ID : MRU_ 435524 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

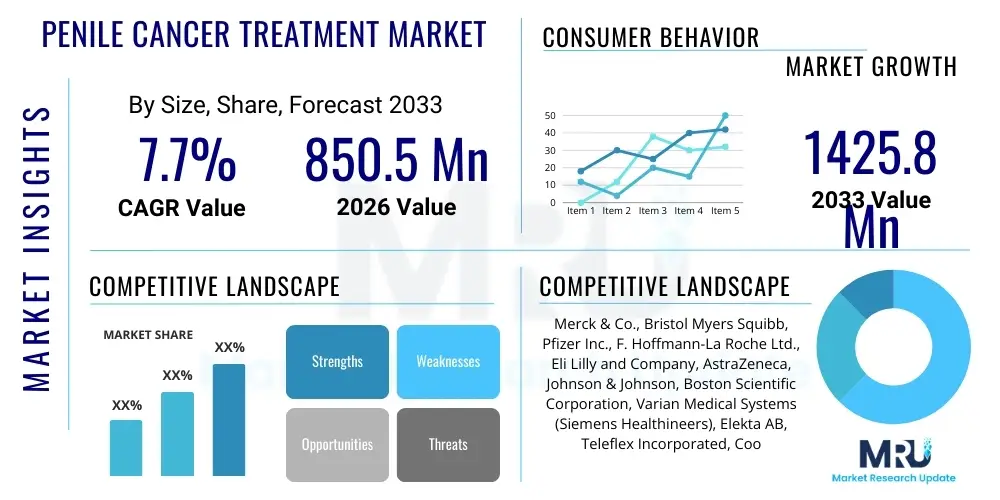

The Penile Cancer Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.7% between 2026 and 2033. The market is estimated at USD 850.5 Million in 2026 and is projected to reach USD 1425.8 Million by the end of the forecast period in 2033.

The Penile Cancer Treatment Market encompasses a range of therapeutic interventions designed to manage, treat, and cure malignant tumors originating in the penile tissue. While penile cancer is considered rare in Western nations, its prevalence is notably higher in certain regions of South America, Africa, and Asia, driving the necessity for specialized treatment protocols and innovative pharmaceutical and medical device solutions. The treatment modalities span from minimally invasive surgical techniques, such as laser ablation and Mohs surgery, to systemic treatments including chemotherapy, radiation therapy, and increasingly, targeted therapy and immunotherapy. The primary objective within this market is not only to eradicate the disease but also to preserve organ function and minimize psychological and physical morbidity, which significantly influences the adoption rate of advanced, organ-sparing techniques over traditional methods like total penectomy.

Product innovation in this domain is highly focused on optimizing patient outcomes through multimodal approaches. For instance, advancements in localized radiation delivery, such as brachytherapy, offer high efficacy while significantly reducing collateral damage to adjacent healthy tissue. Furthermore, the pharmaceutical pipeline is showing promising developments, particularly in utilizing immune checkpoint inhibitors (e.g., PD-1/PD-L1 inhibitors) for patients with advanced or recurrent metastatic disease, where conventional chemotherapy has limited success. The effectiveness of these new drugs is reshaping standard clinical guidelines, positioning systemic treatments as increasingly viable options for advanced stages, which historically relied heavily on aggressive surgery. Key market applications include treating carcinoma in situ (CIS), localized squamous cell carcinoma (SCC), and highly metastatic penile cancers.

The market is currently being driven by several macro factors, including greater global awareness leading to earlier diagnosis, improved screening programs in high-risk populations, and significant investment in oncological research focused on rare cancers. Earlier diagnosis drastically increases the success rate of curative treatments, favoring organ-sparing surgery and localized therapy. Moreover, improvements in healthcare infrastructure, particularly in developing economies, are facilitating access to sophisticated treatment modalities, previously confined to established markets. The main benefits derived from market growth include enhanced patient survival rates, improved quality of life post-treatment, and the development of less morbid treatment options, addressing the severe psychological burden associated with this cancer type. Driving factors also include technological integration, such as robotic-assisted surgery, which offers greater precision during complex surgical procedures.

