ID : MRU_ 432270 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

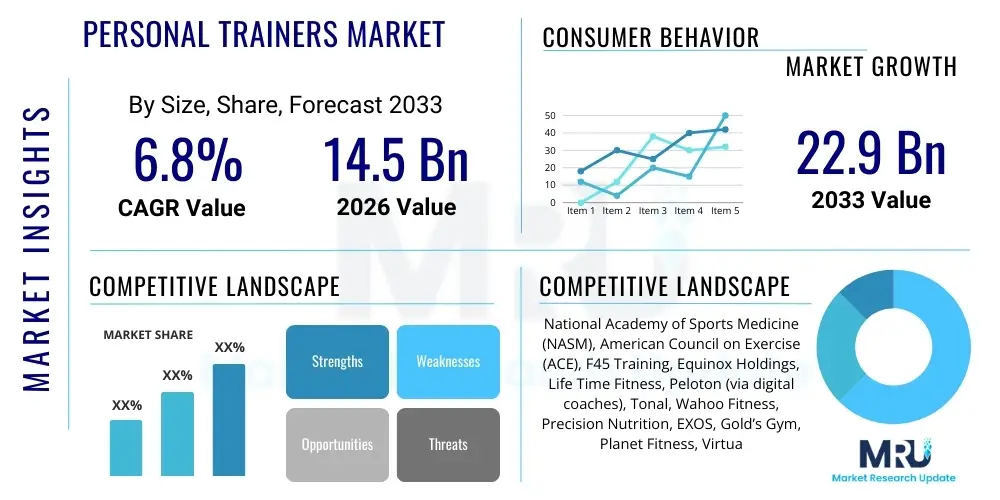

The Personal Trainers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $14.5 Billion in 2026 and is projected to reach $22.9 Billion by the end of the forecast period in 2033.

The Personal Trainers Market encompasses professional services provided by certified fitness experts who guide individuals or small groups in achieving specific health and fitness goals. These services range from tailored exercise routines and nutritional counseling to specialized athletic training and rehabilitation support. The market is fundamentally driven by a rising global awareness concerning preventive healthcare, the increasing prevalence of lifestyle diseases such as obesity and diabetes, and a strong cultural shift towards prioritizing holistic wellness. Personal trainers act as crucial motivators and educators, ensuring client safety and optimizing performance through evidence-based methodologies. This professionalism significantly differentiates structured training from general gym memberships, positioning personal training as a premium, results-oriented service.

Major applications for personal training services span several demographics and specific needs, including general fitness and weight management, specialized sports performance enhancement, post-injury physical rehabilitation, and corporate wellness programs designed to boost employee productivity and health. The flexibility offered by modern personal training—delivered both in traditional gym settings and increasingly through virtual platforms (online coaching, live video sessions)—has vastly expanded the accessibility of these services. This omnichannel approach allows trainers to connect with clients across geographical boundaries and varying schedules, catering to busy professionals, remote populations, and those preferring home-based workouts.

The primary benefits driving market expansion include highly personalized attention, optimized goal achievement through customized programming, accountability, injury prevention through proper form correction, and the integration of behavioral change strategies for long-term adherence. Driving factors prominently feature the aging population seeking specialized strength and mobility programs, the pervasive influence of social media driving demand for specific body aesthetics and fitness trends, and technological advancements enabling sophisticated tracking, personalized programming, and remote service delivery, thereby expanding the trainer's reach and enhancing client experience.

The Personal Trainers Market exhibits robust growth propelled by favorable business trends centered around digital transformation and consumer preference for specialized wellness solutions. Key business trends include the strong adoption of subscription-based hybrid models (combining in-person and digital coaching), the monetization of micro-niches such as corrective exercise, pre/postnatal fitness, and high-intensity interval training (HIIT), and increased corporate investment in employee health benefits that often include access to subsidized personal training. Market profitability is enhanced by the scaling capabilities provided by virtual training platforms, which reduce overhead costs associated with physical gym space, allowing trainers to service a larger client base efficiently while maintaining high standards of personalization and accountability.

