ID : MRU_ 435793 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

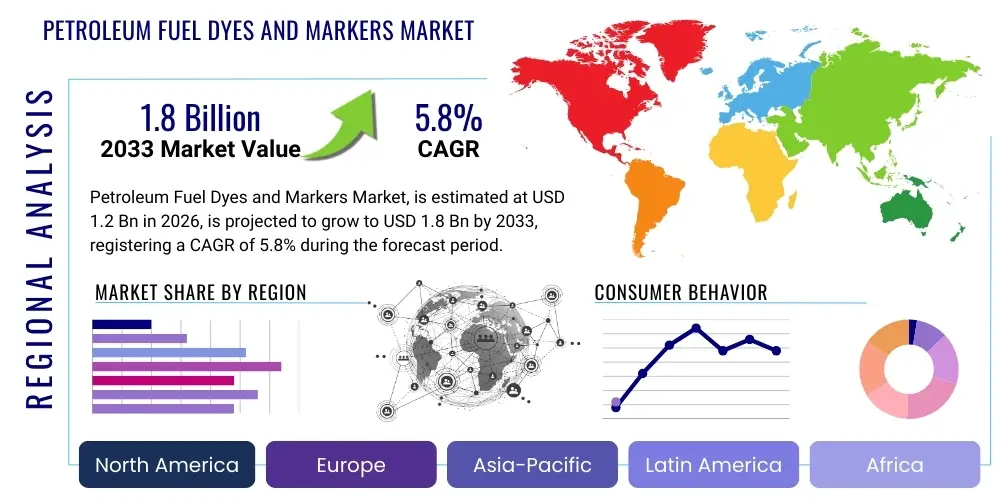

The Petroleum Fuel Dyes and Markers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 1.8 Billion by the end of the forecast period in 2033.

The Petroleum Fuel Dyes and Markers Market encompasses specialized chemical compounds utilized globally to identify, authenticate, and differentiate various types of petroleum products, primarily for taxation, regulatory compliance, and anti-fraud purposes. These chemical additives are crucial tools employed by governmental bodies and fuel distributors to ensure that lower-taxed or subsidized fuels (such as heating oil or agricultural diesel) are not diverted for use in higher-taxed applications (like road transportation). The products range from visible solvent-based dyes that impart specific colors to invisible markers, which are detectable only through sophisticated laboratory or field testing apparatus, offering a robust defense against fuel adulteration and smuggling operations. The core function of these markers is to facilitate easy and rapid verification of fuel origin and intended use, supporting fiscal integrity across the energy supply chain.

The operational mechanism of fuel markers often involves sophisticated molecular structures that are difficult and expensive for illicit operators to remove or mask, thereby ensuring the longevity and reliability of the marking system. Major applications span high-volume consumption sectors, including gasoline, on-road diesel, off-road diesel (non-taxed or rebated), kerosene, and aviation fuels, where regulatory mandates require clear distinction based on quality or tax status. Key benefits derived from the use of advanced dyes and markers include enhanced government revenue protection, promotion of fair competition among legitimate fuel suppliers, and maintenance of engine performance standards by preventing the use of substandard or contaminated fuels. The global shift toward cleaner fuels and stricter environmental mandates has also driven the need for highly specific markers capable of surviving complex refining processes and identifying environmentally compliant blends.

Driving factors for sustained market growth are deeply rooted in intensifying regulatory landscapes worldwide, particularly concerning sulfur content differentiation and carbon taxation schemes. Governments, facing significant revenue losses due to fuel fraud, are continuously investing in advanced, next-generation marking technologies that offer superior traceability and resistance to common chemical removal techniques. Furthermore, the expansion of global trade in refined petroleum products necessitates standardized international marking protocols, compelling major refineries and logistics companies to adopt certified dye and marker systems. The ongoing focus on protecting the subsidy systems in developing economies, coupled with increased consumer awareness regarding fuel quality, solidifies the foundational demand for reliable and robust fuel authentication solutions.

The Petroleum Fuel Dyes and Markers Market is experiencing dynamic shifts, driven by escalating fuel fraud prevention efforts and stricter international regulatory compliance requirements. Business trends highlight a significant pivot toward invisible marking technologies and advanced chemical tracers that provide higher levels of security and are difficult to reverse engineer. Key market players are investing heavily in research and development to create solvent dyes and markers that are compatible with increasingly complex fuel chemistries, including biofuels and high-octane gasoline blends, ensuring consistent performance regardless of the fuel substrate. Consolidation among specialty chemical manufacturers and strategic partnerships with governmental regulatory agencies are defining the competitive landscape, prioritizing integrated solutions that combine physical marking with digital traceability systems.