The Penile Cancer Treatment Market exhibits robust growth, primarily propelled by the shift toward minimally invasive and organ-preserving surgical techniques, coupled with the introduction of novel systemic therapies tailored for advanced stages. Business trends indicate a strong focus on strategic collaborations between pharmaceutical companies and specialized oncological centers to expedite clinical trials for rare disease indications. Furthermore, there is a discernible trend among device manufacturers to miniaturize brachytherapy applicators and enhance imaging guidance systems for radiation delivery, increasing the precision and accessibility of these treatments globally. The economic impact of treating rare cancers, often requiring personalized or complex care pathways, also drives healthcare providers toward value-based reimbursement models that favor high-efficacy, low-morbidity solutions, influencing purchasing decisions across hospital networks and specialized cancer institutes.

Regional trends reveal that North America and Europe maintain dominance in terms of technology adoption and expenditure on cutting-edge pharmaceuticals, benefiting from well-established oncology pipelines and favorable reimbursement policies for advanced treatments. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This rapid expansion in APAC is attributable to a high baseline incidence rate of penile cancer in several regional countries, coupled with substantial improvements in healthcare access and increasing patient willingness to seek specialized treatment rather than relying on palliative care. Latin America and the Middle East also show burgeoning potential, driven by rising health expenditures and government initiatives aimed at modernizing oncology care services, particularly through partnerships that bring Western diagnostic and therapeutic platforms to local markets.

Segmentation trends highlight that surgical treatment modalities, specifically organ-sparing procedures, currently hold the largest market share due to their proven efficacy in early-stage disease. However, the systemic therapy segment, encompassing chemotherapy, targeted therapy, and immunotherapy, is anticipated to experience the fastest growth rate. This rapid growth is fueled by the success of immune checkpoint inhibitors in refractory or metastatic cases, offering hope where traditional cytotoxic agents have failed. Within the drug class segment, the increasing use of epidermal growth factor receptor (EGFR) inhibitors and other biologically targeted agents signals a move away from generalized cytotoxic chemotherapy towards personalized molecular approaches, optimizing treatment efficacy while minimizing systemic toxicity across various demographic groups.

Users frequently inquire about how Artificial Intelligence (AI) can overcome the challenges associated with the rarity and highly heterogeneous nature of penile cancer, particularly concerning diagnostic accuracy and treatment planning. Key concerns revolve around leveraging machine learning for improved risk stratification, enhancing the precision of radiation planning, and personalizing systemic treatment regimens based on limited patient data sets. Users also express interest in AI’s role in automating image analysis for earlier detection of pre-cancerous lesions or small primary tumors that might be missed by the human eye. The central expectation is that AI will standardize and optimize diagnostic pathways, providing reproducible, high-confidence results across varied clinical settings, thereby mitigating diagnostic delays common in rare cancers and improving overall patient management pathways.

The implementation of AI algorithms is poised to significantly transform the pathological and radiological assessment of penile cancer. For pathological analysis, deep learning models can be trained on vast digital slide archives to accurately grade tumors and identify key molecular markers relevant for prognosis and treatment selection, surpassing the variability inherent in human interpretation. In the radiological domain, AI-powered image segmentation tools are crucial for defining tumor boundaries and critical organ structures during complex brachytherapy or external beam radiation planning. This precision minimizes the radiation dose to surrounding healthy tissues like the urethra and glans, substantially reducing acute and late-term toxicities, which is a critical consideration in preserving patient quality of life after therapy.

Furthermore, AI is expected to revolutionize clinical trial design and patient recruitment, especially relevant for rare diseases like penile cancer where patient pools are small and geographically dispersed. Predictive analytics can identify potential candidates for novel drug trials based on genetic and clinical profiles, accelerating the translation of innovative treatments from bench to bedside. AI also supports the development of personalized predictive models that forecast a patient’s response to neoadjuvant chemotherapy or radiation, allowing clinicians to adjust therapeutic intensity proactively. This level of customization ensures that patients receive the most effective regimen tailored to their unique disease characteristics, moving the market closer to true precision oncology practices and potentially improving treatment efficacy margins.

