ID : MRU_ 436223 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

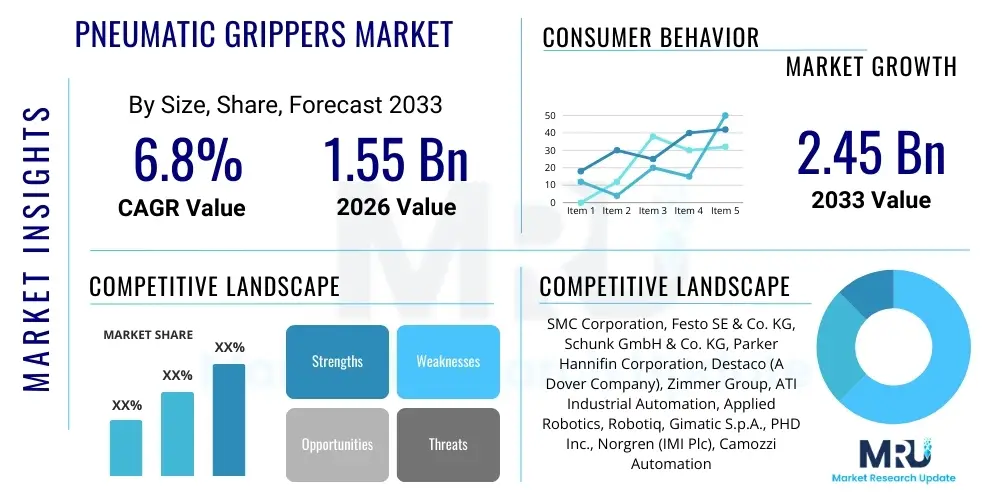

The Pneumatic Grippers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.55 Billion in 2026 and is projected to reach USD 2.45 Billion by the end of the forecast period in 2033. This growth trajectory is significantly influenced by the escalating demand for industrial automation across manufacturing sectors, particularly in regions undergoing rapid infrastructure development and technological modernization. The inherent simplicity, cost-effectiveness, and high force-to-weight ratio of pneumatic systems continue to drive their adoption, cementing their role as fundamental components in automated material handling and assembly processes globally. The market expansion is further underpinned by advancements in sensor integration and miniaturization, enhancing the precision and flexibility of pneumatic gripping solutions.

The Pneumatic Grippers Market encompasses devices utilized in automated industrial processes to pick up, hold, and place objects. These devices operate using compressed air to actuate jaws or fingers, enabling efficient handling of components ranging from delicate electronics to heavy metal parts. Key products include two-jaw parallel grippers, three-jaw concentric grippers, angular grippers, and specialized radial grippers, each designed for distinct handling requirements based on workpiece geometry and application velocity. These mechanisms are integral to streamlining production cycles, minimizing human error, and improving overall operational safety and throughput across various manufacturing environments, solidifying their status as critical automation components.

Major applications of pneumatic grippers span automotive manufacturing, electronics assembly, packaging, pharmaceuticals, and machine tending. In the automotive sector, they are crucial for handling body parts, engine components, and assemblies during welding and painting operations. The electronics industry relies on high-precision pneumatic micro-grippers for handling sensitive PCBs and small electronic components during assembly. Benefits derived from deploying these technologies include enhanced cycle times, high reliability under demanding conditions, robust design requiring minimal maintenance, and the ability to handle a wide range of payloads with relatively straightforward control systems. Furthermore, their rapid response capabilities make them suitable for high-speed pick-and-place operations common in modern packaging lines.

The primary driving factors propelling the pneumatic grippers market include the global push toward Industry 4.0 and smart factory initiatives, necessitating flexible and highly efficient end-of-arm tooling (EOAT). The rising labor costs in industrialized nations and emerging economies further accelerate the adoption of robotic automation, where pneumatic grippers serve as essential interfaces between robots and the materials being processed. Continuous innovation focusing on higher gripping force efficiency, integration of smart sensors for enhanced feedback, and the development of lightweight composite materials for construction contribute significantly to market expansion. The simplicity of pneumatic systems compared to complex electric servo grippers also maintains their competitive edge in applications where cost efficiency and robust performance are paramount considerations.

