ID : MRU_ 431953 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

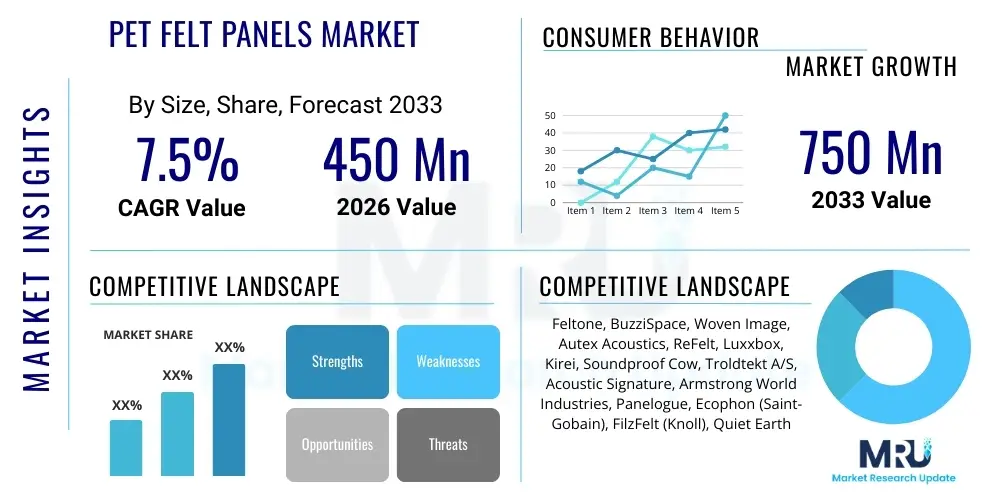

The PET Felt Panels Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 750 Million by the end of the forecast period in 2033.

The PET Felt Panels market encompasses the production and distribution of acoustic panels derived primarily from recycled polyethylene terephthalate (PET) plastic bottles. This product category is fundamentally positioned within the sustainable building and interior design sectors, offering dual benefits of superior sound absorption and environmental responsibility. PET felt is manufactured through a process involving washing, shredding, melting, and forming the recycled plastic into non-woven polyester fibers, which are then compressed and thermally bonded into rigid or flexible panel formats. These panels are increasingly utilized across commercial, institutional, and residential environments where noise reduction and aesthetic appeal are critical design requirements, reflecting a growing global emphasis on occupant well-being and green certifications in construction projects.

Major applications of PET felt panels span across corporate offices, educational facilities, healthcare settings, retail spaces, and specialized environments like recording studios and home theaters. In corporate settings, they are essential for mitigating noise pollution in open-plan layouts, enhancing speech privacy, and improving overall cognitive function among employees. The inherent material benefits, such as lightweight structure, durability, fire resistance, and mold resistance, make them a favored alternative to traditional acoustic treatments. Furthermore, the material’s versatility allows for extensive customization in terms of color, thickness, texture, and shape, enabling architects and interior designers to integrate acoustic solutions seamlessly into complex architectural visions without compromising aesthetic standards.

The primary driving factors propelling the expansion of this market include stringent governmental regulations promoting sustainable building practices, such as LEED and BREEAM certifications, which favor materials with high recycled content. Concurrently, the increasing recognition of the health and productivity benefits associated with optimal acoustic environments is stimulating demand. The global push toward circular economy principles further reinforces the market, positioning PET felt panels as a key innovation in tackling plastic waste while addressing sophisticated acoustic challenges in modern construction. Continuous technological advancements in manufacturing processes are also leading to more cost-effective production methods and enhanced product performance, broadening the market’s accessibility across various price points and application areas globally.

The global PET Felt Panels market is experiencing robust growth driven by accelerating global sustainability mandates and the paradigm shift toward human-centric office and educational design. Business trends indicate a strong move toward vertical integration among key manufacturers, aiming to secure reliable sources of high-quality recycled PET (rPET) flake supply and achieve greater control over the production lifecycle, enhancing profitability and ensuring compliance with green claims. Furthermore, there is a visible trend toward offering comprehensive acoustic solutions, where panels are integrated with lighting systems or modular furniture, moving beyond simple wall treatments to holistic interior solutions. Customization capabilities, facilitated by advanced cutting and printing technologies, are unlocking premium market segments that demand unique and highly personalized interior aesthetics for high-end commercial projects.

