ID : MRU_ 434175 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

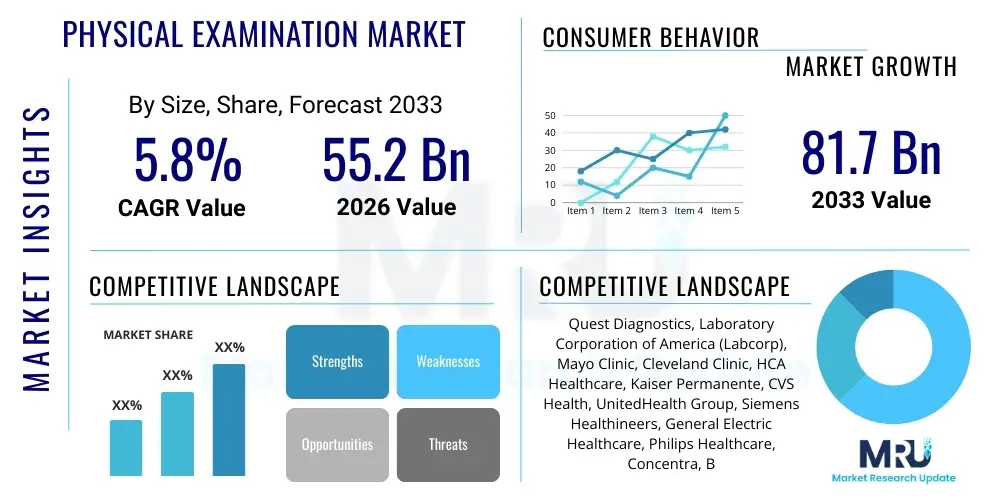

The Physical Examination Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $55.2 Billion in 2026 and is projected to reach $81.7 Billion by the end of the forecast period in 2033.

The Physical Examination Market encompasses the provision of comprehensive health assessments, ranging from routine annual check-ups and wellness visits to specialized pre-operative or employment-mandated screenings. These examinations are fundamental pillars of modern preventive healthcare, aiming to detect underlying health issues early, manage chronic conditions, and promote overall wellness. The scope of products and services includes basic vital sign measurements, physical inspections, detailed medical history reviews, and often supplementary laboratory and diagnostic tests, all performed by qualified healthcare professionals such as physicians, physician assistants, and nurses. The growing societal emphasis on proactive health maintenance, coupled with rising incidence rates of lifestyle diseases, substantially drives the demand for these formalized assessment services globally.

Major applications of physical examinations span across diverse sectors, including corporate wellness programs focused on employee health, regulatory compliance checks required for specific industries like aviation or heavy machinery operation, and personalized medicine strategies where baseline health data is essential for tailored treatments. The inherent benefits include reduced healthcare costs over the long term due to early disease interception, improved quality of life for patients through timely intervention, and enhanced public health surveillance through widespread data collection. These examinations serve as crucial touchpoints in the patient journey, solidifying the relationship between patients and primary care providers and facilitating informed clinical decision-making based on objective and subjective health indicators.

The market is increasingly influenced by technological integration, particularly the adoption of portable diagnostic tools and electronic health records (EHRs) which streamline the examination process and improve data accuracy. Key driving factors include increasing government initiatives promoting preventive healthcare screenings, the aging global population requiring more frequent and complex assessments, and expanding health insurance coverage that often mandates or incentivizes periodic physicals. Furthermore, the shift towards value-based care models encourages providers to prioritize comprehensive, preventive services like physical examinations to achieve better patient outcomes and lower systemic costs, reinforcing the market’s positive trajectory.

The Physical Examination Market is poised for robust expansion, driven primarily by evolving business trends centered on digitization and decentralization of healthcare delivery. Key business trends include the proliferation of retail health clinics and urgent care centers, which offer accessible and convenient alternatives to traditional hospital settings for routine physicals. Furthermore, corporate contracts for large-scale employee health screenings represent a significant revenue stream, pushing providers to offer scalable, efficient, and standardized examination packages. Investment in interoperable electronic medical records (EMR) systems is crucial, ensuring seamless data transfer and continuity of care across various providers and facilitating predictive analytics based on aggregated physical health data.

Regional trends indicate North America currently dominating the market, underpinned by stringent corporate regulatory requirements, high awareness regarding preventive medicine, and extensive insurance coverage for annual physicals. However, the Asia Pacific region is projected to exhibit the highest growth rate, fueled by rapidly expanding healthcare infrastructure, rising disposable incomes, and government campaigns addressing endemic and lifestyle-related diseases through mass screening programs. Europe maintains a strong presence due to established universal healthcare systems that prioritize primary and preventive care, though growth might be comparatively slower than APAC due to market saturation and regulatory complexities regarding data privacy (GDPR) impacting cross-border health data utilization.

