ID : MRU_ 433126 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

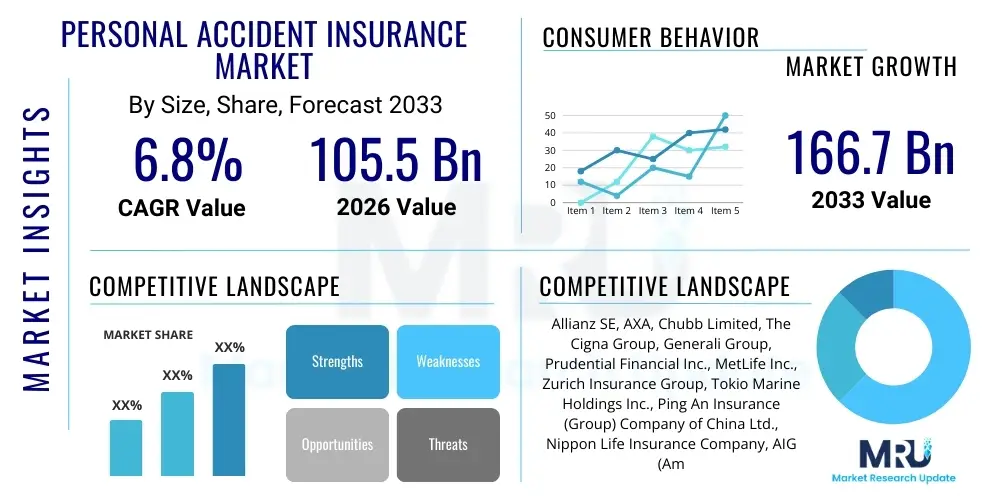

The Personal Accident Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $105.5 Billion in 2026 and is projected to reach $166.7 Billion by the end of the forecast period in 2033. This robust expansion is primarily fueled by rising global awareness regarding financial security in the event of unforeseen accidents, coupled with increasing disposable incomes in emerging economies, which allows greater penetration of voluntary insurance products. The market's valuation reflects a steady shift towards comprehensive coverage options, moving beyond basic death and disability benefits to include temporary disablement, critical illness riders, and specialized coverage for adventure sports or occupational hazards, thereby expanding the average premium per policyholder.

Market expansion is significantly underpinned by mandatory insurance regulations introduced by various governments, particularly concerning workplace safety and travel. Furthermore, the digitalization of the insurance distribution channel, emphasizing mobile applications and direct-to-consumer platforms, has streamlined the process of purchasing and managing policies, making personal accident insurance highly accessible even to segments previously underserved by traditional brokerage models. The development of micro-insurance schemes in high-growth regions like Asia Pacific also contributes substantially to the overall market size, catering to the large population base seeking affordable protection against accidental risks. Insurers are innovating by integrating wellness programs and preventive health benefits into accident policies, enhancing the perceived value proposition.

The transition toward personalized underwriting enabled by data analytics is refining pricing strategies, ensuring that premiums accurately reflect individual risk profiles. This approach attracts lower-risk individuals who might otherwise find traditional policies overly expensive, simultaneously allowing insurers to manage risk exposure more effectively. The increasing frequency and severity of natural disasters and road accidents globally necessitate greater individual financial resilience, pushing consumers towards securing specialized protection. Overall, the foundational driver remains the intrinsic human need for security against unexpected physical and economic shocks, cementing the long-term growth trajectory of this essential insurance sector.

The Personal Accident Insurance Market encompasses policies designed to provide financial compensation for the policyholder or their beneficiaries in the event of injuries, disability, or death resulting directly and solely from an accident. This essential insurance product serves as a crucial component of personal financial planning, offering a safety net that covers medical expenses, loss of income due to temporary or permanent disablement, and specific lump-sum payouts. Unlike standard health insurance which primarily covers illness-related medical costs, personal accident policies focus exclusively on accidental injuries, providing specific benefits regardless of any existing health coverage. The increasing volatility in employment stability and rising medical inflation have amplified the necessity for these specialized protection plans among global consumers.

The major applications of personal accident insurance span several crucial areas, including coverage for catastrophic injuries requiring long-term care, financial support during recovery from minor accidents that prevent work, and securing the financial future of dependents through death benefits. Key benefits include fixed payouts irrespective of actual medical costs incurred (often functioning as income replacement), worldwide coverage availability, and simplified underwriting processes that usually do not require extensive medical examinations. Furthermore, these policies often include riders for enhanced coverage such as ambulance charges, specific surgical costs, or educational grants for dependent children if the policyholder sustains permanent total disability or death. This versatility makes it highly appealing across diverse socio-economic strata.

