ID : MRU_ 432739 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

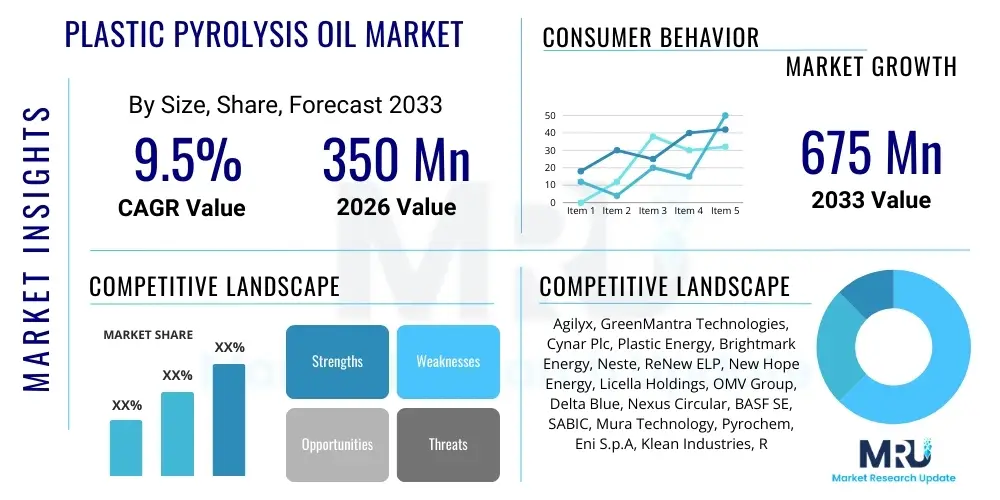

The Plastic Pyrolysis Oil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 675 Million by the end of the forecast period in 2033.

The Plastic Pyrolysis Oil Market encompasses the production and commercialization of liquid hydrocarbon fuel derived from waste plastics through the process of thermal decomposition in an oxygen-free or low-oxygen environment. This sustainable technology, known as plastic pyrolysis, converts complex polymer structures into simpler molecular compounds, primarily yielding pyrolysis oil (also known as plastic-derived oil or PDO), along with secondary products such as syngas and carbon black. Plastic pyrolysis oil serves as a critical bridge between environmental waste management and the energy sector, offering a viable, circular economy solution to the global plastic pollution crisis. The resulting oil possesses properties similar to conventional fossil fuels, making it suitable for direct use in industrial boilers, furnaces, and, increasingly, as a crucial feedstock for petrochemical crackers and refineries aiming to produce new virgin-quality plastics or sustainable fuels.

The core product, Plastic Pyrolysis Oil, is characterized by its high energy density and potential to displace fossil-based feedstocks, supporting global decarbonization and waste diversion mandates. Major applications of this oil span the energy sector, where it is utilized for power generation and heating, and the burgeoning chemical recycling industry, where it is co-processed to produce high-value polymers. Specific plastic types, such as polyethylene (PE), polypropylene (PP), and polystyrene (PS), are predominantly used as feedstock, yielding optimal oil quality. The benefits of this market include significant reduction in landfill waste, lowered dependence on crude oil resources, and the creation of a closed-loop system for previously non-recyclable plastic streams. The increasing global regulatory pressure to enhance recycling rates and restrict the use of single-use plastics directly contributes to the robust supply chain for feedstock necessary for pyrolysis operations.

Key driving factors accelerating market adoption include governmental incentives and subsidies promoting sustainable waste processing technologies, substantial investment from major petrochemical companies seeking to meet recycled content goals, and technological advancements that enhance the efficiency and scalability of pyrolysis reactors. Furthermore, growing consumer awareness regarding environmental stewardship and corporate commitments towards Net Zero targets are forcing industries, including manufacturing and logistics, to seek out and incorporate sustainable hydrocarbon alternatives. The versatility of the oil, coupled with its ability to handle mixed, contaminated, or low-grade plastic waste that conventional mechanical recycling cannot process efficiently, positions the Plastic Pyrolysis Oil market for sustained expansion across developed and emerging economies.

The Plastic Pyrolysis Oil market is experiencing significant transformation, driven primarily by circular economy mandates and increased private sector investment in chemical recycling infrastructure. Business trends indicate a strong move toward industrial-scale continuous pyrolysis units, shifting away from smaller batch processes to maximize efficiency and achieve feedstock supply reliability necessary for integration into existing refinery operations. Strategic partnerships between waste management companies and major chemical producers are defining the competitive landscape, focused on securing stable, high-volume inputs of residual plastic waste. Regionally, Asia Pacific is forecast to maintain market dominance due to massive plastic waste generation volumes and rapidly developing regulatory frameworks supporting waste-to-fuel initiatives, though regulatory clarity in Europe (especially concerning the end-of-waste status for pyrolysis oil) is driving substantial investment in advanced European facilities. Segment-wise, the application of Pyrolysis Oil as a direct feedstock for petrochemicals is exhibiting the highest growth trajectory, overshadowing its use purely as boiler fuel, reflecting the industry's strategic pivot towards high-value polymer production rather than energy generation.