Regionally, North America and Europe continue to dominate the market due to well-established regulatory frameworks and high enforcement standards concerning fuel taxation and quality control, particularly in distinguishing between taxable road diesel and untaxed agricultural or heating oils. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth, primarily fueled by rapid industrialization, massive infrastructure development leading to high diesel consumption, and increasing governmental initiatives in countries like India and China to curb illicit fuel activities and protect subsidy programs. Latin America and the Middle East & Africa (MEA) present emerging opportunities as these regions modernize their regulatory bodies and seek cost-effective methods to minimize revenue leakage associated with fuel adulteration and theft across vast, often porous, distribution networks.

Segment trends underscore the dominance of the Solvent Dyes category, valued for its immediate visual impact and cost-effectiveness, particularly in distinguishing standard fuel types. Simultaneously, the market is witnessing accelerated adoption of advanced Marker Systems, including fluorescent, spectroscopic, and isotopic markers, especially in high-security applications like aviation fuel certification and military contracts, where absolute proof of authenticity is required. Application-wise, the Diesel segment remains the largest consumer due to widespread use in transportation, industrial machinery, and agricultural sectors, often involving multiple tax tiers that necessitate complex marking schemes. The industry is also observing growth in niche applications, such as specialized marine fuel markers, driven by new international maritime organization (IMO) regulations concerning low-sulfur fuels.

Common user questions regarding AI's influence on the Petroleum Fuel Dyes and Markers Market generally revolve around four core themes: can AI enhance fraud detection and enforcement, how can AI optimize the marker supply chain, will AI predict fuel fraud hotspots, and what role will machine learning play in developing new marker chemistries? Users express high expectations that AI, particularly machine learning and computer vision, could significantly improve the efficiency and accuracy of enforcement activities, moving beyond traditional random sampling. The core concern often centers on the practical implementation challenges, data requirements, and the necessity for integrating legacy testing infrastructure with modern AI-driven analytics platforms. The consensus is that AI will act less as a direct replacement for chemical markers and more as a sophisticated analytical layer, translating vast amounts of field data into actionable intelligence, thereby making the existing marking system substantially more effective and preemptive rather than reactive.

AI is poised to revolutionize the enforcement side of the market by providing predictive analytics capabilities that identify high-risk routes, distribution centers, and blending operations where fuel fraud is most likely to occur. By analyzing historical enforcement data, satellite imagery, point-of-sale transactions, and marker testing results, AI algorithms can pinpoint anomalies indicative of illicit activities, allowing regulatory bodies to allocate limited inspection resources far more efficiently. Furthermore, advanced AI-driven computer vision systems, integrated with automated sampling equipment, can dramatically speed up the verification process at large ports or border crossings. These systems could potentially analyze colorimetric responses or spectroscopic signatures of marked fuels in near real-time, instantly flagging discrepancies that warrant deeper human investigation, thus dramatically reducing latency in the enforcement cycle and increasing deterrence effectiveness across the entire petroleum supply chain.

In the chemical manufacturing segment, AI and machine learning are beginning to accelerate the R&D process for novel dye and marker formulations. By simulating molecular interactions and predicting the stability, detectability, and compatibility of potential new markers within various fuel matrices, AI reduces the need for extensive and costly traditional lab trials. This capability is critical for developing "future-proof" markers that remain robust against increasingly sophisticated attempts at chemical removal or masking. Moreover, AI optimization of the supply chain logistics for these specialty chemicals—managing inventory levels based on geopolitical risk, regulatory changes, and forecasted fuel consumption—ensures that the critical supply of dyes and markers is maintained efficiently globally, minimizing stockouts and maximizing the effectiveness of government marking programs across various international jurisdictions and varying seasonal demand cycles.

The Petroleum Fuel Dyes and Markers Market is powerfully shaped by a dynamic interplay of Drivers, Restraints, and Opportunities, which collectively constitute the critical Impact Forces guiding its trajectory. A primary Driver is the increasing stringency of global fuel taxation and environmental regulations, particularly the mandates requiring clear differentiation between high-sulfur and low-sulfur fuels, as well as tax-exempt versus road-use fuels. Governments worldwide are actively seeking sophisticated marking solutions to combat substantial revenue losses from illegal blending and smuggling, viewing markers as an essential fiscal safeguard. This regulatory push is compounded by the necessity for advanced security features in markers that are non-removable and specific to unique fuel types, promoting continuous investment in R&D for next-generation markers.