The dynamics of the Penile Cancer Treatment Market are significantly shaped by a complex interplay of drivers (D), restraints (R), and opportunities (O), which collectively define the impact forces. A primary driver is the increasing efficacy and adoption of organ-sparing surgeries, responding directly to patient demand for improved post-treatment quality of life and reduced morbidity associated with radical procedures. Coupled with this, substantial progress in understanding the molecular pathology of penile cancer, specifically the role of Human Papillomavirus (HPV) infection, drives targeted therapy development. Conversely, the market faces constraints primarily due to the disease's low incidence rate in major developed markets, resulting in less research funding and fewer dedicated clinical trials compared to common cancers, leading to slower FDA/EMA approvals for new agents and limiting the commercial scalability of specialized products. However, a significant opportunity lies in expanding treatment access and awareness in high-incidence regions, such as parts of Africa and Southeast Asia, which are currently underserved but represent massive latent patient pools.

The impact forces generated by these DRO factors suggest a strategic market trajectory centered on technological niche specialization. The high investment required for complex surgical devices (like robotic platforms) and highly specialized radiation units acts as a restraint in resource-limited settings, while simultaneously being a powerful driver in affluent nations. Furthermore, regulatory hurdles unique to rare or orphan diseases can prolong market entry for novel pharmaceuticals. Nevertheless, the growing prevalence of HPV vaccination programs globally, while acting as a long-term preventative measure that might eventually reduce incidence, creates an immediate opportunity for diagnostic companies focused on HPV-related tumor markers and screening technologies. The lack of standardized clinical guidelines in some emerging markets also presents an opportunity for global oncology organizations to establish best practice protocols, driving the procurement of associated technologies and drugs.

Overall, the market is moderately competitive but highly specialized. The critical impact force stems from the balance between curative intent and preservation of sexual and urinary function. Any technological advancement that shifts this balance in favor of preservation (e.g., highly focused thermal ablation, proton therapy) rapidly gains market traction. The reluctance of patients to seek early medical attention due to stigma associated with the disease continues to be a profound restraint, leading to diagnosis at advanced stages where treatment options are limited and more invasive, thus hindering the efficacy gains achieved by early-stage treatments. Therefore, successful market penetration relies heavily on manufacturers and healthcare providers investing in awareness campaigns aimed at early identification and reducing associated social stigmas across various cultural landscapes.

The Penile Cancer Treatment Market is meticulously segmented across various dimensions, including Treatment Modality, Drug Class, Stage of Disease, and Distribution Channel. This granular analysis is crucial for stakeholders to identify specific growth pockets and tailor their R&D and commercial strategies. The dominance of surgical treatment reflects the curative intent associated with localized disease, necessitating high-precision instruments and advanced imaging technologies. However, the rapidly evolving landscape of systemic therapy indicates a major future shift towards pharmacological management, especially as biomarker identification becomes more standardized. Understanding the relative growth rates across these segments, particularly the uptake of biologics over conventional cytotoxic drugs, provides deep insight into physician preference and clinical outcome prioritization within oncology practices globally.

Segmentation by stage of disease is highly impactful, as localized (Stage I and II) disease primarily drives the demand for localized therapies (surgery, radiotherapy), while advanced (Stage III and IV) disease predominantly fuels the systemic therapy market. The substantial morbidity associated with Stage III/IV disease necessitates aggressive combination therapies, driving the adoption of novel drug combinations and complex delivery systems. Furthermore, geographical variations in the presentation stage of penile cancer (e.g., later presentation in developing nations versus earlier detection in highly screened populations) directly influence the relative market size of the respective segmentation categories within those regions, requiring a geographically sensitive marketing strategy.

The segmentation by distribution channel is characterized by the dominance of hospital pharmacies and retail pharmacies, reflecting where treatment is administered. Highly specialized treatments like brachytherapy or complex chemotherapeutic regimens are exclusively handled within hospital settings or specialized cancer centers, driving significant revenue through direct sales to institutional buyers. Conversely, oral chemotherapy agents or supportive care medications prescribed for home use pass through retail pharmacy channels. Analyzing the shift in power between these channels, particularly the increasing role of specialized oncology centers for complex treatment delivery, helps in optimizing supply chain logistics and inventory management for high-cost, low-volume treatments.