Segmentation trends highlight the increasing demand for Specialized Physical Examinations, particularly those tailored for athletes, occupational exposure, or pre-surgical risk assessments, which command higher average procedure costs. The Service Provider segment is witnessing a noticeable shift towards Diagnostic Labs and Corporate Clinics, as these entities offer faster turnaround times and focused services, contrasting with the broader scope and potential waiting times associated with traditional hospitals. Technology integration, such as the use of tele-triage tools before an in-person physical, is also influencing how consumers access and perceive the value of these necessary health assessments, leading to more efficient utilization of healthcare resources.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Physical Examination Market predominantly revolve around three critical themes: efficiency enhancement, diagnostic accuracy improvement, and the potential displacement of human examiners. Common questions focus on how AI can automate routine data collection (e.g., AI-powered vital sign monitoring or automated medical history intake), whether AI algorithms can predict disease risk more accurately than traditional physician assessments based on physical cues, and the ethical/regulatory challenges associated with integrating AI into established clinical workflows. Users seek clarification on the role of AI—will it supplement or supplant the physician's hands-on role in a comprehensive physical assessment? There is high expectation for AI to transform the administrative burden and enhance the subjective parts of the physical exam by providing objective, quantitative data analysis.

AI's primary influence is manifesting in the augmentation of diagnostic capabilities, shifting the physical examination from a largely qualitative assessment to a data-intensive, quantitative process. Machine learning models are increasingly deployed to analyze imaging data (e.g., skin lesions, retinal scans) collected during a physical, identify anomalies in heart sounds captured by smart stethoscopes, or analyze gait and posture changes indicative of neurological issues. This integration allows primary care providers to leverage advanced diagnostic support tools instantly, leading to faster, more precise identification of potential health risks that might be subtle or missed during a traditional subjective examination. However, the requirement for human oversight remains paramount, ensuring that AI recommendations are clinically contextualized and ethically applied to patient care.

The long-term impact involves the standardization and personalization of physical examinations. AI tools help standardize the data capture process across different clinics and providers, reducing inter-examiner variability—a historical challenge in physical assessment. Simultaneously, AI facilitates personalized risk stratification by correlating examination findings with vast datasets of patient histories and genomic information, moving beyond a one-size-fits-all annual check-up to a dynamic, risk-adjusted screening schedule. This evolution promises to optimize the frequency and scope of physical assessments, dedicating more intensive resources to high-risk individuals while simplifying the process for those with low predicted health risks, thereby improving resource allocation within the healthcare system.

The Physical Examination Market is driven by the imperative to shift from reactive disease management to proactive health maintenance, catalyzed by global demographic shifts and increasing chronic disease prevalence. Key drivers include government and organizational initiatives mandating or heavily subsidizing preventive health screenings, recognition of the cost-effectiveness of early intervention, and rising consumer health literacy which encourages regular check-ups. Restraints include the significant cost associated with comprehensive physicals, especially when advanced diagnostics are involved, coupled with inconsistent reimbursement policies across different healthcare systems and payor classes. Furthermore, patient reluctance due to time constraints or perceived inconvenience presents a persistent barrier to widespread annual attendance. The primary opportunity lies in the integration of innovative technologies, specifically telehealth and AI-driven remote monitoring, which promise to lower operational costs and improve patient accessibility.

The core Impact Forces shaping this market are regulatory mandates, technological innovation, and changing consumer behavior. Regulatory bodies often dictate the frequency and scope of physicals in occupational health settings (e.g., commercial drivers, pilots), providing a baseline demand floor. Technological advancements, particularly in point-of-care diagnostics and miniaturized sensors, allow for faster, less invasive, and more information-rich examinations performed in non-traditional settings. Shifts in consumer behavior, influenced by digital health platforms and personalized wellness trends, drive demand for holistic assessments that extend beyond basic clinical parameters to include lifestyle and nutritional evaluations. The convergence of these forces dictates market evolution, forcing traditional providers to innovate or risk losing market share to agile, technology-focused health service companies.

Specific challenges related to the COVID-19 pandemic highlighted the necessity for hybrid examination models, blending virtual consultations with essential in-person assessments, accelerating the adoption of new protocols. Market participants must navigate the ethical deployment of AI tools, ensuring diagnostic accuracy while maintaining patient data privacy (Restraint). Opportunities are abundant in underdeveloped and developing markets where healthcare infrastructure is rapidly expanding, offering greenfield sites for implementing efficient, digitized examination protocols, especially through public-private partnerships aimed at mass population screening. Success in this complex landscape requires a strategic balance between maintaining high clinical standards, achieving cost efficiency, and adapting services to meet the evolving convenience demands of the modern patient.