Regionally, North America and Europe maintain market dominance due to high discretionary incomes and established fitness cultures, characterized by sophisticated regulatory frameworks for trainer certification and extensive utilization of professional fitness centers. However, the Asia Pacific (APAC) region is demonstrating the highest growth velocity, fueled by rapidly urbanizing populations, rising disposable incomes, and the growing influence of Western health and fitness trends, particularly in emerging economies like China and India. Latin America and the Middle East and Africa (MEA) are also showing promising expansion, primarily driven by governmental initiatives promoting public health and increased awareness regarding preventive measures against chronic diseases, though market penetration remains lower compared to developed regions.

Segment trends highlight the significant expansion of the Online/Virtual Training segment, challenging the traditional dominance of In-Person Training, particularly following recent global health disruptions that accelerated digital adoption. Furthermore, segmentation by specialization reveals a burgeoning demand for trainers proficient in holistic wellness, integrating mental health coaching, sleep optimization, and advanced nutritional planning alongside traditional physical fitness routines. Within the end-user segment, the 35-55 age demographic represents a core revenue stream, typically seeking maintenance, anti-aging, and disease prevention programs, while the younger demographic (18-34) drives adoption of performance-focused training and digital solutions.

User queries regarding the integration of Artificial Intelligence (AI) into the personal training landscape primarily revolve around job displacement fears, the efficacy and safety of automated training plans, and the potential for AI to democratize access to high-quality coaching. Common concerns center on whether AI algorithms can truly replicate the motivational, empathetic, and nuanced correctional capabilities of a human trainer. Conversely, users express excitement about AI's potential to revolutionize personalization, offering highly adaptive workouts based on real-time physiological data (e.g., heart rate variability, sleep quality, recovery metrics) and automated nutritional tracking, far surpassing what human trainers can manually process.

The consensus suggests that AI will not replace human trainers but rather function as a powerful assistive tool, significantly enhancing efficiency and client outcomes. AI is expected to automate administrative tasks, optimize scheduling, and provide deep analytical insights into client progress, freeing up the trainer to focus on high-value interactions such as motivation, form correction, and behavioral coaching. This symbiotic relationship transforms the personal trainer role from a physical guide to a high-level wellness strategist utilizing cutting-edge technological support, thereby increasing the value proposition and scalability of professional fitness services across the market.

The Personal Trainers Market is shaped by a confluence of accelerating drivers, structural restraints, and emerging opportunities, collectively defined as the DRO and Impact Forces. Key drivers include the global health crisis shifting consumer behavior towards self-care and preventive medicine, coupled with increasing disposable incomes globally allowing for investment in premium, specialized health services. The rapid advancement and affordability of fitness technology, particularly wearables and integrated training apps, also significantly drives market adoption by making objective progress tracking and personalized coaching highly accessible and engaging. Furthermore, the rising professionalization and standardization of the industry, driven by major certifying bodies, lends credibility and trust, attracting a broader client base.

However, the market faces significant restraints. A primary constraint is the high cost associated with one-on-one personal training, which limits its accessibility to affluent demographics, particularly in developing economies. Another significant restraint is the market saturation of unqualified or insufficiently certified individuals, which dilutes trust and creates pricing pressures for certified professionals. The high client turnover rate, inherent in a service-based industry where clients often leave once initial goals are met, poses a continuous challenge to revenue stability. Additionally, the lack of standardized regulatory oversight across various global regions creates inconsistency in service quality and ethical practices.

Opportunities for growth are concentrated in untapped niches, such as personalized genomics-based training, digital health integration with clinical services, and expansion into underserved corporate and institutional wellness markets. The integration of virtual reality (VR) and augmented reality (AR) coaching environments presents a massive opportunity to create immersive and highly engaging remote training experiences, expanding market penetration beyond traditional geographic limits. Furthermore, strategic partnerships between fitness professionals, healthcare providers, and technology firms will unlock new collaborative business models focused on comprehensive wellness management rather than just physical fitness.

The Personal Trainers Market segmentation analysis reveals critical differences in service delivery, specialization, and consumer preferences, allowing market participants to tailor their offerings effectively. Services are broadly categorized based on the mode of delivery (In-Person vs. Online) and the specific client demographic or goal (e.g., General Fitness, Specialized Rehabilitation). Understanding these segments is paramount for strategic market entry and resource allocation, as the growth rates and profitability metrics vary significantly between traditional studio models and scalable digital platforms.