The value chain for the Penile Cancer Treatment Market begins with upstream activities focused on research and development (R&D) and raw material sourcing. Upstream innovation is primarily driven by academic institutions, biotech firms, and large pharmaceutical companies specializing in oncology, focusing on identifying novel molecular targets, optimizing drug synthesis (for systemic treatments), and designing advanced medical devices (for surgery/radiotherapy). Since penile cancer is an orphan indication in many regions, R&D is highly collaborative, often involving government grants or philanthropic funding to offset the high risk associated with developing products for small patient populations. The sourcing of raw materials, particularly for complex biologic drugs and high-purity components required for medical implants (e.g., brachytherapy seeds), must adhere to stringent quality control standards dictated by regulatory bodies like the FDA and EMA.

The midstream phase involves manufacturing, product assembly, and stringent quality assurance. For systemic therapies, this involves drug formulation and sterile packaging. For medical devices, particularly those used in organ-sparing surgery and brachytherapy, precision manufacturing is paramount. The distribution channel analysis highlights the critical role of specialized logistics, given that many treatments (especially radiopharmaceuticals or specific biologics) require cold chain management and rapid delivery to oncology centers. Direct distribution models are often preferred for high-value, specialized equipment, allowing manufacturers to provide direct technical support and training to clinical staff, ensuring proper utilization and maintenance of complex technology platforms like robotic surgery systems or high-dose-rate brachytherapy machines.

Downstream activities center on the delivery of the treatment, including clinical administration, patient monitoring, and post-treatment care. Direct channels, primarily through specialized hospitals and cancer centers, dominate the administration of complex treatments (surgery, radiation, infusions). Indirect channels, involving retail and specialized pharmacies, handle outpatient prescriptions, particularly for oral chemotherapy agents or supportive medications. The value realization in the downstream phase is heavily reliant on reimbursement policies established by government payers (Medicare/Medicaid) and private insurers. Effective management of post-treatment complications and long-term follow-up care is essential, as patient outcomes influence the perceived value and future adoption of specific treatment modalities, completing the feedback loop back to R&D for continuous product improvement and optimization of treatment protocols.

The primary end-users and buyers in the Penile Cancer Treatment Market are large hospitals and multi-specialty healthcare systems, particularly those housing dedicated oncology departments and specialized cancer centers. These institutions represent the major purchasers of high-capital equipment such as advanced radiation therapy machines (e.g., Linear Accelerators, HDR Brachytherapy units), robotic surgical systems, and bulk quantities of high-cost systemic therapies, including novel immunotherapies and targeted agents. Since penile cancer treatment often requires a multidisciplinary team approach involving urologists, radiation oncologists, and medical oncologists, institutions capable of integrating these services are the key consumption centers, seeking comprehensive packages and training programs from vendors rather than isolated products.

Specialized oncology clinics and ambulatory surgical centers (ASCs) constitute the second significant customer base, especially for localized treatments and outpatient systemic therapy infusions. ASCs are increasingly adopting minimally invasive surgical techniques, positioning them as key buyers for laser ablation devices, electrosurgical units, and specific imaging technologies required for precise tumor visualization during localized procedures. These centers prioritize cost-effectiveness and efficiency, driving demand for products that facilitate rapid patient turnaround and lower overheads compared to large hospital stays, especially in environments where reimbursement favors outpatient treatment delivery models for suitable patients.

Governmental healthcare providers and national health services (like the NHS in the UK or centralized procurement agencies in developing nations) act as major institutional buyers, often negotiating large-volume contracts for standardized drug protocols and essential medical devices. Their purchasing decisions are highly sensitive to price, clinical guidelines, and population health priorities. Furthermore, clinical researchers and academic medical centers represent a niche but critical customer segment, consistently purchasing advanced diagnostic tools, experimental drugs, and specialized equipment necessary for conducting clinical trials and advancing the understanding of this rare disease. Their demand drives the early adoption of highly innovative, yet often expensive, treatment technologies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.5 Million |

