ID : MRU_ 436161 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

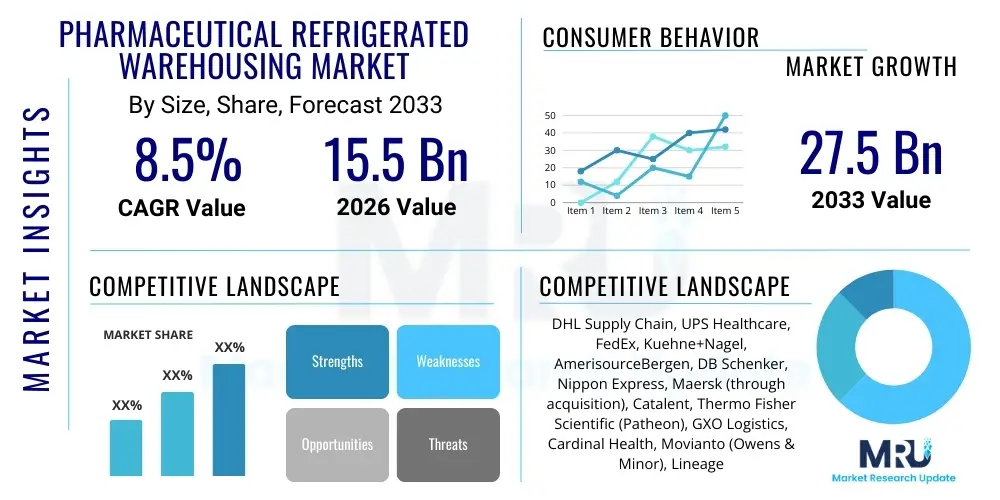

The Pharmaceutical Refrigerated Warehousing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 15.5 Billion in 2026 and is projected to reach USD 27.5 Billion by the end of the forecast period in 2033.

The Pharmaceutical Refrigerated Warehousing Market encompasses specialized logistics infrastructure designed to store temperature-sensitive pharmaceutical products, including vaccines, biologics, and specific therapeutic proteins, under strictly controlled climatic conditions, typically ranging from 2°C to 8°C (refrigerated) or below -20°C (frozen). This highly specialized sector is critical for maintaining the efficacy, safety, and regulatory compliance of temperature-sensitive pharmaceuticals throughout the supply chain. The core purpose is to mitigate risks associated with temperature excursions that could lead to product degradation, resulting in massive financial losses and significant public health hazards. Given the increasing complexity of modern drug pipelines, particularly the shift toward biologics and advanced therapy medicinal products (ATMPs), the demand for certified, state-of-the-art cold chain storage facilities is escalating globally. These facilities utilize advanced monitoring systems, robust backup power supplies, and strict Standard Operating Procedures (SOPs) to ensure continuous temperature integrity, satisfying stringent regulatory requirements from bodies like the FDA, EMA, and WHO.

The primary driving factors for this market are the rapid expansion of the biologics and biosimilars segments, which are inherently temperature-sensitive, coupled with mandatory global immunization programs requiring extensive cold storage networks. Furthermore, the global proliferation of sophisticated vaccines, evidenced prominently by the demand spike during recent public health crises, has necessitated massive investment in both established and emerging markets to bolster refrigerated warehousing capacity. The benefits derived from these specialized services include enhanced product shelf life, guaranteed compliance with Good Distribution Practice (GDP) guidelines, reduction in product waste, and assurance of patient safety through maintained drug efficacy. The operational landscape is characterized by high capital expenditure, stringent quality control measures, and the imperative for real-time visibility across the entire storage duration.

Major applications of pharmaceutical refrigerated warehousing span global distribution hubs, regional storage depots, and specialized facilities for clinical trial material management. Key players are investing heavily in automation and digital technologies, such as IoT-enabled temperature sensors and blockchain ledger systems, to enhance transparency and security within the cold chain. This market is intrinsically linked to global health trends and pharmaceutical R&D success, ensuring that high-value, temperature-critical medicines reach patients worldwide without compromise. The continuous regulatory pressure for end-to-end temperature traceability further solidifies the role of specialized refrigerated warehousing as an indispensable component of the modern pharmaceutical supply ecosystem.