Driving factors for market growth are multifaceted. Urbanization leading to increased traffic congestion and higher accident rates, coupled with greater participation in recreational and professional activities carrying inherent risks, necessitates comprehensive accident protection. Regulatory impetus in developing countries promoting financial inclusion and mandating basic accident coverage for employees or specific vehicle classes also spurs demand. Lastly, aggressive marketing and digital onboarding strategies employed by insurance carriers, leveraging comparative ease of purchase, significantly contribute to the market's expansive introduction into new demographic segments, making protection ubiquitous and instantaneous.

The Personal Accident Insurance Market is characterized by robust resilience and dynamic growth, driven largely by shifting consumer perceptions toward proactive risk management and accelerated digital transformation within the insurance industry. Key business trends indicate a strong move toward customization and modular policy design, allowing customers to tailor coverage limits and specific riders (e.g., fractured bone benefits, burns, adventure sports) according to their occupation and lifestyle. Furthermore, partnerships between insurers and digital ecosystem providers—such as fintech companies, e-commerce platforms, and health tech providers—are creating embedded insurance opportunities, integrating accident coverage seamlessly into the purchase journey of related products or services, thus maximizing penetration at the point of need. Regulatory standardization, particularly concerning claim settlements and disclosure, is enhancing market trustworthiness and consumer confidence globally.

Regionally, the Asia Pacific (APAC) market leads in terms of growth potential, fueled by massive population bases, improving economic prosperity, and relatively low historical insurance penetration rates, making it a critical focus area for global carriers. North America and Europe, while being mature markets, exhibit trends favoring sophisticated, high-value policies, often bundled with life or health insurance, emphasizing comprehensive disability benefits and long-term care riders. Specific regional regulatory frameworks, such as varying definitions of "permanent disability" across jurisdictions, mandate localized product differentiation. The rapid technological adoption in APAC, especially mobile-first distribution, allows for faster scalability compared to markets reliant on legacy distribution channels.

Segmentation trends highlight the increasing dominance of the permanent disability segment in terms of premium value, reflecting higher potential payouts and greater actuarial risk, leading to higher premiums. Distributionally, the agency channel still maintains relevance for complex high-net-worth policies, but the direct channel, facilitated by online aggregators and insurer portals, is rapidly gaining share due to its cost-efficiency and convenience for standard policies. The corporate segment, driven by mandatory employer-provided group personal accident policies, remains stable and provides a significant foundation for recurring revenues. Insurers are heavily investing in proprietary data analytics models to refine risk assessment within these diverse segments, optimizing both pricing and loss ratios efficiently.

User queries regarding AI's influence predominantly revolve around automation in claims processing, personalized pricing, and fraud detection capabilities. Consumers are keen to know if AI can simplify the often-complex claim filing process, ensuring faster and more transparent payouts. They also frequently question how AI algorithms utilize personal data to determine premiums, focusing on fairness and data privacy concerns associated with sophisticated risk profiling. Insurers, conversely, prioritize AI's role in minimizing moral hazard and accidental claim inflation through enhanced predictive modeling and cross-referencing capabilities against vast medical databases. The overriding user expectation is that AI will reduce operational costs, translating into more affordable premiums and superior customer service experiences.

The adoption of Artificial Intelligence (AI) is fundamentally transforming the operational landscape of the Personal Accident Insurance market, moving it toward unparalleled levels of efficiency and precise risk management. AI and Machine Learning (ML) algorithms are extensively utilized in enhancing the underwriting process by rapidly analyzing a multitude of data points—including lifestyle factors derived from wearable technology data (with consumer consent), occupational risk profiles, and historical claims data—to generate highly accurate, individualized risk scores. This capability allows insurers to move away from standardized, broad-based pricing models toward dynamic, personalized premium calculations, offering competitive advantages and improving customer acquisition rates among lower-risk populations.