The Pneumatic Grippers Market demonstrates robust growth, driven primarily by pervasive trends in industrial automation, coupled with sustained investment in manufacturing capacity expansion across Asia Pacific. Business trends highlight a strong shift toward modular and easily configurable gripping systems that support rapid changeovers in production lines requiring high flexibility, such as those catering to diverse consumer electronics or specialized packaging requirements. Suppliers are increasingly focusing on offering integrated solutions that combine the gripper, sensing technology, and necessary air preparation units, streamlining the procurement and implementation process for end-users. Consolidation activities and strategic partnerships are also becoming prevalent, as major players seek to expand their geographic reach and bolster their technological portfolio, particularly in areas related to enhanced durability and higher cleanroom compatibility for regulated industries.

Regionally, Asia Pacific (APAC) maintains its dominance, spurred by heavy automation adoption in China, Japan, South Korea, and emerging economies like India and Vietnam, specifically within the automotive, electronics, and fast-moving consumer goods (FMCG) packaging sectors. North America and Europe, characterized by high labor costs and mature manufacturing bases, exhibit steady growth, focusing more on high-precision applications, such as medical device manufacturing and advanced aerospace component handling, where integration with collaborative robots (cobots) is a key trend. These regions prioritize sophisticated grippers with advanced feedback mechanisms and high reliability, often seeking solutions compliant with stringent safety and operational standards.

Segmentation trends indicate that two-jaw parallel grippers remain the largest segment due to their versatility and suitability for general industrial tasks. However, the fastest-growing segment is angular grippers and specialized adaptive grippers, catering to complex component geometries and high-mix, low-volume production scenarios, which demand greater flexibility from the EOAT. By payload, medium-duty grippers constitute the core market volume, balancing capacity and speed for most standard industrial robot applications. Furthermore, the push for energy efficiency is influencing product design, with manufacturers developing lighter grippers that require less compressed air, aligning with broader corporate sustainability goals and reducing operational expenses for manufacturers.

User queries regarding the impact of Artificial Intelligence (AI) on the Pneumatic Grippers Market primarily revolve around how AI can enhance the performance, flexibility, and longevity of these traditionally mechanical devices. Key themes frequently encountered include the application of machine learning for predictive maintenance of pneumatic systems, utilizing AI-driven vision systems to guide dynamic gripping operations, and employing generative design to optimize gripper geometry for specific, complex handling tasks. Users are deeply concerned about integrating basic, fast-cycling pneumatic components into sophisticated smart factory ecosystems and expect AI to bridge the gap between simple actuation and intelligent operation, thereby maximizing uptime and operational precision.

The core expectation is that AI will transform pneumatic grippers from fixed tools into adaptive components capable of handling highly variable inputs. This involves utilizing machine learning algorithms trained on operational data—such as pressure fluctuations, cycle times, and temperature—to detect subtle deviations indicative of potential failure, shifting maintenance from reactive to predictive models. Furthermore, AI-powered vision systems are becoming essential for applications involving random bin picking or handling components with slight positional variability, enabling the robot, and by extension the gripper, to make real-time adjustments to approach angle, grip force, and orientation, which is crucial for maximizing success rates in complex automation tasks.

Ultimately, the impact of AI is focused on optimizing operational parameters and extending the lifespan of pneumatic installations. AI-driven control systems can dynamically adjust the compressed air flow and pressure based on the payload characteristics and required speed, minimizing energy waste while ensuring the optimal gripping force—preventing damage to delicate parts or slippage of heavy items. This transition toward 'intelligent gripping' ensures that pneumatic solutions remain competitive against electric alternatives by offering enhanced capability, adaptability, and significantly reduced overall cost of ownership through maximized efficiency and minimized unexpected downtime.

The Pneumatic Grippers Market is significantly influenced by a blend of persistent drivers, inherent restraints, and burgeoning opportunities that shape its growth trajectory and competitive landscape. Key drivers include the overwhelming global trend toward automation, particularly in sectors struggling with escalating labor costs and the need for high-volume production with consistent quality, such as automotive, electronics, and high-speed packaging. The robust nature, high speed, and relatively low initial investment cost of pneumatic systems compared to servo-electric grippers make them highly attractive for entry-level automation projects and environments where simplicity and durability are paramount. Continuous innovation in miniaturization and materials science also enhances their applicability in tight spaces and cleanroom environments, further expanding their addressable market.

