ID : MRU_ 433574 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

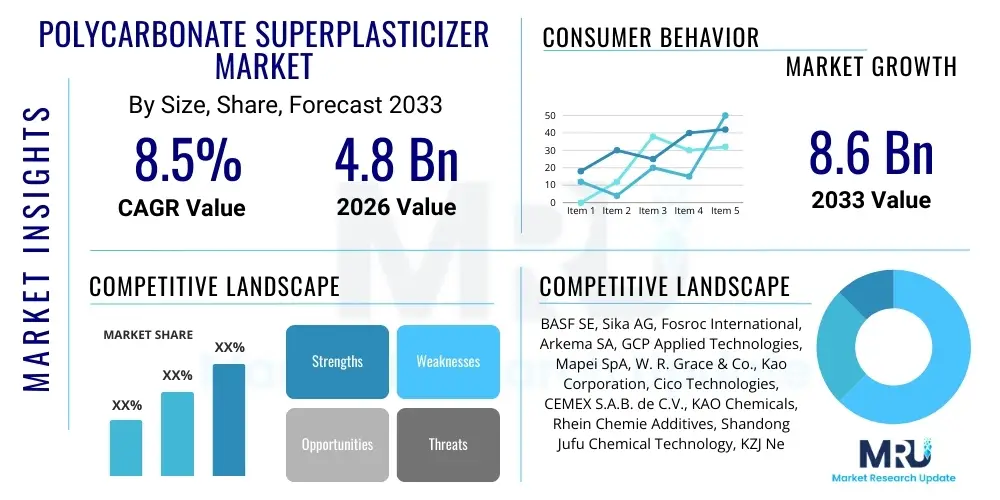

The Polycarbonate Superplasticizer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 8.6 Billion by the end of the forecast period in 2033.

The Polycarbonate Superplasticizer (PCE) Market encompasses advanced chemical admixtures primarily used in concrete and mortar production to significantly reduce water content while maintaining or enhancing slump flow and workability. These high-performance water reducers are essential for creating high-strength, durable concrete mixes, especially those used in complex infrastructure projects and high-rise construction. PCE superplasticizers operate through steric hindrance and electrostatic repulsion mechanisms, effectively dispersing cement particles and allowing for lower water-to-cement ratios without compromising flow characteristics, leading to superior final product quality.

Major applications of polycarbonate superplasticizers span across ready-mix concrete, precast concrete manufacturing, high-performance concrete (HPC), and ultra-high-performance concrete (UHPC) segments. Their key benefits include improved early and late compressive strength, reduced permeability, minimized shrinkage and cracking, and enhanced overall concrete longevity. This chemical efficiency allows construction companies to meet increasingly stringent performance specifications and accelerate construction timelines, driving their integration into modern building practices worldwide. The inherent flexibility in molecular design of PCEs allows for tailored formulations addressing specific ambient conditions and material inputs.

The primary driving factors for market growth include rapid global urbanization, massive government investments in infrastructure development (such as bridges, highways, and high-speed rail networks), and the rising demand for green building materials that require less water and achieve maximum material efficiency. Furthermore, technological advancements leading to the development of polycarboxylate ether-based superplasticizers with superior slump retention capabilities and wider compatibility with various cementitious materials are solidifying their dominant position over traditional superplasticizers like sulfonated naphthalene formaldehyde (SNF) and sulfonated melamine formaldehyde (SMF).

The Polycarbonate Superplasticizer Market is characterized by robust growth, driven primarily by the escalating demand for high-performance concrete in developing economies and the necessity for sustainable construction solutions globally. Key business trends indicate a strong focus on innovation, particularly the development of customized, low-dosage PCE admixtures that offer extended slump retention crucial for long-distance concrete transportation in metropolitan areas. Strategic mergers, acquisitions, and partnerships aimed at strengthening supply chain resilience and expanding regional manufacturing footprints are prevalent among major market participants seeking to optimize logistics and reduce operational costs associated with raw material procurement.

