ID : MRU_ 437762 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

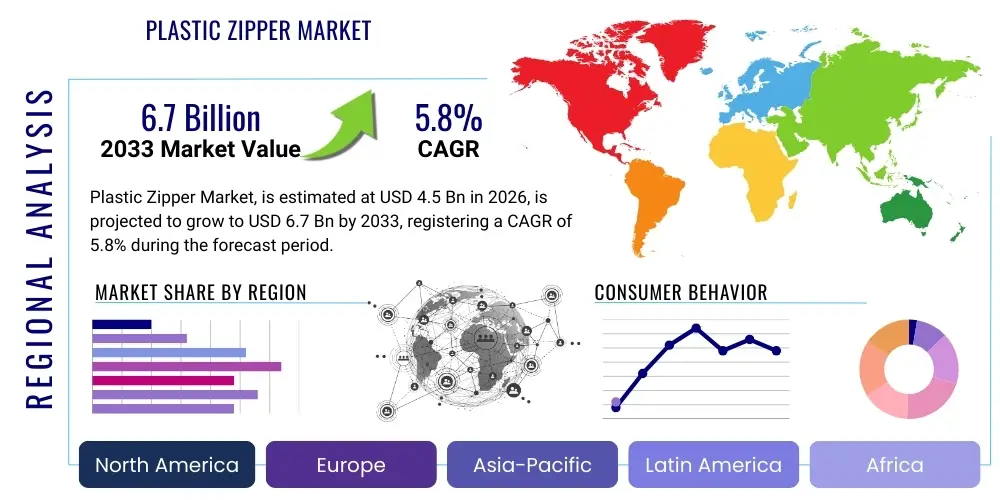

The Plastic Zipper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 6.7 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the robust growth of the global apparel and textile industries, particularly in emerging economies where manufacturing output is continually increasing. The cost-effectiveness, lightweight nature, and resistance to corrosion offered by plastic zippers compared to their metal counterparts have positioned them as the preferred fastening solution across various end-use sectors, including fast fashion, outdoor gear, and luggage manufacturing.

The market expansion is also underpinned by continuous innovation in polymer science, leading to the development of higher-performance plastic zippers that offer enhanced durability, better aesthetic integration (such as invisible and reversed coil zippers), and specialized functionalities like waterproofing or fire resistance. Manufacturers are investing heavily in automation and precision injection molding technologies to scale production and meet the high volume demand originating from large-scale global brands. Furthermore, shifting consumer preferences towards athleisure and technical apparel, which prioritize lightweight and flexible materials, significantly contribute to the escalating adoption rates of plastic fastening systems worldwide.

Regional dynamics play a critical role in shaping the market size, with the Asia Pacific region commanding the largest share due to its concentration of textile manufacturing hubs, notably China, India, and Vietnam. However, North America and Europe represent mature markets characterized by higher Average Selling Prices (ASP) for specialty zippers used in performance sportswear and luxury goods, focusing heavily on sustainability and compliance with strict environmental regulations. The growing focus on developing zippers from recycled plastics (rPET) or bio-based polymers represents a key trajectory that will influence market value and drive premium pricing segments in the coming years, ensuring sustained growth throughout the forecast period.

The Plastic Zipper Market encompasses the manufacturing, distribution, and sale of fastening devices primarily constructed from synthetic polymer materials such as Nylon (polyamide), Polyester, and polyacetal (POM). These zippers, which operate via interlocking teeth or coils secured onto fabric tape, serve as indispensable components across a vast spectrum of consumer and industrial applications. Their lightweight structure, resistance to environmental degradation including rust and moisture, and inherent flexibility make them highly preferable, particularly in industries where material weight and longevity are crucial design considerations. The core product categories include coil zippers (the most common type), Vislon or molded plastic zippers (known for strength), and invisible zippers (used primarily for aesthetic purposes in high-end garments), all designed to provide reliable, non-corrosive closure systems.

Major applications of plastic zippers span the global textile and manufacturing supply chain, with the apparel industry—including outerwear, casual wear, sportswear, and fashion accessories—being the dominant end-user. Beyond clothing, plastic zippers are essential in the manufacturing of luggage, backpacks, camping gear, footwear, and home furnishing items such as mattress covers and upholstery. The inherent benefits, including ease of dyeing to match fabric colors, lower production cost compared to brass or aluminum zippers, and compliance with various international standards regarding non-toxicity, fuel their pervasive adoption. Moreover, the increasing demand for high-performance zippers in technical textiles, such as medical and protective clothing, further diversifies the market landscape.

