ID : MRU_ 435782 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

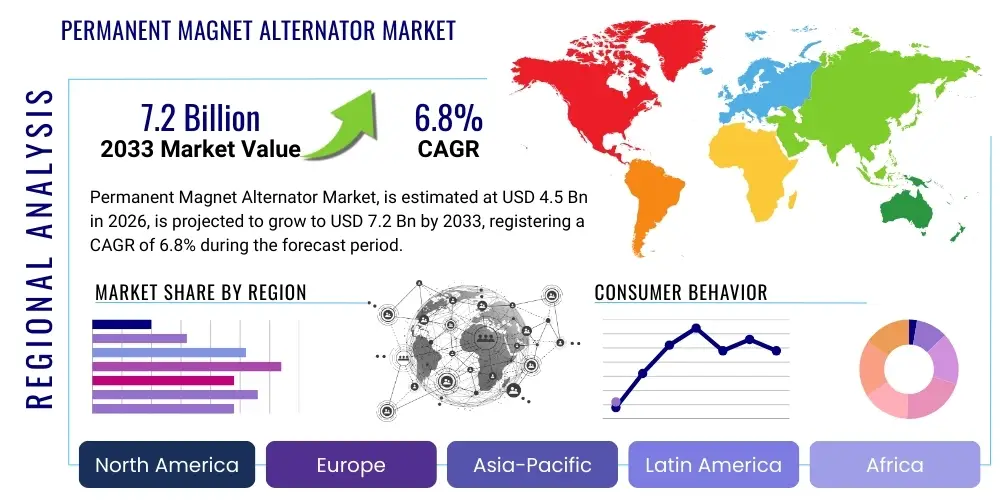

The Permanent Magnet Alternator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.2 Billion by the end of the forecast period in 2033.

The Permanent Magnet Alternator (PMA) Market encompasses highly efficient electrical machines utilizing permanent magnets instead of conventional field windings to generate electrical power. These devices are gaining significant traction across diverse industries due to their superior power density, dramatically reduced weight, and intrinsically enhanced reliability compared to traditional wound-rotor alternators. PMAs fundamentally eliminate ohmic losses associated with field excitation currents, leading to efficiency gains often exceeding 95% under optimal load conditions. This inherent efficiency makes them indispensable components in energy-conscious systems and mandates compliance with increasingly stringent global energy standards, thereby positioning them as a critical technology for the global energy transition.

Major applications of PMA technology span critical sectors including electric and hybrid vehicles (EVs/HEVs), where they frequently function as integrated starter-generators (ISGs) or high-efficiency charging systems, supporting advanced 48V mild-hybrid architectures crucial for fuel economy improvements. Simultaneously, the burgeoning renewable energy sector, particularly in direct-drive wind turbines, leverages PMAs for superior low-speed performance and minimal maintenance, essential for large-scale offshore installations. Furthermore, they are extensively utilized in specialized aerospace power generation systems, where weight reduction is paramount, and in industrial machinery requiring robust, variable speed operation and maximum power output from compact enclosures.

The market growth is fundamentally driven by the global imperative to reduce carbon emissions and drastically increase overall system energy efficiency, catalyzed by government mandates such as the EU Green Deal and rigorous regional fuel economy standards. The rapid, irreversible electrification of the transportation sector globally, coupled with massive capital investments in renewable energy infrastructure, specifically decentralized and offshore wind power, are primary catalysts. Technological advancements in magnetic materials, notably the refinement of high-coercivity Neodymium Iron Boron (NdFeB) for elevated operating temperatures, further enhances the performance characteristics of PMAs, enabling higher power output from smaller, lighter designs, directly fueling their wide-scale integration into next-generation power and mobility systems globally. The capability of PMAs to maintain high efficiency across a wide range of operational speeds provides a decisive performance advantage over traditional induction generators, securing their position in future sustainable energy frameworks.

