes. Telehealth platforms remain foundational, enabling synchronous and asynchronous virtual therapy and psychiatric consultations, thereby overcoming geographical limitations and reducing the logistical burden on families. Advanced teletherapy solutions often incorporate specialized features such as secure, child-friendly interfaces, integrated parental portals, and tools for real-time observation of behavioral cues. Beyond basic video conferencing, the current technology focus is shifting toward integrated ecosystem solutions that combine scheduling, billing, clinical documentation, and measurement-based care capabilities, ensuring seamless operations for providers and consistent data collection for researchers and payers.

Digital Therapeutics (DTx) represent the cutting edge of technological adoption, offering clinically validated, software-driven interventions designed to treat specific conditions. For the pediatric demographic, this often takes the form of highly engaging, gamified applications (e.g., Akili Interactive's EndeavorRx for ADHD) that are approved by regulatory bodies like the FDA. These applications provide prescribed treatment delivered directly through a digital medium, often complementing traditional psychotherapy or pharmacological regimens. Furthermore, the integration of ambient AI and machine learning algorithms is transforming diagnostic processes and risk stratification. AI tools analyze behavioral patterns, language complexity, and physiological data collected via wearable devices or smartphone interactions to provide objective insights that augment, rather than replace, clinical judgment, leading to earlier, more precise interventions.

Emerging technologies like Virtual Reality (VR) and Augmented Reality (AR) are gaining traction, particularly in exposure therapy for anxiety, phobias, and social skills training for children with Autism Spectrum Disorder (ASD). VR environments allow children to practice coping mechanisms in controlled, immersive settings that can be customized to their specific developmental level and therapeutic goals, offering an element of play that increases engagement and reduces therapeutic resistance. The convergence of these technologies—AI for insights, VR/AR for engagement, and Telehealth for delivery—is creating a robust technological infrastructure aimed at scaling evidence-based treatments and making high-quality pediatric behavioral care more palatable, effective, and accessible to a generation that is natively digital.

North America, led by the United States and Canada, currently holds the dominant share of the Pediatric Behavioral Health Market, largely attributable to superior healthcare expenditure, extensive insurance coverage, and high public awareness campaigns driven by robust private sector investment and strong advocacy organizations. The U.S. market is characterized by a fragmented but highly innovative landscape, where federal mandates (such as the Mental Health Parity and Addiction Equity Act) drive market expansion and ensure better reimbursement for services, particularly for telehealth. However, this region also faces the most pronounced challenge regarding the shortage of specialized pediatric practitioners, accelerating the demand and adoption for scalable digital health solutions and collaborative care models that integrate behavioral specialists into primary care settings for efficient resource utilization.

Europe represents a mature market, heavily influenced by state-funded healthcare systems that prioritize population health and preventative interventions. Countries such as the United Kingdom (NHS), Germany, and the Nordic nations have established comprehensive school-based mental health programs and publicly financed child and adolescent mental health services (CAMHS). The focus in Europe is on creating structured pathways from primary care to specialized services, with a strong regulatory emphasis on data security (GDPR compliance) impacting the implementation of cross-border digital health solutions. While growth rates are steady, they are generally lower than in North America due to the centralized nature of service provision and slower adoption of purely commercial digital therapeutics compared to publicly funded, evidence-based integration projects.

The Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR during the forecast period. This rapid growth is fueled by increasing urbanization, rising disposable incomes, and, critically, a noticeable shift away from traditional cultural stigmas surrounding mental illness, particularly among younger, highly educated populations in countries like China, India, and Australia. Governments across APAC are recognizing the economic burden of untreated mental health issues and are consequently increasing public spending on child welfare and health infrastructure. This region presents significant opportunities for low-cost, mobile-first therapeutic solutions and culturally adapted digital content, yet market penetration is complex due to highly disparate regulatory environments and the immense challenge of building a trained, specialized workforce at the necessary scale.

The foremost driver is the rising global prevalence and diagnosis rates of mental health conditions such as anxiety, depression, and ADHD among children and adolescents, coupled with increased parental awareness and significant improvements in legislative support for mental health insurance parity.

Telehealth is fundamentally restructuring access by allowing remote psychiatric consultation and therapy, effectively mitigating geographical barriers and reducing wait times, which is essential given the critical nationwide shortage of specialized pediatric practitioners.

Historically, the Autism Spectrum Disorder (ASD) segment commands a significant share due to the required intensity and long-term nature of intervention and support services; however, the anxiety and depression segments are exhibiting the fastest growth rates.

The critical restraints include the severe and persistent workforce shortage of specialized pediatric psychiatrists and licensed clinical social workers, compounded by regulatory complexity surrounding state licensing and persistent societal stigma in many regions.

DTx provides evidence-based, software-driven interventions, often gamified for pediatric engagement, serving as prescribed treatments that can supplement traditional therapy and medication, enhancing adherence and providing scalable solutions for widespread conditions like ADHD and anxiety.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.