Conversely, the market faces notable restraints, primarily related to the requirement for a centralized air supply infrastructure, which adds complexity and initial cost, especially in smaller setups or retrofitting older facilities. Energy inefficiency associated with generating compressed air, often resulting in high operational costs compared to modern electric grippers, poses a significant competitive challenge, particularly in regions prioritizing energy conservation. Furthermore, the inherent lack of position feedback and limited force control variability in standard pneumatic grippers restricts their suitability for highly delicate or variable-force applications, creating a technological ceiling that electric alternatives often surpass. Leakage and noise generation associated with pneumatic systems also remain operational drawbacks.

Significant opportunities exist in the integration of pneumatic grippers with collaborative robots (cobots), offering flexible and safe human-robot interaction solutions, especially for Small and Medium-sized Enterprises (SMEs) seeking scalable automation. The expansion of high-growth segments such as food and beverage processing and medical devices, which demand specific hygienic and cleanroom-compatible gripping solutions, presents substantial market potential. Furthermore, manufacturers are focusing on overcoming the feedback limitation by integrating advanced sensors and IO-Link communication capabilities directly into pneumatic units, effectively creating smart pneumatic grippers that bridge the gap between traditional mechanical action and digital intelligence. The push for lightweight composite grippers also reduces the payload demand on the robotic arm, increasing overall system efficiency.

The Pneumatic Grippers Market segmentation provides a critical view of product adoption based on configuration type, application load, functionality, and end-use industry. The market is broadly categorized into parallel, angular, and specialized grippers, reflecting the diverse requirements for handling different object shapes and sizes. Analysis across these segments helps stakeholders understand which product designs are dominating specific industrial applications—for instance, the heavy reliance on parallel grippers for general machine tending versus the increasing use of angular and specialized grippers for complex assembly tasks in the electronics sector. The sustained growth of the market is underpinned by specialized customization, where standard pneumatic actuation is adapted to handle unique, often sensitive or irregular, industrial components.

The value chain for the Pneumatic Grippers Market commences with the upstream suppliers of raw materials and core components, crucial for manufacturing durable and reliable pneumatic systems. This upstream segment includes suppliers of high-grade aluminum and specialized alloys for the gripper body, seals and O-rings made from robust elastomers (such as Nitrile rubber or FKM for high-temperature/chemical resistance), and precision-machined steel components for piston assemblies and guidance mechanisms. The efficiency and quality of these foundational inputs directly dictate the performance characteristics—speed, longevity, and accuracy—of the final pneumatic gripper product. Furthermore, specialized component manufacturers provide critical elements such as magnetic sensors, flow control valves, and air preparation units (filters, regulators, lubricators) which are essential for the operation of the integrated system.

Moving downstream, the value creation shifts toward manufacturing, assembly, system integration, and distribution. Manufacturers (like SMC, Festo, Schunk) focus on precision engineering, modular design, and quality assurance, often developing proprietary technologies for enhanced gripping force or adaptive jaw mechanisms. The distribution channel plays a pivotal role, relying heavily on both direct sales teams for major OEM accounts (original equipment manufacturers in robotics and automation) and indirect channels utilizing authorized regional distributors and specialized system integrators. System integrators are particularly important as they bridge the gap between the component supplier and the complex end-user application, providing customization, programming, and installation support to ensure the pneumatic gripper functions optimally within the broader automated cell.

Direct channels are preferred for high-volume or highly customized orders where close technical consultation is necessary, especially with major automotive or electronics manufacturers. Indirect channels, including e-commerce platforms and regional resellers, focus on serving SMEs and general industrial maintenance, repair, and operations (MRO) needs, emphasizing inventory availability and rapid delivery. The structure of the distribution network is crucial for achieving market penetration and providing essential aftermarket support, including spare parts and repair services. The final stage involves the end-user, whose feedback drives iterative improvements in gripper design, particularly concerning longevity, resilience in harsh environments, and seamless integration with emerging robotic platforms.

