ID : MRU_ 432818 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

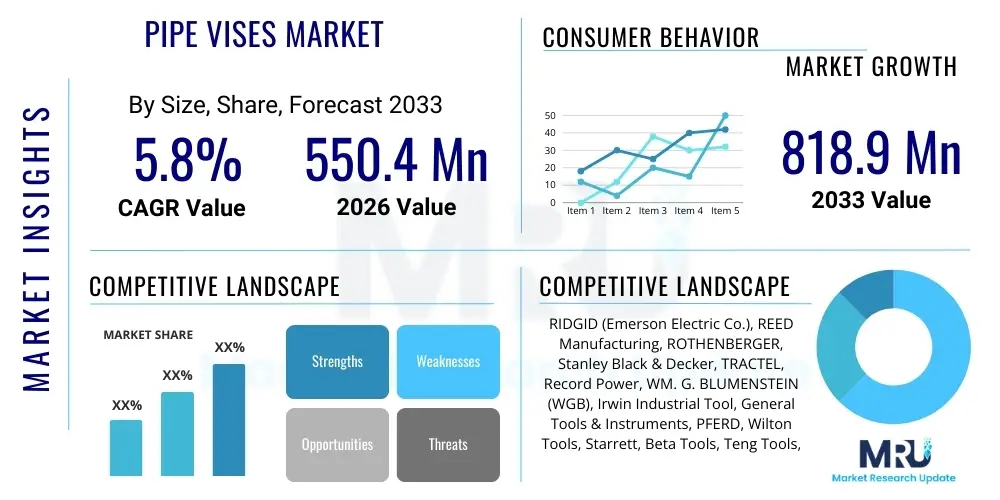

The Pipe Vises Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 550.4 Million in 2026 and is projected to reach USD 818.9 Million by the end of the forecast period in 2033.

The Pipe Vises Market encompasses the manufacturing, distribution, and sale of specialized clamping tools designed to securely hold piping materials, cylindrical rods, and tubing during cutting, threading, welding, or assembly operations. These tools are fundamental components across numerous industrial and commercial sectors, acting as essential anchors for maintaining alignment and stability, thereby ensuring the precision and safety of pipe manipulation tasks. Pipe vises are indispensable in demanding environments such as oil and gas pipeline construction, municipal water and sewage infrastructure projects, industrial plant maintenance, and large-scale commercial and residential plumbing installations. The efficacy of a pipe vise directly influences the quality of the final piping system, necessitating robust design, durable materials, and reliable gripping mechanisms to accommodate various pipe sizes and material compositions, including steel, PVC, copper, and specialized alloys. Market growth is closely correlated with global investment cycles in infrastructure development and the increasing complexity of modern fluid conveyance systems, demanding ever more precise and efficient tooling solutions for on-site operations and fabrication shops globally.

The product scope of the Pipe Vises market is broadly segmented into several categories based on design and application, primarily Chain Pipe Vises and Yoke Pipe Vises, alongside specialized bench mounts and portable tripod models. Chain pipe vises utilize a robust chain mechanism wrapped around the pipe, secured by a gripping jaw, offering excellent versatility for irregularly shaped objects and large-diameter pipes, making them a staple in heavy industrial settings. Conversely, Yoke pipe vises employ an adjustable screw clamp and a hinged jaw assembly to secure the pipe rigidly, generally favored for smaller to medium-sized pipes where precision threading is paramount. The major applications span critical sectors, including the energy industry (onshore and offshore drilling), public utility maintenance (gas and water distribution networks), Heating, Ventilation, and Air Conditioning (HVAC) system installations, and petrochemical processing facilities. The core benefits derived from using specialized pipe vises include enhanced operational safety by preventing pipe slippage, significant improvement in threading accuracy, increased productivity through faster material handling, and the ability to perform complex modifications directly at the installation point, reducing the need for prefabricated components.

Driving factors propelling the expansion of the Pipe Vises Market include the sustained global push towards modernizing aging infrastructure, particularly in established economies across North America and Europe, which necessitates extensive repair and replacement work on utility pipelines. Simultaneously, rapid urbanization and industrialization across emerging economies in the Asia Pacific region are generating massive demand for new water supply networks, gas pipelines, and industrial complexes, directly fueling tool procurement. Furthermore, the recovery and stabilization of crude oil and natural gas prices globally have stimulated capital expenditure in the energy sector, leading to increased pipeline construction and maintenance activities that require specialized, high-capacity pipe vises. Technological advancements focused on ergonomics, lighter materials such as aluminum alloys for portable tripod bases, and quick-release mechanisms are making modern pipe vises more efficient and user-friendly, contributing significantly to their adoption rate among professional contractors and maintenance crews who prioritize portability without compromising clamping strength. The convergence of infrastructure spending and efficiency demands forms a solid foundation for market expansion throughout the forecast period.