The Pharmaceutical Refrigerated Warehousing Market is poised for robust expansion driven by structural shifts in the pharmaceutical pipeline toward temperature-sensitive biologics and advanced therapies, coupled with relentless regulatory demands for cold chain integrity. Business trends indicate significant consolidation among third-party logistics (3PL) providers specializing in cold chain, alongside substantial capital investment in developing smart warehouses featuring advanced automation like Automated Storage and Retrieval Systems (AS/RS) and specialized robotic handling designed for precise temperature environments. Key market participants are focusing on establishing comprehensive global networks, expanding cross-docking capabilities, and integrating sophisticated data analytics platforms to predict logistical bottlenecks and ensure proactive temperature management. Furthermore, sustainability is emerging as a critical trend, with providers adopting energy-efficient refrigeration technologies and aiming for green building certifications, balancing high energy consumption requirements with corporate environmental mandates.

Regionally, North America and Europe maintain dominance due to mature regulatory frameworks, high consumption of complex biologics, and established distribution infrastructures. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth, propelled by increasing healthcare expenditure, expanding pharmaceutical manufacturing bases (especially in China and India), and governmental initiatives to improve cold chain accessibility for massive immunization programs. Latin America and the Middle East & Africa (MEA) are seeing focused infrastructure development, often spurred by partnerships between global 3PLs and local logistics firms to address urbanization and expanding rural access needs. These emerging markets represent significant opportunity but also present unique challenges related to infrastructure reliability, customs complexity, and last-mile cold delivery integrity, necessitating tailored warehousing solutions.

Segment trends reveal that the storage of biological materials and vaccines remains the dominant application segment, though the demand for personalized medicine storage, requiring ultra-low temperature environments (e.g., -80°C), is witnessing accelerated growth. In terms of temperature range, the 2°C to 8°C segment holds the largest market share due to its requirement for standard vaccines and insulin; however, the ultra-low category is gaining prominence fueled by mRNA vaccine technology and cell and gene therapies. Third-Party Logistics (3PL) services are increasingly preferred over owned facilities, particularly by small to mid-sized biotech firms, due to the high operational costs and specialized expertise required for managing pharmaceutical cold storage, driving the service segment toward outsourcing models characterized by greater flexibility and scalability.

Users frequently inquire about how Artificial Intelligence (AI) can enhance the reliability, efficiency, and cost-effectiveness of cold chain logistics in pharmaceutical warehousing. Common questions revolve around AI’s capability in predictive maintenance for refrigeration equipment, optimizing inventory placement within temperature zones to minimize energy usage, and utilizing machine learning algorithms for demand forecasting, especially concerning volatile vaccine schedules. Concerns often center on the security of sensitive temperature data handled by AI systems and the initial integration complexity and high capital investment required to transition from traditional temperature monitoring to AI-driven predictive control. The overarching expectation is that AI will move the industry beyond reactive temperature control towards a highly optimized, preventative operational model, significantly reducing the risk of costly temperature excursions and improving overall supply chain resilience.

The Pharmaceutical Refrigerated Warehousing market is fundamentally driven by the escalating research and development focus on biologics, which require stringent temperature control, alongside increasingly strict global regulatory compliance mandates (GDP). Restraints primarily stem from the high capital expenditures required for constructing and validating specialized cold storage infrastructure, coupled with the substantial operational costs associated with maintaining ultra-low temperatures and managing complex, energy-intensive backup systems. Opportunities are centered on technological advancements, specifically the integration of IoT, blockchain, and automation for end-to-end traceability and operational efficiency, particularly in emerging markets where infrastructure investment is catching up. These forces collectively shape the market's trajectory; the stringent regulatory environment acts as a barrier to entry but simultaneously compels existing players to invest continuously in sophisticated, resilient infrastructure, thereby elevating service quality and reliability across the sector.

Driving factors are numerous and interconnected: the global aging population increases the demand for complex therapeutic agents, many of which are temperature-sensitive; the accelerated development and mass production of vaccines, particularly those requiring ultra-cold storage, fundamentally expands the need for specialized storage facilities; and continuous regulatory evolution mandates higher standards of validation, monitoring, and documentation, pushing warehousing providers toward specialized expertise and advanced systems. Furthermore, global supply chain risks and the imperative for quick disaster response necessitate geographically distributed and highly resilient cold storage hubs, driving market investment in redundant infrastructure and dual-source power capabilities to ensure uninterrupted service delivery even under extreme conditions. This environment rewards providers who can demonstrate not only capacity but also uncompromising quality management systems.

