ID : MRU_ 433881 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

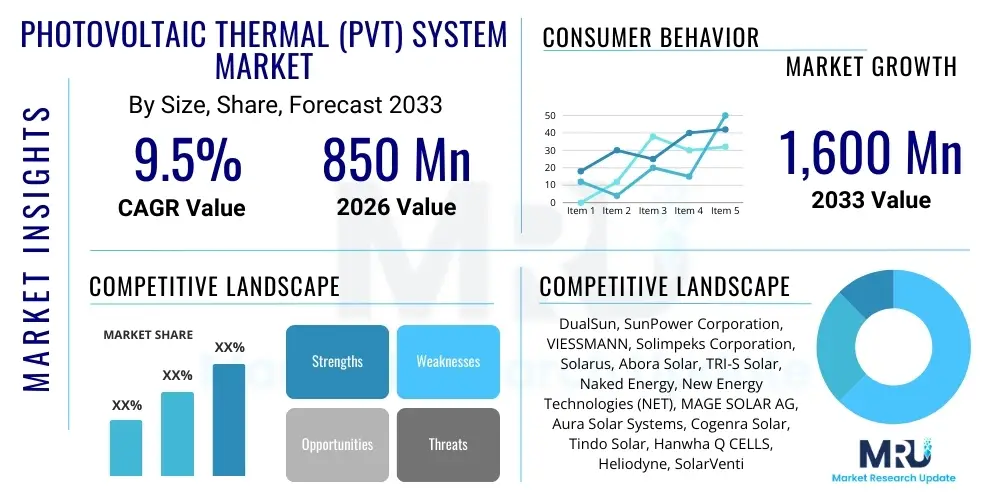

The Photovoltaic Thermal (PVT) System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 850 Million in 2026 and is projected to reach USD 1,600 Million by the end of the forecast period in 2033.

The Photovoltaic Thermal (PVT) System Market encompasses innovative technology that integrates conventional photovoltaic (PV) modules, designed to generate electricity, with thermal energy collectors, designed to generate heat. This synergy allows the system to produce both electrical and thermal energy from the same surface area, significantly increasing overall energy conversion efficiency compared to separate PV panels and solar thermal collectors. PVT systems are critical components in the global shift towards high-efficiency, multi-utility renewable energy sources, addressing the increasing demand for sustainable heating, cooling, and power generation solutions across various sectors.

Key applications of PVT systems span residential heating and domestic hot water supply, commercial building climate control, and industrial process heating. The unique benefit of PVT technology lies in its ability to simultaneously utilize incident solar radiation for dual energy output. Furthermore, by actively cooling the PV cells, thermal management improves the electrical efficiency of the PV component, as excessive heat is a primary factor degrading standard PV performance. This dual output capability positions PVT as a crucial enabler for Zero Energy Buildings (ZEBs) and decentralized energy production initiatives, promoting energy independence and reduced carbon footprints globally.

The primary driving factors accelerating market expansion include stringent government regulations promoting renewable energy adoption, escalating energy costs globally, and growing consumer awareness regarding the advantages of highly efficient, space-saving renewable systems. Technological advancements, particularly in collector design, fluid dynamics, and hybrid integration systems, are further enhancing the commercial viability and performance of PVT solutions. The market is also heavily influenced by subsidies and tax credits provided in key regions like Europe and North America to incentivize the installation of these highly efficient solar technologies.

The Photovoltaic Thermal (PVT) System market demonstrates robust expansion, underpinned by converging trends in energy efficiency and decarbonization. Business trends show a strong shift towards liquid-based PVT collectors due to their superior thermal transfer capabilities, driving innovation in heat exchange materials and design. Regionally, Europe currently dominates the market share, driven by ambitious renewable energy targets and established regulatory frameworks supporting high-efficiency building standards, particularly in Germany and Scandinavia. However, the Asia Pacific region, led by China and India, is projected to exhibit the highest growth rate, fueled by massive infrastructure development and urgent needs for sustainable power generation to meet rapid urbanization demands. Segmentation trends highlight the residential sector as the largest consumer segment, primarily using PVT for domestic hot water and space heating, while the industrial sector is increasingly adopting concentrating PVT (CPVT) solutions for process heat applications requiring higher temperatures.