| Market Forecast in 2033 | USD 1425.8 Million |

| Growth Rate | 7.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Merck & Co., Bristol Myers Squibb, Pfizer Inc., F. Hoffmann-La Roche Ltd., Eli Lilly and Company, AstraZeneca, Johnson & Johnson, Boston Scientific Corporation, Varian Medical Systems (Siemens Healthineers), Elekta AB, Teleflex Incorporated, Cook Medical, Olympus Corporation, GE Healthcare, Sun Pharmaceutical Industries Ltd., Cipla Limited, Spectrum Pharmaceuticals, Inc., Janssen Biotech, Inc., Takeda Pharmaceutical Company Limited, Bayer AG. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Penile Cancer Treatment Market is heavily influenced by the imperative to achieve oncological clearance while maximizing organ preservation and functional outcomes. A cornerstone technology is advanced radiation delivery systems, particularly High-Dose-Rate (HDR) Brachytherapy, which allows precise internal radiation administration directly to the tumor site. Modern HDR systems utilize complex planning software and miniaturized applicators designed for the penile anatomy, ensuring high conformality of the dose and steep dose fall-off to critical structures. Furthermore, external beam technologies like Intensity-Modulated Radiation Therapy (IMRT) and Volumetric Modulated Arc Therapy (VMAT), and increasingly Proton Therapy, are used to treat advanced regional disease (lymph nodes) with superior precision, sparing surrounding organs and reducing long-term treatment-related side effects, reflecting a broader trend towards highly precise non-surgical management techniques.

In the surgical domain, the adoption of robotic-assisted surgery systems (e.g., using the da Vinci platform) has been transformative, particularly for performing complex, minimally invasive inguinal lymphadenectomy (removal of lymph nodes). Traditional open lymphadenectomy is associated with high rates of morbidity, including lymphedema and wound complications. Robotic platforms provide surgeons with enhanced visualization (3D, magnified), tremor reduction, and articulated instrumentation, enabling precise dissection of the lymphovascular bundles and minimizing tissue trauma. This technological shift directly supports the market's focus on reduced invasiveness and faster recovery times, making robotic platforms a significant area of capital expenditure for leading specialized cancer centers globally, enhancing their appeal to both patients and skilled surgical staff.

Beyond surgery and radiation, molecular diagnostics and biomarker technologies represent a rapidly expanding technological segment. The increasing recognition of HPV-driven tumors necessitates sophisticated molecular testing platforms (e.g., PCR-based assays and Next-Generation Sequencing – NGS) to accurately determine the HPV status and identify actionable genomic alterations, such as mutations in tumor suppressor genes or activation of growth factor pathways (e.g., EGFR). These diagnostic advancements guide the selection of targeted therapies and immunotherapies, moving treatment protocols from empirical approaches to highly personalized regimens. The continuous integration of AI and machine learning tools into these diagnostic workflows further ensures standardized, high-throughput analysis, solidifying the trend toward precision oncology as the benchmark of advanced penile cancer care delivery.

Geographically, the Penile Cancer Treatment Market demonstrates varied dynamics influenced by incidence rates, healthcare expenditure, and regulatory landscapes. North America, driven by the United States, commands a significant market share, characterized by high adoption rates of premium-priced systemic therapies (especially immunotherapies) and specialized surgical technologies (robotic systems). The region benefits from robust R&D activity, favorable reimbursement policies for advanced oncological procedures, and highly concentrated specialized cancer centers that prioritize the latest treatment modalities, translating to rapid integration of clinical trial results into standard practice. Furthermore, the strong presence of major pharmaceutical and biotechnology companies fuels continuous product launches and market competition in this region.

Europe represents the second-largest market, with countries like Germany, France, and the UK leading in clinical research and established public health infrastructure. The European market shows a strong preference for localized treatments, particularly brachytherapy, due to established clinical expertise and centralized healthcare systems that often standardize care pathways. However, market access can be slower for novel drugs compared to the US, due to rigorous Health Technology Assessment (HTA) processes focused on demonstrating cost-effectiveness in addition to clinical benefit. The introduction of unified clinical guidelines across the European Union is expected to harmonize treatment protocols, potentially increasing the adoption of standardized advanced therapeutic options across member states.

The Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate during the forecast period. This accelerated growth is primarily attributed to high prevalence rates in several South Asian and Southeast Asian countries, coupled with rapidly expanding healthcare infrastructure and increased disposable income allowing patients to access specialized care. While awareness and early diagnosis remain challenges, significant government investment in cancer control programs and growing medical tourism focused on high-quality oncology care are driving the demand for both advanced surgical equipment and systemic treatments. Countries like China and India are emerging as critical markets due to their large patient pools and increasing adoption of Western treatment protocols and imported medical devices, making them crucial targets for global market expansion efforts.