The primary segmentation based on service delivery continues to show that In-Person Training holds significant revenue share, valued for the direct physical supervision, immediate form correction, and inherent motivational atmosphere. However, the fastest-growing segment is undeniably Online/Virtual Training, fueled by its cost-effectiveness, schedule flexibility, and geographical reach, catering particularly well to Millennials and Gen Z who are comfortable with digital interactions and app-based services. This shift necessitates investment in high-quality digital content, secure payment gateways, and seamless user experience interfaces.

Further segmentation by specialization highlights the market maturation beyond generic fitness advice. Niche specializations such as medical fitness (working with chronic conditions), senior fitness (focusing on balance and mobility), and corrective exercise protocols are commanding premium pricing due to the required advanced certifications and highly specific expertise. This trend indicates that future market success will be driven by trainers who can demonstrate deep competency in specialized domains rather than broad, generalized fitness knowledge, thus creating high barriers to entry for novice practitioners.

The Personal Trainers market value chain begins with the upstream activities centered on education, certification, and content creation. Upstream stakeholders include accredited certifying organizations (e.g., NASM, ACE, ACSM), specialized education providers, and technology developers creating advanced training software and wearable devices. The quality and rigor of certification directly influence the professionalism and marketability of the trainers downstream. Continuous education and specialization courses, often delivered digitally, are critical components at this stage, ensuring trainers maintain up-to-date knowledge on exercise science, nutrition, and emerging technologies like biofeedback monitoring.

The core value addition occurs at the midstream stage, where the certified personal trainer designs, delivers, and adapts the coaching service. This stage involves needs assessment, program development, exercise instruction, motivation, and progress tracking. Critical differentiators here include the trainer's specialization, interpersonal skills, and ability to effectively integrate technology for remote accountability and communication. Business models are varied, ranging from employment within large gym chains (receiving a fixed salary plus commission) to operating as independent contractors utilizing their own branding and pricing structures, which often yields higher margins but demands greater entrepreneurial effort.

Downstream activities involve the distribution channels and client acquisition strategies. Distribution channels include physical fitness facilities, dedicated personal training studios, corporate wellness contracts, and, increasingly, proprietary or third-party digital platforms/apps. Direct and indirect distribution are both prominent. Direct channels involve trainers marketing themselves directly to clients via social media or personal referrals. Indirect channels involve partnerships with gyms (acting as lead generators), rehabilitation clinics (for referrals), or corporate brokers managing wellness vendor contracts. The final interaction focuses on client retention, built through consistent results, exceptional customer service, and incentivizing long-term commitment through subscription or package pricing models.

Potential customers in the Personal Trainers Market are highly diverse but generally seek expert guidance to overcome physical plateaus, manage health risks, or achieve time-sensitive performance goals. The largest segment of end-users consists of busy professionals (ages 35-55) who value efficiency and results, often utilizing personal trainers to combat the sedentary effects of office work and manage stress, prioritizing convenient scheduling and measurable health outcomes. These customers often opt for hybrid training models that fit into unpredictable work schedules, utilizing remote check-ins alongside limited in-person sessions.

Another significant customer base comprises individuals managing or preventing lifestyle diseases, such as those with pre-diabetes, hypertension, or chronic joint issues. This demographic prioritizes trainers with specialized certifications in medical fitness and therapeutic exercise, often relying on trainers as part of a multidisciplinary health team (alongside doctors and physical therapists). For this group, the primary motivation is not aesthetics but functional improvement, pain reduction, and disease risk mitigation, making the trainer's credibility and referral network vital determinants of purchasing behavior.

Furthermore, the youth sports and competitive athlete markets represent premium potential customers, demanding highly specialized coaches focused on peak performance, injury prevention protocols, and sport-specific conditioning. This segment typically involves higher financial investment and longer contract durations, driven by intense performance targets. Finally, the growing senior population (55+) represents a rapidly expanding customer segment, primarily seeking trainers specializing in fall prevention, bone density maintenance, and preserving independence and mobility, emphasizing safety and low-impact, progressive programming.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $14.5 Billion |