Restraints and challenges remain significant, including the volatile global energy prices that directly impact the high operational costs of maintaining cold environments, posing profitability challenges for providers, especially in competitive markets. Another major constraint is the scarcity of highly skilled labor necessary to operate and maintain sophisticated automated cold chain systems and manage complex regulatory filings; this talent gap can impede rapid market expansion. Opportunities lie predominantly in technological adoption, where utilizing advanced telematics, real-time monitoring, and predictive analytics offers avenues for differentiating service quality and optimizing energy consumption. The market impact forces dictate a trend toward specialization, where general warehousing is replaced by purpose-built facilities focused on specific temperature ranges and regulatory requirements, favoring large, well-capitalized logistics partners capable of absorbing high initial investment costs and navigating complex compliance landscapes globally. The growing preference for outsourced logistics management by pharmaceutical companies also strongly impacts market structure, favoring 3PLs.

The Pharmaceutical Refrigerated Warehousing market is primarily segmented based on the specific temperature range required for storage, the type of service offered (storage versus distribution), the products being stored, and the end-users utilizing these critical facilities. Analyzing these segments provides strategic insights into the specialized infrastructure investments and service customization required across different market verticals. The segmentation by temperature range highlights the technical complexity required for ultra-low environments compared to standard cold storage, while the product segmentation underscores the dominance of biologics and vaccines in driving current market demand. Understanding end-user preferences helps market players tailor their service offerings, ranging from bulk storage for manufacturers to specialized inventory management for hospitals and clinical research organizations. This granular analysis is crucial for capacity planning and optimizing cold chain networks globally.

The value chain for pharmaceutical refrigerated warehousing is highly integrated and commences with upstream activities focusing on the procurement of specialized equipment and technology. This involves sourcing high-efficiency, compliant refrigeration units, thermal insulation materials, advanced temperature monitoring systems (IoT sensors, data loggers), and robust backup power infrastructure necessary to maintain climate control integrity 24/7. Key upstream suppliers include manufacturers of specialized HVAC systems, validated packaging materials, and cold chain monitoring software developers. The operational core of the chain involves the warehousing and logistics providers (3PLs or in-house divisions) who manage storage, inventory control, and compliance documentation, representing the highest value-add segment due to the regulatory complexity and risk management required.

Midstream activities involve the primary operations of the warehouse, including receiving, quality inspection, precise temperature monitoring, efficient slotting, and secure storage according to GDP guidelines. Distribution channels are bifurcated into direct and indirect routes. Direct distribution involves shipments directly from the warehouse hub to major end-users such as large hospital networks or pharmaceutical wholesalers. Indirect distribution relies on an intricate network of specialized cold chain carriers (trucking, air cargo) that move products to regional distribution centers or smaller clinics and pharmacies, often involving multiple handoffs where temperature integrity must be meticulously maintained and documented using real-time GPS and temperature tracking devices.

The downstream segment concludes with the delivery of the temperature-sensitive products to the end-users—hospitals, pharmacies, and patients. Compliance and validation services are critical throughout the chain, ensuring that every transition point meets regulatory standards. The overall efficiency and reliability of the value chain are increasingly reliant on digital integration, allowing for immediate intervention in case of temperature deviation and providing comprehensive audit trails for regulatory bodies. The move towards outsourced logistics has elevated the strategic importance of 3PLs as critical nodes in this complex, high-stakes supply chain, requiring them to invest continually in advanced technology and specialized training to manage high-value pharmaceutical inventories effectively.

The primary customers for pharmaceutical refrigerated warehousing services are entities that manufacture, distribute, or utilize large volumes of temperature-sensitive biological and chemical compounds. Pharmaceutical and biotechnology companies constitute the largest customer segment, requiring bulk storage for newly manufactured drug batches, specialized environments for stability testing samples, and global distribution hubs for launching new products, particularly high-value monoclonal antibodies and proprietary biologics. These customers seek secure, compliant facilities that offer scalability and advanced inventory management systems to minimize waste and ensure product traceability from manufacturing plant to final market. Their requirements often include highly customized temperature profiles and the capability to handle stringent international export/import regulations for cold chain products.

A second major customer category includes Clinical Research Organizations (CROs) and academic research institutions involved in late-stage clinical trials. These organizations need specialized cold storage for clinical trial materials, patient samples, and investigational new drugs (INDs), often requiring ultra-low temperature storage (-80°C) and highly flexible, on-demand logistics services due to unpredictable trial timelines and global site distribution. The demand here focuses intensely on adherence to Good Clinical Practice (GCP) guidelines, ensuring sample integrity is maintained throughout the study duration, making reliability and validation paramount factors in provider selection.