The Physical Examination Market is segmented based on the type of examination, the service provider delivering the assessment, and the primary application or purpose of the examination. This detailed segmentation allows stakeholders to target specific consumer groups and develop tailored service offerings, ranging from high-volume, standardized screenings to complex, personalized diagnostic procedures. The structural breakdown reflects the diversity of clinical needs and the various organizational models involved in the delivery of preventive and mandatory health assessments. Understanding these segments is crucial for accurate market forecasting and strategic planning, particularly concerning resource allocation and technological investment across the healthcare continuum.

Segmentation by Type reveals distinct requirements and utilization patterns. Annual Physical Examinations represent the largest and most frequent segment, driven by insurance incentives and standard health maintenance recommendations. Pre-employment and Occupational Health Examinations are governed by specific regulatory requirements and industry standards, demanding specialized assessments tailored to job function and risk exposure. Specialized Examinations, such as those focusing on sports fitness, immigration, or geriatric care, often involve a multidisciplinary approach and utilize advanced diagnostic technologies, reflecting the high value placed on targeted clinical depth and precision in these niche areas.

The breakdown of Service Providers demonstrates the shift towards decentralized care. While Hospitals and Clinics remain foundational, Diagnostic Laboratories and specialized Corporate/Wellness Clinics are capturing significant growth, capitalizing on their ability to offer efficient, focused, and timely services. Application segmentation underscores the market's primary mission: Preventive Screening focuses on the asymptomatic population, Chronic Disease Management uses physicals as a monitoring and adjustment tool, and Regulatory Compliance provides the mandatory assessments required by governmental or industry bodies, ensuring broad market coverage across distinct consumer motivations.

The value chain for the Physical Examination Market begins with upstream activities focused on the procurement of essential medical supplies, diagnostic equipment, and technology infrastructure. This stage involves manufacturers of medical devices (stethoscopes, sphygmomanometers, EHR systems, lab analyzers) and pharmaceutical companies providing necessary vaccines or testing materials. Effective upstream management requires robust supplier relationships to ensure the availability of high-quality, certified medical technology, increasingly focused on smart, connected devices that enhance data acquisition during the examination process. Procurement efficiency directly impacts the operational cost structure of downstream providers, setting the foundation for service delivery.

Midstream processes center on the operational delivery of the physical examination service itself. This includes the recruitment and training of qualified personnel (physicians, nurses, technicians), facility management (hospitals, clinics, mobile units), and the integration of IT systems for patient scheduling, data collection, and billing. Distribution channels are varied, spanning Direct Channels (patients booking appointments directly with hospitals or primary care providers) and Indirect Channels (corporate entities contracting third-party administrators or wellness providers for employee physicals, or insurance companies directing patients to preferred provider networks). The efficiency of scheduling and the quality of the patient experience are crucial determinants of value at this stage.

Downstream activities focus on post-examination services, including the analysis and interpretation of test results, patient follow-up, referral to specialists if necessary, and data archiving. This stage relies heavily on robust EHR systems for secure data transmission and longitudinal tracking of patient health metrics. Value is realized when the physical examination translates into actionable clinical outcomes, prompting positive behavioral changes or timely medical intervention. Feedback mechanisms from payors and patients further refine the upstream and midstream components, ensuring the delivered service remains clinically relevant, cost-effective, and aligned with preventive health goals.

The potential customer base for the Physical Examination Market is extremely diverse, fundamentally encompassing any individual or organization requiring an assessment of health status for personal, occupational, or regulatory reasons. The primary end-users are individual consumers, particularly those covered by insurance plans that mandate or incentivize annual check-ups. This group is increasingly motivated by wellness trends and a desire for proactive disease prevention, seeking comprehensive reports that detail biometric data, risk factors, and personalized lifestyle recommendations. Demographic factors such as age significantly influence utilization, with pediatric and geriatric populations requiring specialized, frequent physical assessments.

Institutional customers represent another critical segment. This includes large corporations and small and medium enterprises (SMEs) that utilize physical examinations for employee screening (pre-employment, annual wellness programs, occupational exposure monitoring) aimed at minimizing workplace risk and optimizing productivity. Government agencies, particularly those overseeing sectors like transportation, military, and public safety, are mandatory buyers of specialized physical assessments to ensure personnel meet rigorous fitness standards. Educational institutions and universities also require health clearances for students and staff, especially those involved in contact sports or healthcare fields.