| Market Forecast in 2033 | $22.9 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | National Academy of Sports Medicine (NASM), American Council on Exercise (ACE), F45 Training, Equinox Holdings, Life Time Fitness, Peloton (via digital coaches), Tonal, Wahoo Fitness, Precision Nutrition, EXOS, Gold’s Gym, Planet Fitness, Virtual Trainer+, Future, Trainerize, TrainerRoad, Whoop (Partner Services), PerformBetter, Mindbody, ClassPass. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape within the Personal Trainers Market is rapidly evolving, driven primarily by the need for enhanced personalization, efficiency, and remote monitoring capabilities. Wearable technology, including smartwatches, continuous glucose monitors (CGMs), and advanced fitness trackers, forms the foundational layer, providing trainers and clients with objective, real-time data on sleep quality, caloric expenditure, heart rate variability (HRV), and recovery status. This data is crucial for moving beyond static programming towards truly adaptive, periodized training plans, enabling trainers to make adjustments based on the client's physiological readiness, significantly reducing the risk of overtraining or injury. Furthermore, integrating these data streams into centralized training applications allows for seamless communication and immediate feedback, crucial for the success of remote coaching models.

Software platforms and dedicated training apps represent the central processing hubs for modern personal training businesses. Solutions like Trainerize, TrueCoach, and proprietary platforms developed by major fitness chains streamline administrative tasks, including scheduling, billing, and progress documentation. Critically, these platforms integrate features such as video exercise libraries, automated check-in reminders, and progress visualization tools that enhance client engagement and accountability, effectively replicating many non-physical aspects of in-person coaching. The adoption of cloud-based infrastructure ensures high accessibility and scalability, allowing independent trainers to manage a global client base efficiently.

Looking ahead, emerging technologies such as Artificial Intelligence (AI) and Machine Learning (ML) are set to redefine content delivery and personalization. AI algorithms are being developed to analyze movement patterns captured via smartphone cameras or specialized sensors, offering corrective feedback on exercise form (virtual spotters). Virtual Reality (VR) and Augmented Reality (AR) coaching platforms offer immersive workout experiences, particularly valuable for home fitness, providing detailed visual cues and gamified motivational elements. The convergence of biofeedback technology, AI analysis, and robust digital platforms is transitioning the market toward highly predictive, data-driven wellness coaching, vastly improving efficiency and client results.

North America

North America, particularly the United States, commands the largest share of the global Personal Trainers Market revenue, driven by a deeply ingrained fitness culture, high prevalence of chronic lifestyle diseases, and substantial disposable income levels allocated to wellness services. The region benefits from a robust ecosystem of highly professionalized certification bodies (ACE, NASM, NSCA) which ensure high standards of quality and ethical practice, lending credibility to the profession. The market is characterized by high penetration of both large commercial gym chains (acting as primary employers) and a growing segment of independent, niche-focused trainers operating specialized studios.

A significant trend in North America is the sophisticated adoption of digital solutions. The COVID-19 pandemic permanently accelerated the shift towards hybrid and fully virtual training models, with US and Canadian consumers demonstrating high willingness to pay for premium online coaching delivered via dedicated apps. Corporate wellness programs in major cities are increasingly utilizing personal trainers to manage employee health, providing a stable, high-value revenue stream. Furthermore, the convergence of fitness and healthcare—with physical therapists often transitioning into or collaborating closely with medical fitness trainers—is expanding the market's therapeutic scope and legitimacy.

Key countries driving growth are the United States, which represents the global center for fitness innovation and consumer spending, and Canada, which follows similar health trends but often features a higher degree of government involvement in promoting public health initiatives. The market in this region is competitive, necessitating continuous professional development and strategic specialization (e.g., corrective exercise, longevity training) for trainers to maintain premium pricing and market differentiation.

Europe

Europe represents the second-largest market, characterized by mature fitness markets in Western countries (Germany, UK, France) and rapidly developing markets in Eastern and Southern Europe. Western European nations exhibit strong consumer interest in specialized, science-backed training methods, particularly those related to injury rehabilitation and athletic performance. The emphasis on high quality of life and preventive medicine, strongly supported by government health campaigns, creates a stable demand floor for professional training services.

The European market structure differs slightly from North America, with a higher prevalence of small, independent studio models and intense competition among large, budget-friendly gym chains. Regulations regarding personal trainer qualifications vary significantly across member states, influencing pricing and service standardization. Countries like Germany and the UK have strong certification structures, while markets in Scandinavia focus heavily on sustainable, long-term health coaching rather than short-term aesthetic goals.