Key strategic activities among market participants focus on vertical integration, enhancing manufacturing efficiencies, and forging strategic partnerships with HVAC providers and building developers to streamline installation and adoption. The competitive landscape is characterized by a mix of specialized PVT manufacturers and large diversified solar energy companies integrating PVT into their product portfolio. Financial performance of key players is increasingly tied to effective supply chain management, particularly regarding copper and aluminum component costs, and successful navigation of regional certification standards. Furthermore, the development of smart PVT systems integrated with AI-driven energy management platforms represents a crucial area for future investment and differentiation, promising optimized energy harvesting and distribution based on real-time climate and demand data.

Regulatory support remains pivotal to market success. Policies such as feed-in tariffs, renewable heat incentives, and performance-based grants significantly lower the initial investment barrier for end-users, accelerating market penetration. The inherent resilience and long operational lifespan of PVT systems contribute to a favorable total cost of ownership (TCO) calculation, making them increasingly attractive compared to separate PV and thermal installations. The market’s future trajectory is contingent upon continued material innovation, standardization of system integration protocols, and sustained governmental commitment to transitioning away from fossil fuel-based heating and cooling solutions.

User inquiries regarding the role of Artificial Intelligence (AI) in the PVT market predominantly center on system optimization, predictive maintenance, and smart grid integration. Common user concerns include how AI can manage the dual output (electricity and heat) effectively, ensuring optimal performance under varying weather conditions, and whether AI integration increases system complexity or cost. Expectations are high regarding AI’s capability to maximize energy yield, predict component failures, and seamlessly integrate PVT systems into broader smart home or smart grid ecosystems, ultimately making PVT systems more reliable, efficient, and user-friendly by automating complex control strategies.

AI algorithms are being deployed to dynamically adjust the flow rate of the thermal fluid, ensuring that the solar cells maintain their optimal operational temperature, thereby maximizing both electrical and thermal output throughout the day and across seasonal changes. Machine learning models use historical weather data, current irradiance levels, and internal temperature readings to predict future performance and preemptively adjust system parameters. This level of optimization drastically reduces energy wastage and increases the overall system Coefficient of Performance (COP). The implementation of digital twin technology, driven by AI, further aids in complex urban planning scenarios, simulating the integration of PVT arrays onto diverse building architectures to forecast optimal design specifications before physical installation.

Furthermore, AI facilitates advanced fault detection and diagnostics (FDD). By analyzing sensor data streams from pressure gauges, temperature probes, and power meters, AI can instantly detect anomalies indicative of potential issues like pump failure, leakage, or fouling in heat exchangers. This predictive capability shifts maintenance schedules from reactive to preventive, extending system lifespan and minimizing downtime, which is a major factor in improving the TCO for large-scale commercial and industrial PVT installations. The seamless integration of these systems into demand-side management programs via AI ensures that the energy generated aligns efficiently with fluctuating user demand and utility grid requirements.

The Photovoltaic Thermal (PVT) System market is propelled by key drivers such as escalating global commitments to renewable energy and significant improvements in energy conversion efficiency offered by hybrid systems. However, the market faces restraints, primarily high initial installation costs compared to conventional separate PV and thermal systems, and complexity in system integration and plumbing, requiring specialized labor. Opportunities are abundant, centered on expanding applications in industrial process heat, and developing low-cost, modular PVT collectors suitable for mass production and easier installation. The market is subject to intense impact forces from environmental regulations pushing for building energy efficiency and the sustained volatility of conventional energy prices, making PVT an increasingly cost-competitive long-term solution.