Regional trends reveal that Asia Pacific (APAC) is emerging as the fastest-growing market, primarily fueled by massive infrastructure development, rapid urbanization, and increased adoption of international building standards in commercial real estate across countries like China, India, and Southeast Asian nations. North America and Europe, while mature markets, maintain dominance in terms of technological innovation and market valuation, largely due to stringent environmental policies, high awareness regarding acoustic quality, and the widespread refurbishment of existing commercial buildings to meet modern sustainability targets. The Middle East and Africa (MEA) region show burgeoning potential, particularly within high-profile hospitality and institutional projects where striking architectural design and acoustic performance are paramount requirements.

Segment trends underscore the dominance of the commercial application segment, driven by persistent demand for acoustic privacy in modern workspaces. Within product types, ceiling panels and baffles are witnessing significant uptake, offering effective overhead sound control solutions that are particularly suitable for large, reverberant spaces. The material thickness segment shows increasing traction for 12mm and 24mm panels, balancing acoustic efficacy with cost and ease of installation. Segmentation analysis also highlights the expanding role of distributors and specialized acoustic consultants in the sales channel, reflecting the technical nature of product specification and installation required in sophisticated architectural projects. Overall, the market remains highly competitive, prioritizing innovation in material aesthetics, acoustic performance metrics, and verified sustainable sourcing credentials.

Common user questions regarding AI's influence on the PET Felt Panels market typically center on efficiency gains in manufacturing, the personalization of design, and the integration of acoustic elements into smart building ecosystems. Users are keen to understand how Artificial Intelligence can optimize the complex production processes involving recycled materials, specifically concerning defect detection, material density control, and waste minimization during cutting and molding. Furthermore, there is significant interest in AI-driven acoustic modeling software that can accurately predict required panel placement and density based on room geometry and intended function, moving beyond traditional calculation methods. Expectations include using AI to analyze real-time acoustic data in occupied buildings, adjusting or recommending maintenance schedules for panels, or providing dynamic design suggestions tailored to fluctuating occupant needs, thereby enhancing the functional lifespan and efficacy of PET felt installations in smart environments.

The PET Felt Panels market is currently shaped by a powerful confluence of drivers, restraints, and opportunities that dictate its trajectory and competitive landscape. Key drivers primarily revolve around the strong global impetus toward sustainability and the increasing regulatory environment favoring circular economy materials. The demonstrable benefits of PET felt in enhancing indoor environmental quality (IEQ), particularly through effective noise reduction, directly contribute to improved occupant productivity and well-being, which is a major purchasing criterion for commercial developers. These factors create robust, sustained demand, especially in high-density urban areas where noise pollution is a chronic issue, pushing architects to specify high-performance, aesthetically pleasing acoustic materials derived from recycled sources. The versatility of design and customization capabilities further solidifies its position as a preferred modern building material.

However, the market faces significant restraints that temper its growth rate and market penetration. The relatively high initial cost of PET felt panels compared to conventional gypsum or mineral fiber acoustic boards remains a barrier for budget-constrained projects, particularly in developing economies, despite the long-term cost benefits associated with durability and environmental compliance. Furthermore, the reliance on a stable supply chain of post-consumer PET bottles introduces volatility; fluctuations in recycling rates and competition from other industries utilizing rPET (e.g., textiles, packaging) can impact raw material prices and availability. Finally, achieving consumer and designer awareness regarding the distinct performance and sustainability attributes of PET felt, often requiring detailed technical specification support, poses a perpetual marketing challenge that requires significant investment in educational content.

Opportunities for market acceleration are abundant, primarily focused on technological innovation and market expansion. The development of advanced manufacturing techniques that allow for even higher recycled content (approaching 100%) or novel material blends to enhance fire resistance and durability represents a lucrative avenue. Geographically, untapped potential lies in residential retrofit markets, driven by increasing consumer expenditure on home office upgrades and interior design enhancements, moving beyond the traditional commercial focus. Moreover, the integration of PET felt with smart technology, such as embedded sensors or integrated heating/cooling elements, opens up premium niche markets requiring multi-functional, sophisticated building solutions. These forces collectively create a dynamic market environment where innovation and verified sustainability credentials are essential for sustained competitive advantage.