The primary customers for pneumatic grippers are entities heavily invested in industrial automation, spanning multiple sectors that require repeatable, high-speed handling of components during manufacturing, assembly, or packaging. Major original equipment manufacturers (OEMs) of industrial and collaborative robots constitute a core customer base, integrating grippers as standardized or optional end-of-arm tooling packages provided to their clients. Beyond OEMs, large-scale automotive manufacturers and tier-one suppliers are persistent high-volume buyers, utilizing heavy-duty pneumatic grippers for tasks such as stamping, chassis assembly, and powertrain component handling, where robustness and sustained force are non-negotiable requirements across continuous production lines.

Another crucial customer segment resides within the electronics and semiconductor industry, characterized by the need for ultra-high precision and contamination control. These end-users, including manufacturers of smartphones, computer components, and medical electronics, purchase specialized, often miniaturized, cleanroom-compatible pneumatic grippers designed to handle delicate parts without scratching or particulate generation. Furthermore, the burgeoning logistics and e-commerce sector represents a rapidly expanding customer base, particularly for high-speed pick-and-place applications in automated warehousing, where robust, quick-cycling pneumatic grippers are deployed on sorters and packaging lines to manage varying package sizes and weights efficiently.

The food and beverage and pharmaceutical industries form a critical segment focusing on hygienic design. Potential customers here require grippers made from corrosion-resistant materials (like stainless steel) and designs that facilitate easy cleaning, mandatory for compliance with strict sanitation regulations. These applications include handling packaged food items, filling bottles, and manipulating medical devices during assembly and sterilization. Ultimately, any manufacturing or processing facility seeking to reduce manual labor, increase throughput efficiency, and improve component consistency through automation represents a potential buyer of pneumatic gripping technology, from high-volume standardized facilities to specialized job shops needing flexible, customizable EOAT solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.55 Billion |

| Market Forecast in 2033 | USD 2.45 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SMC Corporation, Festo SE & Co. KG, Schunk GmbH & Co. KG, Parker Hannifin Corporation, Destaco (A Dover Company), Zimmer Group, ATI Industrial Automation, Applied Robotics, Robotiq, Gimatic S.p.A., PHD Inc., Norgren (IMI Plc), Camozzi Automation S.p.A., Haddington Dynamics, IAI America, SAS Automation, Bimba Manufacturing, Zayer S.A., Jergens Inc., Weiss Robotics GmbH & Co. KG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Pneumatic Grippers Market is evolving from simple mechanical actuation toward smart, integrated, and modular systems, largely influenced by the requirements of Industry 4.0 environments. A primary focus involves enhancing the precision and adaptability of standard pneumatic devices through sophisticated digital integration. Key technological advancements include the embedding of miniaturized magnetic sensors and proximity switches directly into the gripper body, providing immediate feedback on jaw position (open/closed) and component presence. This integration moves pneumatic systems beyond basic actuation, allowing them to communicate crucial status information back to the PLC or robotic controller, thereby facilitating error detection and validating successful pick-and-place operations in high-speed applications.

Furthermore, significant development is centered around improving material science and mechanical design to optimize performance metrics. The use of advanced, lightweight composite materials, particularly carbon fiber or reinforced plastics, is becoming prevalent in the construction of gripper bodies and fingers. This technological shift reduces the overall mass of the end-of-arm tooling, enabling the robotic arm to operate at higher speeds or handle larger payloads, while simultaneously reducing inertia and minimizing energy consumption. Coupled with enhanced internal design, such as optimized piston geometries and improved sealing techniques, these material improvements ensure higher durability, reduced maintenance intervals, and extended operational lifespans, even in demanding environments characterized by dust or moisture.

The most forward-looking technological trend involves the digitalization of pneumatic control through smart valves and IO-Link compatibility. Modern pneumatic systems are increasingly utilizing smart pressure regulators and proportional flow control valves that can be digitally managed to adjust gripping force dynamically and precisely without requiring mechanical adjustments. This technology allows for rapid re-configuration between handling different components with varying fragility, effectively providing a degree of flexibility previously exclusive to electric grippers. This digital interface, often compliant with the IO-Link standard, enables seamless data exchange, remote diagnostics, and simplified parameterization, which is crucial for modern automated production lines requiring instant changeover and comprehensive data logging capabilities for process optimization and traceability.