Conversely, the market faces significant Restraints, primarily stemming from the high upfront costs associated with implementing and maintaining sophisticated marker detection and verification infrastructure, particularly in developing economies where resources are limited. Furthermore, the constant challenge posed by illicit operators who develop counter-technologies to remove or mask existing markers necessitates continuous and costly innovation, leading to a perpetual technology arms race. Compatibility issues also present a restraint; as the fuel matrix becomes more complex with the inclusion of various biofuel percentages (e.g., ethanol, biodiesel), existing dyes and markers must be rigorously tested to ensure they do not degrade, interfere with engine performance, or become undetectable, thereby increasing product development complexity and time-to-market.

Significant Opportunities lie in the penetration of advanced invisible marker technologies, such as spectroscopic tracers and DNA marking systems, which offer superior security and are far harder to counterfeit or remove than traditional visual dyes. There is a burgeoning market for integrated solutions that combine chemical markers with digital platforms (e.g., blockchain for traceability) to provide end-to-end authentication and audit trails from the refinery gate to the consumer pump. The ongoing global transition toward renewable and sustainable fuels also creates specific niche opportunities for markers designed exclusively for highly regulated advanced biofuels, ensuring their certification and tax compliance. These Impact Forces ensure that while initial compliance costs act as a short-term barrier, the long-term imperative of fiscal protection and environmental compliance will propel the market toward advanced, high-security marking systems, securing sustained growth.

The Petroleum Fuel Dyes and Markers market is systematically segmented based on Type, Product Type, Application, and End-Use, reflecting the diverse regulatory and technical requirements across the fuel industry. The segmentation analysis provides granular insights into which product chemistries and end-user applications drive the most significant market revenue and growth potential. The Type segmentation, distinguishing between Dyes and Markers, reveals the foundational split between visual identification and covert authentication methods. While dyes offer cost-effective, immediate verification, the complexity of modern fuel fraud increasingly drives demand toward highly specialized, non-visible markers that withstand chemical tampering and require specialized detection equipment, signaling a strategic shift in market focus toward higher-security products.

The Product Type segmentation is crucial, breaking down the chemical families utilized. Solvent Dyes remain dominant due to their solubility in hydrocarbon fuels and vibrant color output, serving as the industry standard for common differentiations (e.g., red diesel). However, the rise of specialized proprietary Marker Systems, including fluorescent compounds, biological markers (DNA markers), and chemical tracers, highlights the need for advanced anti-counterfeiting measures, especially in sensitive high-value fuel chains like aviation. These advanced markers are typically required by regulatory bodies aiming for maximum protection against sophisticated adulteration, driving premium pricing and technological innovation within this sub-segment and expanding the total addressable market for high-security solutions.

Application analysis centers on the distinct regulatory environments of different fuel types. Diesel applications constitute the largest segment globally due to widespread use in commercial transport, agriculture, and construction, often carrying different tax liabilities that necessitate robust marking protocols. The Gasoline segment follows, primarily driven by octane differentiation and quality control. Furthermore, niche applications like Aviation Fuel (Jet Fuel) require extremely rigorous marking for safety and regulatory compliance, while Marine Fuel marking is gaining prominence following the global IMO 2020 sulfur cap mandate, demanding specialized markers compatible with new low-sulfur heavy fuel oils and marine gas oils, thereby diversifying market opportunities.

The Value Chain for Petroleum Fuel Dyes and Markers begins with Upstream activities centered on the procurement and synthesis of highly specialized chemical intermediates. This stage is dominated by specialty chemical manufacturers who must adhere to stringent quality control standards, ensuring high purity and consistent performance of the chemical ingredients, which often include complex organic molecules and proprietary compounds. Research and development activities, involving chemical engineers and regulatory experts, are critical at this stage to develop markers that are thermally stable, highly soluble in hydrocarbon matrices, and resistant to chemical stripping, demanding significant intellectual capital investment and compliance testing before commercialization. The high barriers to entry related to specialized chemistry and intellectual property characterize the upstream segment of the value chain.

The Midstream phase involves the formulation, production, and primary distribution of the finished dye and marker products. Manufacturers convert raw chemical intermediates into concentrated liquid or powder formulations, tailored to meet specific regulatory requirements (e.g., concentration levels mandated by national tax authorities). Packaging and logistics are crucial here, as these chemicals must be handled and shipped under strict environmental and safety guidelines to major customers, including large international oil companies (IOCs), national oil companies (NOCs), and governmental agencies responsible for marking programs. Efficient inventory management and the ability to rapidly supply customized marker batches are key competitive differentiators in this midstream phase, often involving direct sales models to ensure product integrity and confidentiality.