Furthermore, government public health agencies, particularly those managing national immunization stockpiles and pandemic preparedness resources, represent crucial potential buyers. Their needs center around massive, long-term storage capacity for vaccines and essential biological response kits, often necessitating centralized storage points with exceptional disaster recovery protocols and highly secure premises. Retail pharmacy chains and large hospital systems are also significant end-users, requiring localized cold storage and just-in-time delivery services for inventory management of high-turnover refrigerated medicines like insulin and standard vaccines, preferring providers who can integrate seamlessly with their internal stock management software and ensure reliable, time-definite delivery schedules.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 27.5 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DHL Supply Chain, UPS Healthcare, FedEx, Kuehne+Nagel, AmerisourceBergen, DB Schenker, Nippon Express, Maersk (through acquisition), Catalent, Thermo Fisher Scientific (Patheon), GXO Logistics, Cardinal Health, Movianto (Owens & Minor), Lineage Logistics, Agility Logistics, CEVA Logistics, United Drug Distribution, World Courier, Marken (UPS subsidiary), Cryoport |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of pharmaceutical refrigerated warehousing is rapidly evolving, moving toward highly automated, data-driven systems designed to ensure maximum compliance and operational efficiency. Central to this transformation is the deployment of the Internet of Things (IoT), where wireless sensors and data loggers provide continuous, real-time monitoring of temperature, humidity, and pressure conditions within storage units and throughout transportation routes. This robust data stream is crucial for proactive risk management, allowing operators to detect minute temperature deviations instantly and trigger automatic corrective actions or alerts, satisfying the stringent regulatory requirements for comprehensive temperature mapping and excursion reporting. Furthermore, advanced Warehouse Management Systems (WMS) are specifically tailored for cold chain logistics, integrating complex slotting algorithms that consider both temperature zones and expiry dates, optimizing retrieval speed and minimizing manual intervention in sensitive environments.

Another pivotal technology is the adoption of Automated Storage and Retrieval Systems (AS/RS) and specialized robotics designed to operate efficiently within refrigerated and freezer environments, minimizing the need for human personnel exposure to extreme cold and significantly increasing throughput and inventory accuracy. These automation technologies ensure product stability is maintained during handling and reduce the potential for human error associated with manual retrieval processes. Additionally, blockchain technology is gaining traction, providing an immutable, distributed ledger for tracking the entire cold chain journey of high-value pharmaceuticals. This provides an unparalleled level of transparency and trust among stakeholders, enabling seamless verification of compliance and temperature history for regulatory audits and enhancing consumer confidence in drug integrity.

Finally, data analytics and cloud computing platforms are essential components, enabling warehouses to analyze massive datasets generated by IoT sensors and WMS systems. Predictive analytics, often powered by AI, allow facility managers to anticipate maintenance needs for refrigeration equipment, optimize energy consumption based on predictive weather patterns, and fine-tune inventory strategies according to real-time global demand fluctuations. The focus remains on creating a digital twin of the cold chain, allowing for simulation, optimization, and validation prior to execution, thereby establishing a resilient, highly compliant, and sustainable pharmaceutical storage environment that meets the future demands of complex biological product logistics.

The primary temperature ranges are refrigerated (2°C to 8°C) for most vaccines and insulin, frozen (-15°C to -25°C) for certain sensitive drugs, and ultra-low (-60°C to -80°C) and cryogenic (below -150°C) for advanced therapies like cell/gene products and specialized biological samples, each requiring distinct storage technology and validation.

Regulatory bodies such as the FDA and EMA enforce Good Distribution Practices (GDP) which mandate strict requirements for temperature monitoring, facility validation, documentation, and emergency protocols. These guidelines necessitate continuous investment in certified infrastructure and specialized training to maintain product efficacy and supply chain integrity.

IoT (Internet of Things) plays a critical role by providing real-time, continuous temperature and humidity data via wireless sensors. This data enables predictive maintenance, instantaneous alerts for temperature excursions, and creates comprehensive, tamper-proof audit trails essential for regulatory compliance and efficient risk management throughout the storage period.

The demand for ULT warehousing is surging due to the growing pipeline of advanced therapeutic products, including mRNA vaccines, cell and gene therapies (ATMPs), and complex biologics, which require storage below -60°C to preserve their molecular structure and therapeutic viability, driving infrastructure development in this niche segment.

Yes, outsourcing to specialized Third-Party Logistics (3PL) providers is increasingly common, particularly for small to mid-sized biotech and pharma companies. 3PLs offer the necessary scale, technical expertise, global network reach, and high compliance standards required for cold chain logistics without the prohibitive capital expenditure of building and managing proprietary facilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.