Growth opportunities in Europe are concentrated on digital transformation and expanding into corporate wellness. Adoption of online training services is rising, though often lagging behind North America due to strong cultural preference for face-to-face interaction, particularly among older demographics. The market is also seeing increased demand for health technology integration, with consumers readily adopting European-developed wearables and health apps that integrate seamlessly with local healthcare systems.

Asia Pacific (APAC)

The APAC region is the fastest-growing market globally, driven by massive population density, rapid economic development, rising disposable incomes, and the swift adoption of Western health and fitness trends, particularly among the youth and urban middle class. Countries like China, India, Japan, South Korea, and Australia are critical growth engines, each exhibiting unique market dynamics shaped by local cultural norms and regulatory environments.

In China and India, the market is characterized by explosive growth in the urban fitness infrastructure, with local and international gym chains expanding rapidly. Demand for personal training is high but often price-sensitive, leading to rapid expansion of small-group training models and high-volume, lower-cost services. The penetration of digital coaching is escalating quickly, overcoming infrastructure challenges in expansive geographies through mobile-first training platforms.

Australia and Japan represent mature APAC markets, sharing similarities with North American consumer behavior—high willingness to pay for specialized, premium coaching, particularly in high-performance sports and anti-aging programs. However, cultural modesty in many parts of Asia can sometimes hinder the adoption of highly visible, high-intensity training styles, favoring more discreet, specialized health and wellness centers. The primary driver remains the urgent need to address rising rates of lifestyle diseases associated with urbanization and sedentary work practices across the region.

Latin America (LATAM)

The Latin American market is experiencing significant developmental momentum, particularly in major economies such as Brazil, Mexico, and Argentina. Market growth is stimulated by increasing awareness of health benefits and a rising middle class with greater purchasing power. Brazil, with its strong cultural emphasis on physical appearance and robust sports participation, holds a dominant position in the regional market for personal training services.

However, the LATAM market faces challenges related to economic volatility and income disparity, which restrict the addressable market size for premium, one-on-one training services. As a result, small-group training, outdoor fitness boot camps, and community-based fitness initiatives are highly popular and represent a crucial point of service delivery. Digital adoption is accelerating, especially through mobile applications, allowing trainers to offer cost-effective virtual programs to a wider base.

Key focus areas for trainers in this region include weight management, body transformation, and general conditioning. Professionalization is steadily improving, though the regulatory landscape for certifications remains less unified compared to North America or Europe, leading to more informal market entry pathways for new practitioners.

Middle East and Africa (MEA)

The MEA region presents a complex but high-potential market. The Middle Eastern Gulf states (UAE, Saudi Arabia, Qatar) are characterized by substantial investment in luxury fitness facilities, high per capita spending on wellness, and government initiatives aimed at combating high obesity rates among local populations. Demand for specialized, highly credentialed expatriate trainers is particularly strong in these nations, especially for high-end, in-home training and women-only fitness centers.

In the African sub-region, the market is nascent but rapidly expanding in economic hubs like South Africa, Nigeria, and Kenya. Growth is driven by urbanization and the emergence of a health-conscious middle class. Here, the challenge lies in lower service affordability and infrastructure limitations for high-tech digital solutions. Personal training services often focus on foundational health, preventative fitness, and community engagement models.

Across the entire MEA region, cultural and religious considerations heavily influence service delivery, leading to strong segmentation by gender and demand for private, highly discrete training environments. Digital services are proving valuable in overcoming geographical barriers and providing access to internationally recognized training expertise that may not be locally available.

The Personal Trainers Market is anticipated to exhibit robust expansion, projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between the forecast years of 2026 and 2033, driven largely by digital adoption and increasing health awareness globally.

AI is transforming the personal trainer role by acting as a powerful assistant, not a replacement. AI automates complex tasks like program adaptation using real-time biometric data, scheduling, and progress tracking, allowing human trainers to focus on high-value activities such as motivation, behavioral change coaching, and nuanced form correction, thus enhancing service scalability and efficiency.

North America currently holds the largest revenue share in the Personal Trainers Market due to high consumer spending power, established fitness infrastructure, and advanced penetration of both specialized in-person and premium hybrid digital coaching services.

The key drivers include the rising global prevalence of chronic lifestyle diseases necessitating professional intervention, the increasing consumer focus on preventive healthcare, widespread accessibility through advanced digital coaching platforms, and the growing professionalism and specialization of trainers within niche fields like medical fitness and rehabilitation.