Drivers prominently include regulatory mandates, such as the EU’s Energy Performance of Buildings Directive (EPBD), which necessitate superior energy performance in new constructions and renovations, thereby favoring integrated, high-efficiency technologies like PVT. The technological driver stems from the recognized performance advantage: cooling the PV cells significantly boosts electrical output while simultaneously producing useful thermal energy. This combined efficiency addresses the critical need for space optimization in densely populated urban environments where roof space is limited. Furthermore, subsidies and fiscal incentives offered by governments globally act as a powerful accelerator, reducing the financial burden associated with the higher upfront capital expenditure of PVT systems.

Restraints are primarily focused on market penetration challenges. The lack of standardized installation procedures and the relatively high specialization required for maintenance currently limit widespread adoption, especially in emerging economies. Moreover, the long payback period for some commercial PVT installations, despite lower operational costs, can deter immediate investment decisions. Opportunities for market expansion exist in the development of lightweight, aesthetically pleasing PVT facade integration systems, opening up non-roof applications, and the strategic focus on concentrated PVT (CPVT) for industrial applications that require medium-to-high temperature thermal outputs (e.g., textile, food processing, and chemical industries). Impact forces, such as the ongoing global emphasis on sustainability and the fluctuating cost of natural gas, continuously enhance the value proposition of reliable, decentralized solar solutions.

The Photovoltaic Thermal (PVT) System market segmentation offers a detailed view of market structure based on technological configuration, application suitability, and geographical deployment. Primary segmentation revolves around the type of heat transfer medium (liquid or air), which significantly impacts the system’s design complexity and typical applications. Liquid-based systems are dominant, used extensively in residential and commercial settings for hot water, while air-based systems are often used for pre-heating ventilation air and space heating. Application segmentation reveals residential use as the foundational market, but commercial and industrial applications are exhibiting faster growth due to the scale and intensity of their heating and cooling demands.

Technology segmentation distinguishes between Flat Plate PVT and Concentrating PVT (CPVT). Flat Plate PVT systems are the most common due to their simplicity and ability to function effectively with diffuse radiation, making them ideal for standard building integration. Conversely, CPVT systems utilize optics to focus solar radiation, achieving much higher temperatures necessary for industrial processes or large-scale utility operations, although they require sun-tracking mechanisms. Geographic segmentation is crucial, with distinct regulatory environments and climate patterns dictating market dominance, highlighting Europe's technological leadership and Asia Pacific's massive volume potential.

Further analysis of the end-user base confirms that while residential uptake is driven by consumer desire for energy independence and lower utility bills, commercial segment growth is fueled by regulatory pressures (e.g., mandatory renewable energy deployment in new public buildings) and the need for significant operational cost reductions in large facilities like hospitals and hotels. This structural diversity necessitates highly customized product offerings and segmented marketing strategies by market players to address specific regional and application requirements effectively, driving continued product diversification across all major segments.

The value chain for the Photovoltaic Thermal (PVT) System market begins with upstream material suppliers, focusing on key components like silicon wafers for PV cells, specialized thermal absorber materials (e.g., copper, aluminum), heat transfer fluids (glycol or water mixtures), and high-grade glazing materials. Efficient sourcing and quality control at this stage are paramount, as material costs constitute a significant portion of the total system expenditure. Manufacturers then integrate these components, requiring specialized assembly processes that combine electrical wiring, fluid tubing, and insulation. The complexity of integrating these two distinct technologies demands high precision engineering and specialized manufacturing facilities capable of producing integrated hybrid collectors efficiently and at scale.

The midstream involves system integrators and distributors. Due to the hybrid nature of PVT, distribution channels often overlap between electrical component suppliers and HVAC specialists. Direct channels are prevalent for large commercial and utility projects, where manufacturers handle sales, design, and installation oversight directly to ensure optimal system performance and adherence to specifications. Indirect channels, utilizing specialized wholesalers and authorized dealers, dominate the residential segment, leveraging established networks of plumbers, electricians, and certified solar installers. Training and certification of these installation professionals are critical components of maintaining product quality and safety downstream.