The market faces inherent challenges related to the variability of feedstock quality, which impacts the consistency of the resulting pyrolysis oil and necessitates advanced pre-treatment and post-processing technologies. Nevertheless, technological improvements, such as catalytic pyrolysis, are addressing these quality issues, improving oil yield, and lowering process temperatures, thereby enhancing overall economic feasibility. Financial viability is further bolstered by the issuance of regulatory incentives such as Renewable Identification Numbers (RINs) or comparable carbon credits in various jurisdictions. The primary restraints include high initial capital expenditure required for sophisticated pyrolysis plants and the complex logistical challenges associated with sorting, cleaning, and transporting vast quantities of specific plastic waste types. Overall market resilience is high, however, as the fundamental problem—plastic waste accumulation—continues to provide an unlimited supply source, ensuring long-term demand for effective conversion technologies like pyrolysis.

Long-term prospects for the Plastic Pyrolysis Oil market are extremely favorable, anchored by global commitments to achieving material circularity. The transition from linear economic models is accelerating demand for secondary feedstocks that do not compromise product quality, positioning pyrolysis oil as indispensable for chemical manufacturing. Investment is particularly flowing into modular, decentralized pyrolysis systems which allow for easier scalability and placement near waste sources, mitigating transportation costs. Key stakeholders are prioritizing research into refining the crude pyrolysis oil to meet stringent standards for immediate co-processing, effectively making it a ‘drop-in’ replacement for naphtha. This strategic focus ensures that pyrolysis oil becomes an integrated component of the modern refining and petrochemical value chain, solidifying its role not just as a waste solution, but as an essential element of sustainable industrial production.

User queries regarding AI's influence on the Plastic Pyrolysis Oil market primarily revolve around efficiency improvements, feedstock management, and predictive maintenance capabilities. Users are concerned with how machine learning can address the chronic challenge of feedstock heterogeneity—a major variable impacting oil quality and operational stability. Key expectations include using computer vision and AI algorithms for advanced, high-speed sorting and categorization of mixed plastic waste to ensure consistent input quality for the pyrolysis reactors. Furthermore, users seek AI solutions for dynamic process optimization, where temperature, residence time, and catalyst ratios are adjusted in real-time based on subtle changes in feedstock characteristics, thereby maximizing yield and minimizing energy consumption. A significant theme is the implementation of AI for predictive failure analysis across complex pyrolysis units, minimizing downtime which is costly and severely impacts the economic competitiveness of continuous operations.

The market dynamics for Plastic Pyrolysis Oil are governed by a robust interplay of Drivers (D), Restraints (R), Opportunities (O), and associated Impact Forces, dictating the pace and direction of growth. Key drivers include stringent global environmental regulations mandating higher recycling rates and the urgent need to divert vast volumes of non-recycled plastic waste from landfills and incineration. The strong corporate sustainability pledges from major petrochemical and consumer goods companies—often requiring a minimum percentage of recycled content—exert significant upward pressure on demand for high-quality, chemically recycled intermediates like pyrolysis oil. These drivers are amplified by the impact force of rapidly diminishing landfill capacity and escalating disposal taxes across key industrial regions, making pyrolysis a financially attractive alternative to traditional disposal methods. Furthermore, the increasing acceptance of pyrolysis oil as a viable feedstock substitute by major refiners, facilitated by ongoing successful co-processing trials, provides market legitimacy and scale.

However, significant restraints temper the market’s explosive potential. The most critical restraint is the high capital investment required for constructing and commissioning commercial-scale pyrolysis facilities, often requiring multi-million dollar commitments that pose barriers to entry for smaller players. Additionally, the operational expenses are influenced by the highly variable and often high logistical costs associated with securing, sorting, cleaning, and preparing heterogeneous plastic waste feedstock, which is often bulky and contaminated. Regulatory uncertainty regarding the ‘end-of-waste’ status for plastic pyrolysis oil in certain jurisdictions hinders its seamless cross-border trade and integration into standardized petrochemical supply chains. The impact force of volatility in crude oil prices also plays a critical role; when crude prices drop significantly, the economic viability of pyrolysis oil as a substitute fuel source diminishes, forcing producers to rely heavily on the higher-value petrochemical feedstock application.