The Permanent Magnet Alternator market is witnessing robust, high-CAGR growth, underpinned by significant global shifts in business focus towards decarbonization, advanced materials utilization, and energy system resilience. Key business trends include the vertical integration of specialized magnet manufacturing capabilities by leading PMA suppliers to mitigate supply chain risks associated with rare-earth elements. Furthermore, strategic partnerships between PMA manufacturers and power electronics firms are becoming commonplace, aimed at co-developing highly integrated, intelligent motor-generator systems. The intense R&D focus on Axial Flux PMA (AF-PMA) architecture is redefining product offerings, particularly targeting the compact and high-torque requirements of urban e-mobility platforms and drone technology, marking a clear pivot from traditional radial flux designs, while simultaneously addressing the need for cost-effective, high-volume production methodologies.

Regionally, the Asia Pacific (APAC) region solidifies its dominance, primarily due to the overwhelming scale of electric vehicle production capacity in East Asia and substantial government-backed initiatives for onshore and offshore wind installations, particularly in China and India. These governments have implemented crucial industrial policies favoring domestic manufacturing and rapid technology adoption. North America and Europe, while having a slightly smaller market share by volume, focus heavily on the high-specification, high-reliability segments, including aerospace power systems, high-performance luxury EVs, and specialized industrial applications where performance and durability outweigh cost constraints. These developed regions are also leading in the implementation of sophisticated smart grid technologies, which necessitate the efficient, responsive power generation capabilities inherent in PMAs, driving demand for intelligent, connected PMA solutions.

Segmentation analysis reveals the automotive sector, specifically the battery electric vehicle and mild-hybrid sub-segments, maintains the largest and fastest-growing application share, driven by aggressive volume targets set by OEMs worldwide and favorable consumer trends favoring electrified mobility. In terms of product type, while Radial Flux PMAs currently hold a substantial installed base, the Axial Flux PMA segment is unequivocally projected to register the highest Compound Annual Growth Rate (CAGR) over the forecast period, reflecting its architectural advantages in demanding, space-constrained, high-efficiency environments. This executive overview underscores a market defined by rapid innovation, increasing geopolitical awareness regarding material sourcing, and strong, diversified demand derived from global infrastructure transformation initiatives focused on superior energy utilization, alongside a fierce competitive landscape driven by patent portfolios and manufacturing scale.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Permanent Magnet Alternator (PMA) market frequently revolve around achieving unprecedented levels of efficiency and reliability through intelligent operational control and accelerated design processes. The core themes center on how sophisticated AI algorithms, specifically machine learning and deep learning, can be utilized to maximize the energy harvest efficiency from variable sources like turbulent wind flows or fluctuating vehicle load demands, pushing the effective operating envelope of the PMA beyond conventional control limits. Furthermore, there is strong user interest in leveraging AI to predict and mitigate critical failure modes, such as localized demagnetization resulting from transient thermal spikes or unforeseen electrical stress, ensuring asset longevity and reducing costly, unscheduled downtime, particularly in remote installations like deep-sea offshore platforms.

AI is fundamentally transforming the lifecycle management and operational efficiency of PMAs, transitioning systems from reactive diagnostics to proactive, high-precision predictive maintenance protocols. By integrating high-frequency sensor data—including detailed analysis of current waveforms, vibrational spectrums, acoustic emissions, and thermal gradients—advanced machine learning models can identify subtle, pre-failure signatures indicative of winding insulation degradation, inter-turn short circuits, or early bearing fatigue. This capability is exceptionally critical in high-capital investment areas like utility-scale offshore wind farms, where logistical costs for corrective maintenance are prohibitive. Deploying AI models leads directly to optimized maintenance scheduling, potentially extending mean time between failures (MTBF) by double-digit percentages and significantly lowering overall operational expenditure (OPEX) for asset owners, thereby maximizing the lifetime profitability of the asset.

Beyond operational deployment, AI-driven simulation and generative design optimization are radically accelerating the pace of innovation in PMA architecture and material selection. Generative design utilizes AI to explore a vast, multi-dimensional design space, generating thousands of novel rotor/stator configurations, optimizing coil geometry (e.g., hairpin vs. distributed windings), and selecting the optimal grade and placement of permanent magnets. These algorithms target complex, simultaneous objectives, such as minimizing total harmonic distortion (THD), eliminating cogging torque for smoother low-speed operation, and maximizing the specific power density without compromising thermal stability. This computational approach drastically reduces the reliance on costly physical prototyping iterations, thereby shortening the time-to-market for specialized, high-performance PMA designs tailored precisely for niche automotive or aerospace applications, providing a robust competitive advantage to technologically advanced manufacturers.