The Pipe Vises Market is undergoing a transformation driven by global infrastructure investment cycles, technological advancements in material science, and a strong emphasis on worker safety and ergonomic design. Key business trends indicate a palpable shift toward lightweight, portable vise models, particularly tripod vises manufactured from high-strength aluminum alloys, catering to the mobility requirements of modern contracting firms that operate across diverse job sites. There is a noticeable consolidation among leading tool manufacturers who are expanding their product portfolios to offer integrated solutions, pairing vises with complementary tools like specialized cutters and threaders to enhance user convenience and system compatibility. Furthermore, the rising adoption of IoT-enabled job site management systems is indirectly influencing the demand for durable, standardized tools capable of withstanding prolonged and rigorous field conditions, pushing manufacturers to improve the longevity and corrosion resistance of their products, particularly the gripping components and mounting systems, leading to higher average selling prices for premium models and sustained revenue growth.

Regionally, the market exhibits a dichotomy: North America and Europe represent mature markets characterized by replacement demand and a strong preference for high-quality, specialized products adhering to stringent safety certifications, providing stability and steady revenue streams. Conversely, the Asia Pacific (APAC) region is forecasted to demonstrate the fastest growth rate, fueled by massive government investments in smart city development, expansion of municipal utilities, and significant construction projects in countries like China, India, and Southeast Asia. The regional trends in APAC favor volume production and competitive pricing, though there is a growing segment demanding professional-grade tools for highly specialized projects, driving localized manufacturing and distribution efforts. The Middle East and Africa (MEA) market growth remains robust, primarily anchored by large-scale oil and gas pipeline projects, demanding heavy-duty, corrosion-resistant, high-capacity yoke and chain vises suitable for harsh desert or offshore environments, contributing to high average transaction values within this specific geographical cluster.

Segmentation trends reveal that the Yoke Pipe Vise segment maintains a dominant market share due to its superior precision and ease of use in common plumbing and HVAC tasks, particularly those involving smaller to medium diameter pipes requiring accurate threading. However, the Chain Pipe Vise segment is anticipated to witness faster revenue growth, driven by escalating activities in large diameter pipeline construction and maintenance, especially within the energy and utility sectors, where their versatility and capacity are unmatched. The application segment analysis highlights Industrial Use (including manufacturing and heavy engineering) as the largest consumer, but Commercial/Residential Construction is expanding rapidly due to housing booms in key global urban centers. Manufacturers are increasingly focusing on developing modular vise systems that can adapt to both bench mounting and tripod setups, offering increased flexibility to end-users and capturing a broader share of the diverse market segments by providing customizable solutions to varying operational demands.

Analysis of common user questions related to AI's impact on the Pipe Vises Market reveals key themes revolving around supply chain resilience, predictive tool failure, and the optimization of construction scheduling. Users often query how Artificial Intelligence and Machine Learning (ML) can predict optimal tool replacement cycles, given the intense wear and tear these tools endure on site. There is also significant interest in using AI-driven systems to manage inventory levels of consumable vise components (like jaw inserts or chains) across geographically dispersed construction projects, minimizing downtime associated with equipment failure or non-availability. Furthermore, advanced users in large engineering procurement and construction (EPC) firms frequently ask about the potential for AI to optimize the design phase of custom vises for niche applications involving non-standard materials or extremely high-pressure piping systems, aiming for enhanced safety margins and reduced manufacturing costs through simulation and generative design techniques applied to clamping geometries and stress points.