The most defining trend is the rapid expansion of the Online/Virtual Training and Hybrid Models segment. This shift offers trainers geographical flexibility and cost-effective scalability, catering to consumer demand for convenience, personalized programming, and accountability without mandatory physical attendance.

Clients are increasingly seeking trainers with advanced certifications in highly specialized areas. These include Medical Fitness (working with chronic conditions), Senior Fitness (mobility and balance), Corrective Exercise Specialist (injury prevention), and certified specialists in specialized diets or performance optimization, signaling a market shift towards competence in niche wellness solutions.

Regulatory restraints, primarily the lack of uniform standardization and licensing across different countries, pose a challenge by allowing unqualified individuals to enter the market. This creates inconsistency in service quality, erodes consumer trust, and drives price competition, particularly impacting certified, premium trainers.

Wearable technology provides critical, objective data on physiological status (HRV, sleep, recovery). This data moves training from subjective assessment to adaptive, data-driven prescription, enabling trainers to adjust workouts in real-time based on the client's readiness, thereby maximizing safety and optimizing performance outcomes in highly personalized ways.

The 35-55 age demographic, often composed of established professionals, represents the most stable revenue stream. This group typically seeks maintenance programs, stress management, anti-aging solutions, and disease prevention, valuing convenience and proven efficacy, often leading to longer-term client retention.

Corporate wellness programs are a significant opportunity, representing an indirect channel for client acquisition. Companies integrate personal training as a key employee benefit to boost productivity, reduce healthcare costs, and improve retention, providing trainers with predictable bulk contracts and a steady flow of motivated clients.

The market addresses affordability challenges primarily through the expansion of small-group training (SGT) and highly scalable digital/virtual coaching models. SGT provides personalized attention at a lower cost per individual, while virtual training reduces the trainer's operational overhead, allowing for more competitive pricing structures accessible to broader income brackets.

VR and AR present opportunities to create highly immersive and interactive remote training environments. These technologies can enhance motivation through gamification and provide detailed visual feedback on form correction in a home setting, expanding the reach of high-quality coaching to individuals who prefer working out outside traditional gym environments.

APAC growth is characterized by rapid market penetration and urbanization-driven demand, starting from a lower market maturity base. Unlike North America's dominance in premium, long-established services, APAC sees faster adoption rates for budget-friendly, high-volume models and mobile-first coaching solutions.

The upstream segment involves the creation of foundational assets, specifically trainer education, certification standards provided by accredited bodies (like NASM or ACE), and the development of core software and technology that enables efficient service delivery and client management, ensuring professional readiness before client interaction begins.

Accountability in remote settings is maintained through structured digital check-ins, automated messaging sequences, use of integrated tracking applications that monitor workout completion and nutritional adherence, and the utilization of video calls for live form critique and motivational reinforcement, replicating the structure of in-person interactions digitally.

Despite the rapid growth of digital options, traditional In-Person Training (one-on-one and small group) continues to hold the largest market share in revenue, valued by clients for the immediate, non-verbal feedback, physical safety supervision, and superior motivational environment provided by direct human interaction.

Social media acts as a powerful marketing and branding tool, enabling trainers to build trust, showcase expertise, and acquire clients directly without relying solely on gym referrals. It also drives consumer demand by promoting specific aesthetic goals and fitness trends, influencing clients' choice of specialized trainers.

Modern consumers seek holistic results; physical activity alone is often insufficient. Trainers who integrate comprehensive nutritional coaching or partner with registered dietitians offer a higher-value, more effective service package, crucial for achieving goals like weight loss or sports performance, enhancing retention and market competitiveness.

General fitness focuses on improving overall health, strength, and appearance for healthy individuals. Medical fitness specifically targets individuals with chronic diseases (like diabetes or cardiovascular issues) or post-rehabilitation needs, requiring specialized knowledge, closer communication with healthcare providers, and protocols focused strictly on safety and therapeutic outcomes.

The market is responding by expanding the Senior Fitness specialization, focusing on maintaining functional independence, improving balance, increasing bone density, and utilizing low-impact, progressive resistance training. This segment demands highly empathetic trainers who understand geriatric physiology and injury prevention protocols.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.