The Downstream segment focuses on the application, detection, and enforcement side of the value chain. This involves the integration of the marker injection systems at refineries, bulk terminals, and distribution hubs, ensuring precise and consistent dosing of the fuel. Distribution channels are predominantly direct-to-customer for high-volume users (refineries) and regulated bodies, often utilizing specialized logistics providers knowledgeable in hazardous material transport. Indirect channels may involve specialized distributors who supply smaller blenders or regional enforcement agencies with testing kits and detection equipment. The final crucial step in the downstream value chain is the enforcement and verification process, requiring the deployment of sophisticated field and laboratory testing equipment, often managed by government agencies or third-party compliance firms, closing the loop on the efficacy of the entire marking system.

The primary customers for Petroleum Fuel Dyes and Markers are entities with direct involvement in the production, distribution, and taxation of refined petroleum products, driven by mandatory compliance requirements. End-users are broadly categorized into three major groups: the upstream and midstream oil and gas industry, governmental and regulatory bodies, and high-volume consumers. Oil and Gas Refineries and Bulk Fuel Terminal Operators represent the largest commercial segment, as they are typically mandated by law to introduce the required tax markers or differentiate dyes directly into the fuel stream at the earliest possible stage before distribution. These customers require high-volume, consistent supply, and technical support to ensure accurate dosing and adherence to stringent application tolerances, forming long-term contractual relationships with specialty chemical suppliers.

Governmental Agencies and Regulatory Bodies, such as national revenue departments, customs organizations, and environmental protection agencies, are critical customers not only as mandate setters but also as direct purchasers of advanced marker systems and accompanying detection technology. These entities often contract directly with chemical providers for proprietary, highly secure markers designed exclusively for national fuel integrity programs, providing stability and security to the market. Their procurement requirements are heavily focused on anti-counterfeit features, ease of field detectability, and robust performance under varying climatic conditions, emphasizing reliability over cost optimization, thereby driving demand for high-end marker solutions.

Lastly, high-volume commercial and institutional users, including large Transportation and Logistics companies, Agricultural Cooperatives utilizing rebated fuels, and Defense & Military organizations, constitute the indirect but influential end-user base. While they may not purchase the markers directly, their consumption patterns dictate the volume and types of fuels that require marking. Moreover, certain industries, like aviation and marine transport, might require specialized fuel markers for internal quality assurance or compliance with international regulatory bodies (e.g., IATA, IMO). The underlying demand is fundamentally inelastic, dictated by regulatory compliance and the need to protect against engine damage from adulterated fuels, ensuring continuous consumption across all global regions regardless of economic fluctuations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 1.8 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SGS SA, Johnson Matthey, Orient Chemical Industries Ltd., The Dow Chemical Company, BASF SE, Innospec Inc., Sun Chemical (DIC Corporation), Spectracolor Inc., United Color Manufacturing, Inc., Ciba Specialty Chemicals (now part of BASF), Pylam Products Co., Inc., American Gas & Chemical Co., Dynalene Inc., Chromatech Incorporated, Mid Continent Chemical Co., Inc., Authentix, Inc., Tracereport, Inc., R.N. Naphtha Dyes, John Hogg Technical Solutions, Steiner Fuel. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Petroleum Fuel Dyes and Markers market is underpinned by an increasingly sophisticated technology landscape focused on achieving higher levels of security, traceability, and robust detectability across diverse fuel environments. Traditional technologies rely on simple, solvent-based dyes that offer immediate visual identification but are susceptible to masking or removal. The current technological evolution is moving aggressively towards sophisticated, proprietary chemical markers known as "covert markers." These technologies include fluorescent tracers that respond only to specific wavelengths of light, specialized spectroscopic markers that produce unique signatures detectable only by laboratory instruments (such as UV-Vis spectrophotometers or mass spectrometry), and advanced chemical tagging compounds designed to withstand the harsh thermal and chemical environments of refining and blending processes, ensuring longevity and integrity throughout the supply chain.

A critical area of technological advancement involves the development of proprietary marker detection equipment. For governmental enforcement, the focus is on creating field-portable, rugged, and highly accurate detection devices that can yield quantifiable results in minutes, reducing reliance on centralized laboratory testing. These advanced portable analyzers often utilize miniaturized spectroscopy techniques coupled with digital interfaces, enabling direct transmission of results and GPS coordinates to central compliance databases. Furthermore, the integration of computational chemistry techniques is accelerating the discovery of new marker molecules. Machine learning algorithms are being employed to predict the stability and compatibility of potential new markers with complex fuel mixtures, especially those containing high proportions of biofuels, drastically cutting down the traditional time and expense involved in chemical synthesis and testing, ensuring technological readiness for future fuel standards.