While pipe vises themselves are mechanical, non-electronic tools, the integration of AI influences the upstream manufacturing process and downstream logistics/usage context. In manufacturing, AI is revolutionizing quality control by utilizing computer vision systems to inspect the precision of casting and machining processes, ensuring that the gripping surfaces and thread mechanisms of the vises adhere strictly to extremely tight tolerances, drastically reducing the occurrence of defective units reaching the market. Moreover, ML algorithms are deployed in raw material procurement to forecast price volatility and manage inventory, optimizing the cost structure for manufacturers dealing with specialty steel and cast iron. This AI-driven optimization in the upstream segment ensures more stable pricing and supply chain reliability for end-users. The secondary impact involves integrating these mechanical tools into smart construction environments where sensors track tool utilization rates and performance metrics, feeding data back into AI models that predict maintenance requirements, thereby preventing catastrophic failures and extending tool life significantly for high-value industrial clients.

The future expectation concerning AI is less about making the vise itself "smart" and more about enhancing the ecosystem in which the vise operates. For instance, predictive maintenance models can analyze environmental factors (temperature, humidity, exposure to corrosive agents) alongside usage data (tracked via site telemetry) to issue alerts recommending timely chain lubrication or jaw replacement, optimizing operational expenditure for large fleet owners. Additionally, AI-powered design tools allow manufacturers to rapidly prototype and test new ergonomic features, such as optimized handle placement or weight distribution, using digital twins to simulate real-world usage stress. This focus on AI-assisted resilience and efficiency, rather than direct automation of the clamping action, summarizes the core impact, ensuring that the necessary physical stability provided by the vise is supported by highly intelligent operational management and manufacturing quality assurance processes.

The Pipe Vises Market dynamic is shaped by a confluence of powerful drivers (D) and limiting restraints (R), interspersed with critical opportunities (O), all subjected to various impact forces. A primary driver is the pervasive need for repair, rehabilitation, and replacement of extensive aging infrastructure globally, particularly utility networks for water, sewage, and natural gas, necessitating continuous demand for reliable pipe handling tools. Furthermore, stringent safety regulations enforced in developed economies mandate the use of certified and robust clamping solutions, pushing end-users away from rudimentary or unverified equipment. A significant restraint remains the high volatility and fluctuating cost of raw materials, primarily high-grade steel and iron castings, which directly impacts manufacturing margins and the final pricing of the vises, leading to procurement hesitancy during periods of sharp inflation. Opportunities primarily reside in the development and proliferation of lightweight, corrosion-resistant vise models, and the expansion into high-growth developing markets where infrastructure investment is aggressively scaling up. The interplay of these factors defines the competitive landscape and strategic decision-making within the sector, demanding manufacturers prioritize efficiency and material sourcing resilience.

Key impact forces operating on the market include the bargaining power of buyers, which is moderate to high, especially from large industrial distributors and EPC contractors who purchase in bulk and demand specialized features or custom sizing. The bargaining power of suppliers is moderate; while standard steel commodities are plentiful, specialty alloys required for extreme durability components (like hardened jaws) are sourced from a concentrated supplier base, granting them some leverage. The threat of new entrants is relatively low due to the established brand loyalty, the high capital requirement for precision manufacturing (casting/forging facilities), and the need for recognized certifications demonstrating tool reliability. The most significant external force is the threat of substitutes, which includes advanced pipe joining technologies such as electrofusion, specialized welding robotics, and increasingly automated pressing tools that reduce the need for traditional threading and manual manipulation, potentially diminishing the role of high-capacity threading vises in certain applications over the long term, pushing manufacturers to integrate their vises more closely with these evolving fabrication technologies.

The market faces external influences rooted in global geopolitical stability and environmental regulations. Geopolitical tensions often affect large cross-border pipeline projects, slowing down demand for the heaviest duty chain vises, while stringent environmental, social, and governance (ESG) standards are compelling manufacturers to adopt more sustainable production methods, including reduced waste and energy consumption in the foundry processes. This creates an opportunity for companies that can offer "green" vises made from recycled materials or via energy-efficient manufacturing, appealing to environmentally conscious municipal clients. Ultimately, the market trajectory will be heavily influenced by how quickly manufacturers can integrate advanced materials and ergonomic features while navigating the persistent challenges posed by cost volatility and the gradual shift toward automated pipe joining methods, necessitating continuous innovation in clamping stability and overall tool modularity to maintain relevance across all end-user sectors.