The Permanent Magnet Alternator market is fundamentally shaped by a formidable combination of technology drivers and regulatory opportunities, carefully balanced against significant material supply risks and complex manufacturing barriers. The dominant driver remains the global, systemic commitment to enhancing energy efficiency, encapsulated by aggressive government-led mandates promoting electrification across all mobility platforms (e.g., EU CO2 targets, China's New Energy Vehicle policies) and significant capital allocation towards robust, low-maintenance renewable energy infrastructure, such as utility-scale wind and micro-grid solutions. This regulatory environment creates a continuous, baseline demand for components, such as PMAs, that deliver intrinsically higher efficiency profiles than traditional inductive alternatives, driving compulsory industry-wide adoption across Tier 1 suppliers and OEMs.

A second major driver is the exponential growth trajectory of the Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) sectors globally. PMAs, functioning often as highly integrated motor-generators, are central to maximizing regenerative braking efficiency and ensuring optimal power management in advanced 48V mild-hybrid systems, providing the high torque and power density necessary for vehicle performance and range extension. This sustained high-volume demand provides the necessary economic scaling to drive down unit costs and accelerate technological refinement, further solidifying the PMA's technical dominance over conventional alternators in future automotive architectures. The parallel opportunities lie in the successful commercialization of advanced, rare-earth-free PMAs, such as those utilizing specialized composite magnets or advanced ferrite-based alternatives, which would effectively neutralize the critical geopolitical and price volatility risks associated with Neodymium and Dysprosium dependency, opening vast new cost-sensitive markets.

However, market expansion faces substantial restraints, primarily revolving around the highly concentrated global supply chain for key rare-earth elements. This dependency introduces significant risks concerning extreme price volatility, potential geopolitical instability, and material shortages, which directly impact the cost of production and margin stability for PMA manufacturers, forcing strategic inventory stockpiling and resource diversification. Furthermore, the high initial capital investment required for precision manufacturing, including specialized magnet handling, advanced winding techniques (like hairpin coils), and high-tolerance rotor balancing, along with the complexity of integrating advanced wide-bandgap (SiC/GaN) power electronics needed for optimal PMA control, acts as a substantial barrier to entry for smaller or less technologically mature firms seeking to enter the high-performance segments.

The prevailing impact forces acting on the PMA market demonstrate high internal competition driven by profound technological differentiation. Porter's Five Forces analysis highlights that the rivalry among existing competitors is intensifying, particularly between manufacturers specializing in established radial flux technology and newer entrants focusing exclusively on cutting-edge Axial Flux (AF-PMA) designs, each vying for crucial, multi-year automotive and aerospace OEM contracts. The threat of substitution is demonstrably low because conventional wound-field alternators cannot feasibly meet the stringent efficiency, weight reduction, and power density targets mandated by modern electrified applications. Conversely, the bargaining power of major buyers (such as large Automotive OEMs and Tier 1 wind turbine manufacturers) is exceptionally high, as they enforce rigorous quality standards, demand long-term price stability, and require guaranteed supply capacity under tight delivery schedules, placing substantial financial and operational pressure on PMA suppliers to innovate while maintaining aggressive cost controls.

The comprehensive Permanent Magnet Alternator market segmentation is critical for dissecting the diverse growth opportunities and technological preferences across various industrial sectors. This analysis categorizes the market based on intrinsic design characteristics (flux type), core material dependency (magnet type), power output capability, and targeted application environment. This structural breakdown allows market stakeholders to precisely measure segment saturation, identify white-space opportunities, and align their investment in R&D and manufacturing capacity with the most promising, high-growth sectors, particularly those demanding extreme efficiency and compactness, such as e-mobility and distributed power generation.

Segmentation by Type is foundational, distinguishing between Radial Flux, Axial Flux (AFPMAs), and emerging Transverse Flux designs. Radial Flux PMAs are mature, robust, and cost-effective for medium-to-high power industrial applications, characterized by easier cooling mechanisms and established supply chains. In contrast, Axial Flux designs, known for their thin, pancake profile and superior torque density, are rapidly gaining ground in e-mobility, directly challenging traditional architectures due to their inherent suitability for space-constrained vehicle integration. Analyzing segment preference here reflects a fundamental market shift towards lightweight, compact power solutions essential for optimizing vehicle performance metrics, including mass centralization and improved vehicle dynamics.