The driving factors for market growth are manifold and intertwined with global macroeconomic trends. Key drivers include the rapid expansion of the fast fashion sector requiring enormous volumes of low-cost, reliable components, and the burgeoning e-commerce penetration which facilitates quicker turnover in textile manufacturing. Furthermore, continuous product innovation focusing on enhanced mechanisms, environmental responsibility, and greater design flexibility allows manufacturers to target niche markets effectively. The shift away from heavy, rigid fastening options towards lighter, more resilient polymer solutions supports the overall growth trajectory of the Plastic Zipper Market, reinforcing its position as a highly dynamic segment within the broader global accessories industry.

The Plastic Zipper Market is experiencing significant transformation, driven by a confluence of evolving business trends focused on sustainability, digitalization of supply chains, and advanced manufacturing precision. Businesses are prioritizing the adoption of Circular Economy models, specifically by utilizing recycled polyethylene terephthalate (rPET) in zipper tape and components, responding directly to stringent environmental mandates and rising consumer demand for eco-friendly products. Competition remains intense, primarily based on pricing and volume capabilities, compelling major players to invest in high-speed, automated production lines to achieve economies of scale and maintain competitive margins across global markets. Strategic partnerships with major fashion retailers and sportswear giants are crucial for securing long-term contracts and leveraging design co-creation opportunities.

Regional trends indicate that the Asia Pacific (APAC) region retains its undisputed leadership in consumption and production, serving as the global manufacturing center for apparel and textiles. This dominance is supported by favorable governmental policies, lower operational costs, and established, sophisticated supply chain networks. However, North American and European markets exhibit different trend characteristics, focusing less on sheer volume and more on high-performance, specialized, and customizable plastic zippers (e.g., zippers for extreme weather gear, military applications, or luxury fashion). These developed regions prioritize quality assurance and compliance, pushing technological boundaries for features such as antimicrobial properties and extreme temperature resilience. Latin America and the Middle East & Africa (MEA) are emerging as high-growth potential regions, underpinned by expanding domestic textile industries and increasing urbanization leading to higher disposable incomes and greater consumer spending on apparel and accessories.

Segment trends highlight the exceptional growth of the Coil Zipper segment due to its versatility, low profile, and cost advantage, making it ubiquitous in ready-to-wear clothing. The Invisible Zipper sub-segment is rapidly gaining traction, particularly in womenswear and premium garments, where aesthetic seamlessness is prioritized. In terms of end-use, the Sportswear and Outerwear segments are projected to record the highest growth rates, driven by the global athleisure trend and the requirement for lightweight, water-resistant, and high-strength plastic fasteners suitable for demanding physical activities. Material innovation focuses heavily on enhancing the tactile feel and long-term durability of polymers like POM, ensuring that plastic zippers can withstand frequent use and industrial washing processes without compromising functionality.

Common user questions regarding AI's influence in the Plastic Zipper Market revolve primarily around operational efficiency, quality control, and supply chain predictability. Users frequently inquire about the feasibility of using AI for detecting microscopic defects in zipper teeth during high-speed production, optimizing raw material procurement schedules based on fluctuating polymer market prices, and enhancing demand forecasting accuracy for specialized zipper types. The overarching theme is the application of sophisticated algorithms to reduce waste, minimize manual inspection labor, and increase the responsiveness of the highly complex, global textile supply chain. Users seek confirmation on whether AI-driven predictive maintenance can prevent costly machinery downtime, thereby stabilizing production output.

The implementation of Artificial Intelligence and Machine Learning (ML) is fundamentally transforming the manufacturing and logistics aspects of the plastic zipper industry. AI-powered Computer Vision systems are being deployed on production lines, utilizing high-resolution cameras and ML models to perform real-time, 100% inspection of zipper coils and components, identifying minute defects such as misalignment, uneven molding, or broken elements far more reliably and faster than traditional human inspection methods. This capability drastically reduces defect rates, ensures adherence to high-quality international standards, and minimizes expensive recalls, directly benefiting brands focused on high-performance applications.