The market is primarily driven by the increasing demand for organ-preserving treatment modalities, advancements in precision radiation therapy (like HDR Brachytherapy), and the successful integration of immune checkpoint inhibitors for metastatic and advanced disease. Additionally, rising global awareness leading to earlier diagnosis improves treatment outcomes, boosting demand for curative options.

Immunotherapy, particularly the use of PD-1/PD-L1 inhibitors, is becoming critically important in the treatment landscape, especially for patients with recurrent or metastatic penile squamous cell carcinoma where traditional chemotherapy has limited efficacy. These agents offer a new standard of care for advanced stages, driving the systemic therapy segment's rapid growth.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR). This acceleration is due to the high baseline incidence of penile cancer in several APAC countries, coupled with substantial improvements in healthcare infrastructure, increasing access to specialized oncological care, and greater patient affordability for advanced treatments.

Major restraints include the low prevalence of penile cancer in major developed economies, which results in limited dedicated research funding and slower clinical development cycles for new drugs. Furthermore, the societal stigma associated with the disease often leads to delayed diagnosis, limiting the applicability of highly effective early-stage treatments and increasing overall morbidity.

The key technological trend is the adoption of robotic-assisted surgery, particularly for complex procedures like inguinal lymphadenectomy. Robotic platforms offer enhanced precision, 3D visualization, and minimal invasiveness, significantly reducing post-operative complications such as lymphedema and wound infections compared to conventional open surgery, prioritizing functional recovery.

Advancements in molecular diagnostics, including high-fidelity HPV testing and NGS for genomic profiling, are crucial. Accurate staging and identification of molecular biomarkers allow clinicians to personalize treatment plans, favoring targeted therapy or immunotherapy over generalized chemotherapy for specific patient subsets, thereby improving response rates and minimizing systemic toxicity.

The Penile Cancer Treatment Market is projected to reach an estimated value of USD 1425.8 Million by the end of the forecast period in 2033, demonstrating a significant growth trajectory driven by technological adoption and expansion into high-prevalence geographies.

The Surgical Treatment Modality segment currently holds the largest market share. This dominance is attributed to the high efficacy of surgery, particularly organ-sparing techniques, as the primary curative intervention for localized (Stage I and II) disease, which accounts for a substantial proportion of diagnosed cases seeking treatment.

Brachytherapy, especially High-Dose-Rate (HDR) Brachytherapy, plays a central role as an organ-preserving radiation technique. It allows for the precise delivery of high radiation doses directly to the tumor while sparing surrounding critical structures, making it highly effective for localized tumors and offering a vital alternative to surgical amputation in carefully selected patients.

Personalized medicine is fundamentally reshaping systemic therapy by relying on advanced genomic and proteomic profiling to identify unique tumor characteristics. This approach enables the tailored use of drugs, such as EGFR inhibitors for specific genetic mutations, ensuring higher therapeutic impact and fewer off-target side effects compared to non-targeted cytotoxic agents, leading to better long-term survival rates.

Yes, widespread public health initiatives promoting HPV vaccination are a long-term factor expected to restrain the market growth by reducing the future incidence of HPV-associated penile cancers. However, in the near term, it drives demand for accurate HPV diagnostic testing technologies for existing cases and screening programs.

The primary concern for patients is preserving the functional integrity and aesthetic appearance of the organ post-treatment. This concern significantly influences treatment selection, driving high demand for less invasive, organ-sparing treatments over radical surgeries that can lead to severe physical and psychological trauma.

Clinical trials face challenges primarily due to the rarity of the disease, resulting in difficulty recruiting sufficient patient numbers for statistically robust studies. This often necessitates multi-center international collaborations and reliance on specialized orphan drug designation pathways to accelerate product development and regulatory approval processes.

Hospital pharmacies and specialized cancer centers represent the most critical distribution channel for specialized treatments. Procedures like brachytherapy, robotic surgery, and intravenous infusion of complex biologic drugs require the sophisticated infrastructure and expertise only available within these institutional settings, necessitating direct procurement from manufacturers.

AI’s impact is substantial, particularly in enhancing diagnostic precision through automated image analysis (radiology and pathology) and optimizing treatment planning, especially for radiation dosimetry. AI also assists in predictive modeling for patient outcomes, standardizing care pathways, and accelerating clinical research for this rare oncological condition.