The PET Felt Panels market is segmented comprehensively based on several critical parameters including Type, Application, End-use, and Thickness, allowing for targeted analysis of consumer preferences and market needs across various sectors. Analyzing these segments provides strategic insights into which product configurations are gaining traction and which end-user industries are driving the most significant volume and value growth. This detailed categorization helps manufacturers tailor their product portfolios, pricing strategies, and distribution channels to maximize market reach and responsiveness. Key segmentation highlights the shift toward customized solutions and high-density panels necessary for meeting stringent acoustic requirements in commercial environments.

The value chain for the PET Felt Panels market begins fundamentally at the upstream stage with the sourcing and preparation of raw materials, which primarily involves the collection, sorting, washing, and flaking of post-consumer PET bottles to produce high-quality recycled PET (rPET) flakes or pellets. This segment is highly sensitive to global recycling infrastructure efficiency and commodity pricing volatility, meaning securing long-term, stable contracts with reliable recycling partners is critical for cost management and ensuring the sustainability claims of the final product. The processing stage then transforms the rPET into non-woven felt through advanced manufacturing techniques like needle punching and thermal bonding, which requires specialized, energy-intensive machinery. Efficiency at this stage, focusing on minimizing energy use and maximizing yield, directly impacts the final product's competitive pricing and environmental footprint.

The midstream of the value chain involves the fabrication and customization processes, where large sheets of PET felt are cut, shaped, printed, and sometimes laminated or backed with specialized adhesives to meet specific architectural requirements. This customization is often facilitated by advanced technologies such as CNC cutting, laser etching, and high-resolution digital printing, adding significant value and differentiating premium products. Following fabrication, the distribution channel plays a pivotal role in market penetration. Sales are typically managed through a mix of direct and indirect channels. Direct sales are common for large-scale commercial contracts, involving close collaboration between manufacturers and architecture/design firms (A&D). Indirect channels utilize specialized acoustic distributors, building material wholesalers, and increasingly, e-commerce platforms targeting smaller residential or DIY markets, requiring robust logistics and warehousing capabilities to handle varying product sizes and complex installation guides.

The downstream segment encompasses the end-users—architects, interior designers, commercial developers, and facility managers—who specify and install the panels. The success in the downstream market relies heavily on providing comprehensive technical support, including acoustic performance data (NRC ratings), fire safety certifications, and aesthetic samples, effectively bridging the gap between technical material properties and architectural vision. Installation services, whether provided directly by the manufacturer or through certified contractors, finalize the value chain, ensuring the panels function optimally in the intended environment. The circularity of the product is also a growing consideration, with some manufacturers initiating take-back programs to recycle the panels at the end of their useful life, thereby closing the loop and enhancing the product’s long-term environmental value proposition.

The primary end-users and buyers of PET felt panels are highly segmented across the commercial, institutional, and residential construction ecosystems, with purchasing decisions heavily influenced by specifications set by architects and interior designers. Commercial real estate developers constitute a major customer base, particularly those undertaking large-scale office park developments, high-rise buildings, and mixed-use facilities where employee well-being and green building certifications (e.g., LEED Platinum, WELL Building Standard) are non-negotiable requirements. These customers prioritize high Noise Reduction Coefficient (NRC) performance, fire safety compliance, and verifiable documentation of recycled content to meet their corporate sustainability mandates and enhance property valuations in a competitive market. Furthermore, the hospitality sector, including hotels, resorts, and high-end restaurants, is increasingly adopting these panels for subtle noise control that complements luxurious and modern design aesthetics.

Institutional customers, encompassing the educational sector (universities, K-12 schools) and healthcare facilities (hospitals, clinics), represent another critical customer segment. In schools, effective acoustic management is directly linked to improved learning outcomes and speech intelligibility in classrooms and auditoriums, driving sustained demand for durable, non-toxic, and easy-to-clean acoustic solutions like PET felt. Healthcare environments utilize these panels to reduce stress-inducing ambient noise, contributing to patient recovery and staff concentration, making material specifications highly focused on hygiene, low Volatile Organic Compounds (VOCs), and stringent fire ratings. Facility management companies that oversee the refurbishment and maintenance of existing building stock are also key purchasers, focusing on panels that offer quick installation and long-term durability to minimize disruption during operational periods.