Furthermore, AI significantly accelerates and streamlines the claims adjudication process, a historically labor-intensive and error-prone activity. Natural Language Processing (NLP) is employed to analyze accident reports, medical records, and policy documentation instantaneously, validating claim legitimacy and calculating appropriate payouts with minimal human intervention. This not only drastically reduces the time-to-settlement, dramatically improving customer satisfaction but also minimizes potential human error and subjective bias. The integration of image recognition and predictive modeling tools helps in flagging suspicious patterns or anomalies in claims submissions, acting as a crucial defense against fraudulent activities, thereby protecting the insurer's loss ratio and the integrity of the insurance pool.

The dynamics of the Personal Accident Insurance market are shaped by a delicate interplay of powerful drivers, structural restraints, and emerging opportunities, all magnified by critical impact forces such as regulatory changes and technological disruption. Increasing public awareness about the financial burden of accidental injuries acts as a primary market driver, compelling individuals to seek supplementary financial protection. However, consumer perception that this coverage is secondary to traditional health insurance, coupled with high initial costs for comprehensive policies, imposes notable restraints. The opportunity lies in leveraging digitalization to offer micro-insurance products targeting low-income segments. These forces interact to accelerate product innovation while requiring insurers to manage complex regulatory requirements and maintain stringent data security standards across diverse international markets, balancing accessibility with profitability.

Key drivers include rising healthcare costs globally, making lump-sum accident benefits increasingly vital for managing deductibles and co-pays; mandatory corporate group insurance provisions in industrialized nations; and aggressive expansion of distribution networks, especially through bancassurance and digital platforms. Additionally, demographic shifts, such as an aging population that is more susceptible to accidental falls and injuries, continuously bolster the demand for tailored coverage. Conversely, significant restraints include the lack of standardized definitions for injuries and disability across different policy wordings and jurisdictions, leading to potential disputes and consumer confusion. Furthermore, high loss ratios resulting from fraudulent claims or overly generous policy interpretations sometimes necessitate premium hikes, deterring price-sensitive consumers.

Opportunities for expansion are abundant, particularly in integrating accident insurance with life and health products, offering seamless, multi-coverage solutions. The proliferation of wearable technology provides an opportunity for risk mitigation and premium incentives through 'Pay-How-You-Live' models, aligning insurer and policyholder interests in safety. The impact forces, especially technological advancements like AI and blockchain, are instrumental in reshaping the competitive landscape. AI is improving efficiency, while the need for robust data governance (e.g., GDPR compliance) exerts a powerful external force, requiring substantial investment in compliance infrastructure. The macroeconomic force of interest rate volatility also impacts investment returns, indirectly affecting pricing strategy and product competitiveness in a highly price-elastic market.

The Personal Accident Insurance market is comprehensively segmented based on coverage type, end-user, distribution channel, and duration, allowing carriers to precisely tailor offerings and marketing strategies to specific consumer needs and risk profiles. Coverage segmentation differentiates between policies focusing on accidental death, permanent total disability, temporary total disability, and medical expense reimbursement, with the latter two often bundled for comprehensive protection. End-users are primarily categorized into individual purchasers, group/corporate entities, and affinity groups, each requiring specialized policy designs—for instance, corporate policies necessitate seamless integration with employee benefits packages, whereas individual policies require highly flexible customization options. This granular approach ensures market responsiveness and maximizes potential market penetration across varied customer bases.

The distribution landscape remains highly fragmented but is rapidly trending towards digital channels. Traditional avenues such as insurance brokers, agents, and bancassurance channels continue to serve complex or high-value policies, leveraging personal advice and trust. However, direct sales (online portals, mobile apps) and aggregators are gaining substantial momentum due to the product's relative simplicity and the consumer demand for immediate comparison and purchase. Policy duration, segmented into short-term (e.g., travel insurance, specific project coverage) and long-term (annual renewable policies), influences pricing and renewal strategies. The long-term segment forms the bedrock of stable, recurring premium revenue, whereas short-term policies offer high-volume sales catering to temporary risk exposure needs.

The value chain for Personal Accident Insurance begins with upstream activities focused on product design and actuarial pricing. This stage involves deep data analytics regarding mortality and morbidity rates, occupational hazards, and regional accident statistics to develop precise premium models and policy wordings. Key participants in the upstream sector include data providers, regulatory bodies (setting compliance standards), and specialized reinsurance firms that stabilize the carrier's risk exposure. The quality and granularity of data utilized here directly influence the competitiveness and sustainability of the insurance products being offered, necessitating continuous investment in advanced modeling tools and demographic research to stay ahead of evolving risk profiles.