Market segmentation provides a crucial framework for understanding the diverse needs of end-users across different operational environments and pipe dimensions, ensuring that product development efforts are precisely targeted. The Pipe Vises market is predominantly segmented based on Product Type (Chain Vises vs. Yoke Vises), Material Used (Cast Iron vs. Forged Steel/Aluminum), Mounting Configuration (Bench Mount vs. Portable/Tripod Vises), and End-User Application (Industrial, Commercial, and Residential). This stratification allows market participants to identify lucrative niches, such as the growing demand for highly portable aluminum tripod vises in commercial HVAC installation, contrasting sharply with the stable demand for heavy-duty cast iron bench vises utilized in fixed fabrication workshops associated with the oil and gas sector, which prioritize sheer holding power and permanence over mobility. Analyzing these segments is essential for formulating accurate sales strategies and resource allocation, recognizing that pricing sensitivity and feature requirements vary significantly across these distinct categories, especially concerning factors like pipe capacity and jaw hardness.

The differentiation between Yoke Vises and Chain Vises is central to the market structure, where Yoke models dominate the light-to-medium duty category, offering quicker setup and high precision necessary for threading smaller pipe diameters commonly found in standard construction. Chain Vises, conversely, represent the high-capacity, heavy-duty segment, indispensable for utility contractors and industrial applications dealing with pipes exceeding four inches in diameter, offering versatile gripping power adaptable to various pipe coatings and conditions. Furthermore, the material segmentation reflects a key competitive battleground, pitting traditional, highly durable Cast Iron against newer, weight-saving Forged Steel and Aluminum compositions. The shift toward aluminum tripod vises represents a significant trend driven by contractor preference for reducing manual labor strain and increasing job site mobility, despite the higher initial cost compared to traditional, heavier iron models. Manufacturers must balance the trade-off between material cost, ultimate tensile strength, corrosion resistance, and total tool weight when addressing specific application requirements within these segments.

The value chain for the Pipe Vises Market begins with the upstream procurement of essential raw materials, primarily high-quality pig iron, various steel alloys (including specialized tool steels for jaws), aluminum, and specialized casting sands or molds. This initial stage is highly sensitive to global commodity prices and involves intensive processes such as precision casting (for main bodies) and specialized forging or machining (for hardened jaws and threaded mechanisms). Manufacturers must establish robust relationships with reliable metal suppliers who can guarantee material purity and consistency, as the structural integrity of the final product is paramount for safety standards. Given the substantial weight and specific performance requirements, logistical costs for raw material input and initial processing are high, making geographic proximity to efficient steel production centers a competitive advantage for vise manufacturers seeking to minimize transportation overheads and ensure streamlined production.

The midstream stage involves rigorous manufacturing and assembly processes, including specialized CNC machining to ensure the accuracy of the jaw mechanisms, heat treatment to harden gripping surfaces for enhanced wear resistance, and the application of corrosion-resistant coatings. Quality control is a critical bottleneck here, particularly testing the clamping load capacity and dimensional precision of the threaded components, which determine the tool's performance and lifespan. Distribution forms the downstream segment, dominated by a mix of direct sales to large industrial clients (EPC firms, major utilities) and, more commonly, indirect sales through a tiered network. The indirect channels typically include major industrial supply distributors (e.g., Grainger, Fastenal equivalents), specialized plumbing and HVAC supply houses, and online marketplaces. Specialized plumbing wholesalers play a crucial role as they often provide value-added services such as technical support and immediate product availability, making them preferred channels for professional contractors who require just-in-time inventory.

The efficiency of the distribution channel dictates market penetration and customer reach. Direct channels are utilized for highly customized or large-volume governmental contracts, allowing manufacturers maximum control over pricing and customer service, although requiring substantial internal sales infrastructure. Indirect distribution, leveraging established networks, provides broad market coverage but involves margin sharing and dependence on distributor performance. The increasing influence of e-commerce platforms has introduced a hybrid model, blurring the lines between direct and indirect sales, allowing manufacturers to reach smaller, previously inaccessible contractors while maintaining brand visibility and controlling pricing more effectively. Successful companies optimize this value chain by investing in advanced material handling (minimizing casting defects) and establishing highly efficient, global distribution partnerships capable of handling the bulky and heavy nature of pipe vise inventory across varied geographic locations, ensuring reliable supply to diverse end-user demands.

The customer base for the Pipe Vises Market is heterogeneous, primarily consisting of professional tradespeople and large industrial organizations that rely on secure pipe manipulation for their core operations. The most significant segment of potential customers comprises specialized plumbing, heating, ventilation, and air conditioning (PHVAC) contractors who utilize vises daily for cutting, reaming, and threading piping systems in commercial and residential construction projects. These buyers prioritize portability, quick setup time, and moderate capacity (up to 4 inches). Another major group consists of municipal and public utility maintenance departments (water, gas, sewage) that require heavy-duty, fixed bench and tripod vises capable of handling larger diameter pipes and surviving harsh environmental exposure, often purchasing equipment through long-term government contracts where durability and adherence to specifications are non-negotiable purchasing criteria.