Downstream activities center on installation, commissioning, operation, and maintenance (O&M). Unlike standard PV panels, PVT systems require expertise in both electrical and hydraulic systems, elevating the complexity and cost of installation. End-users receive support through long-term performance monitoring services, often facilitated by IoT sensors and remote diagnostic platforms. The effective management of the thermal fluid, pump functionality, and heat exchanger efficiency are primary focuses of O&M. Strong partnerships with local installation firms and sustained efforts in professional training are essential for manufacturers to reduce installation risks and ensure customer satisfaction, thereby strengthening the overall value chain and fostering long-term market growth.

The primary customers for Photovoltaic Thermal (PVT) systems are highly diverse, spanning residential, commercial, and industrial sectors, all unified by the objective of reducing energy expenditures and enhancing sustainability profiles. Residential homeowners, particularly those in high-cost energy regions or those building custom, energy-efficient homes, represent a critical segment, valuing PVT’s ability to provide both electricity and abundant hot water using minimal roof space. This customer group is primarily interested in return on investment (ROI) through utility bill savings and governmental incentives, often favoring simpler, liquid-based flat plate systems.

The commercial sector constitutes a rapidly expanding customer base, encompassing institutions such as hotels, hospitals, universities, and large office complexes, all of which have substantial, simultaneous demands for electricity (lighting, IT infrastructure) and thermal energy (hot water for sanitation, space heating/cooling). These commercial entities seek high-efficiency solutions that comply with corporate sustainability mandates and reduce large operational overheads. The decision-making process here involves facilities managers and CFOs, who prioritize long-term reliability, low maintenance, and scalability of the PVT deployment.

Industrial users, particularly those requiring medium-to-high temperature process heat (e.g., food processing, brewing, chemical manufacturing), are emerging as major potential buyers, especially for Concentrating PVT (CPVT) technology. For these customers, PVT systems offer a clean, stable source of thermal energy that can replace fossil fuels in specific manufacturing steps. Utility-scale customers, including municipalities developing district heating and cooling networks, represent a highly strategic segment, utilizing large arrays of PVT collectors to provide centralized, efficient thermal energy distribution to entire urban zones, driven by city-level decarbonization targets and energy security considerations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1,600 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DualSun, SunPower Corporation, VIESSMANN, Solimpeks Corporation, Solarus, Abora Solar, TRI-S Solar, Naked Energy, New Energy Technologies (NET), MAGE SOLAR AG, Aura Solar Systems, Cogenra Solar, Tindo Solar, Hanwha Q CELLS, Heliodyne, SolarVenti, Sunroof, SolaX Power, PV-T.eu. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Photovoltaic Thermal (PVT) market is characterized by ongoing innovation aimed at improving thermal extraction efficiency, reducing heat losses, and enhancing system aesthetics for better building integration. A central focus is on optimizing the absorber design, moving beyond simple copper tubes to microchannel heat exchangers and advanced fluid dynamics that maximize contact between the thermal fluid and the photovoltaic cells. Modern PVT systems utilize specialized selective coatings on the absorber plate to maximize solar absorption while minimizing thermal re-radiation, thereby increasing the useful heat collected. Furthermore, advances in insulation materials, particularly vacuum insulation panels (VIPs), are being incorporated into glazed PVT collectors to drastically reduce heat loss, making them effective even in colder climates or high-temperature applications.

Another significant area of development is the integration of advanced control systems. These electronic controllers, often utilizing microprocessors and sophisticated sensors, manage the synchronization of electricity generation and heat extraction. Modern controllers employ variable speed pumps and advanced algorithms to prioritize either electrical or thermal output based on real-time household or facility demand, meteorological data, and energy storage levels. This "smart" control capability is crucial for maximizing the economic returns of the system. In the concentrating PVT (CPVT) segment, the technology focuses on high-precision optics (mirrors or lenses) and effective tracking systems to concentrate sunlight onto small, high-efficiency multijunction PV cells, while the excess heat is simultaneously captured for thermal output, pushing the envelope of total energy conversion efficiency above 80%.