Regionally, the Asia Pacific (APAC) market dominates in terms of consumption volume, spearheaded by massive infrastructure programs in China and India, alongside sustained commercial and residential construction booms across Southeast Asia. North America and Europe, while mature, exhibit high value growth, largely due to stringent quality standards necessitating high-end PCE formulations and a strong commitment to sustainable building practices, including the increased use of supplementary cementitious materials (SCMs) which require specialized PCE compatibility. Emerging markets in Latin America and the Middle East and Africa (MEA) are showing promising growth trajectories, supported by rapid industrialization and diversification of their construction sectors away from conventional methods.

Segmentation trends highlight the dominance of the ready-mix concrete segment as the primary consumer, although the precast concrete market is experiencing the fastest growth rate driven by increased standardization and efficiency demands in building production. In terms of type, the Polycarboxylate Ether (PCE) segment maintains overwhelming supremacy due to its superior performance characteristics, chemical versatility, and ability to be engineered for specific performance targets compared to older generation superplasticizers. Continuous R&D investment is shifting focus towards bio-based and highly specialized PCE derivatives designed for niche applications like 3D printing concrete and deep-sea construction.

User queries regarding the intersection of Artificial Intelligence (AI) and the Polycarbonate Superplasticizer Market predominantly center on optimization, quality control, and predictive performance modeling. Users are keen to understand how AI algorithms can revolutionize the formulation process, moving beyond empirical testing to predicting the optimal PCE dosage and structure required for a specific concrete mix design, thus reducing waste and development time. Concerns often revolve around the high initial investment required for integrating sophisticated machine learning models into traditional chemical manufacturing and construction processes, alongside the necessity for high-quality, vast datasets covering diverse cement, aggregate, and environmental variables to train effective AI models. Expectations are high regarding AI's ability to enhance supply chain efficiency, manage real-time quality assurance during concrete mixing, and develop novel, highly efficient polymer structures using generative design techniques.

The Polycarbonate Superplasticizer Market is powerfully influenced by the dynamic interplay between persistent demand drivers, material cost restraints, and emerging sustainability opportunities. Key drivers include accelerating global construction activity, especially in infrastructure and housing sectors, coupled with regulatory mandates promoting high-strength and durable concrete structures which necessitate advanced chemical admixtures. These drivers maintain continuous upward pressure on market growth, ensuring PCEs remain indispensable components in high-specification concrete production worldwide. The immediate impact forces currently shaping the market involve intense competition among regional manufacturers, fluctuating feedstock costs (driven by oil price volatility), and the increasing adoption of automated construction techniques like 3D printing which rely on specially formulated, flowable concrete mixes.

Restraints largely center around the volatility and increasing cost of petrochemical-derived raw materials, particularly ethylene oxide derivatives, which impacts manufacturing profitability and pricing stability for end-users. Additionally, market penetration in smaller, rural construction projects remains challenging due to the higher perceived cost of PCEs compared to conventional alternatives, despite their long-term performance benefits. The lack of standardized testing protocols across diverse regional markets also occasionally hinders rapid global product acceptance and necessitates tailored regional formulations, adding complexity to R&D and manufacturing processes.

Significant opportunities exist in the development of next-generation PCE formulations tailored for low-carbon cement production (e.g., geopolymer concrete and alternative binders), addressing the industry's push towards decarbonization. Furthermore, the expansion of the precast concrete sector globally, driven by efficiency and speed, offers a fertile ground for high-end PCE applications demanding high early strength. The emergence of specialized applications, such as self-compacting concrete (SCC) and concrete for extreme environments (e.g., marine or high-temperature settings), promises high-margin niche market expansion for technologically advanced players. The critical impact forces necessitate continuous technological innovation and strategic supply chain management to maintain competitive advantage.