The second tier of critical customers includes the Energy and Petrochemical sector, encompassing oil and gas pipeline construction companies, refining plant operators, and offshore drilling maintenance teams. These end-users demand the highest levels of safety and capacity, relying heavily on rugged chain vises and specialized hydraulic gripping systems for large-scale, high-pressure piping applications. Their purchasing decisions are driven by stringent regulatory compliance, tool certification standards, and the need for maximum reliability in hazardous environments, leading to preferences for premium, specialized forged steel vises. Additionally, general manufacturing and fabrication workshops, which often require in-house pipe fitting for machinery or process lines, represent stable but less volume-intensive buyers, focusing on versatility and long-term bench mount stability within a controlled industrial environment.

A smaller, yet growing, segment involves institutional maintenance teams (universities, hospitals, large corporate facilities) and the advanced DIY market. Institutional buyers seek highly reliable, medium-duty vises for internal infrastructure repairs, valuing ease of use and long warranties. The DIY market, accessed primarily through retail hardware stores and online platforms, focuses on low-to-medium capacity yoke vises with an emphasis on affordability and simplicity. Targeting these diverse buyers requires manufacturers to develop a broad product matrix, from highly specialized, expensive industrial models tailored for corrosive environments to cost-effective, user-friendly options for the residential market, ensuring that marketing efforts and distribution channels are tailored to the specific procurement processes and technical requirements of each distinct potential customer group to maximize market penetration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 550.4 Million |

| Market Forecast in 2033 | USD 818.9 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | RIDGID (Emerson Electric Co.), REED Manufacturing, ROTHENBERGER, Stanley Black & Decker, TRACTEL, Record Power, WM. G. BLUMENSTEIN (WGB), Irwin Industrial Tool, General Tools & Instruments, PFERD, Wilton Tools, Starrett, Beta Tools, Teng Tools, KNIPEX, Klein Tools, C. & J. Products, Superior Tool Co. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Pipe Vises Market is characterized less by radical electronic innovation and more by continuous material science advancements and mechanical engineering refinement aimed at improving durability, portability, and operational efficiency. A core technological trend involves the transition from traditional, heavy cast iron structures toward high-strength, lightweight aluminum and specialized alloy compositions, particularly in portable tripod vise designs. This shift significantly reduces the overall weight of the equipment, enhancing contractor mobility and reducing the risk of workplace injuries associated with manual handling, without compromising the clamping force required for secure operation. Furthermore, metallurgical improvements focus on developing jaw inserts made from hardened tool steel with specialized tooth geometries or non-marring coatings, ensuring exceptional grip on diverse materials (e.g., plastic, stainless steel) while extending the service life of the gripping components, thereby lowering the total cost of ownership for end-users operating in rigorous industrial settings.

Another area of significant technological development is the implementation of quick-release mechanisms and modular vise designs. Modern pipe vises often incorporate enhanced locking systems and rapid adjustment features that allow users to secure and release pipes much faster than traditional screw-driven clamps, dramatically improving productivity on job sites where numerous cuts or threading operations are required. Modular technology allows a single vise frame to accept various interchangeable components, such as different jaw types or specific pipe capacity extenders, maximizing the tool's versatility across a wider range of applications and pipe sizes. This modularity not only offers economic advantages but also streamlines inventory management for contractors. Moreover, ergonomic design principles are increasingly integrated, focusing on optimized height adjustability, non-slip feet for tripod models, and user-friendly handle interfaces, reflecting an industry-wide commitment to worker safety and reducing musculoskeletal strain associated with repetitive clamping actions in physically demanding utility and construction environments, further driving the replacement cycle toward these technologically superior models.