Furthermore, AI algorithms are playing a pivotal role in optimizing raw material inventory and enhancing supply chain resilience. By analyzing vast datasets related to global oil prices, geopolitical events, shipping lane capacity, and historical demand patterns, AI provides highly accurate predictive models for polymer purchasing. This allows manufacturers to procure Nylon and Polyester resins at optimal times, mitigating the financial risks associated with volatile petrochemical markets. In the planning phase, AI optimizes factory floor layouts and scheduling, dynamically adjusting production sequences to maximize throughput and minimize energy consumption, marking a clear path toward Smart Factory operations within the plastic zipper manufacturing domain.

The Plastic Zipper Market is influenced by dynamic forces encapsulated within its Drivers, Restraints, and Opportunities (DRO), which collectively determine the market's trajectory and profitability. Key drivers include the accelerating global demand from the voluminous ready-to-wear and sportswear segments, coupled with the inherent advantages of plastic materials—specifically, superior cost efficiency, lighter weight, and resistance to corrosion compared to metal alternatives. The rapid proliferation of e-commerce and fast fashion models necessitates flexible, high-volume production of components, a requirement plastic zippers are optimally positioned to meet. Additionally, product diversification into technical textiles, such as military or medical applications, provides new avenues for specialized, higher-margin growth, further stabilizing demand and overall market performance.

Conversely, the market faces significant restraints that dampen potential growth rates and pose strategic challenges for manufacturers. The primary restraint is the inherent volatility in the pricing of crude oil derivatives, which are the fundamental raw materials (Nylon, Polyester resins) for plastic components; these fluctuations make long-term cost planning difficult and impact profitability margins. Furthermore, increasing global regulatory pressure on single-use plastics and general plastic waste management is forcing companies to invest heavily in sustainable alternatives, which often carry higher initial production costs. The market is also characterized by intense, cutthroat price competition, particularly from low-cost Asian manufacturers in the unorganized sector, leading to commoditization in standard zipper types and placing downward pressure on average selling prices globally.

Opportunities for strategic expansion lie in aggressive pursuit of the circular economy, focusing on developing truly recyclable or biodegradable plastic zippers that align with global sustainability initiatives, thus capturing premium market share. Technological advancements in automation and precision manufacturing offer opportunities to improve product quality while lowering labor costs, enhancing overall operational efficiency. The market is further shaped by the Impact Forces of substitution threat (though currently low due to performance superiority) and supplier power (high due to reliance on specific polymer suppliers). Buyer power is extremely high, especially exerted by major global apparel brands, who dictate pricing, quality standards, and ethical sourcing requirements, compelling zipper manufacturers to continuously innovate and comply with rigorous sourcing audits.

The Plastic Zipper Market segmentation provides a granular understanding of the diverse product offerings and their utilization across various end-user industries, facilitating targeted marketing and strategic investment decisions. The market is primarily segmented based on product type (Coil Zippers, Vislon/Molded Zippers), material used (Nylon, Polyester, POM), application (Apparel, Luggage, Footwear, Others), and mechanism (Open-End, Closed-End). Coil zippers, often made from polyester or nylon, represent the foundational segment due to their flexibility, ease of manufacturing, and cost-efficiency, making them suitable for most general apparel applications, ranging from skirts and dresses to interior pockets.

The Vislon or molded plastic zipper segment, characterized by individually molded, robust teeth typically made from POM (Polyoxymethylene), commands higher pricing due to superior strength and durability. These are predominantly used in heavy-duty applications such as outerwear, protective clothing, and robust luggage where resistance to extreme force or temperature variations is essential. Geographically, segmentation highlights the distinction between high-volume, cost-sensitive production centers in Asia Pacific and the high-value, specialized, and quality-driven markets in North America and Europe, where demand for niche products like waterproof and hidden zippers dominates.

Further analysis by end-use confirms that the Apparel sector remains the undisputed largest consumer, driven by fast fashion and seasonal turnover. Within apparel, the sportswear and outerwear categories are growing fastest, requiring advanced plastic zipper technology that offers features like water repellency, UV resistance, and minimal weight. Understanding these segments is crucial for key market participants aiming to optimize their product portfolio, enabling them to capitalize on the increasing adoption of performance materials and the global shift toward more casual and technical dressing styles.

The value chain for the Plastic Zipper Market is segmented into five core stages: upstream material sourcing, manufacturing and assembly, distribution and logistics, downstream application, and post-sales service. Upstream activities involve the procurement of specialized synthetic resins—primarily Nylon (Polyamide), Polyester, and Polyoxymethylene (POM)—along with necessary chemicals, colorants, and textile tape materials. The supply of these base polymers is dominated by a few large petrochemical companies, giving suppliers moderate leverage. Efficient sourcing strategies, including long-term contracts and hedging against price volatility, are critical at this initial stage to stabilize input costs for zipper manufacturers. Quality control starts here, ensuring the polymers meet tensile strength and colorfastness requirements.