The core midstream activities revolve around policy underwriting, distribution, and policy administration. Distribution is highly reliant on diverse channels, ranging from captive agents who offer personalized advice to digital platforms that emphasize self-service and speed. Effective policy administration, including premium collection, endorsements, and renewals, is being increasingly automated using cloud-based systems to reduce operational friction and improve the customer experience. This segment requires significant investment in CRM systems and cybersecurity infrastructure to manage vast amounts of sensitive personal data securely and efficiently across all touchpoints, ensuring compliance with strict global data protection laws.

Downstream activities center on claims management and customer relationship services, which are critical determinants of customer retention and brand reputation. Claims processing involves verification, fraud detection, and settlement, increasingly relying on AI for speed and accuracy. The primary distribution channels, both direct (insurer websites) and indirect (brokers, bancassurance), serve distinct customer segments—direct channels cater to tech-savvy, price-conscious buyers of standardized policies, while indirect channels handle complex group policies and cross-selling opportunities, maximizing reach and specialized service provision. Successful players optimize the value chain by creating seamless digital interactions from initial quote generation through to final claim payout, emphasizing speed, transparency, and empathy.

Potential customers for the Personal Accident Insurance Market are broad, encompassing virtually every segment of the working and non-working population globally, given the inherent risk of accidents in daily life. Primary end-users include salaried employees, who are often targeted through corporate group policies as part of their benefits package, providing a stable revenue stream for insurers. Individuals in high-risk professions, such as construction workers, manufacturing personnel, or transportation operators, constitute another critical segment, typically purchasing highly customized policies with elevated coverage limits commensurate with their occupational exposure to severe injury risks. These policies are often mandated or strongly recommended by industry safety standards, driving consistent demand.

Furthermore, self-employed individuals and those operating in the gig economy represent a rapidly growing customer base. Lacking the safety net of employer-sponsored benefits, these individuals recognize the critical need for personal accident coverage to replace lost income during periods of incapacitation, making tailored income protection riders highly attractive. Additionally, the market targets families, particularly primary breadwinners, where the financial consequences of an accidental death or long-term disability can be catastrophic. Students and senior citizens, although requiring lower coverage amounts, are also significant customers, often through specialized, lower-premium policies covering common risks associated with their respective life stages, such as campus injuries or accidental falls.

The fastest emerging segment of potential customers includes users of financial technology platforms and consumers engaging in frequent travel or adventure tourism. Through embedded insurance models, accident coverage is often automatically bundled or offered as an easy add-on during the transaction process, maximizing impulsive and opportunistic purchases. Banks and credit card companies also serve as crucial distribution partners, leveraging their existing customer databases to cross-sell simple, affordable accident policies. Ultimately, anyone seeking supplementary financial security beyond basic health coverage or governmental social security benefits is considered a viable, targetable customer for the Personal Accident Insurance market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $105.5 Billion |

| Market Forecast in 2033 | $166.7 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Allianz SE, AXA, Chubb Limited, The Cigna Group, Generali Group, Prudential Financial Inc., MetLife Inc., Zurich Insurance Group, Tokio Marine Holdings Inc., Ping An Insurance (Group) Company of China Ltd., Nippon Life Insurance Company, AIG (American International Group), Munich Re, Hannover Re, Swiss Re, Aviva plc, Travelers Companies Inc., ICICI Lombard General Insurance Co. Ltd., HDFC ERGO General Insurance Company, Liberty Mutual Insurance |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Personal Accident Insurance market is defined by rapid implementation of advanced digital tools aimed at optimizing every phase of the insurance lifecycle, from customer engagement to risk settlement. Core technological adoption focuses heavily on Cloud Computing to host scalable policy administration systems (PAS) and Customer Relationship Management (CRM) platforms, enabling global accessibility and real-time data synchronization. Furthermore, the integration of APIs (Application Programming Interfaces) allows seamless connectivity between insurer backend systems and external platforms, facilitating the creation of embedded insurance products and enabling rapid data exchange with aggregators and ecosystem partners. This focus on seamless integration is crucial for maintaining competitive speed in a digitally-driven market.

A major technological advancement driving efficiency is the deployment of Telematics and Wearable Technology. While traditionally associated with auto and health insurance, wearables are increasingly used in personal accident policies, particularly those focused on occupational or fitness risks. Data collected (with explicit consent) regarding activity levels, safety compliance, and potentially risky behaviors allows insurers to offer usage-based insurance (UBI) models or wellness incentives, reducing the overall probability of a claim. This utilization of real-time behavioral data transforms risk assessment from a static profile to a dynamic, continuous monitoring process, fundamentally altering the relationship between the insurer and the insured by promoting preventative safety behaviors.