The Polycarbonate Superplasticizer Market segmentation provides a granular view of market dynamics based on chemistry, application, and end-use, reflecting varied demands across the global construction industry. Understanding these segments is crucial for manufacturers to align their product portfolios with specific market needs, such as targeting the high-volume ready-mix sector with cost-effective PCEs or focusing on specialized formulations for the fast-growing precast segment demanding rapid strength development and excellent surface finish. The primary chemical classification, Polycarboxylate Ether (PCE), dominates due to its superior water reduction capability and flexibility in molecular structure modification, enabling tailored performance parameters crucial for modern construction challenges.

Application-based segmentation reveals that general construction applications, particularly residential and commercial building, account for the largest share, driven by urbanization trends and housing demands. However, infrastructure construction, encompassing roads, bridges, tunnels, and dams, represents a significant high-value segment where stringent durability and longevity requirements mandate the use of premium PCEs. The performance demands in infrastructure often drive technological advancements, as these projects require admixtures capable of extended slump retention in hot climates and high resistance to aggressive chemical environments, further solidifying the PCE market's reliance on high-tech solutions.

Geographically, while Asia Pacific leads in volume consumption, the distinct regulatory environments and material preferences in North America and Europe necessitate region-specific product development. Manufacturers are increasingly segmenting their R&D efforts to address factors such as the prevalence of fly ash or slag as SCMs in specific regions, which requires specialized PCE compatibility. This intricate segmentation confirms that market success hinges not only on basic functionality but also on the ability to customize formulations for compatibility with local cement chemistry, aggregate types, and specific project requirements.

The value chain for the Polycarbonate Superplasticizer Market begins with the upstream sourcing of crucial petrochemical raw materials, primarily ethylene oxide, methoxy polyethylene glycols (MPEG), acrylic acid, and various monomers. This upstream segment is highly sensitive to fluctuations in global oil and chemical commodity prices, necessitating rigorous risk management and long-term supply contracts for major manufacturers. Key activities in this stage include polymerization and synthesis, where these monomers are chemically processed to form the complex polycarboxylate ether polymer structures, a step requiring specialized chemical engineering expertise and capital-intensive reaction equipment.

The midstream involves the core manufacturing process, where the synthesized polymers are formulated into concentrated liquid or powder admixtures, often involving proprietary blending with defoamers, air-entraining agents, and retarders to create performance-specific products. Distribution channels play a vital role, encompassing both direct sales to large concrete producers (e.g., major ready-mix companies or large infrastructure project contractors) and indirect distribution through a network of specialized construction chemical distributors and regional agents who provide localized technical support and smaller batch sizes to diverse end-users. Direct distribution often guarantees tighter quality control and stronger client relationships for customized, high-volume products.

Downstream activities focus on application and integration, where the superplasticizers are introduced into the concrete mixing process either at the ready-mix plant or on the construction site. End-users require significant technical support for dosage optimization and mix design troubleshooting, making post-sales service a crucial differentiator in the competitive landscape. The effectiveness of the product is ultimately validated by construction engineers and quality control teams, emphasizing the need for robust product performance data and compliance with local building codes. The efficiency and quality of the distribution channel directly influence market penetration and customer satisfaction, particularly in regions with fragmented construction markets.

Potential customers for Polycarbonate Superplasticizers are predominantly large-scale entities within the construction materials and engineering sectors that require high-performance, durable, and highly flowable concrete mixes. The largest segment of buyers comprises ready-mix concrete producers who utilize PCEs daily to maintain consistent slump flow over long transportation distances and to meet the diverse strength requirements specified by contractors. These companies purchase in bulk volumes and prioritize cost-efficiency, reliable supply, and compatibility with their localized aggregate and cement sources. Their purchasing decisions are heavily influenced by the technical support provided by the superplasticizer supplier.

The second major group includes precast concrete manufacturers specializing in producing structural elements, pipes, railroad ties, and architectural panels off-site. For precast operations, PCEs are critical for achieving rapid demolding times (high early strength), superior surface finish, and highly controlled dimensional accuracy. These customers demand specialized PCE formulations that accelerate hydration kinetics while maintaining fluidity for easy filling of complex molds, driving demand for premium, high-tech admixtures designed for quick cycling operations in manufacturing plants.