Beyond the chemical composition of the marker itself, information technology and digital traceability platforms are becoming foundational components of the overall solution. Modern marking programs increasingly integrate specialized chemical markers with secure digital platforms, such as blockchain technology, to provide an immutable audit trail of the fuel's journey. This digital layer records when and where the marker was injected, who tested the fuel, and the corresponding results, offering end-to-end transparency and reducing opportunities for fraud within the paper trail. This holistic approach, combining advanced chemistry (the marker) with robust digital verification (the traceability system), represents the cutting edge of the market, offering unparalleled security and operational efficiency to both regulatory bodies and fuel distributors across international boundaries and complex distribution networks.

The dynamics of the Petroleum Fuel Dyes and Markers Market vary significantly across major global regions, dictated by regulatory stringency, fuel consumption patterns, and the prevalence of fuel fraud activities. North America, encompassing the highly regulated markets of the United States and Canada, represents a mature market characterized by robust governmental marking programs, particularly for differentiating off-road and agricultural diesel (dyed red) from taxable road diesel. The region’s advanced infrastructure and high enforcement standards drive the adoption of reliable, high-quality solvent dyes and increasingly sophisticated invisible markers to protect substantial tax revenues. Demand is stable, focused heavily on minimizing evasion related to state and federal excise taxes, prompting continuous investment in advanced field testing equipment and mandatory compliance protocols across large distribution terminals.

Europe stands out due to its highly complex and fragmented regulatory environment, where individual member states often employ unique marking schemes to differentiate fuels subject to varying VAT, excise duties, and environmental taxes (e.g., low-sulfur mandates). The region is a key adopter of proprietary and advanced marker systems, driven by stringent environmental regulations and a coordinated effort across EU borders to combat cross-border fuel smuggling and tax fraud. Countries such as the UK and Germany maintain rigorous protocols for coloring gas oil and monitoring biofuel content, pushing manufacturers to develop markers compatible with diverse, mandated biofuel blends. The European market emphasizes high-security markers due to the inherent logistical challenges of an integrated market with multiple, co-existing taxation regimes.

Asia Pacific (APAC) is forecasted to be the fastest-growing region, powered by explosive growth in refined product consumption across India, China, and Southeast Asian nations, driven by massive infrastructure and industrial development. This rapid expansion, combined with the presence of fuel subsidy programs in many countries, creates significant opportunities for illicit activities, driving high demand for marking solutions to curb fraud and protect government spending. Governments in this region are initiating large-scale fuel integrity programs, often leapfrogging older dye technologies directly to advanced spectroscopic markers to ensure transparency and accountability in their vast and often decentralized fuel supply chains, marking it as a critical focus area for global dye and marker suppliers.

Latin America is an emerging market characterized by economic volatility and significant government intervention in the fuel sector, including subsidies and price controls, which inherently lead to high levels of fuel diversion and smuggling, especially across national borders. The requirement for reliable anti-fraud mechanisms is paramount, leading to increased government expenditure on markers, although implementation and enforcement consistency remain regional challenges. The Middle East and Africa (MEA) region presents a highly fragmented landscape. In the Middle East, large NOCs primarily drive demand for markers for quality control and subsidy protection. In contrast, Africa's demand is spurred by the intense challenge of fuel adulteration and theft in long-distance supply routes, compelling countries to adopt marking programs to safeguard both revenue and engine health, making the region a key focus for basic and intermediate dye and marker solutions.

The primary function of fuel markers and dyes is to facilitate the clear differentiation of various petroleum products, crucial for regulatory compliance, accurate tax collection, and preventing fuel fraud or diversion of subsidized fuels. They act as chemical fingerprints confirming the fuel's intended use and tax status.

Invisible chemical markers provide superior security because they are covert, requiring specialized laboratory or field spectroscopic equipment for detection, making them highly resistant to common chemical removal processes or attempts at masking by illicit blenders. Their proprietary nature ensures high authenticity.

The Diesel segment drives the highest demand globally due to its widespread use in commercial transportation, agriculture, and construction, where fuels are often subject to distinct and complex tax tiers (on-road vs. off-road) that necessitate robust, mandated marking protocols for enforcement.

Rising biofuel mandates necessitate the development of new marker chemistries that are fully compatible and stable within ethanol and biodiesel blends, without compromising engine performance or detectability. This drives R&D investment towards advanced, thermally stable marker formulations compatible with complex, oxygenated fuel matrices.

The Asia Pacific (APAC) region is projected to exhibit the highest growth in marker adoption. This is primarily fueled by rapid infrastructure growth, escalating energy consumption, and aggressive governmental initiatives to combat fuel fraud and protect extensive subsidy programs across large economies like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.