The manufacturing and assembly stage is highly capital-intensive, characterized by sophisticated processes such as high-speed injection molding (for Vislon teeth), weaving and knitting (for tape), and automated assembly mechanisms (for attaching teeth, sliders, and stops). Direct manufacturing involves specialized equipment capable of producing millions of zipper meters annually, emphasizing the need for scale and precision to minimize waste and ensure product consistency. Quality and design customization, including matching colors and providing specific puller designs, add value during this stage. Integration of advanced robotics and AI-powered quality checks significantly enhances operational throughput and defect reduction.

Distribution channels are multifaceted, employing both direct and indirect routes to market. Direct sales are typically preferred for large-volume orders from multinational apparel corporations (such as Nike, Adidas, or specialized luxury brands) where customized specifications and direct technical support are mandatory. Indirect channels, involving wholesalers, regional distributors, and agents, cater to smaller manufacturers and regional markets, offering centralized inventory and faster local delivery. Downstream, the final value is realized when the zipper is successfully integrated into the end-user product (e.g., a jacket or backpack). The effectiveness of the supply chain relies heavily on swift, reliable logistics to meet the tight turnaround times demanded by the fast fashion industry, making robust inventory management a competitive differentiator. Post-sales service focuses on managing quality claims and technical support for application in diverse manufacturing settings.

The primary and most voluminous consumers of plastic zippers are companies operating within the global apparel manufacturing sector, encompassing a vast array of sub-segments from high-street fashion to utilitarian workwear. Ready-to-wear manufacturers, particularly those in the casual and sportswear categories, constitute the core demand base, requiring zippers in massive quantities for trousers, jackets, skirts, and dresses. Global giants in athletic and outdoor wear represent another critical segment, demanding high-performance plastic zippers engineered for specific technical requirements, such as enhanced water resistance, extreme durability, and minimal weight, often specifying materials like reverse coil nylon for seamless integration and weather protection.

Secondary but highly significant customer segments include the manufacturers of travel goods and accessories, namely luggage, backpacks, handbags, and specialized carrying cases. In these applications, the inherent corrosion resistance of plastic zippers is crucial, as is their superior resistance to abrasion and impact, which are necessary for heavy-duty travel items. Furthermore, the footwear industry utilizes plastic zippers for boots and specialized sneakers, valuing the material's flexibility and ease of integration into complex designs. These sectors prioritize robustness and long-term functionality under repetitive stress, driving demand for the Vislon type of plastic zipper.

Tertiary potential customers are found within highly specialized industrial and technical textile markets. This includes the manufacturers of military and defense equipment (requiring NIR-compliant and highly robust plastic fasteners), medical textile producers (for surgical gowns, specialized medical device closures, and patient bedding), and the automotive industry (for seat covers, interior panels, and protective casings). These specialized end-users require plastic zippers that meet stringent certifications regarding fire retardancy, chemical resistance, or specific strength-to-weight ratios, representing a smaller volume segment but offering significantly higher margins due to the customization and technical compliance required.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 6.7 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | YKK Corporation, Riri SA, Coats Group Plc, Talon Zipper Inc., KCC Zipper, IDEAL Fastener Corporation, Sanli Zipper Co. Ltd., SBS Zipper Group, Tex Corp, Fujian SBS Zipper Science and Technology, YBS Zipper Co. Ltd., Weixing Industrial Development Co. Ltd., Zizper Industrial Co. Ltd., Max Zipper Co. Ltd., Ningbo MH Industry, Salmi Zippers, A.J. Plast, Zhejiang Yifeng Zipper, KAO SHING Co. Ltd., Shanghai Richeng Zipper. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Plastic Zipper Market is defined by continuous advancements aimed at improving manufacturing efficiency, product durability, and aesthetic versatility. Core manufacturing technologies include highly automated injection molding for creating Vislon teeth, which ensures precise alignment and robust component uniformity at high speeds. For coil zippers, the precision winding and knitting technology used for forming the continuous filament helix onto the textile tape is crucial, demanding sophisticated machinery to maintain consistent pitch and strength. Key players are increasingly integrating sensor-based systems and robotics into assembly lines to manage the high volume of components, reducing manual labor intervention and minimizing error rates, which are essential for maintaining competitive pricing in a volume-driven market.