Conversely, the market is rich with opportunities, primarily focused on technological innovation and market expansion. The development of advanced, continuous catalytic pyrolysis systems promises higher yields and better oil quality, broadening the potential application spectrum. Significant opportunities exist in geographical expansion, particularly within emerging markets like Southeast Asia and Africa, which possess both high plastic waste volumes and nascent recycling infrastructure, offering fertile ground for new plant establishment. The development of specialized pyrolysis units optimized for hard-to-recycle plastics, such as multi-layer packaging or low-grade films, represents a niche opportunity for high-value differentiation. The overarching opportunity is the ability to leverage carbon credit mechanisms and Green Premium pricing, where pyrolysis oil fetches a higher price due to its certified environmental benefits. The convergence of corporate Net Zero strategies and supportive national policies creates a powerful, sustained impact force driving long-term investment into refining and scaling this technology globally.

The Plastic Pyrolysis Oil Market is segmented based on critical factors including the Type of Feedstock utilized, the Technology employed in the conversion process, and the final Application of the resulting oil. Understanding these segments is crucial for stakeholders to target specific supply chains and technological niches. The segmentation by feedstock reflects the diverse nature of plastic waste, with polyolefins (PE and PP) dominating due to their high oil conversion rates and widespread availability. Technology segmentation distinguishes between conventional thermal methods and advanced catalytic approaches, which offer improved product quality. The application segmentation delineates the primary uses, differentiating between direct energy use (fuel oil) and its high-value incorporation into the petrochemical value chain as a circular feedstock for new plastic production.

The value chain for the Plastic Pyrolysis Oil market is complex, spanning from waste collection to final product integration into highly demanding industrial sectors, necessitating rigorous quality control at every stage. The upstream segment is defined by the collection, sorting, baling, and rigorous pre-treatment of waste plastics. This phase is highly fragmented and characterized by significant logistical overheads and variable quality, posing a substantial challenge to consistent plant operation. Efficient collection networks, often involving collaboration with municipal waste management and specialized sorters, are critical for securing the high volume of feedstock required for large-scale continuous operations. Pre-treatment often includes washing, drying, and shredding to remove contaminants like moisture, PVC, and inorganic materials, as these can drastically impact oil quality and reactor integrity.

The midstream phase encompasses the actual conversion process—the pyrolysis plant itself. This involves complex thermochemical reactions, where the operational efficiency and technology type (e.g., fixed-bed, fluidized-bed, or rotary kiln) determine the yield and quality of the crude pyrolysis oil (CPO). Optimization of reactor conditions, including temperature regulation and catalyst selection in catalytic pyrolysis, is essential for maximizing the desired hydrocarbon fractions and minimizing unwanted byproducts like char and corrosive compounds. Post-processing activities, such as de-ashing, de-chlorination, and fractional distillation, are increasingly integrated into the midstream to upgrade the CPO into a refined product suitable for direct injection into refinery crackers or for use as high-grade bunker fuel. Investment in high-efficiency reactors and advanced purification systems is the primary value driver in this segment.

The downstream segment involves the distribution and end-use of the refined pyrolysis oil. Distribution channels are primarily direct, involving long-term supply contracts between pyrolysis producers and major petrochemical companies, refineries, or large industrial consumers. Indirect distribution may involve specialized energy trading firms or brokers who aggregate smaller volumes of pyrolysis oil for blending or delivery to smaller power generation facilities. Success in the downstream market hinges on achieving consistency and meeting stringent quality specifications (e.g., sulfur content, calorific value, density) demanded by refiners. The highest value capture occurs when the oil is successfully utilized as a certified, sustainable feedstock for producing virgin-grade polymers, which commands premium pricing and contributes directly to corporate circularity targets, significantly differentiating it from its use solely as a lower-value fuel source.

The primary customers for Plastic Pyrolysis Oil fall into three major industrial categories: the petrochemical industry, the energy and power generation sector, and the marine and heavy transport industry seeking sustainable bunker fuels. Petrochemical companies and major refiners are the fastest-growing and highest-value customer base. They acquire pyrolysis oil to co-process it alongside conventional naphtha or gas oil within their existing crackers or refining units. This allows them to produce certified circular polymers (e.g., circular polyethylene or polypropylene), meeting the escalating demand from consumer brands for recycled content without compromising performance standards. The critical factor for these customers is the oil's compatibility with their existing infrastructure and a guarantee of reliable, large-scale supply with stringent quality control regarding impurities like chlorine, metals, and sulfur.

The energy sector, including operators of industrial boilers, furnaces, and decentralized power plants, represents a robust and foundational customer segment. These entities utilize pyrolysis oil as a direct heating or energy source, often substituting traditional heavy fuel oil or diesel. The adoption here is driven by cost-effectiveness, provided the price remains competitive with traditional fuels, and by corporate mandates to reduce greenhouse gas emissions through the utilization of waste-derived fuels. While this segment offers consistent demand, the price sensitivity is higher compared to the specialized petrochemical application. Additionally, the marine fuel sector is emerging as a significant potential customer, driven by IMO 2020 regulations and subsequent decarbonization targets, looking for alternative sustainable fuels that can be blended to meet lower sulfur and carbon intensity requirements for shipping.