Asia Pacific (APAC) dominates the Pneumatic Grippers Market, primarily driven by massive investments in manufacturing automation, particularly in China, Japan, and South Korea. These nations are focused on upgrading production facilities to increase efficiency and maintain global competitiveness in high-volume sectors like electronics, automotive, and consumer goods. The region's strong government support for industrial modernization, coupled with a large number of emerging manufacturing hubs (e.g., India, Vietnam), ensures a sustained high demand for cost-effective and robust pneumatic gripping solutions. The rapid proliferation of domestic robot manufacturers in China further fuels the adoption of locally sourced pneumatic EOAT.

North America and Europe represent mature markets characterized by high adoption rates of advanced automation solutions, focusing heavily on precision engineering, compliance, and integrating cobots. Growth in these regions is less volume-driven and more value-driven, centered on complex applications such as aerospace component handling, medical device assembly, and highly flexible packaging operations. European countries, particularly Germany (as a hub for industrial machinery and robotics) and Scandinavia, exhibit strong demand for high-performance pneumatic grippers that integrate advanced sensing capabilities and conform to stringent safety standards (e.g., ISO/TS 15066 for collaborative robot applications). These regions prioritize solutions that offer high reliability and operational efficiency over the entire lifecycle.

Latin America, the Middle East, and Africa (MEA) are emerging regions for pneumatic gripper adoption, largely spurred by foreign direct investment in manufacturing and infrastructure projects. While initial automation levels are lower than in APAC or Europe, sectors such as automotive assembly (Mexico, Brazil) and basic packaging/processing industries in the MEA region are increasingly integrating pneumatic grippers to enhance labor productivity. These regions represent significant untapped market potential as industrialization accelerates, with a strong preference for durable, simple-to-maintain pneumatic solutions that require minimal advanced technical expertise for installation and operation, focusing on standard parallel and angular gripper types.

Pneumatic grippers are typically favored for their significantly lower initial cost, robust design, high speed, and excellent force-to-weight ratio. They are simpler to install and maintain, making them ideal for rapid, high-cycle industrial applications where consistent force and speed are prioritized over highly variable force control or positional feedback, and where an existing compressed air supply is available. Their mechanical simplicity contributes to a higher tolerance for harsh industrial environments.

IO-Link integration transforms standard pneumatic grippers into intelligent components by enabling digital communication. This allows for detailed parameterization (e.g., adjusting grip force thresholds via software), advanced diagnostics, and transmission of status data (jaw position, cycle count) back to the central controller. This capability significantly enhances flexibility, facilitates predictive maintenance, and simplifies system commissioning within Industry 4.0 infrastructures.

The Automotive and Transportation industry remains the largest consumer segment for pneumatic grippers, utilizing them extensively for tasks ranging from handling heavy metal components during welding and stamping to precise assembly of internal parts. The sustained high-volume production requirements and the need for durable, high-force EOAT solidify the automotive sector’s dominant position, particularly favoring robust two-jaw and three-jaw parallel grippers for continuous duty cycles.

The outlook is highly positive. Pneumatic grippers are increasingly being adapted for cobots due to their inherent safety features—specifically, the ease of limiting force output to meet collaborative safety standards (ISO/TS 15066) and their generally lightweight design, which minimizes inertia. Manufacturers are focusing on developing compact, lightweight pneumatic grippers with rounded edges and advanced sensing to ensure safe human-robot interaction in flexible manufacturing and assembly environments.

The primary restraint is the necessity for compressed air infrastructure, which is costly to install and maintain, and the energy inefficiency associated with continuous air generation compared to electric servo systems. Furthermore, standard pneumatic grippers traditionally offer limited variable force control and lack integrated positional feedback, making them less suitable for highly delicate or adaptive handling tasks requiring complex digital force monitoring compared to advanced electric alternatives.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.