A significant technological focus is directed towards material science, specifically the development of advanced polymer compounds that offer enhanced functional characteristics. This includes specialized plastic formulations that provide superior UV resistance, essential for outdoor gear and marine applications, as well as polymers with inherent flame-retardant properties required for professional and protective clothing. Furthermore, the industry is aggressively investing in sustainable material technologies, such as recycling post-consumer PET bottles to produce rPET zipper tapes and utilizing bio-based plastics (like PLA) for zipper teeth, aligning technological advancement with corporate social responsibility goals and impending regulatory demands in developed economies.

In terms of product innovation, the key technological drive is the development of specialty zippers, including hermetically sealed or fully waterproof plastic zippers achieved through advanced coating and sealing processes (like lamination or ultrasonic welding). These specialized fasteners are critical for applications in high-end outerwear, medical isolation suits, and extreme sports equipment. The emergence of Smart Zippers, integrating micro-sensors or RFID/NFC chips directly into the puller or tape structure, represents a futuristic technological frontier, enabling manufacturers and retailers to improve anti-counterfeiting measures, enhance inventory tracking capabilities, and potentially integrate product-use data collection, moving the basic fastener component into the realm of connected textiles and smart apparel.

The Asia Pacific (APAC) region stands out as the undisputed global powerhouse in the Plastic Zipper Market, primarily due to its immense concentration of textile and apparel manufacturing facilities, particularly in China, India, Vietnam, and Bangladesh. This region not only dominates global production capacity, capitalizing on lower labor costs and established supply chain infrastructure, but also acts as the largest consumer market driven by domestic demand and export-oriented manufacturing. The focus in APAC is predominantly on high-volume production of coil and standard Vislon zippers required for fast fashion and mass-market garments, necessitating efficient logistics and aggressive cost management strategies to maintain competitive edge globally.

North America and Europe represent mature, high-value markets characterized by a strong emphasis on quality, specialization, and regulatory compliance. Demand in these regions is skewed towards technical and performance-oriented plastic zippers used in specialized fields such as performance sportswear, luxury goods, and medical textiles, driving higher average selling prices. European consumers and regulators mandate strict adherence to standards concerning chemical safety (e.g., REACH compliance) and environmental sourcing, pushing manufacturers to prioritize rPET and sustainable manufacturing practices. Innovation in features like waterproofing and anti-snag mechanisms is often pioneered and adopted earliest in these Western markets, setting global quality benchmarks.

Latin America and the Middle East & Africa (MEA) are emerging as high-potential growth regions, supported by rapid urbanization, rising middle-class disposable incomes, and increasing investments in domestic textile manufacturing and retail infrastructure. While these markets currently hold a smaller share, the rapid expansion of sportswear consumption and the localization of manufacturing operations promise robust growth over the forecast period. Investment in modern zipper manufacturing technology within these regions is accelerating, driven by local governments seeking to reduce reliance on imported finished garments and establish self-sufficient textile value chains, thereby significantly increasing regional demand for plastic zipper products.

The primary materials are Nylon (Polyamide) and Polyester, predominantly used in coil zippers due to their excellent flexibility, light weight, and lower cost base. Polyoxymethylene (POM), often known as Vislon, is used for molded plastic zippers requiring superior strength and robustness in heavy-duty applications.

The sustainability movement is a significant driver, pushing manufacturers toward adopting recycled plastic (rPET) for zipper tape and components, and developing bio-based polymer alternatives (e.g., PLA). Compliance with environmental regulations and meeting brand mandates for circularity are key factors influencing product development and market competitiveness.

The Asia Pacific (APAC) region, driven primarily by China, India, and Vietnam, dominates both the production capacity and consumption share due to its status as the global hub for textile, apparel, and footwear manufacturing.

Plastic zippers offer key advantages including superior resistance to corrosion (rust), significantly lighter weight, greater flexibility, and the ability to be easily color-matched to fabrics. They are also non-conductive and generally more cost-effective for mass production applications.

Automation, including advanced high-speed assembly and robotics, is critical for increasing production volume, maintaining precision, and lowering operational costs. AI-powered Computer Vision is increasingly used for 100% automated quality inspection, minimizing defects in high-speed manufacturing environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.