Further segmentation by Application highlights the crucial demand drivers. While utility-scale Wind Power generation demands the highest individual unit power ratings and focuses on maximum longevity (often employing thermally stable SmCo magnets), the Automotive segment demands massive volume, aggressive cost reduction, and superior power-to-weight performance (primarily utilizing NdFeB magnets). This differentiation necessitates distinct operational strategies, supply chain configurations, and technology focus for manufacturers targeting different segments, ranging from high-volume standardized components for mass markets to highly customized, low-volume, high-reliability products for niche sectors like aerospace and specialized defense contractors.

The Permanent Magnet Alternator value chain is highly specialized and begins with the extraction and processing of critical raw materials, a phase entirely dominated by the procurement of rare earth elements (REEs) such as Neodymium, Praseodymium, and Dysprosium. Upstream analysis reveals that the initial mining, refinement, and alloying process is geographically concentrated, primarily in East Asia, posing significant supply chain resilience challenges and requiring intense risk management strategies. Specialized magnetic material suppliers then transform these refined alloys into high-grade permanent magnets via complex sintering or bonding processes, demanding extreme precision to achieve the high magnetic flux density and necessary thermal stability for PMA performance. Control over this upstream supply—ensuring quality, consistent thermal characteristics, and stable material pricing—is a significant competitive differentiator for major integrated PMA manufacturers.

The core manufacturing and assembly phase constitutes the highest value-addition step, involving highly automated processes for core stamping, precision coil winding (increasingly utilizing advanced Hairpin winding techniques for high-performance automotive PMAs), and the critical, high-tolerance assembly of the fragile permanent magnets into the rotor structure. This stage relies heavily on proprietary intellectual property related to magnetic circuit optimization, advanced thermal management integration (e.g., sophisticated oil cooling jackets and optimized fluid dynamics), and the seamless integration of external sophisticated power electronics (inverters and controllers). Major PMA OEMs exert control here by maintaining proprietary high-speed manufacturing processes and achieving high-volume economies of scale necessary to meet stringent automotive price targets while maintaining exceptional quality standards required by aerospace clients.

Downstream distribution channels vary significantly based on the end-use market and the required service level. Direct sales channels are overwhelmingly dominant for large-volume customers, particularly global automotive OEMs and Tier 1 wind turbine developers, where long-term, multi-year contracts necessitate stringent quality checks, just-in-time logistics, highly responsive technical support, and comprehensive integrated service agreements covering the full product lifecycle. Indirect channels, utilizing specialized electrical distributors, system integrators, and value-added resellers, are more common for serving smaller industrial clients, the aftermarket replacement sector, and geographically diverse distributed generation projects. The final critical link is the system integration and commissioning phase, where specialized engineering firms ensure the PMA's electrical output is perfectly synchronized and precisely regulated by the associated power electronics to meet the complex dynamic operational requirements of the host vehicle or grid infrastructure, guaranteeing optimal system performance.

The primary customer base for Permanent Magnet Alternators consists of global Original Equipment Manufacturers (OEMs) who integrate these high-efficiency components directly into large-scale, performance-critical systems. The most substantial volume driver is the global automotive industry, particularly manufacturers committed to producing Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and advanced 48V mild-hybrid models across passenger and commercial vehicle segments. These customers demand PMAs designed for ultra-high efficiency, minimal acoustic noise, exceptional thermal stability under continuous high load, and robust design to withstand severe vehicular shock and vibration profiles, essential for maximizing battery range, optimizing fuel efficiency, and enhancing overall vehicle performance characteristics.

A second, extremely high-value customer segment is the utility-scale renewable energy sector, encompassing manufacturers of multi-megawatt wind turbines, especially those specializing in direct-drive technology for complex offshore installations. These clients prioritize maximum reliability, system longevity (lifespans often exceeding 25 years), and high component ruggedness to minimize costly maintenance interventions in remote, harsh marine environments. Their procurement strategies are highly risk-averse, focusing on established Tier 1 suppliers who can guarantee high availability, provide comprehensive extended warranties, and offer integrated services, driving demand for specialized materials like thermally stable Samarium Cobalt magnets to ensure long-term performance integrity.