Indirectly, but critically influential, are the independent architecture and interior design firms (A&D community). They act as the gatekeepers, specifying the materials used in almost all major construction projects. Manufacturers dedicate significant sales and marketing efforts toward educating this community about the technical and aesthetic advantages of PET felt, including its customizable features, color palettes, and structural versatility. The residential market, while smaller in volume, is growing rapidly, driven by homeowners investing in dedicated home offices, media rooms, and aesthetic acoustic solutions to improve quality of life and enhance remote work environments, typically sourcing materials through specialized retail distributors or professional home improvement contractors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 750 Million |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Feltone, BuzziSpace, Woven Image, Autex Acoustics, ReFelt, Luxxbox, Kirei, Soundproof Cow, Troldtekt A/S, Acoustic Signature, Armstrong World Industries, Panelogue, Ecophon (Saint-Gobain), FilzFelt (Knoll), Quiet Earth |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the PET Felt Panels market is constantly evolving, focusing intensely on improving material purity, manufacturing efficiency, and aesthetic versatility. A foundational technology is the advanced recycling process used to convert post-consumer PET into high-quality fiber, specifically chemical recycling techniques which promise higher purity and potentially infinite recycling cycles compared to traditional mechanical recycling. This technological advancement ensures a steady supply of high-grade raw material that meets stringent requirements for color consistency and structural integrity necessary for premium acoustic panels. Furthermore, manufacturers are investing in highly automated, continuous production lines that utilize sophisticated needle punching and thermal bonding technologies, allowing for the creation of panels with customized densities and consistent acoustic performance across large batches, significantly reducing production lead times and labor costs.

In the fabrication phase, precision cutting and customization technologies are paramount to market differentiation. High-speed Computer Numerical Control (CNC) routers and advanced laser cutting systems enable manufacturers to produce complex geometric patterns and custom three-dimensional shapes with exacting precision, offering architects unparalleled freedom in design execution. Complementing this is the emergence of digital printing technology specifically optimized for porous polyester felt surfaces. This allows for high-resolution graphics, wood grain patterns, or photographic images to be printed directly onto the acoustic panels without compromising their sound-absorbing properties, transforming the panels from mere functional elements into primary design features within an interior space. These advancements in digital fabrication are crucial for targeting niche markets demanding bespoke architectural acoustic solutions.

Beyond material processing, innovative product technologies are emerging that integrate additional functionality into the felt panels. This includes the development of multi-functional panels that incorporate lighting elements (LED strips), modular attachment systems (magnetic or interlocking mechanisms for easy reconfigurability), or specialized coatings that enhance fire resistance (Class A certification) or improve hygiene characteristics. Furthermore, there is growing exploration into incorporating Phase Change Materials (PCMs) within the panel structure to offer passive temperature regulation alongside acoustic benefits, moving the product beyond simple sound absorption toward integrated interior climate management solutions. These technological integrations underscore the market's trajectory toward highly engineered, multi-utility building components essential for future smart and sustainable construction projects.

PET Felt Panels are primarily composed of recycled polyethylene terephthalate (rPET) fibers, derived from post-consumer plastic bottles. This use of recycled content significantly reduces landfill waste and the reliance on virgin petroleum-based resources, positioning the panels as a highly sustainable and circular economy building material widely favored for LEED and WELL certified projects globally.

PET Felt Panels are highly effective sound absorbers due to their porous, non-woven fiber structure, which traps sound waves and reduces reverberation. Depending on thickness and density (e.g., 9mm, 12mm, or 24mm), these panels typically achieve a Noise Reduction Coefficient (NRC) ranging from 0.45 up to 0.90, making them suitable for mitigating mid- to high-frequency noise in commercial and institutional settings.

The primary growth applications are commercial offices, where they address noise challenges in open-plan environments, and institutional facilities, such as schools and hospitals, where optimal acoustics are essential for learning and patient recovery. The global emphasis on improving Indoor Environmental Quality (IEQ) and stringent green building mandates are the core demand drivers.

Key challenges include the high initial cost compared to traditional non-sustainable acoustic materials and volatility in the supply chain of high-quality recycled PET (rPET) flakes. Furthermore, competitive pressures require continuous investment in advanced technologies to enhance aesthetic customization and ensure compliance with stringent fire safety standards across different regions.

The Asia Pacific (APAC) region, specifically emerging economies within Southeast Asia, China, and India, is forecast to exhibit the highest Compound Annual Growth Rate (CAGR). This acceleration is attributed to rapid urbanization, massive infrastructure development, and increasing adoption of international commercial building standards that prioritize sustainable and acoustically sound construction materials.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.