Moreover, Building Integrated Photovoltaic Thermal (BIPV/T) systems represent a growing technological segment, where the PVT collector serves not only as an energy generator but also as an integral part of the building envelope (e.g., facade, roofing material). This blending of functions offers aesthetic appeal and reduces material costs associated with traditional mounting systems. Material science breakthroughs are introducing lighter, more durable polymers and composite materials for collector construction, reducing weight and simplifying installation. The adoption of Phase Change Materials (PCMs) for integrated thermal energy storage within the PVT panel is also a burgeoning technology, allowing for delayed use of thermal energy, further enhancing the system's overall utility and matching supply more closely with peak demand periods.

Geographically, the Photovoltaic Thermal (PVT) System Market exhibits highly segmented growth patterns driven by regional climate conditions, energy policies, and construction industry maturity. Europe maintains a leading position, anchored by stringent regulatory frameworks promoting energy efficiency in buildings (e.g., nearly Zero Energy Buildings mandates) and substantial government subsidies for renewable heating solutions in countries like Germany, Austria, and the Netherlands. The region benefits from established supply chains and high awareness among consumers and developers regarding hybrid solar technologies, focusing heavily on residential and commercial building applications.

The Asia Pacific (APAC) region is projected to register the fastest growth rate during the forecast period. This rapid expansion is primarily attributable to massive infrastructure investments in China and India, coupled with critical public policy initiatives aimed at combating air pollution and enhancing rural electrification. Although current adoption levels are lower than in Europe, the sheer scale of energy demand and the push for decentralized renewable solutions present enormous market potential, particularly in urban residential complexes and new industrial zones seeking stable, clean energy inputs. Japan and South Korea also contribute significantly, focusing on technological leadership and high-efficiency product deployment.

North America, led by the US and Canada, represents a mature market with high growth potential, driven by state-level incentives (especially in California and Northeastern states) and increasing consumer interest in energy resilience. The focus in North America is shifting toward high-performance PVT systems that can efficiently handle extreme temperature variations common across the continent. Meanwhile, Latin America and the Middle East & Africa (MEA) are emerging regions. MEA holds long-term promise due to high solar irradiance levels, although market penetration is currently hampered by lack of robust government incentives and infrastructural constraints. Adoption in these regions is typically restricted to high-end commercial projects, specialized agriculture, and remote power generation applications.

The primary advantage of a PVT system is its superior overall energy conversion efficiency, often exceeding 80%, compared to conventional systems. It generates both electricity and thermal energy from the same footprint, saving significant space and improving electrical output by actively cooling the PV cells, which otherwise lose efficiency due to heat.

While the initial cost of PVT systems is generally higher than separate PV installations, they are cost-effective in the long term, particularly in regions with high energy costs or strong governmental renewable heating incentives. The dual output reduces reliance on conventional heating sources, leading to a favorable total cost of ownership and accelerated payback period.

Concentrating PVT (CPVT) technology is best suited for applications requiring medium to high-temperature thermal energy (above 80 degrees Celsius), such as industrial process heat in manufacturing, large-scale district heating networks, or commercial cooling systems (solar thermal cooling).

PVT systems perform effectively across diverse climates. In cold climates, high-efficiency glazed PVT collectors with superior insulation minimize heat loss. In hot climates, the active cooling of the PV cells by the thermal fluid ensures that the electrical output remains high, preventing the efficiency drop experienced by standard PV panels.

Future growth in the PVT market is primarily driven by the Commercial segment (hotels, hospitals) due to large and simultaneous energy needs, and the Industrial segment, where CPVT solutions are increasingly adopted for sustainable process heat, alongside continuous strong residential demand for integrated energy solutions.