Further strategic customers include major aerospace and defense prime contractors. This highly demanding niche requires PMAs that offer the absolute maximum power-to-weight and power-to-volume ratios for use in aircraft Auxiliary Power Units (APUs), critical electro-hydrostatic actuators (EHAs), and specialized military ground power systems. In this segment, unit cost is distinctly secondary to certified performance, adherence to rigorous military specifications, and guaranteed operational reliability under extreme thermal and pressure variations. Finally, the broader industrial and marine sectors, including manufacturers of high-efficiency compressors, pumps, specialized material handling equipment, railway traction systems, and electric propulsion units for commercial vessels, represent steady, long-term demand for medium-to-high power PMAs seeking operational longevity and significant long-term energy cost savings through superior efficiency ratings.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, General Electric Co., ABB Ltd., TMEIC (Toshiba Mitsubishi-Electric Industrial Systems Corporation), Nidec Corporation, ZF Friedrichshafen AG, Continental AG, Denso Corporation, Bosch Rexroth AG, Mitsubishi Electric Corporation, Vestas Wind Systems A/S, VEM Group, Magneti Marelli (Marelli), Marathon Electric, Vanner Inc., Advanced Magnetics Technology, Inc., Regal Beloit Corporation, Parker Hannifin Corp., WEG S.A., Brook Crompton. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape surrounding the Permanent Magnet Alternator market is defined by a fierce pursuit of material superiority and architectural innovation aimed at boosting specific power density and thermal robustness. A cornerstone of current R&D involves advanced magnetic material engineering, focusing intensively on enhancing the intrinsic coercivity of Neodymium Iron Boron (NdFeB) magnets, allowing them to retain strong magnetic flux even when operating at elevated temperatures (up to 200°C) without significant demagnetization. Efforts include utilizing grain boundary diffusion (GBD) techniques, often involving trace amounts of heavy rare-earth elements like Dysprosium, to improve thermal resistance while simultaneously minimizing the quantity of these costly materials. Parallel research streams are aggressively exploring rare-earth substitutes, such as sophisticated Manganese-Aluminum (MnAl) alloys and specialized nitride-based magnets, to de-risk the supply chain for future mass-market applications.

Architecturally, the market is witnessing a major transformation with the increasing prominence of Axial Flux Permanent Magnet Alternators (AFPMAs). These designs, characterized by flux lines parallel to the shaft, facilitate ultra-compact, disc-shaped motors and generators that are fundamentally suited for direct integration into electric propulsion systems (e.g., in-wheel motors or close-coupled hybrid systems). Technological advancements here focus on ironless or coreless stator designs to virtually eliminate parasitic core losses and cogging torque, thereby maximizing efficiency and reducing acoustic noise. However, this demands sophisticated mechanical engineering solutions, often incorporating advanced carbon composite materials, to provide the necessary structural support and cooling efficiency without introducing unwanted magnetic field distortions.

A third critical technological area is the integration of advanced manufacturing techniques and smart control systems. The rapid adoption of automated Hairpin winding technology, particularly in high-volume automotive PMAs, substantially increases the copper fill factor, reduces winding resistance, and significantly enhances the thermal pathway compared to traditional round wire windings, allowing for higher continuous current density. Furthermore, the convergence of PMAs with high-performance power electronics utilizing next-generation wide-bandgap semiconductors, namely Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, is crucial. These devices allow for significantly higher switching frequencies, leading to smaller, lighter converter packages and enabling more precise, high-speed control over the PMA's electrical output, which is essential for maximizing efficiency, minimizing torque ripple, and ensuring seamless integration into complex grid-tied renewable energy generation systems.

The Permanent Magnet Alternator market exhibits distinct regional dynamics heavily influenced by local industrial policy, infrastructure investment, and specific regulatory environments. Asia Pacific (APAC) remains the undisputed global leader in terms of market volume and manufacturing capacity. This dominance is intrinsically linked to the immense governmental push and consumer adoption of electric mobility in China, which serves as the largest single market for EV components globally, creating massive, sustained demand for cost-optimized, high-efficiency PMAs used in propulsion and auxiliary systems. Furthermore, APAC nations, particularly China and India, are undertaking the world's largest expansion of renewable energy capacity, especially onshore wind, driving substantial high-power PMA procurement and fostering a highly competitive local supply base.