Advanced manufacturing techniques, such as precision forging over standard casting for critical load-bearing components, are crucial to the current technology paradigm. Precision forging results in a finer grain structure in the steel, yielding greater strength and shock resistance necessary to withstand the high torques exerted during aggressive threading operations, particularly on large diameter Schedule 80 steel pipe. Beyond material and mechanism innovation, surface treatment technologies are vital, including specialized powder coatings and electroplating processes that offer superior resistance to corrosion, rust, and chemical exposure, ensuring the tool's longevity in harsh environments like coastal construction or chemical plants. While the basic principle of a pipe vise remains constant—to hold a pipe securely—the continuous refinement in materials, mechanisms, and manufacturing precision represents the cutting-edge technology that distinguishes premium, professional-grade equipment from standard, less reliable market offerings, directly influencing purchasing decisions in safety-critical sectors globally and maintaining the competitive edge of market leaders focused on high engineering standards.

The global Pipe Vises Market exhibits significant regional variations in demand, product preference, and growth trajectory, largely influenced by the stage of infrastructure development and regulatory environment in each area. North America, comprising the United States and Canada, represents a mature but stable market characterized by high consumer awareness regarding quality and safety standards. Demand here is predominantly driven by replacement cycles for existing equipment and the sustained need for maintenance and upgrades across vast municipal, oil, and gas pipeline networks. Contractors in this region prioritize precision-engineered yoke vises for commercial threading and lightweight, certified tripod models for ease of site transit, demonstrating a willingness to pay a premium for established brands that meet rigorous safety compliance standards, ensuring predictable, consistent revenue streams based on institutional and commercial maintenance activities.

Europe mirrors North America in its emphasis on high-quality, durable equipment, amplified by stringent European Union regulations concerning workplace safety and product certification (e.g., CE marking). The market in countries such as Germany, the UK, and France is fueled by targeted investments in energy transition projects, modernizing urban utilities, and complex industrial plant refurbishments. European manufacturers often lead in ergonomic design and advanced material research, focusing on modularity and environmental sustainability in their production processes. The demand profile favors highly specialized tools suitable for stainless steel and non-ferrous piping commonly used in high-specification industrial applications, maintaining a competitive landscape focused on technical superiority and adherence to localized engineering specifications, rather than merely competitive pricing strategies.

The Asia Pacific (APAC) region stands out as the primary growth engine for the Pipe Vises Market, driven by unprecedented levels of urbanization, massive government investment in infrastructure development, and rapid industrial expansion across economies like India, China, and Southeast Asian nations. The high volume of new construction projects—including water supply, sewage treatment, power generation, and transportation networks—translates into substantial demand for all types of pipe vises, ranging from heavy-duty chain models for major trunk lines to general-purpose yoke vises for commercial buildings. Price sensitivity is higher in many APAC sub-markets, leading to strong competition from local manufacturers, but there is a rapidly expanding segment that demands internationally certified, high-performance tools for critical infrastructure ventures, making it the most dynamic and complex region for market entry and sustained growth.

Finally, Latin America and the Middle East & Africa (MEA) present distinct market characteristics. Latin America’s demand is often tied to resource extraction projects (mining, oil) and public works projects aimed at expanding basic utility access, resulting in cyclical demand patterns heavily reliant on foreign investment levels. The MEA region is strongly dominated by the Oil and Gas sector, driving significant demand for heavy-duty, corrosion-resistant, high-capacity chain and yoke vises specifically rated for hazardous environments and large-diameter pipelines, particularly in Saudi Arabia, UAE, and other Gulf Cooperation Council (GCC) countries. The procurement in MEA is often project-based, requiring robust distribution and support capabilities tailored to large-scale, isolated construction sites where product failure is unacceptable due to the high costs associated with delays in energy production and transport infrastructure development projects.

The primary driver is the pervasive and sustained global investment in infrastructure modernization and replacement projects, particularly aging municipal water, gas, and sewage utility networks in mature economies, alongside rapid urbanization demanding new utility installations in the Asia Pacific region.

Yoke Pipe Vises generally hold the largest market share due to their widespread use in standard commercial and residential plumbing and HVAC applications involving smaller to medium-diameter pipes where high precision threading is required.

Technological innovation primarily focuses on material science (using high-strength, lightweight aluminum alloys for portability), enhanced ergonomics, the introduction of quick-release mechanisms, and precision hardening of jaws to improve grip stability and prolong tool life in demanding environments.

The main restraint is the high volatility and fluctuating cost of raw materials, particularly specialty steel and cast iron, which are essential for manufacturing durable vise bodies and high-performance gripping jaws, impacting production costs and final market pricing.

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by aggressive governmental spending on new infrastructure, rapid commercial construction, and escalating industrial expansion across major developing economies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.