In addition to AI and ML for underwriting and claims, Blockchain technology is emerging as a disruptive force, especially in managing cross-border policies and reinsurance contracts. Blockchain provides an immutable ledger for policy records and claim histories, dramatically enhancing data security, reducing the likelihood of disputes, and streamlining the complex process of verifying policy status across multiple jurisdictions. Smart contracts, built on blockchain, automatically trigger claim payouts upon verification of predefined conditions (e.g., receipt of a specific medical diagnosis or public accident report), ensuring near-instantaneous settlement for straightforward claims and fostering unparalleled levels of transparency and trust in the digital policy environment.

The Personal Accident Insurance market exhibits distinct regional variations driven by regulatory environment, economic development, and cultural attitudes toward risk. Asia Pacific (APAC) is the engine of market growth, characterized by enormous untapped potential and rapid urbanization. Countries like China and India are seeing explosive growth, supported by government initiatives promoting financial inclusion, a burgeoning middle class, and high rates of mobile internet penetration, which facilitates micro-insurance and instant digital sales. Insurers in APAC focus on scaling up simple, low-cost accident products distributed through telecommunications and e-commerce partnerships to address mass market demand.

North America (NA) and Europe represent mature, high-value markets where growth is driven less by volume and more by the complexity and customization of comprehensive coverage, particularly permanent disability benefits and specialized coverage for niche occupational risks. Regulations in Europe, such as Solvency II, heavily influence capital requirements and product pricing, demanding highly sophisticated actuarial models. In NA, the high cost of healthcare makes supplementary accident coverage—which offers cash payouts regardless of other insurance—a necessity, driving demand among consumers seeking to cover large deductibles or non-medical expenses resulting from an accident. Innovation here centers on integrating policies with broader employee benefits platforms.

Latin America (LATAM) and the Middle East & Africa (MEA) are emerging regions experiencing moderate to high growth, often tied to strong bancassurance distribution models. In LATAM, economic volatility and a desire for financial stability fuel demand for basic accident protection. In MEA, infrastructure development projects and increasing foreign worker populations necessitate group accident insurance provisions. Digitalization is rapidly transforming these markets, bypassing traditional infrastructure limitations and allowing insurers to reach previously inaccessible rural or low-income populations effectively.

PAI provides a fixed lump-sum payment or defined benefits specifically for injury, disability, or death resulting directly from an accident, irrespective of other insurance coverage. Standard Health Insurance, conversely, covers medical and hospitalization costs incurred due to both illness and injury. PAI benefits can be used for non-medical expenses, such as loss of income or debt repayment, making it a critical financial safety net, whereas health insurance typically reimburses specific medical provider charges.

AI significantly affects PAI premiums by enabling more accurate, personalized risk modeling. By analyzing real-time data (e.g., from wearables or digital behavioral patterns) and historical claims data, AI can accurately price the risk for individual policyholders. This precision often leads to fairer, lower premiums for low-risk individuals and helps insurers minimize overall claims leakage by detecting fraud, which ultimately contributes to greater long-term affordability across the market.

Most PAI policies strictly exclude injuries or death resulting from self-inflicted harm, suicide attempts, participation in illegal activities, injuries sustained while under the influence of drugs or alcohol, and injuries related to war, civil unrest, or nuclear risk. Some policies also exclude injuries sustained while participating in extremely hazardous professional or recreational activities unless a specific rider is purchased to cover such risks.

The Direct Sales channel, encompassing insurer websites, mobile applications, and digital aggregators, is projected to experience the fastest growth. This rapid expansion is driven by consumer demand for instant quotes, easy comparison tools, and immediate digital policy issuance. This channel excels in reaching younger demographics and supporting micro-insurance models, especially in high-growth regions like Asia Pacific.

Telematics and wearable technology provide granular, continuous data on policyholder behavior, such as driving habits, physical activity levels, and adherence to safety protocols. In PAI, this data is used to incentivize safer behavior through premium discounts (Pay-How-You-Live models) and allows underwriters to dynamically adjust risk scores, leading to customized pricing and proactively engaging with policyholders on risk mitigation strategies to reduce accidental injury claims.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.