Europe constitutes the most technologically advanced and value-driven market, focusing intensely on high-specification, premium PMA solutions. The region's market leadership is strongly anchored in its commitment to ambitious decarbonization targets, evidenced by significant investment in utility-scale offshore wind farms in the North Sea and Baltic Sea, which almost exclusively utilize highly reliable, multi-megawatt direct-drive PMAs to maximize energy yield. Furthermore, strict EU emissions standards (e.g., Euro 7) and the rapid adoption of 48V mild-hybrid technologies in European vehicle fleets drive demand for highly customized, quality-assured alternators. The emphasis in Europe is not only on peak system efficiency but also on sustainability and circular economy principles, leading to earlier adoption of resource-efficient manufacturing and highly specialized recycling programs for rare-earth materials, often mandated by regional regulation.

North America is characterized by robust and accelerating market growth, propelled by the massive domestic build-out of electric vehicle production capacity and significant federal government incentives aimed at accelerating clean energy adoption, such as the Inflation Reduction Act (IRA) and state-level renewable portfolio standards. The market here is highly segmented, with strong, non-negotiable demand emanating from the high-reliability aerospace and defense sectors, requiring specialized, often military-grade, lightweight PMAs for critical airborne systems. As large auto manufacturers shift production lines within the US, Canada, and Mexico toward full electrification, the requirement for localized, secure supply chains for high-volume automotive PMAs is becoming a primary investment driver, encouraging local component production, technological licensing agreements, and vertical integration to mitigate geopolitical risks associated with imports.

A PMA utilizes robust permanent magnets (often NdFeB or SmCo) mounted on the rotor to generate the required magnetic field, eliminating the need for complex field windings, brushes, and slip rings. This critical design advantage translates to significantly higher energy efficiency (less heat loss), superior power density, and vastly reduced maintenance costs, making PMAs essential for next-generation EVs and direct-drive wind turbines.

The primary constraint is the highly consolidated and volatile global supply chain for high-performance rare-earth elements (REEs), such as Neodymium and Dysprosium. These materials are critical for magnets used in high-power PMAs, and their price fluctuation and geopolitical supply risks introduce substantial uncertainty and manufacturing cost volatility for the entire industry.

The Automotive sector, particularly the surging global production of Battery Electric Vehicles (BEVs) and advanced 48V Mild-Hybrid Electric Vehicles (MHEVs), currently drives the largest volume of demand, utilizing PMAs for crucial integrated starter-generator (ISG) functions and high-efficiency traction systems.

Axial Flux PMAs (AFPMAs) feature magnetic flux running parallel to the axis of rotation, resulting in a unique, flat, and compact "pancake" design. This architecture provides an unparalleled combination of very high torque density and a superior power-to-volume ratio, making them ideally suited for integration into space-constrained vehicle applications like in-wheel motors or close-coupled transmission systems.

AI utilizes sophisticated machine learning algorithms and digital twin technology to enable high-precision predictive maintenance by analyzing complex sensor data (vibration and thermal profiles). This allows operators to accurately anticipate component failures and dynamically optimize the PMA’s control parameters to maximize energy conversion efficiency under real-time variable loads, significantly enhancing reliability and asset uptime.

In the utility-scale wind energy sector, PMAs are typically classified in the High Power rating segment (Above 50 kW). Direct-drive wind turbines, especially offshore models, commonly utilize PMAs capable of generating multi-megawatt outputs (e.g., 5 MW to 15 MW and beyond), requiring robust designs with superior thermal management and high component reliability.

Manufacturers are actively mitigating risk through two primary strategies: first, by investing heavily in R&D for rare-earth-free alternatives (like MnAl magnets) and advanced design architectures that reduce magnet volume; and second, by securing long-term strategic supply contracts, focusing on vertical integration into magnet processing, and developing efficient material recycling pathways to ensure supply resilience and cost control.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.