Furthermore, major infrastructure project contractors and government agencies responsible for mega-projects (dams, bridges, nuclear facilities) constitute a high-value customer base. These projects mandate concrete that offers extreme durability, low permeability, and resistance to harsh environmental exposure, often requiring PCEs that can handle high volumes of Supplementary Cementitious Materials (SCMs). While they may not be the direct buyers (as the ready-mix supplier is), their specifications dictate the required quality and type of superplasticizer used, making them influential decision-makers in the market procurement cycle.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.6 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Sika AG, Fosroc International, Arkema SA, GCP Applied Technologies, Mapei SpA, W. R. Grace & Co., Kao Corporation, Cico Technologies, CEMEX S.A.B. de C.V., KAO Chemicals, Rhein Chemie Additives, Shandong Jufu Chemical Technology, KZJ New Material, KRONOS Worldwide, Boral Limited, Pidilite Industries, Chemsil Silicones, Shanxi Kaidi Chemical, Jiangsu Bote |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Polycarbonate Superplasticizer Market is dominated by advanced polymer synthesis methods focused on tailoring the molecular architecture of Polycarboxylate Ethers (PCEs). Key technological advancements revolve around controlling the length and density of the side chains, as well as the charge density of the main polymer backbone, allowing manufacturers to fine-tune the admixture’s performance characteristics, such as optimizing slump retention duration or achieving higher water reduction ratios. These proprietary synthesis techniques are crucial for maintaining competitive advantage and addressing the complex interaction between superplasticizers and increasingly varied cement chemistries, including those incorporating high volumes of supplementary cementitious materials like fly ash, slag, and limestone filler.

A critical technology area is the development of multi-functional PCEs, which combine superior dispersion capabilities with other performance benefits, such as controlled setting time or enhanced air control. This involves complex copolymerization techniques where different monomers are introduced to the polymer chain to achieve synergistic effects. Furthermore, the technology landscape is being shaped by digitalization, utilizing high-throughput screening and computational chemistry (including AI/Machine Learning models) to rapidly test thousands of potential polymer structures in virtual environments, significantly accelerating the traditional R&D cycle and leading to the discovery of highly efficient, third-generation PCEs that require ultra-low dosages.

In terms of production and application, encapsulation technology is gaining traction, particularly for powdered superplasticizers used in dry-mix mortars and specialty concrete applications, ensuring long shelf life and stable performance upon mixing. Quality assurance technologies, including advanced rheometers and calorimetry tools, are essential for characterizing the performance of new formulations and ensuring batch-to-batch consistency. The push towards sustainable manufacturing is also driving process innovation, focusing on utilizing renewable or bio-based feedstocks where feasible, reducing energy consumption during polymerization, and optimizing chemical yield to minimize waste throughout the production lifecycle.

Polycarboxylate Ether (PCE) superplasticizers primarily rely on steric hindrance (physical separation) for particle dispersion, offering superior water reduction (up to 40%) and better slump retention compared to Sulfonated Naphthalene Formaldehyde (SNF), which relies mainly on electrostatic repulsion.

PCEs allow for significantly lower water-to-cement ratios, which drastically reduces concrete porosity and permeability. This results in concrete with enhanced long-term durability, higher compressive strength, and improved resistance to chemical attack and freeze-thaw cycles.

The Asia Pacific (APAC) region currently dominates the Polycarbonate Superplasticizer market in terms of volume consumption, driven by extensive infrastructure and urbanization projects in major economies like China and India.

PCE compatibility varies depending on the cement chemistry and the presence of Supplementary Cementitious Materials (SCMs). While generally compatible, specialized PCE formulations are often required to optimize performance when high percentages of fly ash, slag, or specialized binders are used.

Key drivers include global infrastructure modernization efforts, increasing regulatory demand for high-strength and long-lasting concrete structures, rapid adoption of automated construction methods (like 3D printing), and the continuous push towards sustainable, low water-demand concrete mixes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.