A growing segment includes insurance companies and healthcare payors. While not direct consumers of the examination service itself, they are critical financial stakeholders who purchase these services indirectly on behalf of their members, influencing customer choice through network inclusion and reimbursement policies. Furthermore, international travel and immigration services constitute a specialized customer base, where mandatory physicals are required to meet border control health standards, driving demand for internationally recognized certifications and specialized testing protocols.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $55.2 Billion |

| Market Forecast in 2033 | $81.7 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Quest Diagnostics, Laboratory Corporation of America (Labcorp), Mayo Clinic, Cleveland Clinic, HCA Healthcare, Kaiser Permanente, CVS Health, UnitedHealth Group, Siemens Healthineers, General Electric Healthcare, Philips Healthcare, Concentra, Bupa, Cigna, Intermountain Healthcare, Mount Sinai Health System, Tenet Healthcare, Baylor Scott & White Health, Sutter Health, Northwell Health |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Physical Examination Market is rapidly transitioning from reliance on basic analog instruments to advanced digital, connected, and often AI-enabled solutions. Key technologies involve Electronic Health Records (EHR) and Electronic Medical Records (EMR) systems, which serve as the foundational digital backbone for collecting, storing, and retrieving comprehensive patient data generated during the physical assessment. The move towards interoperable EHRs is crucial for providing longitudinal health data analysis and ensuring that past examination results are seamlessly accessible to providers across different systems, enhancing the diagnostic value of the current physical assessment. Furthermore, secure cloud-based data storage and transmission protocols are vital for complying with increasingly strict global health data privacy regulations such as HIPAA and GDPR, necessitating significant investment in cybersecurity measures.

Advancements in diagnostic instrumentation constitute another core technological shift. Miniaturized and portable point-of-care (POC) diagnostic devices allow for rapid on-site blood work, urinalysis, and vital sign monitoring, shortening the time required for a comprehensive physical and accelerating clinical decision-making. High-fidelity digital imaging technologies, including portable ultrasound and digital stethoscopes, are replacing traditional instruments, offering objective data capture that can be analyzed by machine learning algorithms for enhanced detection of subtle abnormalities. The integration of biosensors and wearable technology is increasingly commonplace, allowing for passive, continuous monitoring of physiological parameters like heart rate variability, sleep quality, and activity levels, providing a more holistic picture of the patient's health status leading up to and after the formal examination.

Finally, the growing adoption of Telehealth and virtual examination platforms is fundamentally reshaping access and delivery. These platforms utilize specialized remote examination kits, often equipped with connected otoscopes, dermatoscopes, and high-resolution cameras, enabling physicians to conduct crucial parts of the physical exam remotely with objective measurements. AI-powered clinical decision support tools are overlaid onto this data, providing automated risk assessment and flagging potential concerns based on deviations from baseline measurements. This technological convergence increases efficiency, expands geographical reach, and supports the trend towards hybrid care models where the physical exam can be partially virtualized and highly data-driven, optimizing the use of valuable physician time for complex diagnostic interpretation rather than routine data capture.

The primary drivers are the rising global burden of chronic diseases (like diabetes and cardiovascular conditions), escalating corporate and government focus on occupational health and safety compliance, and insurer requirements emphasizing preventive care to mitigate future high-cost treatments. Early detection through mandatory physicals is proven to improve long-term public health outcomes.

Telehealth integration is transforming physical examinations by enabling hybrid models. Routine consultations and medical history reviews are often conducted virtually, reserving in-person visits for hands-on assessments or specialized diagnostic tests. This reduces clinic wait times, improves geographic access, and makes the overall process more efficient for both patient and provider.

The Specialized Physical Examinations segment is anticipated to exhibit the fastest growth, particularly those related to chronic disease monitoring and geriatric care. Furthermore, the Service Provider segment represented by Corporate Wellness Centers and Retail Clinics is expected to expand rapidly due to their convenience and tailored, high-volume service delivery models.

Key technological challenges include ensuring interoperability between diverse Electronic Health Records (EHR) systems used by different providers, overcoming cybersecurity risks associated with handling highly sensitive patient data, and accurately validating AI-driven diagnostic tools to ensure they maintain clinical reliability and regulatory compliance across varied populations.

Health insurance coverage is a critical determinant of examination frequency. Policies that fully cover or heavily subsidize annual preventive physicals significantly increase patient attendance and compliance. Conversely, high deductibles or limited coverage can act as a substantial restraint, causing many individuals to postpone routine check-ups until symptoms manifest.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.