In North America, favorable reimbursement policies, especially those covering specialized surgical procedures (like robotic lymphadenectomy) and high-cost novel systemic therapies (immunotherapies), significantly accelerate the adoption of advanced treatment modalities, making the US a key driver for market revenue and technological advancement.

Major systemic therapies include platinum-based cytotoxic chemotherapy (e.g., Cisplatin combinations), biologically targeted agents such as Epidermal Growth Factor Receptor (EGFR) inhibitors, and Immune Checkpoint Inhibitors (ICIs), which are increasingly used as salvage therapy or first-line treatment for advanced metastatic disease.

Early diagnosis is crucial because localized disease (Stage I/II) is highly amenable to curative, organ-sparing treatments (e.g., laser ablation or limited excision), yielding excellent prognosis and preserving function. Conversely, diagnosis at advanced stages often necessitates radical surgery and less effective systemic treatments, leading to high morbidity and mortality rates.

The Systemic Therapy segment, particularly driven by the Drug Class sub-segment of Immune Checkpoint Inhibitors and Targeted Agents, is anticipated to grow the fastest. This growth reflects ongoing clinical success in treating advanced cases and the shift towards biologically targeted molecular approaches over traditional chemotherapy.

Manufacturers face challenges in Europe due to rigorous Health Technology Assessments (HTA) conducted by individual nations. These assessments require extensive evidence not just of clinical efficacy, but also of cost-effectiveness compared to existing standard treatments, potentially delaying or limiting market access even after regulatory approval.

The current trend strongly favors organ-sparing surgery (OSS) over radical penectomy. Techniques such as wide local excision, glansectomy with reconstruction, and minimally invasive sentinel lymph node biopsy, often supported by advanced intraoperative imaging and robotic assistance, are utilized to maintain quality of life while ensuring adequate oncological margins.

Key technologies include advanced linear accelerators (LINACs) for IMRT/VMAT, High-Dose-Rate (HDR) brachytherapy units, robotic surgical systems (e.g., Da Vinci), and molecular diagnostic platforms (NGS, PCR) for biomarker identification and HPV status determination, all focused on precision and minimal invasiveness.

Large multi-specialty hospitals and highly specialized Comprehensive Cancer Centers are the primary end-users driving demand for capital equipment. These institutions purchase robotic systems, specialized radiation units, and high-throughput diagnostic laboratory equipment to support complex, multidisciplinary treatment pathways required for penile cancer care.

As an orphan disease, the rarity often permits manufacturers of novel therapeutics (especially biologics and immunotherapies) to command premium pricing due to the smaller target market and the high R&D costs associated with developing treatments for rare indications, often subsidized by favorable regulatory incentives.

The high growth forecast in APAC is underpinned by significant public and private investment in oncological care infrastructure, improving access to sophisticated treatments in historically underserved areas, increasing medical awareness campaigns, and a high baseline patient population driven by regional prevalence patterns of the disease.

The main advantage of proton therapy is its ability to deliver a highly conformal radiation dose with maximum precision, characterized by the Bragg peak phenomenon. This significantly reduces the exit dose to surrounding healthy tissues and critical organs, minimizing long-term side effects and morbidity compared to conventional photon-based radiation treatments.

R&D, the upstream activity, is characterized by intensive collaboration between small biotechs, large pharmaceutical entities, and academic research institutions. Focus is placed on identifying novel molecular targets and translating personalized medicine principles into clinical reality for this heterogeneous rare tumor type, often relying on global pooled data sets.

SLNB is vital as a staging procedure to accurately assess regional lymph node status without performing an unnecessary, high-morbidity full inguinal lymphadenectomy on all patients. Its increasing adoption, often guided by dynamic sentinel node mapping, drastically reduces operative morbidity while maintaining diagnostic accuracy for microscopic metastatic disease.

The Penile Cancer Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.7% during the forecast period spanning from 2026 to 2033, reflecting steady advancements in therapeutic modalities and expanding market reach.

Immune checkpoint inhibitors (ICIs), specifically PD-1/PD-L1 targeting agents, are rapidly gaining traction. They are incorporated into treatment guidelines for advanced or recurrent metastatic disease, offering improved durability of response and overall survival benefits compared to traditional salvage chemotherapy regimens.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.