In essence, the market's potential growth is intrinsically linked to the chemical recycling ambitions of global conglomerates like ExxonMobil, SABIC, Shell, and BASF, who require massive, consistent volumes of circular feedstock to fulfill their long-term commitments. Small and medium-sized pyrolysis producers often target local energy consumers or sell refined products to specialized traders. However, the future focus is on securing large-scale, long-term contracts with integrated oil and gas majors and Tier 1 chemical producers, positioning the pyrolysis oil as a strategic component of the shift towards a sustainable, low-carbon materials economy. This trend confirms the transition of pyrolysis oil from a niche waste-to-energy product to a critical petrochemical commodity.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 675 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Agilyx, GreenMantra Technologies, Cynar Plc, Plastic Energy, Brightmark Energy, Neste, ReNew ELP, New Hope Energy, Licella Holdings, OMV Group, Delta Blue, Nexus Circular, BASF SE, SABIC, Mura Technology, Pyrochem, Eni S.p.A, Klean Industries, Recenso GmbH, Itero Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Plastic Pyrolysis Oil market is rapidly evolving, moving away from simple thermal degradation systems towards sophisticated, highly efficient catalytic processes. The core goal of technological innovation is to increase the yield of high-quality liquid oil, minimize unwanted byproducts like char and non-condensable gases, and drastically reduce the levels of contaminants such as chlorine and oxygenates. Traditional thermal pyrolysis relies solely on heat to break down polymer chains but often yields a crude oil requiring extensive post-processing to meet refinery standards. Modern advancements focus heavily on continuous pyrolysis reactors, such as rotary kiln and fluidized bed systems, which enable high throughput, uniform heat distribution, and better scalability essential for meeting industrial demand volumes.

The most impactful technological shift involves the integration of catalytic pyrolysis. By introducing specific catalysts (zeolites, metal oxides, or hierarchical porous materials), manufacturers can selectively guide the cracking process, resulting in a pyrolysis oil with a significantly narrower molecular weight distribution, lower viscosity, and reduced sulfur content—making it far more compatible with existing petrochemical infrastructure. This catalytic approach allows for lower operating temperatures and pressure, translating directly into reduced energy consumption and improved safety profile. Furthermore, advanced pre-treatment technologies, including proprietary scrubbing and chemical stabilization techniques, are critical for managing the corrosive elements derived from certain waste plastics (e.g., PVC), ensuring the longevity and reliability of expensive processing equipment.

Digitalization and modularization are also shaping the competitive technological landscape. The emergence of modular pyrolysis units allows for decentralized waste processing closer to the source of plastic generation, minimizing logistical complexity and transportation costs, particularly in rural or island settings. Furthermore, integrating advanced sensors and Industrial Internet of Things (IIoT) capabilities permits granular control over the pyrolysis process, enabling real-time adjustments based on variations in feedstock characteristics—a feature greatly enhanced by AI/ML analytical tools. Companies are increasingly filing patents related to enhanced fractionation systems, which separate the pyrolysis oil into specific cuts (e.g., naphtha, diesel, heavy oil) immediately after the reactor, maximizing the economic value derived from the heterogeneous output stream and cementing technology as a primary differentiator in this capital-intensive sector.

The global Plastic Pyrolysis Oil market exhibits significant regional variation, driven by differential regulatory environments, waste management infrastructure, and industrial capacity for utilizing the final product.

The primary driver is the global mandate for achieving material circularity and the need for high-quality recycled feedstock that can substitute virgin fossil fuels in petrochemical refining, specifically to meet stringent corporate recycled content targets.

Yes, pyrolysis oil is considered a cornerstone of chemical recycling, enabling the conversion of previously non-recyclable, mixed, and contaminated waste plastics into feedstocks for producing new, virgin-quality polymers, thereby closing the loop on plastic waste.

Key technical challenges include managing feedstock quality variability (especially chlorine and moisture content), ensuring the consistency of the final oil product to meet refinery standards, and overcoming the high energy demand required for continuous, large-scale reactor operations.

Crude pyrolysis oil often requires upgrading due to high oxygenate content and impurities, but modern catalytic pyrolysis and post-processing technologies yield a refined product comparable to naphtha or heavy fuel oil, making it suitable for co-processing in conventional refineries.

While Asia Pacific possesses the largest feedstock volume, Europe and North America, particularly the US Gulf Coast, are leading in terms of strategic, large-scale private investment and commissioning of advanced, continuous catalytic pyrolysis facilities integrated with major petrochemical hubs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.